Last Week’s Reports

U.S. Election

In the 2024 U.S. election, Donald Trump made a historic comeback, securing the presidency once again. His victory was marked by a decisive win over Vice President Kamala Harris, capturing 312 electoral votes.

The election also saw the Republicans gaining control of the Senate, with 53 seats compared to the Democrats’ 46, flipping several key seats. In the House of Representatives, the Republicans maintained a majority with 213 seats, while the Democrats held 202 seats. This election has been one of the most remarkable in recent history, with significant implications for the political landscape in the United States.

Image source: cnn.com

Economic Reports

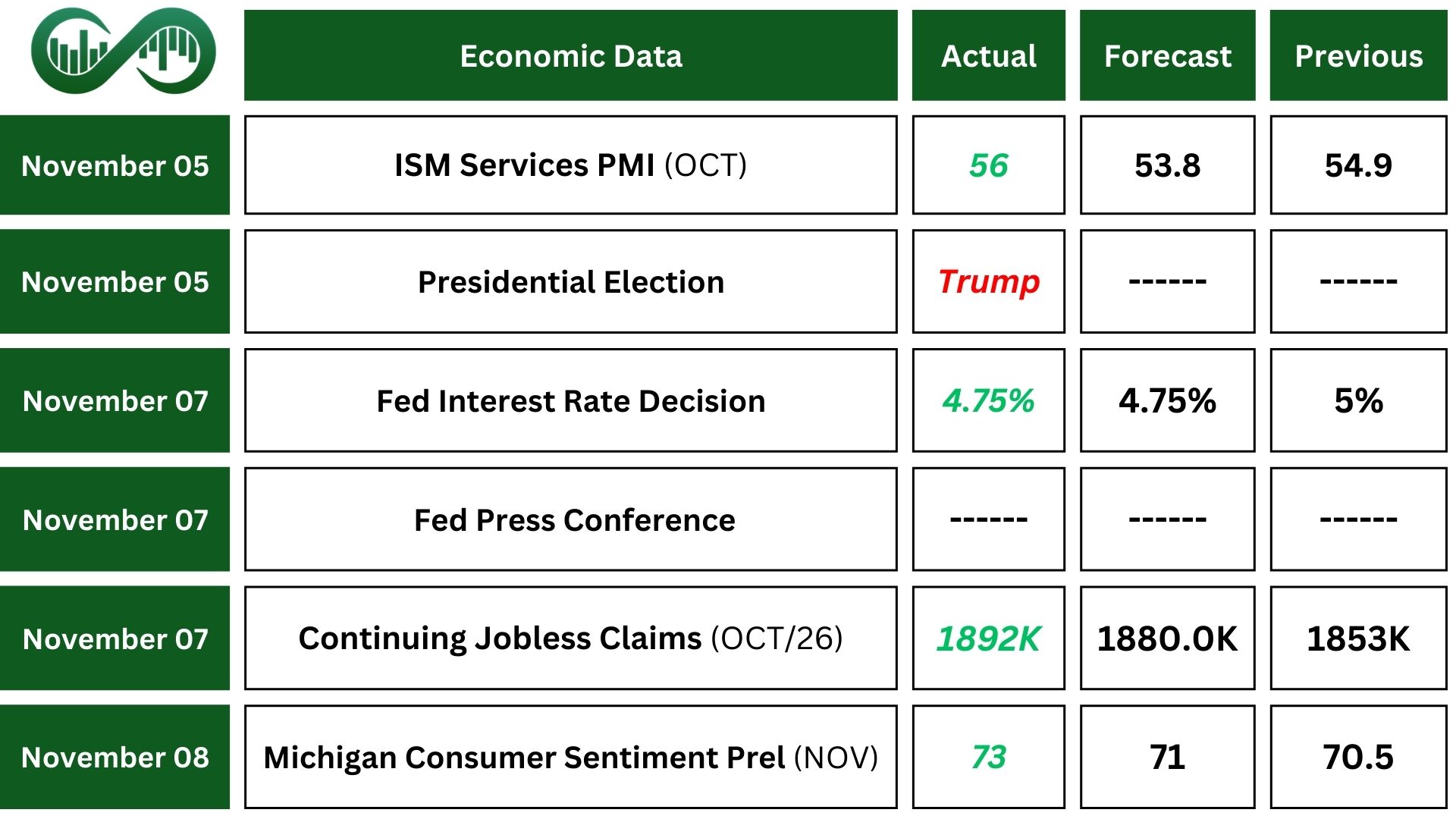

The ISM Services PMI increased to 56 in October, beating forecasts. Key drivers included significant boosts in the Employment and Supplier Deliveries indexes, while the Business Activity and New Orders indexes dropped. Supplier Deliveries Index indicated slower delivery performance. Increased concerns over political uncertainty and impacts from hurricanes and port labor issues.

The FOMC has lowered the federal funds rate target range by 0.25 percentage points to 4.5-4.75 percent. They will also keep reducing their holdings of Treasury securities, agency debt, and mortgage-backed securities.

On November 7, Federal Reserve Chair Jerome Powell cited strong economic conditions, easing inflation at 2.1%, and a stable labor market. Powell highlighted that further policy changes would depend on economic and inflationary trends. He also noted continued reductions in securities holdings, resilient consumer spending, and improved supply conditions. Despite some weakness in the housing sector, labor market conditions remain solid, with a low unemployment rate of 4.1% in October.

Powell assured that the Fed’s monetary policy would adapt to evolving economic conditions, aiming for a balanced approach to support sustainable growth and stable prices. He also addressed the potential impact of Donald Trump’s election victory on monetary policy, emphasizing the Fed’s independence from political influence.

In November, Michigan Consumer Confidence in the U.S. saw an increase, rising to 73 points from 70.50 in October. Means people are more likely to spend money, which can drive economic growth. Higher consumer spending can lead to increased production, job creation, and overall economic expansion.

Michigan 5-Year Inflation Expectations also climbed to 3.10% from 3% in October. When inflation expectations rise, consumers and businesses might anticipate higher prices in the future, leading them to spend or invest more now, which can drive up current inflation.

Earning Reports

Palantir

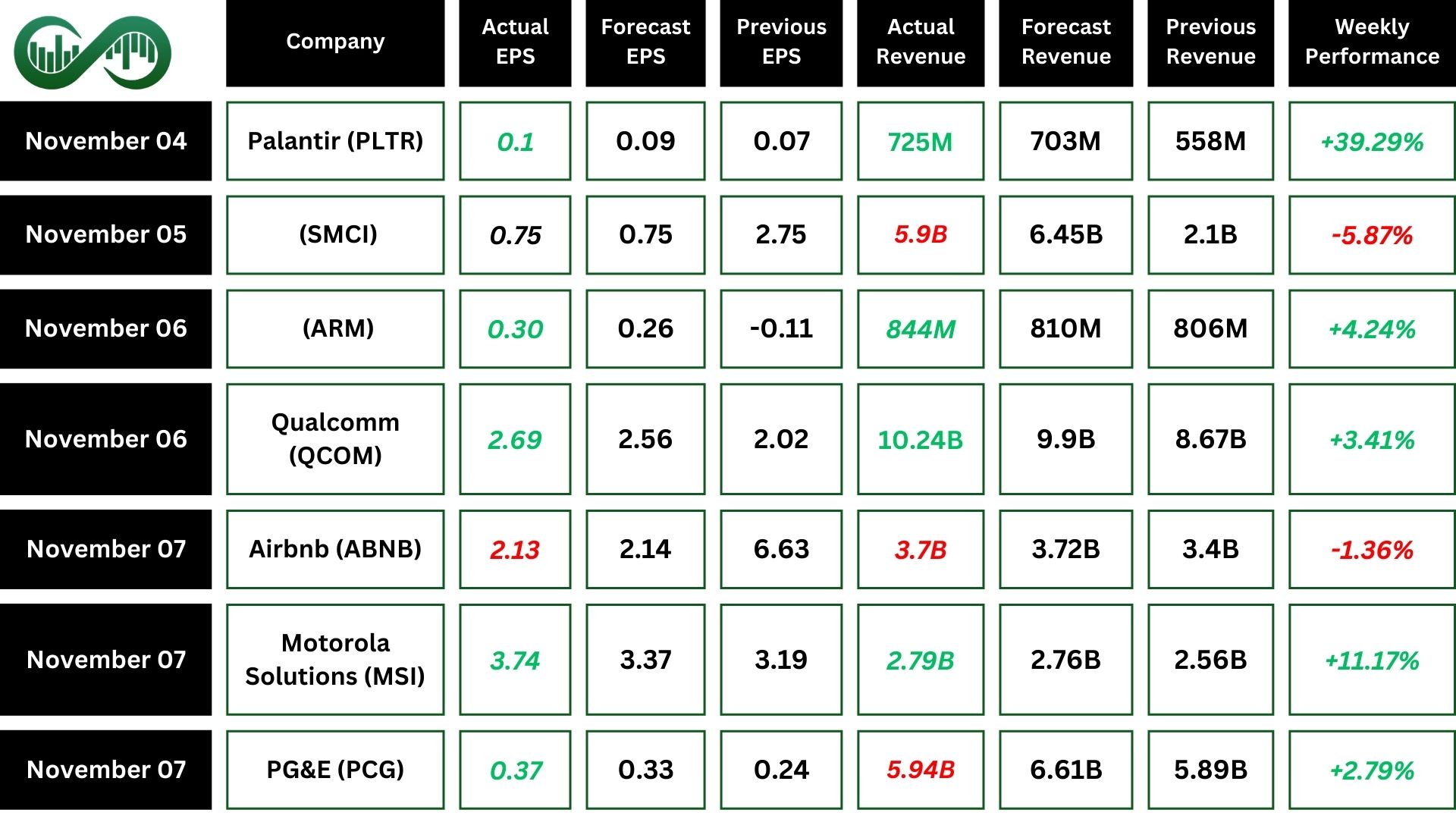

Palantir (PLTR) Technologies reported impressive 3Q earnings. The company’s revenue grew by 30% year-over-year to $726 million, surpassing expectations. U.S. revenue saw an even stronger growth of 44% year-over-year. Palantir’s net income was $143.5 million, up from $71.5 million in the same quarter last year.

The company also raised its full-year revenue guidance to $2.805 billion to $2.809 billion, reflecting confidence in continued growth driven by high demand for its AI solutions.

PLTR showed an impressive surge of 39% after the earnings report.

Super Micro Computer

Super Micro Computer (SMCI) reported Q1 earnings, showing a solid performance despite some challenges. The company’s revenue was $5.9 billion, slightly below the forecasted $6.45 billion. The net sales fell short of the previous guidance range of $6 billion to $7 billion.

However, the earnings per share (EPS) came in at $0.75, meeting the forecasted EPS. The strong demand for AI infrastructure significantly drove the year-over-year growth. Nonetheless, SMCI faced delays in new-generation GPU chips and some governance issues, which impacted their revenue.

However, the revenue guidance for the December quarter fell short of expectations, affecting investor sentiment.

ARM

In Q2 of the fiscal year ending 2025, Arm Holdings (ARM) reported total revenue of $844 million, a 5% increase YoY and above forecasts. Also,Non-GAAP earnings per share were $0.30, surpassing estimates.

The company saw a significant 23% rise in royalty revenue, driven by the adoption of Armv9 and the recovery of the smartphone market. Despite these strong results, Arm’s stock fell slightly in after-hours trading due to a cautious revenue outlook for the next quarter.

The company experienced a 15% decline in license and other revenue due to fluctuations in the timing and size of high-value license agreements.Additionally, the cautious revenue outlook for the next quarter also impacted investor sentiment, causing a slight drop in stock value after the earnings announcement.

Airbnb

Airbnb (ABNB) Q3 2024 earnings report revealed revenue and earnings per share were slightly below expectations. Although, the company demonstrated solid growth with a 10% increase in revenue and higher gross booking value. Revenue increased to $3.7 billion and net income of $1.4 billion, resulting in a 37% net income margin.

The 123 million nights and experiences booked, an 8% increase. App bookings rose by 18%, accounting for 58% of nights booked, and host cancellations reduced by almost 30% compared to the previous year.

Despite this growth, Airbnb faces challenges such as regulatory hurdles in key markets like New York City. The company anticipated margin compression in Q4 2024. ANBN price dropped about 9% after earnings were released.

Motorola Solutions

Motorola Solutions (MSI) reported strong Q3 2024 earnings. The company reported record revenue of $2.79 billion, up 9%. Non-GAAP EPS was $3.74, reflecting a 17% increase. Operating cash flow reached $759 million, and the company ended the quarter with a cash position of $2.1 billion.

Also, the company saw growth in both its Products and Systems Integration segment (11%) and Software and Services segment (7%). Operating margins expanded for the ninth consecutive quarter, and GAAP operating earnings reached $711 million. Additionally, MSI raised its full-year revenue and earnings guidance, reflecting strong business momentum and confidence in continued growth.

Indices

Indices’ Weekly Performance:

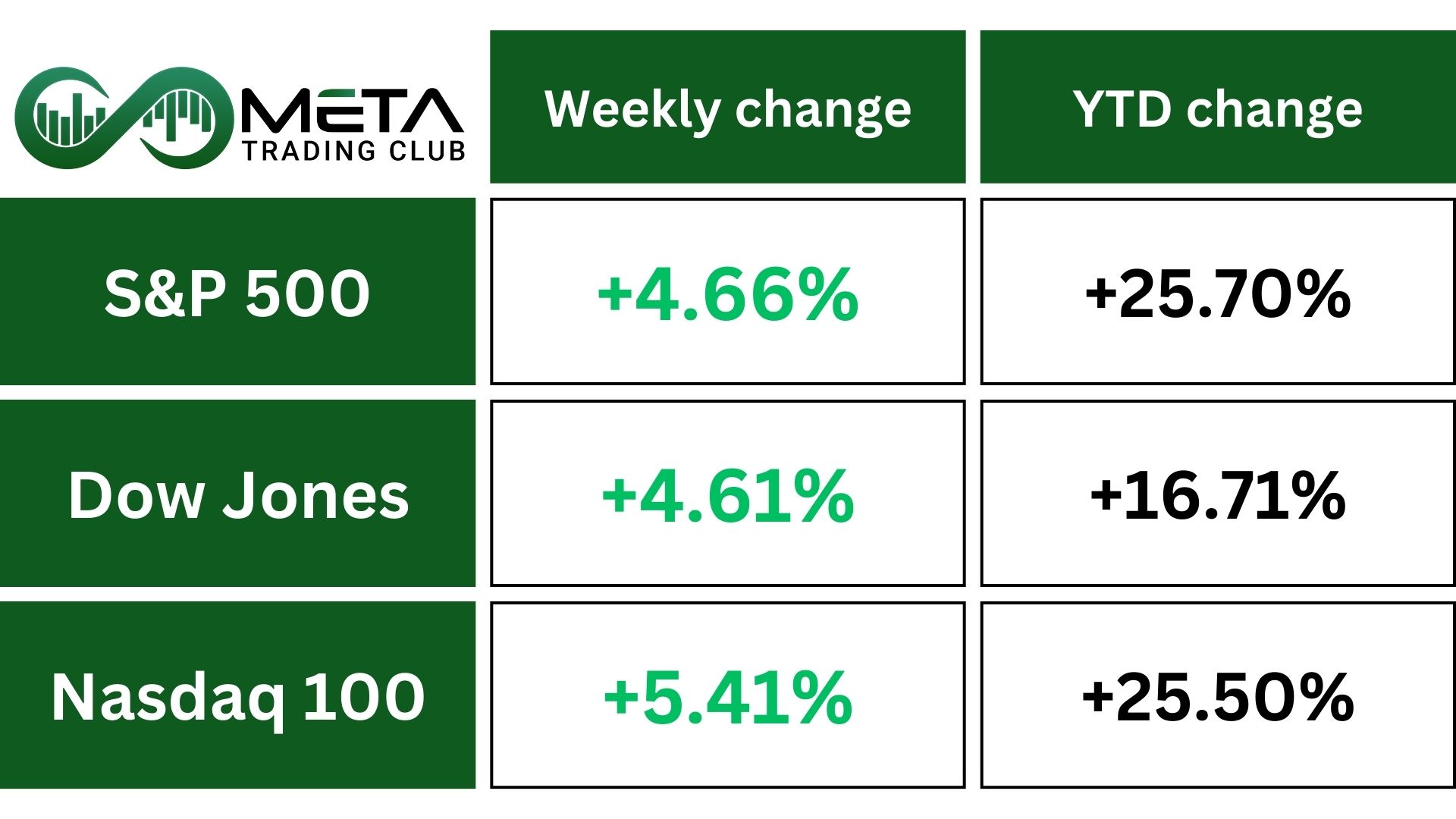

US stocks rallied last week, driven by optimism surrounding Donald Trump’s victory and a supportive interest rate cut from the Federal Reserve.

For the week, the S&P 500 and Dow are each up 4.7%, their best performance since November 2023, while the Nasdaq leads with a 5.9% gain. The Dow soared above 44,000 for the first time and the S&P 500 broke above the 6,000 mark.

Tesla’s stock surged by 29%, pushing its market capitalization past $1 trillion. Axon Enterprises jumped 27% after raising its revenue guidance. The gains were underpinned by the Federal Reserve’s 0.25% interest rate cut, which Fed Chair Jerome Powell said demonstrated confidence in the economy’s strength.

The S&P 500 index is currently in an ascending channel, indicating a bullish trend. If this trend continues, the target price could reach 6100 and 6150. However, if the market becomes overbought, the price might fall and fill the gap between 5860 and 5790.

Stocks

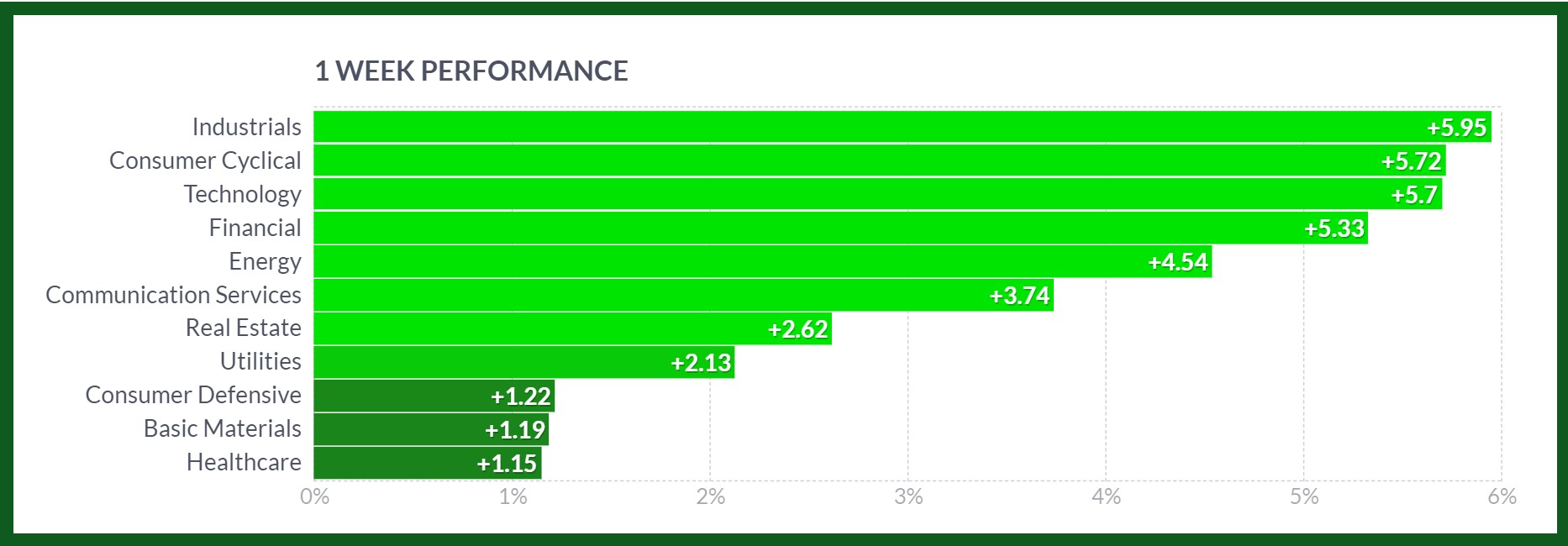

Stock Market Sector’s Weekly Performance:

Source: Finviz

Last week, the US stock market sectors showed varied performances. The industrial sector led with a 5.95% increase, driven by positive economic data and infrastructure spending. The consumer cyclical sector rose by 5.72%, helped by strong retail sales and consumer confidence. The technology sector saw a 5.70% gain due to positive sentiment of Trump’s victory in the election. Financials gained 5.33% on positive interest rate sentiment.

The recent victory of Donald Trump in the US presidential election has also played a significant role in these market movements. Trump’s win has surged trader’s confidence, particularly in sectors like energy, financials, and industrials, due to his pro-business policies, promises of deregulation, and potential tax cuts.

Stock Market Weekly Performance:

Source: Finviz

Top Gainers in the S&P 500

This week, the S&P 500 saw some significant movements among its constituents. Here are the mega and large cap top gainers:

- Tesla, Inc. (TSLA): Surged 29.01% due to Elon Musk’s big bet on Trump’s victory in the election and positive investor sentiment around electric vehicle demand.

- Oracle Corporation (ORCL): Rose 11.31%, driven by continued investment in cloud infrastructure positions it well for sustained growth in the dynamic software industry.

- Morgan Stanley (MS): Up 10.85%, due to receive approval to launch a local futures unit in china.

- Salesforce, Inc. (CRM): Jumped 9.24%, driven by CRM’s plan to hire 1,000 people to expand its workforce to support the growing demand for AI solutions.

- NVIDIA Corporation (NVDA): Surged 9.03%, fueled by positive market sentiment after joining Dow Jones index.

- Broadcom Inc. (AVGO): Rose 8.71%, after announcing VMware cloud foundation enhancements to boost AI and cybersecurity.

Tesla

Elon Musk made a big bet on Donald Trump winning the election, and it paid off. After Trump’s win, Tesla’s stock jumped over $320, rising by 29% in just one week. This increase pushed Tesla’s market value above $1 trillion.

Tesla also started offering leasing options for their new Cybertruck, giving more people a chance to drive this exciting new electric vehicle.

TSLA recently broke upwardly out of its ascending channel, indicating a potential bullish trend. If this breakout is valid, the target price could reach its all-time high around $416. Additionally, the Fibonacci level around $511 could also be a target if the momentum continues.

However, if this breakout turns out to be a fake one, the price might fall back to the midline of the channel around $290.

Commodity

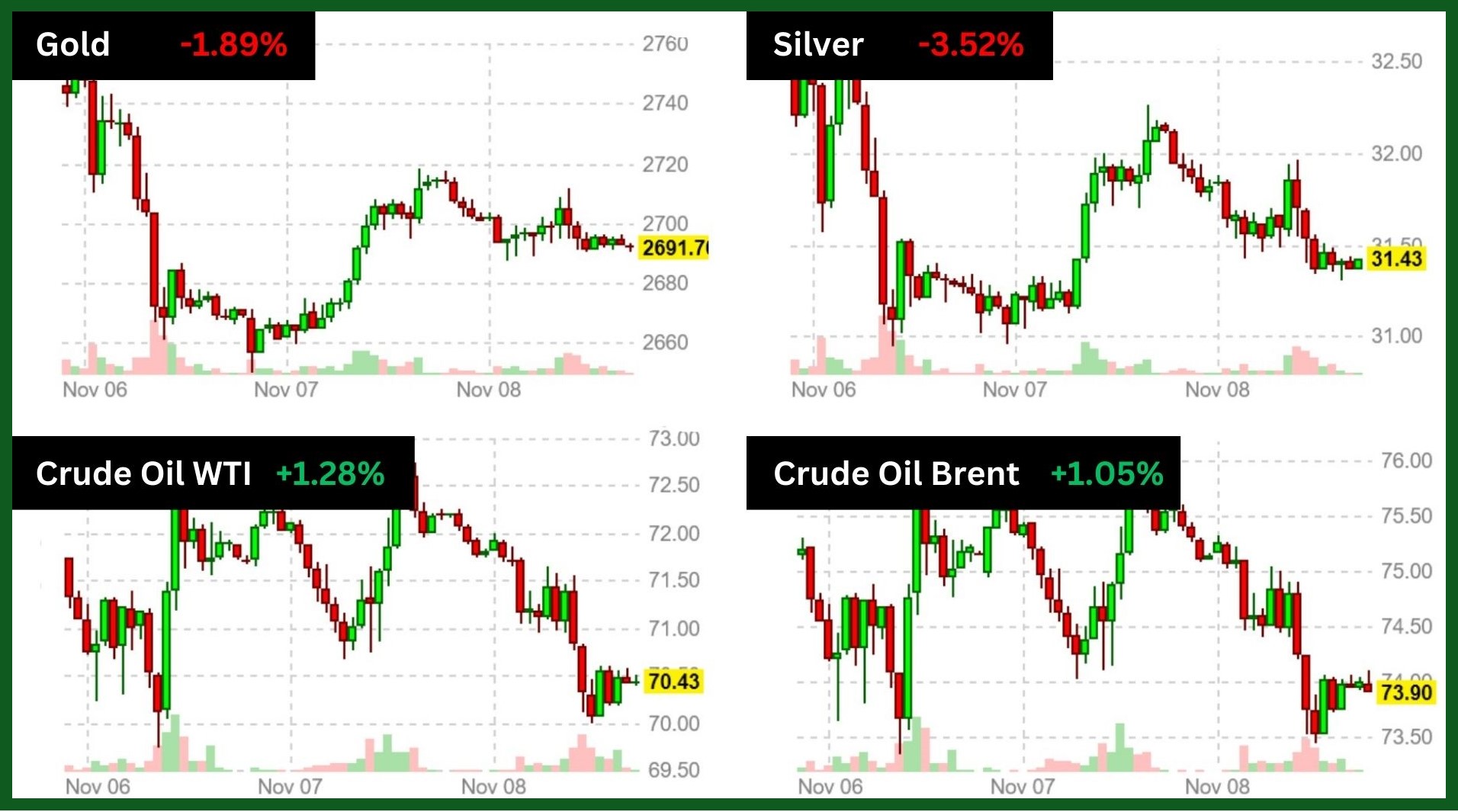

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

After Donald Trump’s victory in the 2024 U.S. presidential election, gold prices experienced a significant decline. The price of gold fell by about 3% to around $2,673 per ounce due to a stronger U.S. dollar and rising bond yields. Although, gold finished the week with 1.89% drop.

Traders were concerned that Trump’s proposed policies, such as higher tariffs, could reignite inflation, leading to higher interest rates and making gold less attractive.

The price of XAU/USD recently broke down from its black ascending trend line and experienced a pullback, signaling a potential bearish trend. If this breakout is genuine, the price has a chance to continue falling towards support zones around 2645 or even lower to 2605. However, if the price does not fall below 2605, it could rebound to the ascending black trend line, creating a trading range between the support and resistance levels.

On Friday, WTI crude oil futures dropped 2.7%, settling at $70.38 per barrel. The decline was due to reduced fears about prolonged supply issues from Hurricane Rafael in the U.S. Gulf of Mexico and disappointment with China’s economic stimulus efforts.

However, expectations of tighter U.S. sanctions on Iran and Venezuela provided some support. Despite Friday’s drop, the oil benchmark still recorded a 1% gain for the week.

Forex

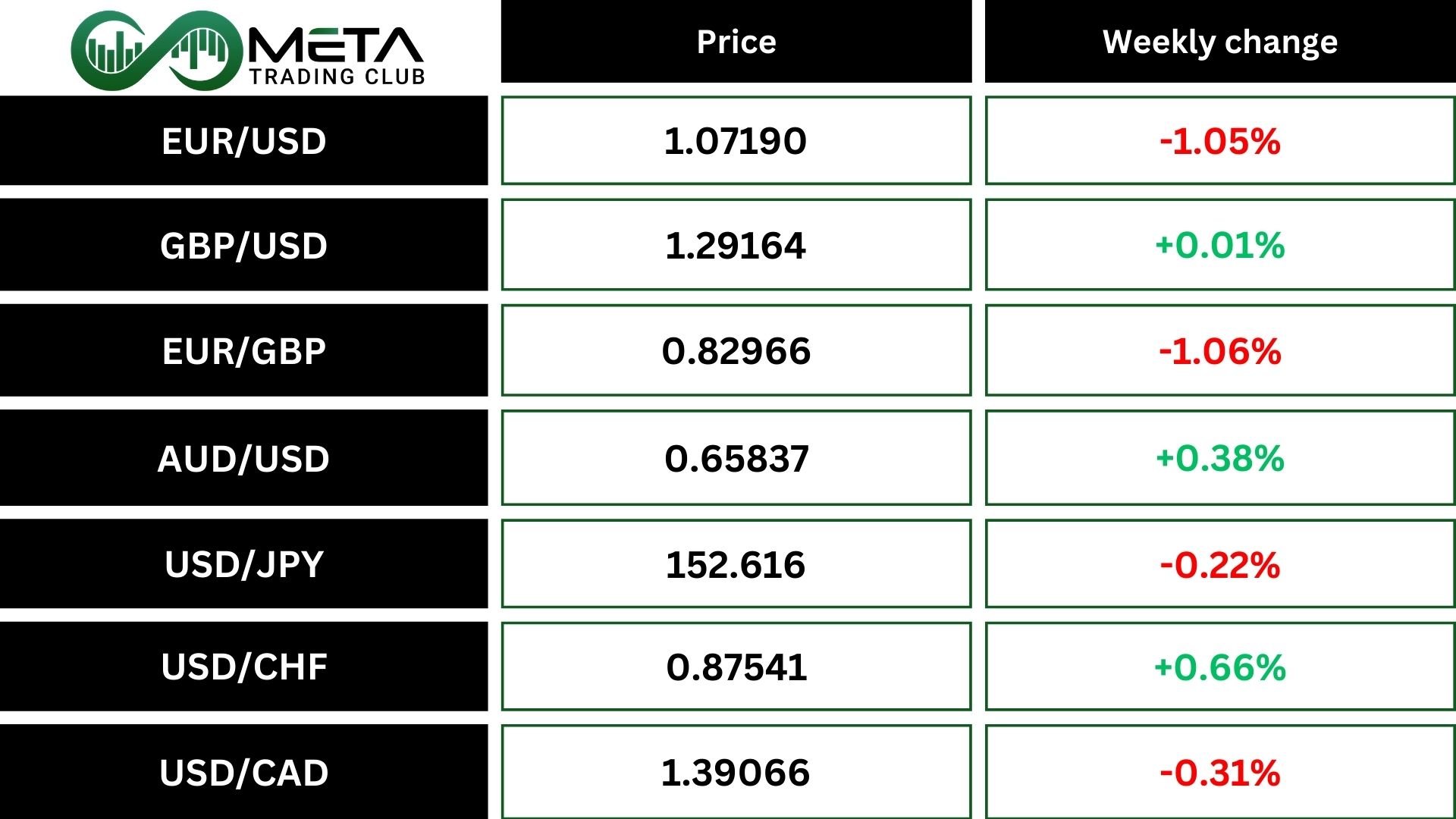

Weekly Performance of Major Foreign Exchange Pairs:

EUR/USD faced significant selling pressure and continued its downtrend. The pair reached the 1.0730 region due to renewed buying pressure on the US Dollar. The US Dollar resumed its upward trend following Donald Trump’s victory in the US presidential election. Trump’s win has bolstered the long-term outlook for the US Dollar, while the Euro has declined due to threats of Trump-imposed tariffs, German political uncertainty, and concerns over the Eurozone’s economic outlook.

The US Dollar Index (DXY) rebounded to nearly 104.70 after a brief dip to 104.20, following a four-month high of 105.50 post-election

AUD/USD managed to recover and halt a multi-week bearish trend, with significant Australian economic reports including the Westpac Consumer Confidence Index and the Australian labor market report.

Crypto

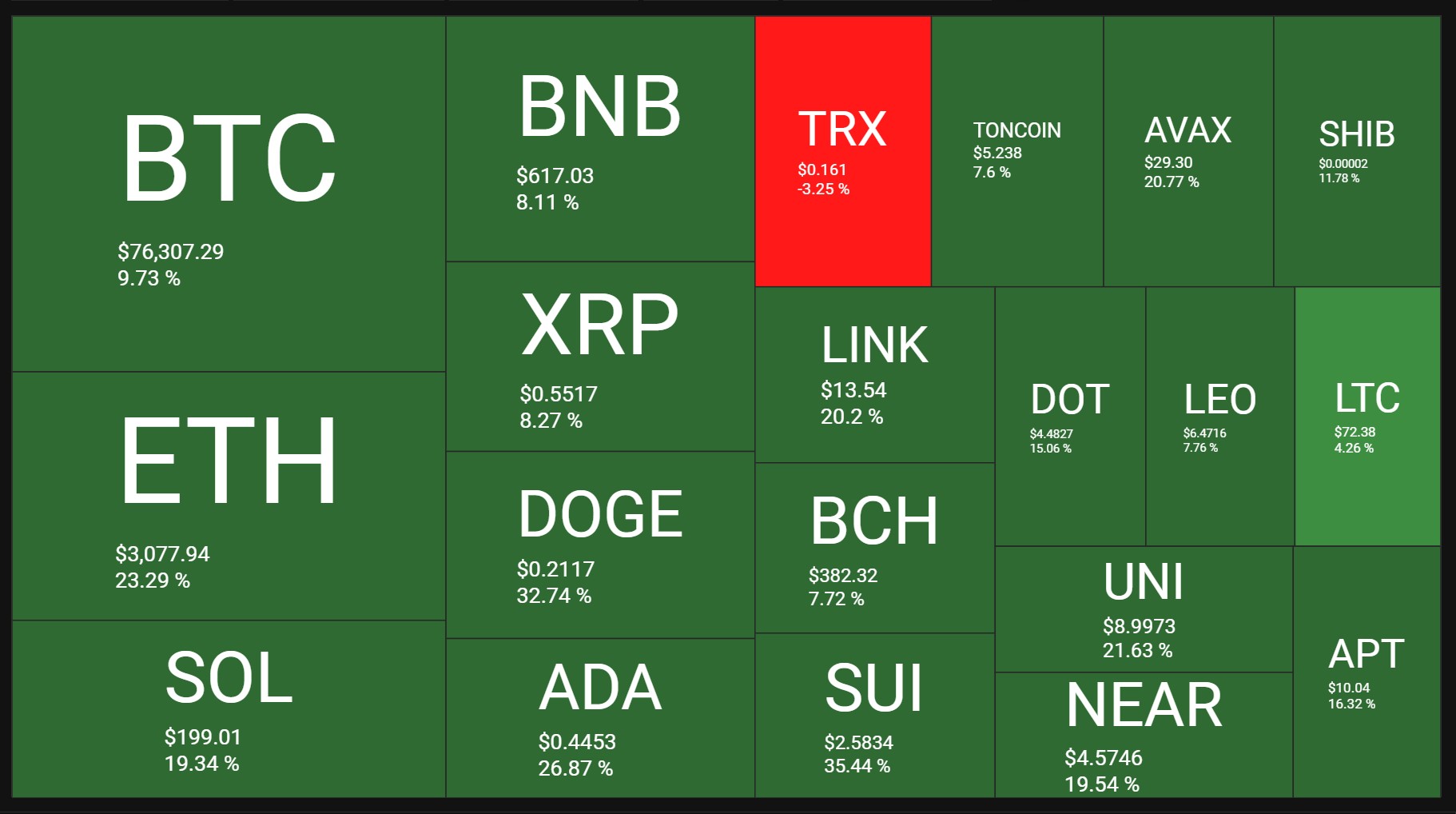

Crypto Market Weekly Performance:

Source: quantifycrypto

The past week has been largely positive for the cryptocurrency market, with significant gains observed in several major and minor cryptocurrencies. The overall market sentiment appears to be bullish, driven by Trump’s victory in election 2024.

Trump is planning to establish a strategic Bitcoin reserve, ensuring that the US government never sells a single coin and even embarks on a buying spree to acquire 1 million Bitcoin over the next five years. Additionally, Trump has pledged to fire Securities and Exchange Commission Chair Gary Gensler “on day one.” More broadly, he aims to collaborate with Congress to pass crypto-friendly regulations that will strengthen the industry and position it ahead of international competition.

Bitcoin recently broke upward from its ascending channel and experienced a pullback, which is considered a bullish signal. If this breakout is triggered, the price could rise as much as the channel width, with a target around 86,000. This rise could happen now or after a price correction to the green support around 74,000.

However, if the breakout fails, the price might fall below the green support line and test the midline of the ascending channel. In this case, BTC would still maintain its uptrend as long as the price remains above 66,835.

Next Week’s Outlook

Economic Events

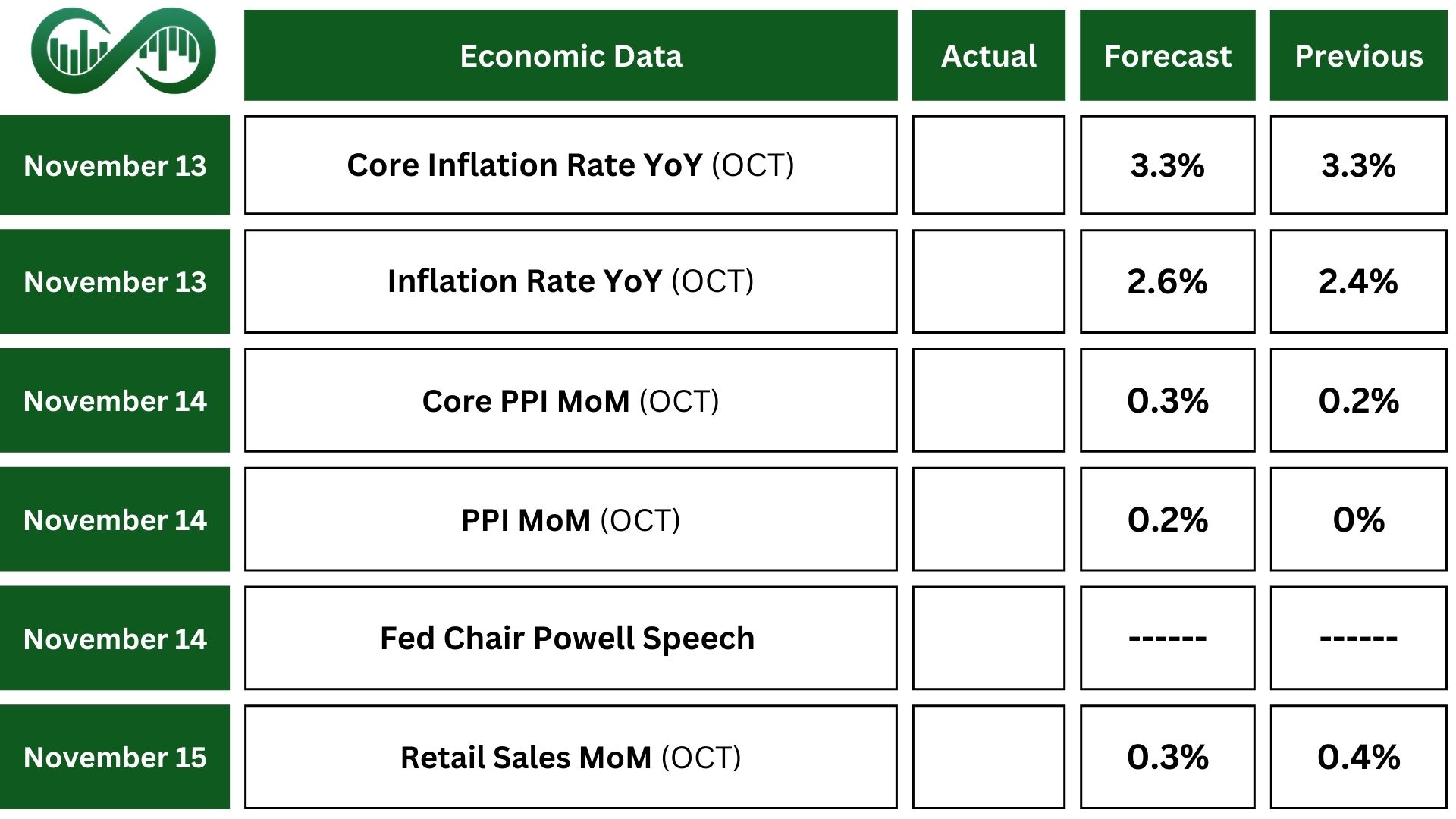

In the US, the upcoming CPI report is important. Forecasts suggest the annual inflation rate may increase to 2.6% from September’s 2.4%, with the monthly rate steady at 0.2%. Core CPI is expected to stay the same, with an annual rate of 3.3% and a monthly rate of 0.3%.

Also, for the PPI, a 0.2% rise is anticipated, lifting the annual rate to 2.3% from 1.8%.

Furthermore, retail sales are projected to grow by 0.3%, slightly less than September’s 0.4%, while industrial production may have contracted by 0.4%.

Traders will also watch for comments from Federal Reserve officials, including Chair Jerome Powell, for clues about December’s policy outlook.

Earning Events

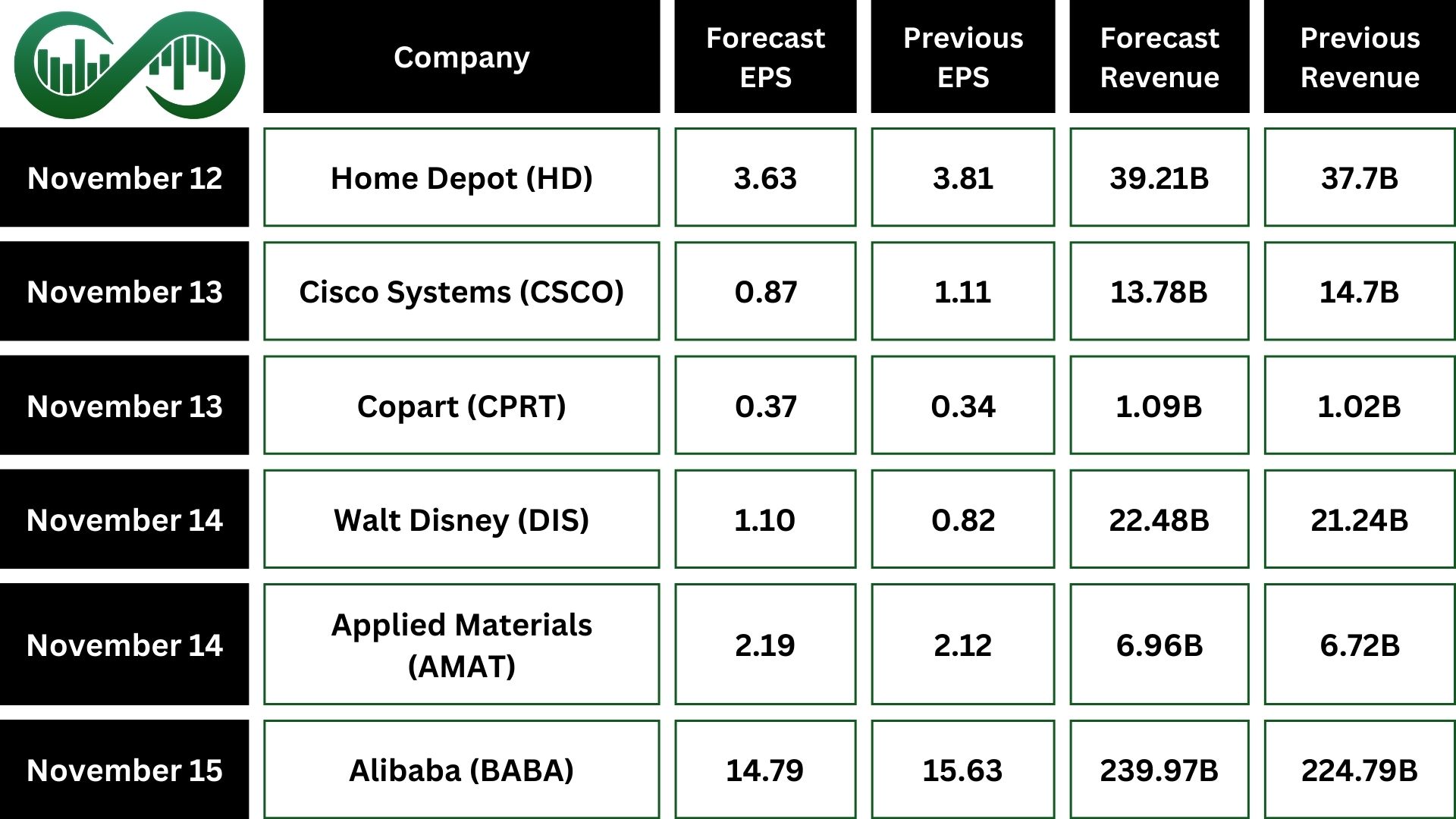

In corporate news, earnings season continues with Home Depot (HD), Cisco Systems (CSC), Alibaba (BABA), Walt Disney (DIS), and Applied Materials (AMAT) set to release their quarterly results.

In corporate news, earnings season continues with Home Depot (HD), Cisco Systems (CSC), Alibaba (BABA), Walt Disney (DIS), and Applied Materials (AMAT) set to release their quarterly results.