What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

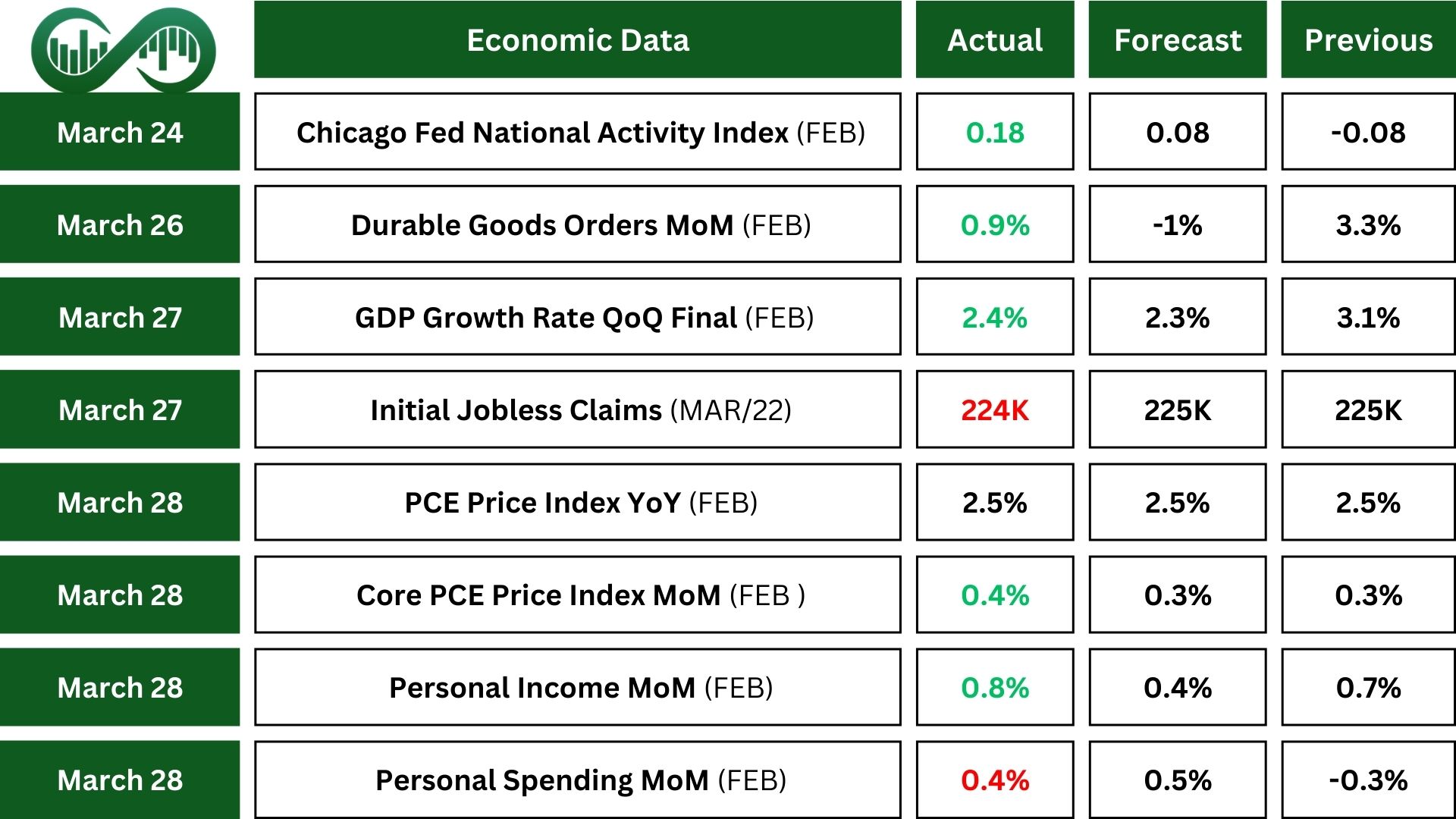

In February, the Chicago Fed National Activity Index rose to 0.18 from -0.08 in January, signaling above-average economic growth.

The S&P Global US Manufacturing PMI fell to 49.8 in March, showing a contraction as output and new orders slowed, while employment dropped for the first time since October. Despite rising costs, business sentiment remained strong. In contrast, the US Services PMI increased to 54.3, driven by better demand and business inflows, though concerns over federal policies and tariffs impacted confidence.

Also, Durable Goods Orders increased 0.9%, defying expectations of a 1% decline. This follows a strong 3.3% rise in January, with the growth primarily driven by transportation equipment, which rose $1.4 billion (1.5%). These figures highlight resilience in manufacturing demand.

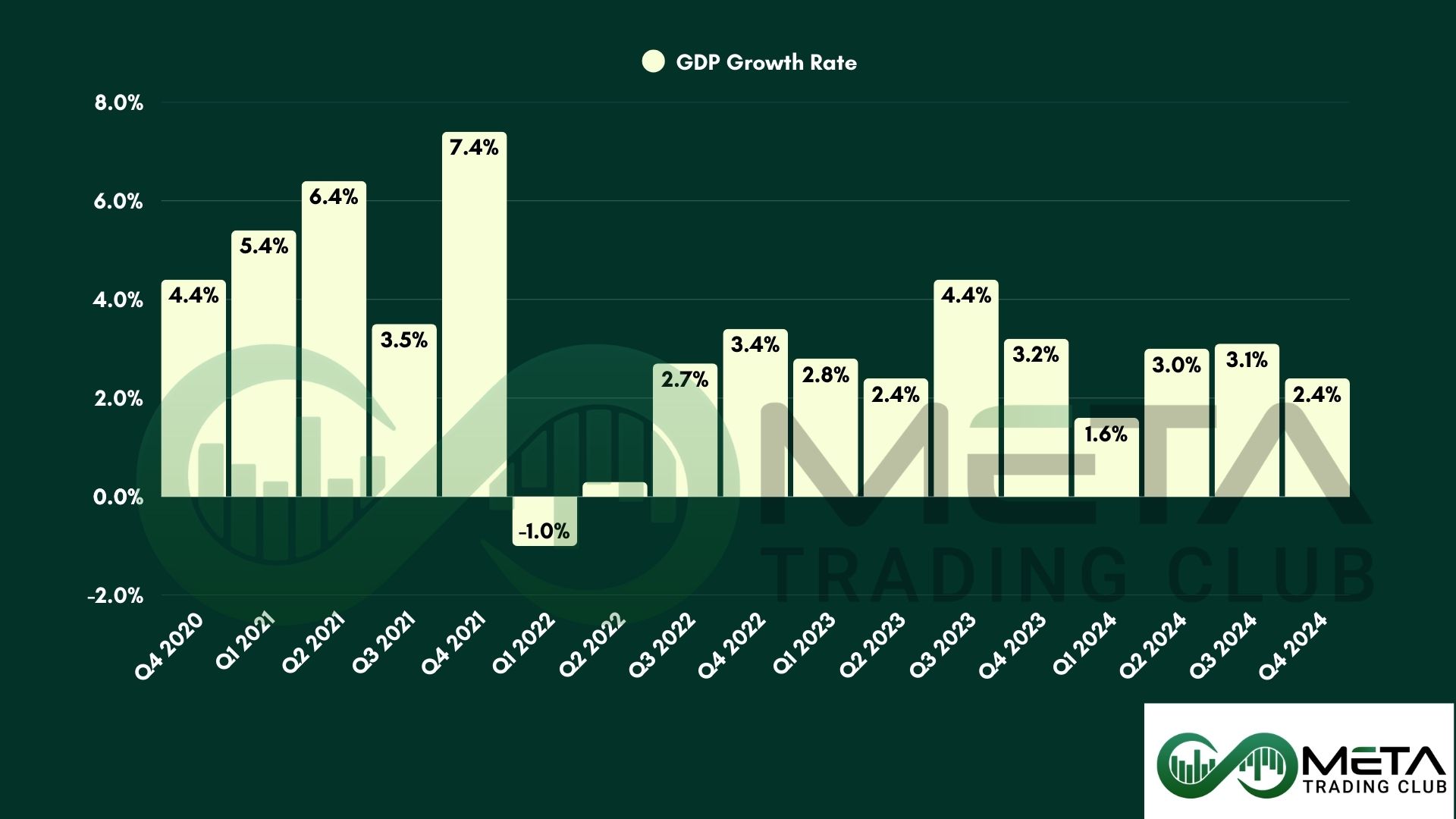

The U.S. economy grew by 2.4% in Q4 2024, slightly surpassing previous estimates but slower than the 3.1% growth in Q3. Increased consumer and government spending drove growth, while reduced investment and lower imports tempered the overall rise. Annual GDP Growth reached 2.8%, reflecting stability that may boost investor confidence.

U.S. jobless claims fell to 224K for the week ending March 22, slightly below expectations. Also, Continuing claims dropped, highlighting the job market’s strength despite tight monetary policies and earlier economic challenges.

In February, the PCE index rose 0.3%, matching January’s rate. Core PCE, excluding food and energy, increased by 0.4%, the highest rise since early 2024. Year-over-year, overall PCE prices stayed steady at 2.5%, while core prices rose to 2.8%.

Personal income surged by 0.8%, its largest monthly gain in over a year, significantly exceeding expectations. Personal spending rebounded 0.4% after a January decline but came in slightly below forecasts. These figures reflect strong economic activity with steady inflation pressures.

Earnings Reports

Cintas

Cintas (CTAS) reported robust fiscal 2025 third-quarter results, with revenue increasing by 8.4% to $2.61 billion, driven by organic growth of 7.9%.

Operating income grew 17.1%, benefiting from a $15 million gain on asset sales. Net income climbed 16.6% to $463.5 million, and diluted EPS surged 17.7% to $1.13.

The company also raised its annual revenue and EPS guidance, reflecting strong operational performance despite foreign currency headwinds.

CTAS stock experienced a notable 6.5% rise following the release of its strong fiscal 2025 third-quarter earnings report. The impressive results, including revenue growth, improved margins, and raised guidance.

Paychex

Paychex (PAYX) reported solid third-quarter fiscal 2025 results, with revenue rising 5% to $1.5 billion and adjusted operating income increasing 9% to $708.5 million.

Diluted earnings per share grew 4% to $1.43, while adjusted EPS rose 8% to $1.49. Meanwhile, during the first nine months of fiscal 2025, Paychex returned $1.2 billion to shareholders through dividends and stock buybacks, maintaining strong financial liquidity.

Also, Paychex announced a definitive agreement to acquire Paycor HCM, expected to close in April 2025, positioning the company for future growth in human capital management.

PAYX stock climbed 5.3% following the release of its strong earnings report. The positive market reaction reflects investor confidence in the company’s solid revenue growth, improved margins, and strategic acquisition plans.

Indices

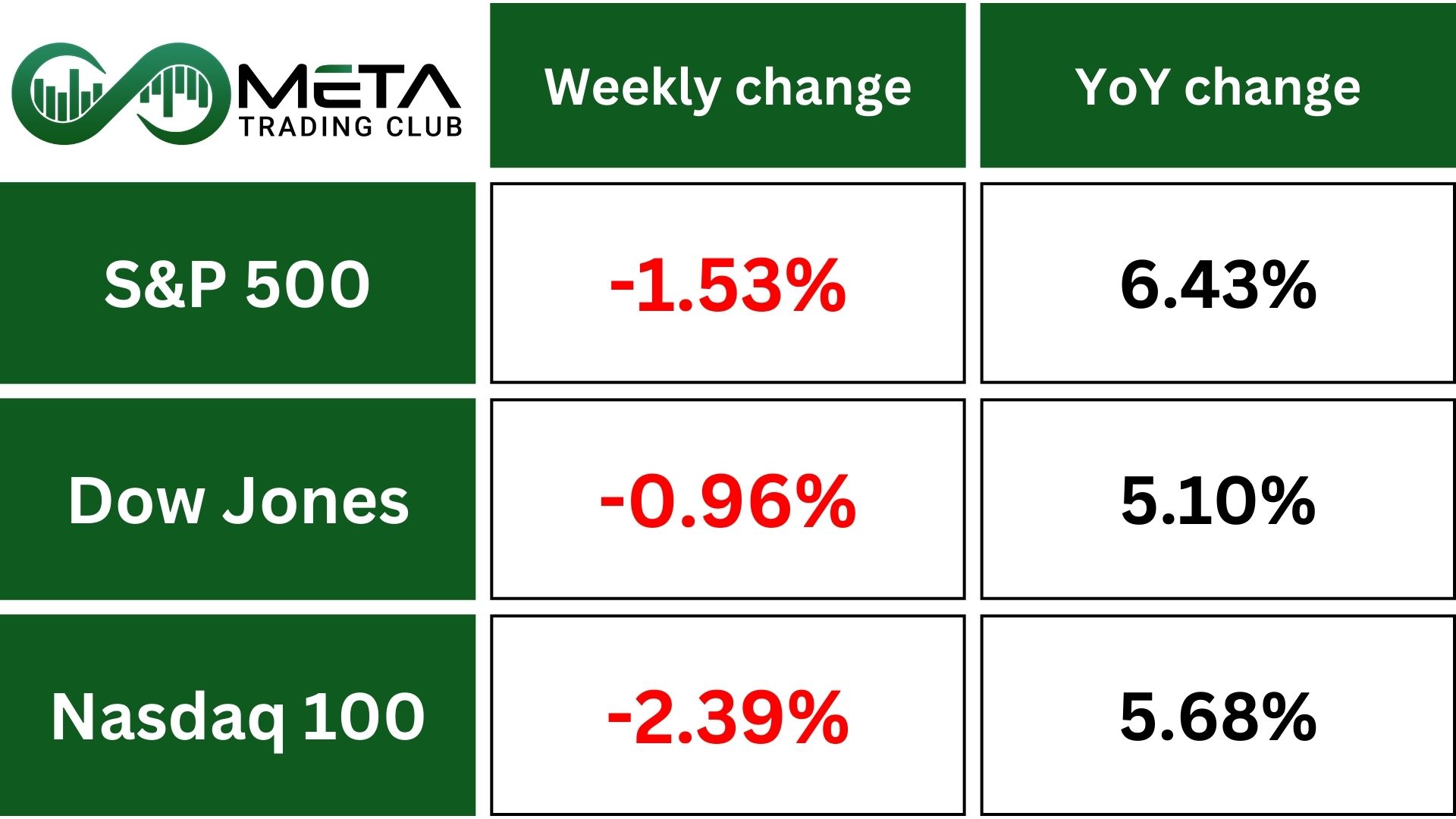

Indices’ Weekly Performance:

U.S. stock indexes dropped this week due to higher-than-expected inflation and President Trump’s announcement of 25% tariffs on car imports, raising fears of rising prices and slower economic growth.

The S&P 500 fell 1.5%, the Nasdaq plunged 2.3%, and the Dow Jones dropped 1% compared to higher levels last week. Most “Magnificent 7” stocks declined, with Tesla being the exception.

On Wednesday, Trump announced tariffs on cars and trucks starting April 3, with more tariffs, including on copper, expected soon. These measures are likely to increase inflation and slow growth, with a possible 20-30 basis point rise in inflation if the auto tariffs are permanent.

February saw core inflation rise to 2.8% annually, while personal spending grew 0.4% and spending growth fell short of expectations. Analysts believe consumer spending growth will remain below 1% in the first quarter, indicating weaker economic momentum.

Technically, SPX pulled back down from the 200-day Moving Average, with diminishing momentum, remaining under the 5,630 resistance level. This suggests a potential decline toward the 5,500 Fibonacci support, or even lower levels.

Stocks

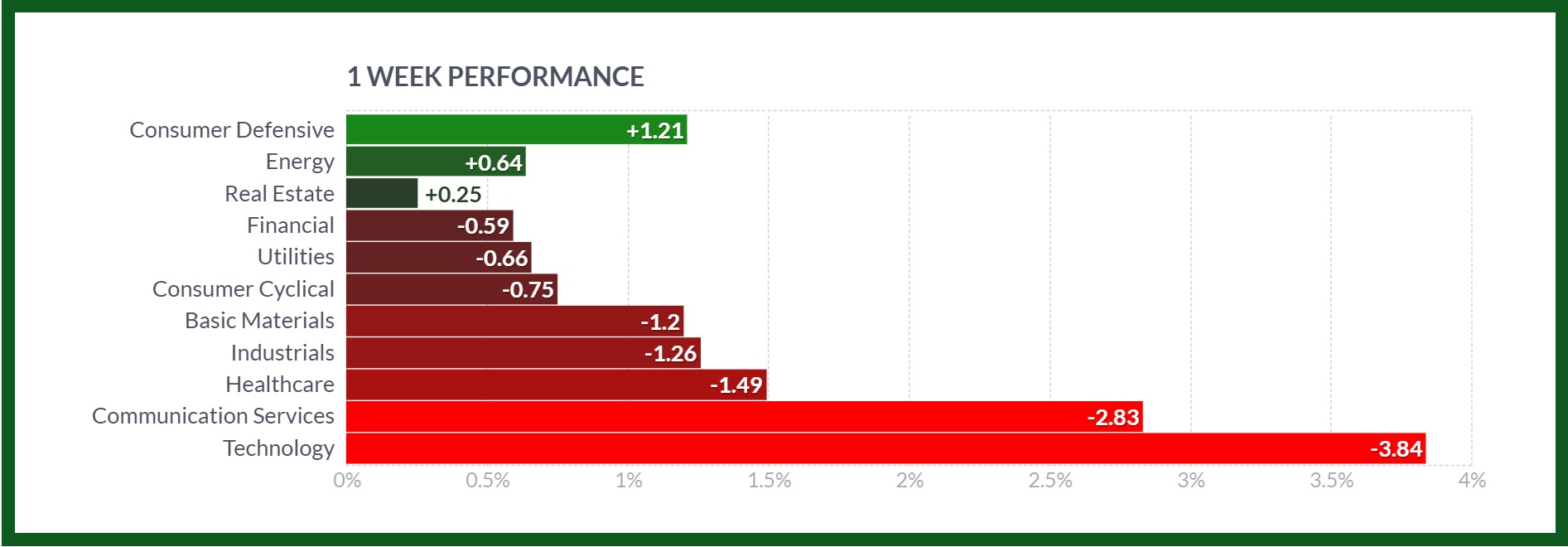

Sector’s Weekly Performance:

Source: Finviz

Most sectors stumbled, with Technology and Communication Services facing significant losses, while Consumer Staples held steady. Growth stocks started the year weaker compared to value stocks.

- Technology (-3.8%): Oracle (ORCL) dropped after reports of U.S. defense contract cuts, also Advanced Micro Devices (AMD) fell on a Jefferies downgrade. Overall, the Semiconductor Index plunged 6%.

- Financials (-0.6%): Despite the sector’s slight dip, W.R. Berkley (WRB) surged 13% after Mitsui Sumitomo announced a 15% stake purchase.

- Consumer Discretionary (-0.75): Tesla (TSLA) rose 6% after optimism around tariff exposure. Auto parts retailers O’Reilly (ORLY) and AutoZone (AZO) hit record highs, but automakers GM and Ford skidded.

- Consumer Staples (+1.6%): Dollar Tree (DLTR) jumped after selling Family Dollar and receiving Wall Street price target boosts.

Other Highlights: Nvidia-backend CoreWeave (CRWV.O) disappointed in its IPO, while GameStop (GME) initially climbed on a bitcoin venture but slid after announcing a $1.3 billion convertible debt offering.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- Cintas (CTAS): Surged 6.3% following its strong fiscal Q3 earnings report, which highlighted an 8.4% revenue increase and raised annual guidance.

- Paychex (PAYX): Rose 5.6% after reporting solid Q3 results, including revenue growth and operating income. The announcement of its acquisition of Paycor HCM further fueled optimism about its future growth prospects.

- O’Reilly (ORLY): Climbed 5.2% driven by gains from Trump’s auto tariff policy.

- FedEx (FDX): Increased 5% after rebounding from last week’s earnings-driven sell-off, as the company introduced cost-cutting initiatives and enhanced operational efficiency.

- Welltower (WELL): Rose 4.7% driven by strong demand in the senior housing and healthcare real estate sectors.

- AutoZone (AZO): Gained 4.5% boosted by benefits from Trump’s auto tariff decision.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

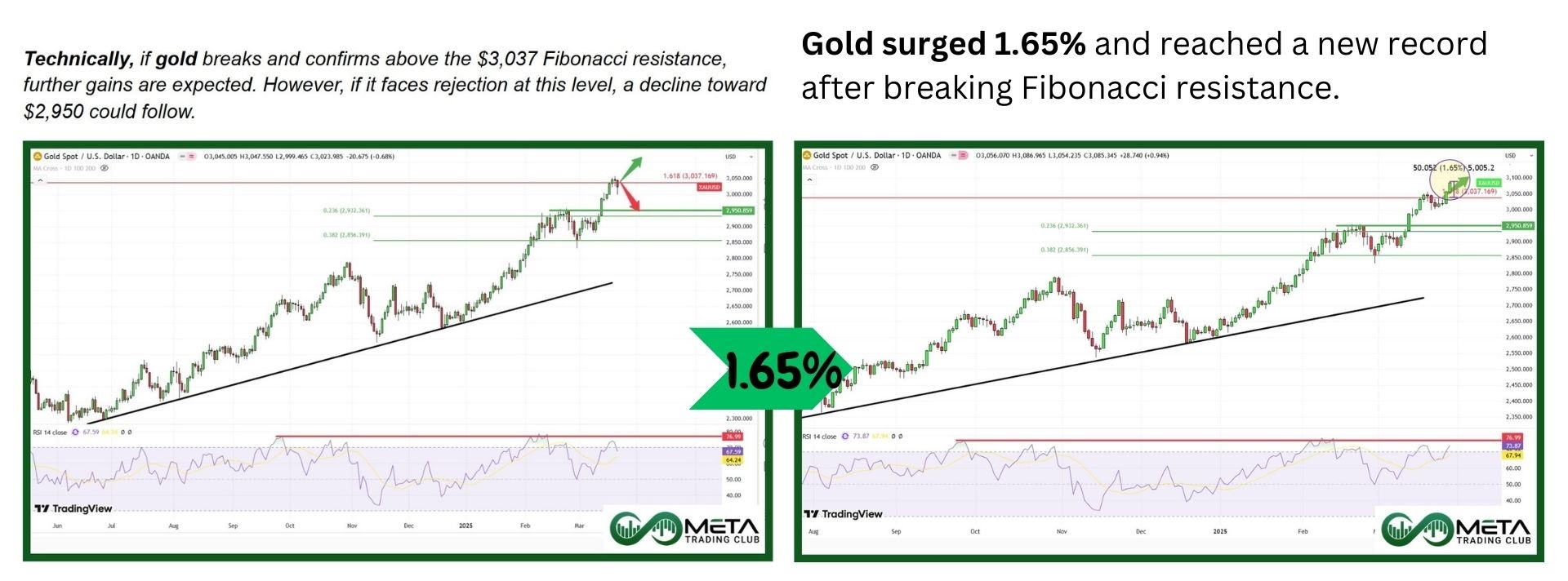

Gold (XAUUSD) reached an all-time high of $3,080 per ounce last week. Traders rushed to buy gold after Donald Trump announced aggressive tariff policies, including a 25% auto duty starting April 3, which could reshape global trade dynamics.

Investors remain anxious ahead of the April 2 tariff announcement, which may target specific countries and industries, potentially including gold. Fears of gold tariffs have driven high demand from central banks, major investors, and U.S. dealers.

Technically, gold faces resistance at $3,090, with possible consolidation around $3,100 if bulls push through.

Crude oil prices achieved a third weekly increase, boosted by U.S. sanctions on Venezuela and Iran. A 3.3 million barrel drop in U.S. crude stockpiles points to strong demand.

Tariffs on Venezuelan oil are expected to further hurt its production, while sanctions on Iran and Venezuela are tightening the global oil supply. Markets are keeping a close eye on these geopolitical issues and their effects on oil prices.

However, WTI crude oil fell 0.8% on Friday due to fears that trade tensions, especially between the U.S. and its main partners, might lead to a global recession.

Forex

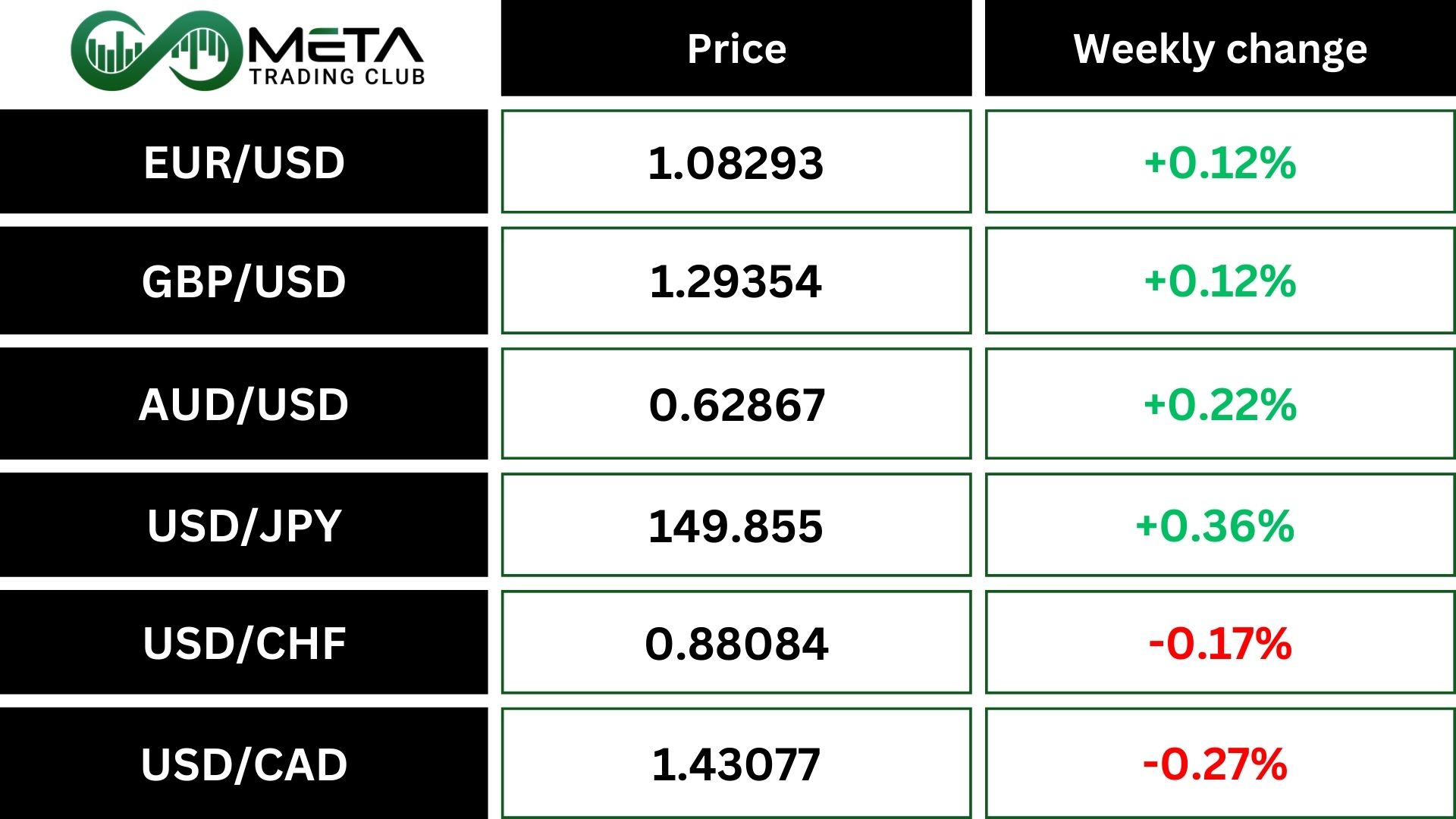

Weekly Performance of Major Foreign Exchange Pairs:

GBP/USD: British pound gained slightly to $1.2935 as UK retail sales unexpectedly rose last month, surprising those who had anticipated a decline amidst the nation’s slow economic growth.

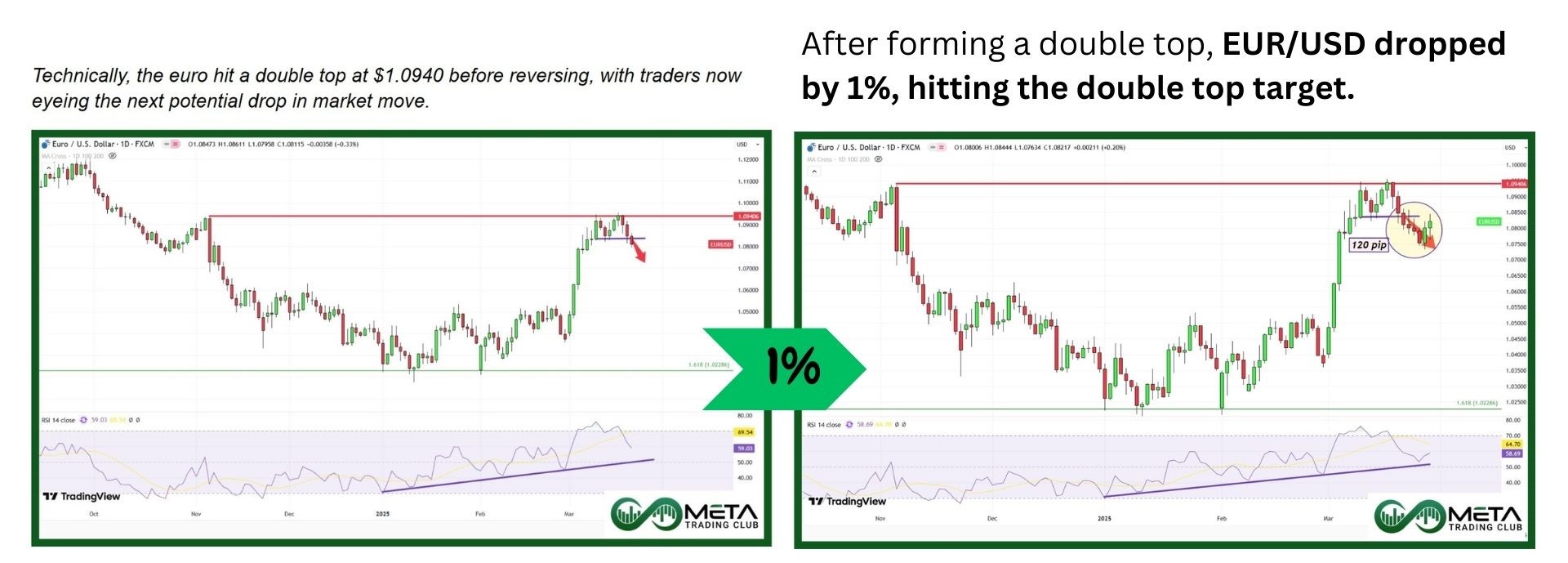

EUR/USD: Euro climbed steadily throughout the week. It gained 0.12% against the dollar. The euro climbed 0.2% to $1.0823, supported by technical factors like the 200-day moving average.

USD/JPY: The dollar rose against the yen as core consumer inflation in Tokyo stayed above the central bank’s target and rose in March.

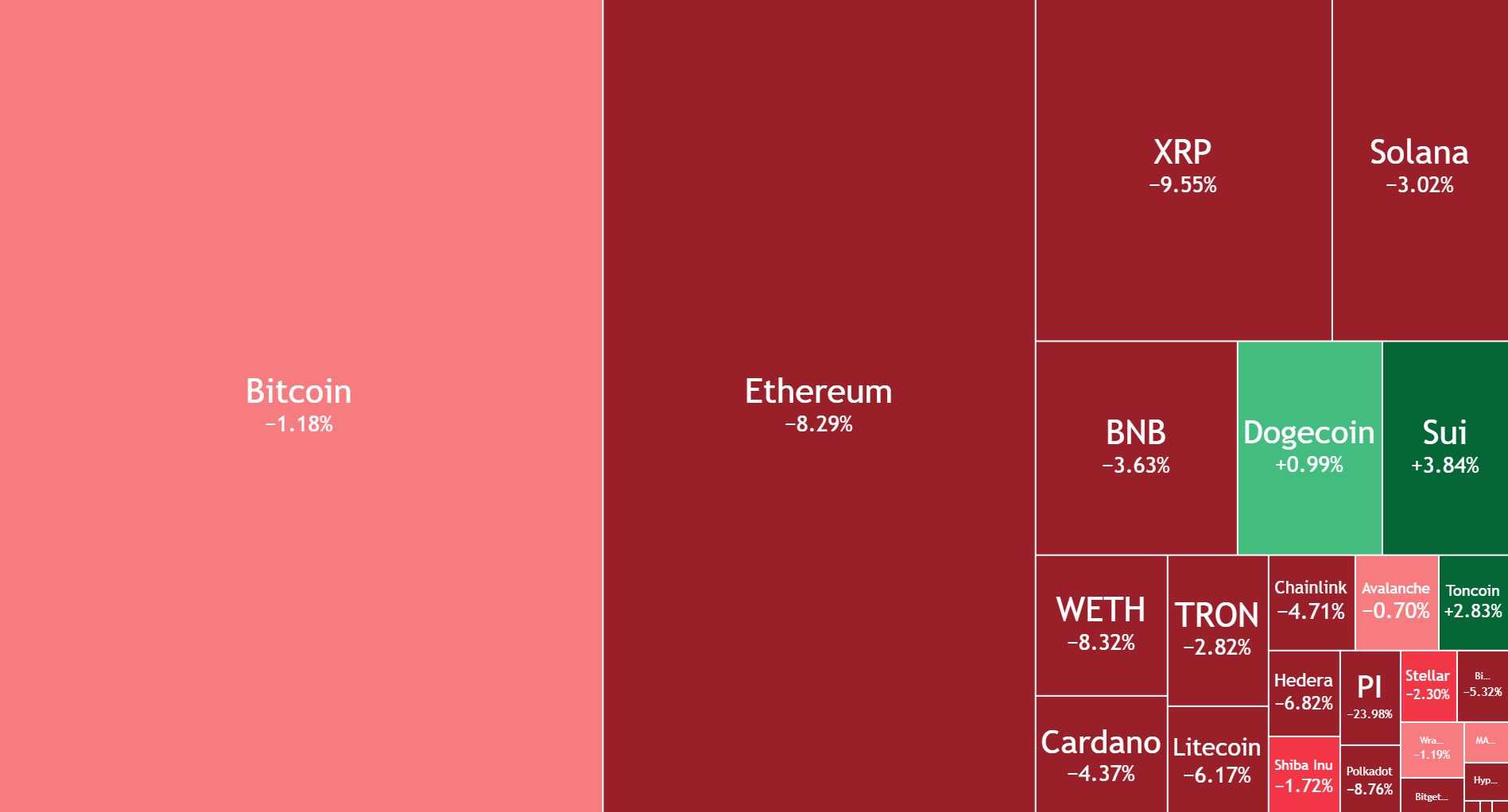

Crypto

Crypto Market Weekly Performance:

Source: Tradingview

Concerns about a global trade war are weighing heavily on cryptocurrency markets. Investors are closely watching for a potential tariff announcement from President Trump on April 2, which could significantly influence Bitcoin’s price trends for the month.

Bitcoin has dropped 18% in the two months following the tariff announcement.

Despite the uncertainty, large Bitcoin holders, or “whales,” with 1,000 to 10,000 BTC, have continued to accumulate. The number of such addresses has grown from 1,956 at the start of 2025 to over 1,990 by late March, though still below the peak of 2,370 in February 2024. This steady accumulation reflects confidence among major investors despite market volatility.

Technically, if bullish confirmations occur, BTC could rise toward the uptrend line. For further upward momentum, it must break the downtrend line with strong force. However, if the Fibonacci support near $80K fails, a further decline to the next Fibonacci support level is expected.

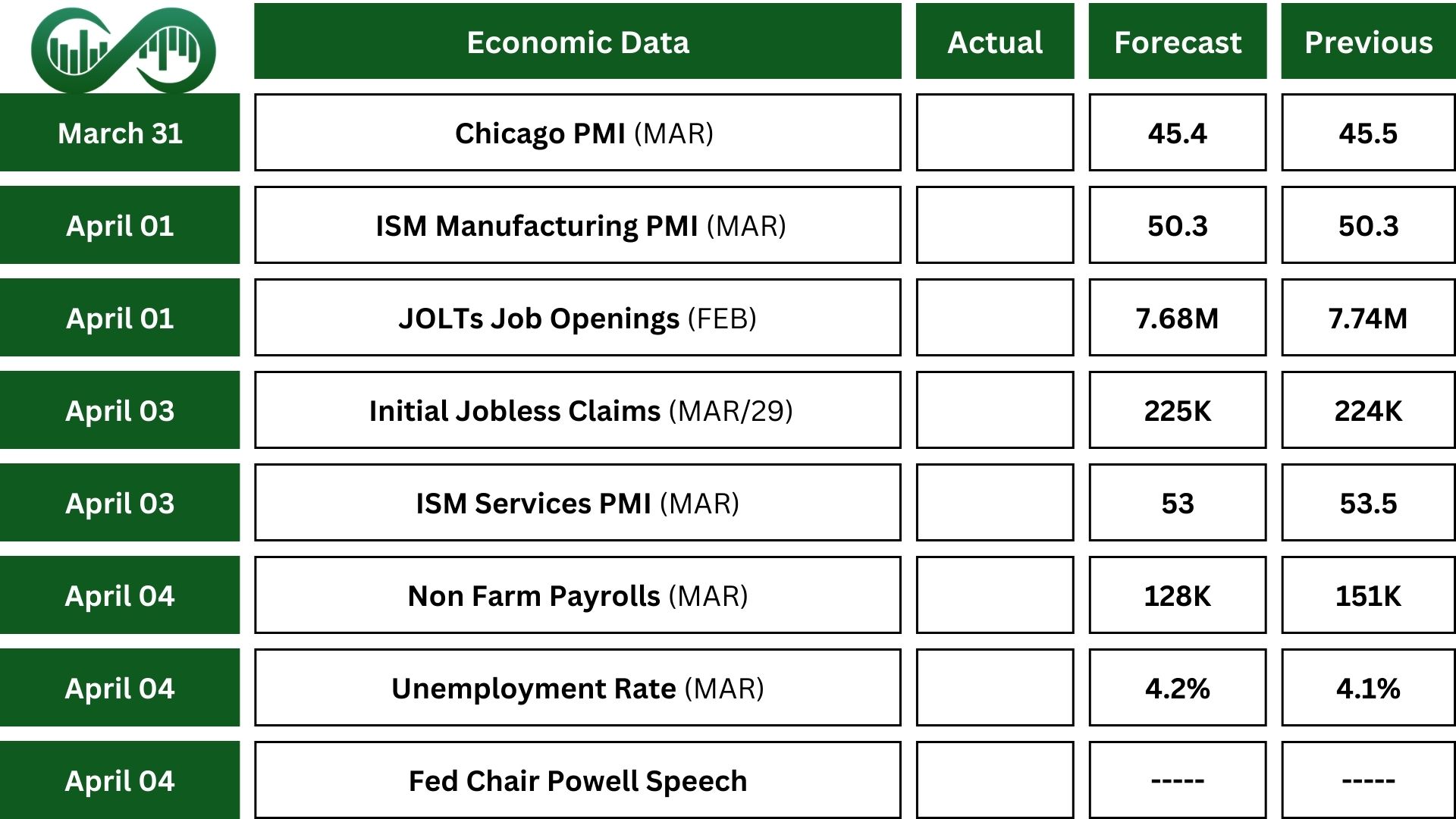

Next Week’s Outlook

Economic Events

Traders in the US are keeping a close eye on the March jobs report to understand the labor market, especially with recent layoffs and new tariffs.

The economy likely added 128,000 Non-Farm Payrolls, fewer than February’s 151,000, and the Unemployment Rate might rise slightly to 4.2%. Wages probably grew at the same pace as before, 0.3%.

Other important job-related data, like JOLTS Job Openings, ADP Employment Change and Challenger Job Cuts, will also be watched.

Beyond jobs, reports on manufacturing and services will show how businesses are doing, with ISM Manufacturing PMI expected to barely grow and ISM Services PMI possibly slowing down. Additional updates will cover factory orders, trade, construction spending, and more. Federal Reserve officials, including Chair Jerome Powell, will also speak, and investors will pay attention to their comments for clues about the economy and future policies.

The upcoming April 2 is expected to outline reciprocal tariffs targeting major U.S. trading partners, aiming to cut the $1.2 trillion trade deficit and boost domestic manufacturing.

Earnings Events

This week is relatively quiet, with no significant earnings reports scheduled.