What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

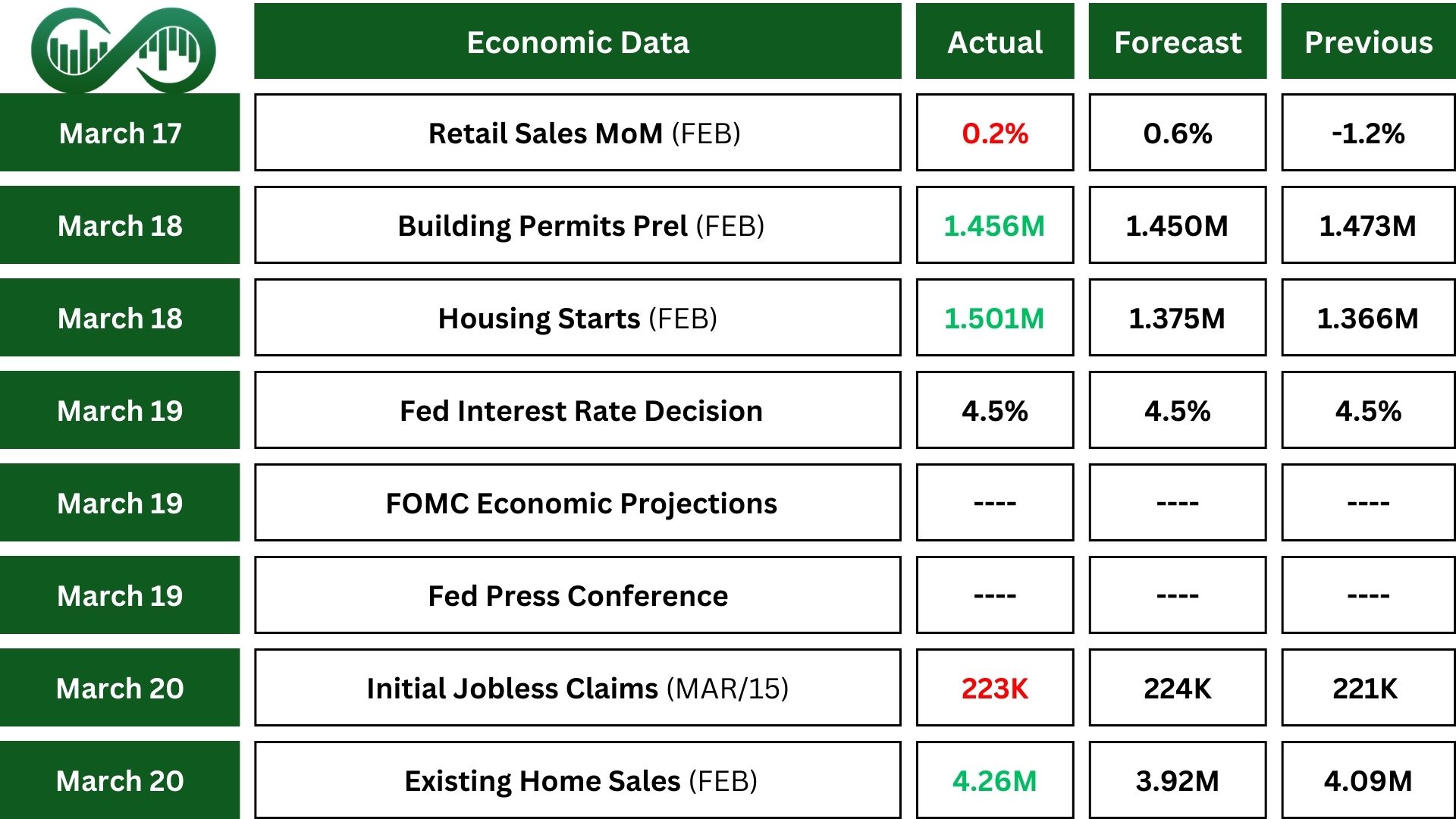

U.S. retail and food sales were $722.7 billion in February 2025, up 0.2% from January, recovering from the 1.2% drop in January. This growth was smaller than expected. Also, sales grew by 3.1% from last year, showing steady improvement despite some ups and downs.

The FOMC holds interest rates between 4.25% and 4.5%, but any changes will depend on new data and risks. Starting in April, they’ll sell fewer Treasury securities ($5 billion monthly) but keep mortgage-backed securities sales at $35 billion. Their goal is to lower unemployment and bring inflation back to 2%, while staying flexible to adjust to economic changes.

The Fed expects slower growth, with GDP rising 1.7% in 2025 and staying at 1.8% later. Unemployment might go up slightly to 4.4% in 2025 but settle at 4.3% afterward. Inflation would drop from 2.7% in 2025 to 2% over time. Interest rates are expected to fall from 3.9% in 2025 to 3% in the long run. These predictions assume no big surprises in the economy.

Chair Powell said the economy is doing well, with a strong job market and steady unemployment. The Fed is being cautious and waiting for more clarity before making changes. They’re ready to act if the job market weakens. Powell mentioned tariffs are slowing growth but raising inflation, and housing inflation is dropping. His calm tone and decision to keep rates steady reassured investors, leading to a rise in stock prices.

Initial Jobless claims in the U.S. increased slightly to 223K in mid-March, staying low and close to expectations. Continuing claims went up by 33K as forecasted. The labor market remains strong despite earlier economic issues. However, Federal employee claims from DOGE firings dropped to 1,066.

Earnings Reports

Micron

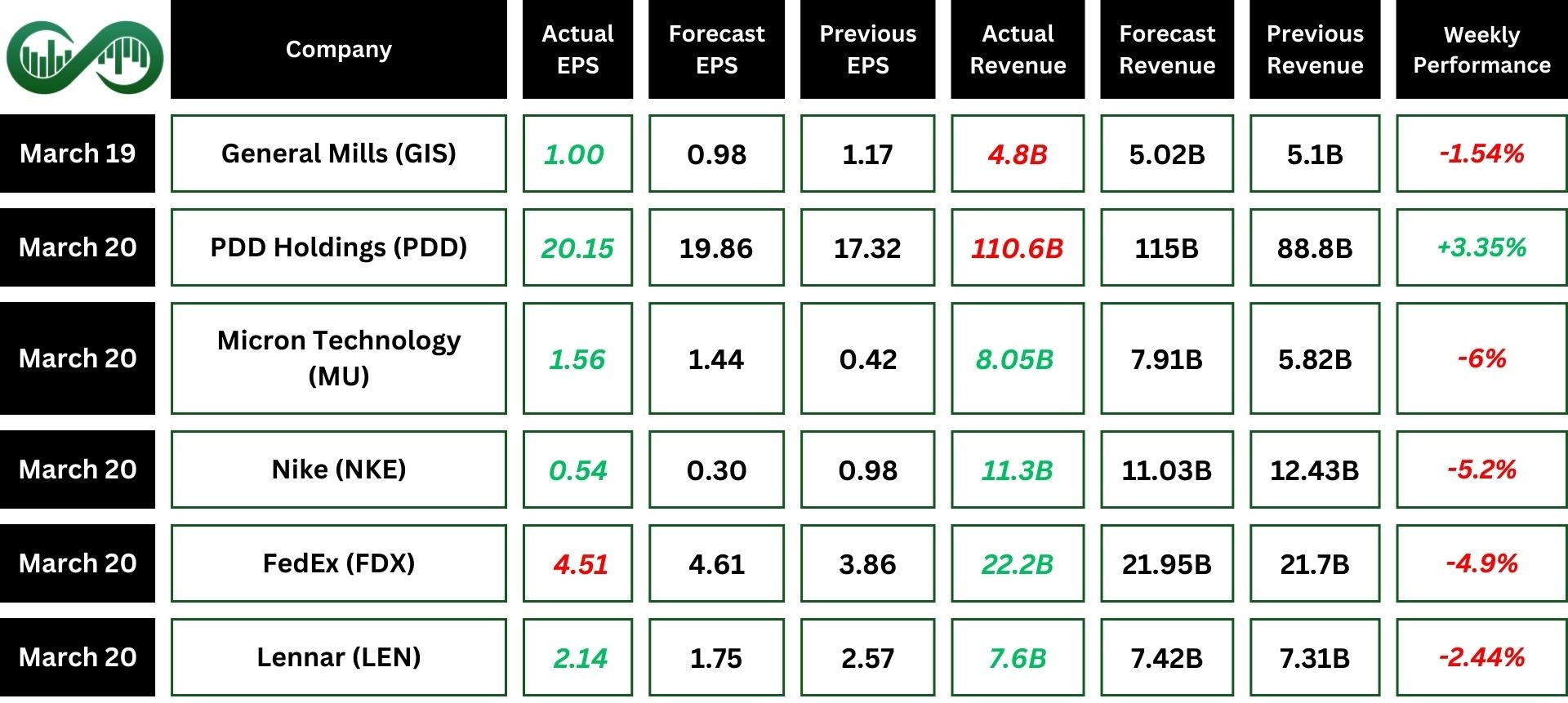

Micron Technology (MU) had a strong Q2 2025, with $8.05 billion in revenue, $1.58 billion in net income, and $3.94 billion in cash flow.

They hit a milestone with over $1 billion in HBM sales and set records for data center DRAM sales thanks to AI demand.

Despite meeting expectations, their stock fell due to concerns about weaker guidance for next quarter, caused by slowing demand, extra inventory, and issues in the NAND market.

Technically, MU has been consolidating within the $84 to $110 range for approximately a year. To signal a bullish trend, it must break above the $110 resistance, while bearish confirmation requires a breakdown below the $84 support level.

Nike

Nike (NKE) reported $11.3 billion in revenue for Q3 fiscal 2025, down 9% from last year but better than expected.

Sales and profit margins dropped due to higher costs and discounts, with net income falling 32% to $0.8 billion.

Despite this, earnings per share of $0.54 beat expectations. Nike paid $594 million in dividends, continuing its 23-year streak of yearly increases.

Nike’s stock dropped to its lowest in five years because of worries about lower sales, reduced profits, and poor performance in key markets like China.

Technically, NKE has dropped below its key support level of $69 and is now approaching the next support at $60, marking its lowest price in five years.

FedEx

FedEx (FDX) announced Q3 2025 results, earning $3.76 per share ($4.51 adjusted) and making $22.2 billion in revenue, which beat forecasts but missed earnings estimates.

Improvements came from cost-saving efforts, better prices, and more shipments, but FedEx Freight struggled with fewer shipments and lower fuel fees.

The company lowered its outlook for fiscal 2025, expecting flat or slightly lower revenue, reduced profits, and cutting spending to $4.9 billion. FedEx’s stock dropped because of this weaker guidance, missed earnings expectations, and challenges in the U.S. industrial and business markets.

Technically, if FDX breaks above $235, the price could surge at least to the trendline. For further gains, it must first break the downtrend line. However, a confirmed break below $224 could lead to a drop toward $210.

Indices

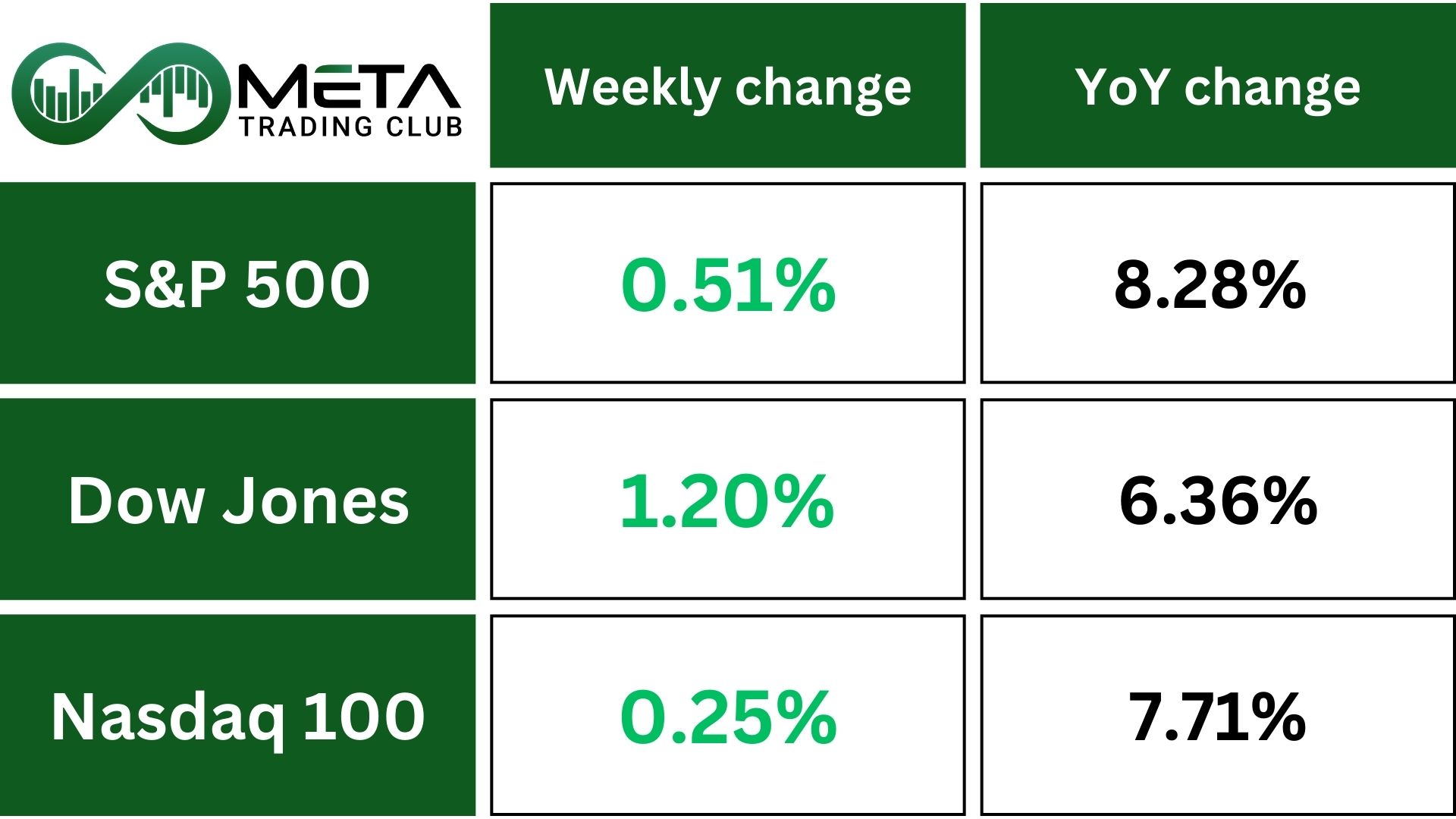

Indices’ Weekly Performance:

US stock indexes went up this week, with the S&P 500, Nasdaq, and Dow Jones making small gains as investors adjusted to new expectations for interest rates and dealt with trade and global tensions.

The Federal Reserve kept rates the same but hinted at possible cuts by the end of the year. Also, the EU postponed tariffs on US goods. A survey showed fewer investors putting money into US stocks, marking a record drop.

Indices went up despite the Federal Reserve highlighting uncertainty in the economy. Investors felt reassured by the Fed’s cautious approach to inflation and growth. Keeping interest rates steady and showing flexibility in handling risks boosted confidence, leading to higher stock prices.

Technically, if SPX breaks and confirms above 5,673, further gains are expected. Conversely, a confirmed drop below 5,636 could lead the index toward the support level of 5,515.

Technically, for NDX to rally, it must break above the 19,883 resistance zone, potentially climbing to 20,600. However, if it drops below the support of 19,300, it could fall further to 18,500.

Stocks

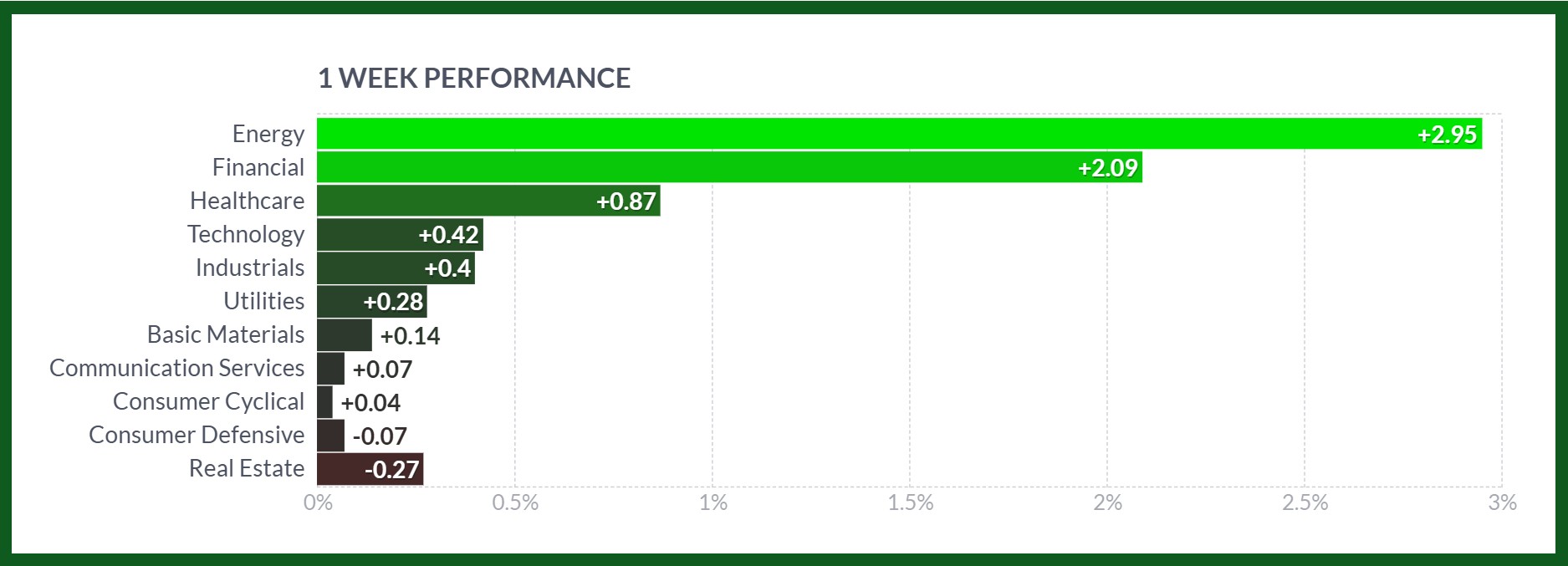

Sector’s Weekly Performance:

Source: Finviz

In the end, only a few sectors performed well, with Energy and Financials leading the way, while defensive sectors weakened.

- Energy: Up 3%, driven by rising oil prices due to U.S. actions in Yemen, new sanctions on Iran, and tighter supply expectations.

- Financials: Up 2%, boosted by Berkshire Hathaway increasing investments in Japanese trading companies, hitting record highs.

- Healthcare: Gained 0.87%, although Incyte‘s stock fell after its drug trials didn’t meet earlier results.

- Technology: Gained 0.42%, with Nvidia dipping due to AI cost concerns, and Micron and Accenture declining on weaker forecasts.

- Industrials: Rose 0.4%, with Boeing up on a U.S. fighter jet contract, while Lockheed Martin fell. FedEx dropped after lowering its annual revenue and profit forecasts.

- Consumer Discretionary: Flat overall. Nike dropped on poor revenue projections, while Tesla rebounded after Musk’s recommendations but still ended its ninth week down.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- Boeing (BA): Surged 10% after Boeing was chosen to develop a cutting-edge, costly fighter jet essential for countering China’s military in the future.

- Applovin (APP): Rose 7% driven positive sentiment despite ongoing investigation claims against the company (May 5, 2025, deadline to apply as lead plaintiff in a securities class action).

- GE Vernova (GEV): Increased 6.4% as the company announced advancements in renewable energy projects, aligning with global trends toward clean energy solutions.

- Uber Technologies (UBER): Climbed 6% following reports that analyst adjusts price target on Uber to $85 from $80

- UnitedHealth (UNH): Gained 5.7% after UnitedHealth Group’s Optum Rx plans to cut up to 25% of reauthorizations for prescription drugs, aiming to make it easier for consumers to access their medications.

- Palantir Technologies (PLTR): Increased 5.4% fueled by new government contracts and increased adoption of its data analytics platforms.

- Advanced Micro Devices (AMD): Rose 5.4% as AMD’s newest processors are perfect for network and security firewalls, storage systems, and industrial control applications, thanks to their high performance and energy efficiency.

- Blackstone (BX): Climbed 5.2% with interest rates staying the same, banks are likely to face prolonged periods of elevated funding costs, affecting their profitability and lending practices.

- Chevron (CVX): Surged 4.9% as plans to build data centers and create the energy systems needed to power them..

- Netflix (NFLX): Increased 4.6% as Netflix’s streaming viewership increased in February 2025, capturing 8.2% of total TV viewing time.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

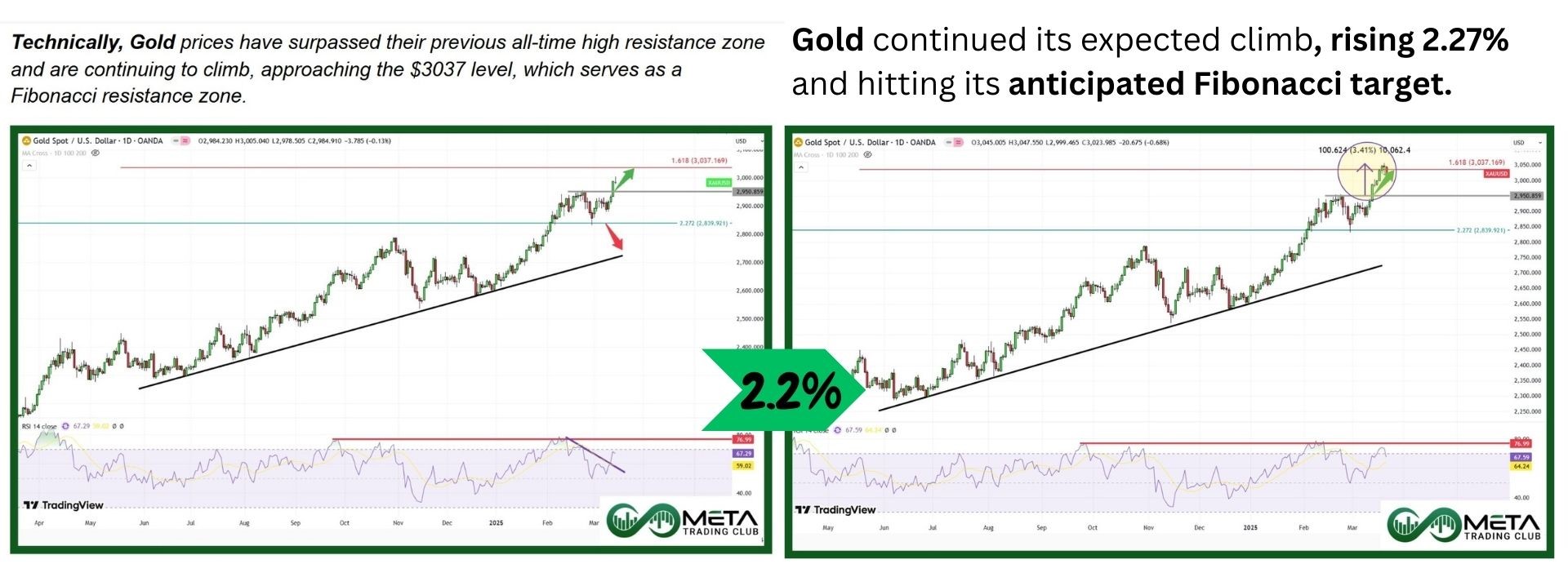

Gold prices have risen for three consecutive weeks, staying above $3,000 per troy ounce. The rally began March 13, as U.S. stocks declined, boosting safe-haven demand. The Federal Reserve’s projections for rate cuts in 2025, higher inflation, and weaker growth have further supported gold prices.

Central banks like China’s and Bolivia’s increased gold buying has also strengthened demand.

Although gold saw minor profit-taking late in the week, geopolitical instability and a weaker U.S. dollar suggest continued growth potential, with long-term investors driving further interest in gold funds.

Technically, if gold breaks and confirms above the $3,037 Fibonacci resistance, further gains are expected. However, if it faces rejection at this level, a decline toward $2,950 could follow.

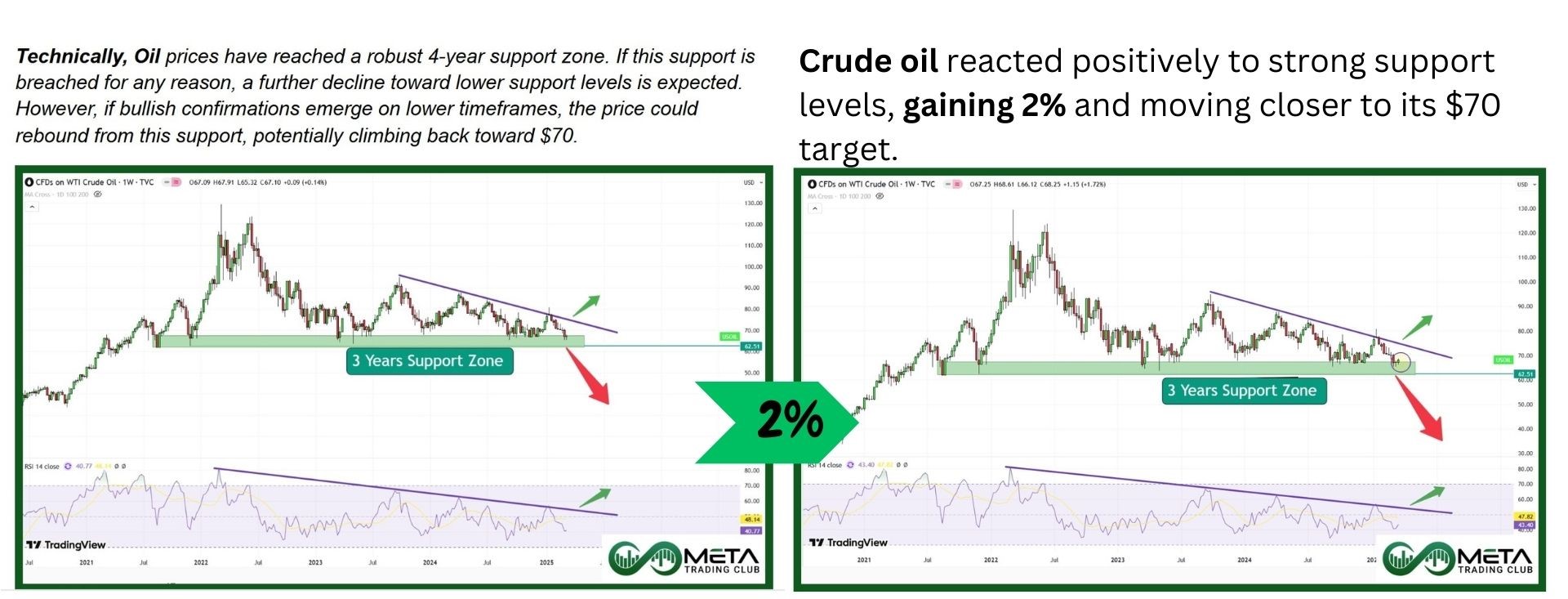

Crude oil prices saw gains last week, supported by U.S. sanctions targeting Iranian oil exports and rising tensions in the Middle East, which could disrupt supplies.

However, gains were limited by a stronger dollar and concerns over global growth due to tariffs. Increased Russian oil exports and OPEC+’s gradual production hike also pressured prices. Meanwhile, weakened oil demand in China added to bearish sentiment, though U.S. sanctions on Russia’s oil sector provided some support by tightening global supply.

Forex

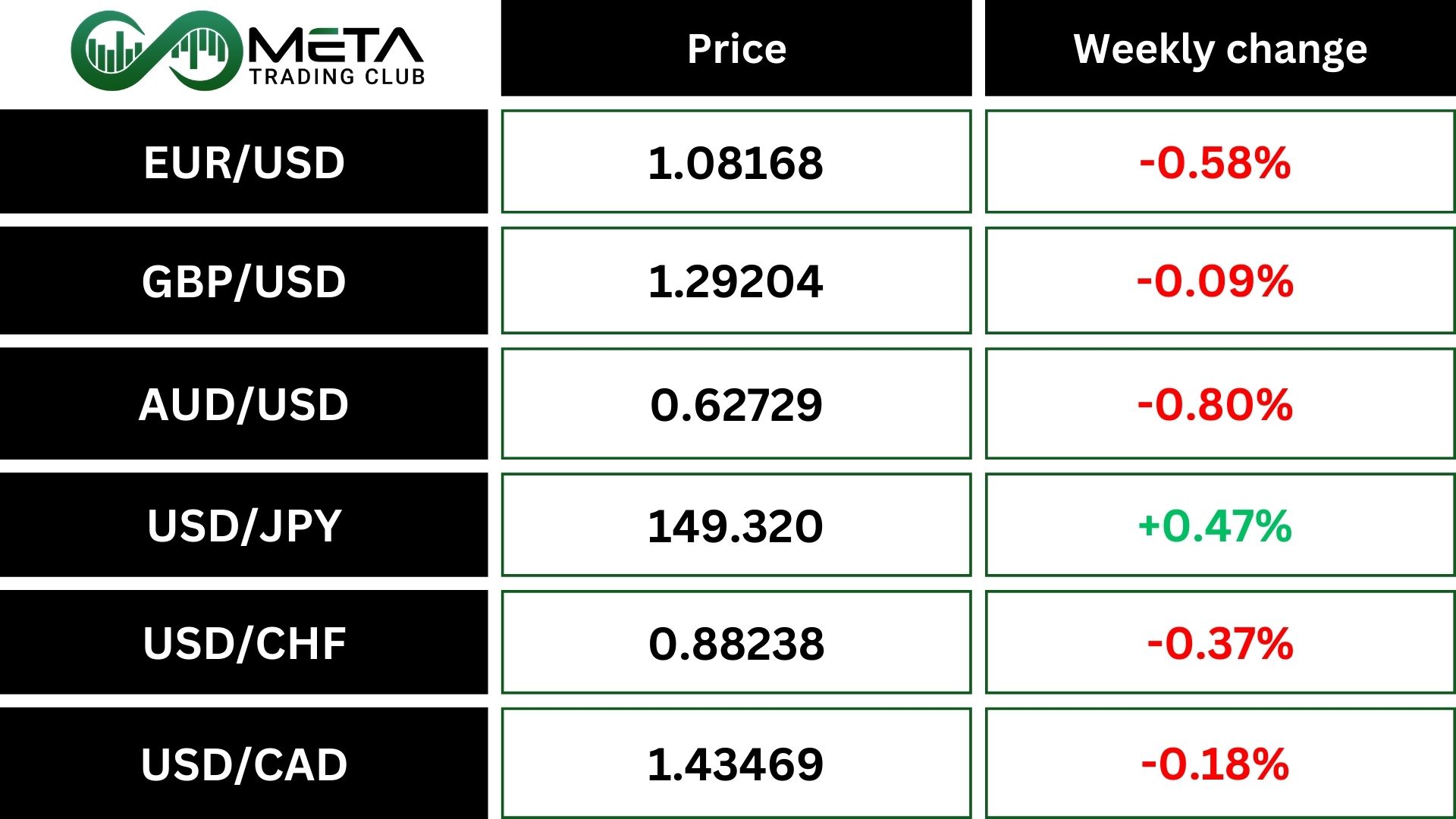

Weekly Performance of Major Foreign Exchange Pairs:

The US dollar index (DXY) rose to 103.88 on Friday, its highest in three weeks, showing little reaction to the Federal Reserve’s decision to hold interest rates steady while planning two cuts later this year. Despite tariff concerns, Powell’s optimistic remarks boosted stock markets, leading to the best Fed day rally for equities since July. However, the dollar struggled as rival currencies dominated forex trades.

Technically, the dollar has dropped 6.5% from its January peak of 110.17 and is nearing pre-election levels, with key support at 100 and resistance at 107.70.

The EUR/USD pair declined as the US dollar surged across the forex market. This comes after two weeks of gains fueled by Germany’s spending plans to boost its economy, though questions remain about the details of those plans.

This marks a reversal for the euro after weeks of gains that peaked at $1.0950, a five-month high. Speculation grows that the dollar is regaining strength despite trade tariffs and the Federal Reserve’s potential rate cuts.

Technically, the euro hit a double top at $1.0940 before reversing, with traders now eyeing the next potential drop in market move.

Als, Federal Reserve, Bank of England, and Bank of Japan kept their interest rates steady this week, with the Fed hinting at two rate cuts later this year. Meanwhile, the British pound slipped after the Bank of England warned that future rate cuts are not guaranteed. The dollar also pushed GBP/USD down.

Crypto

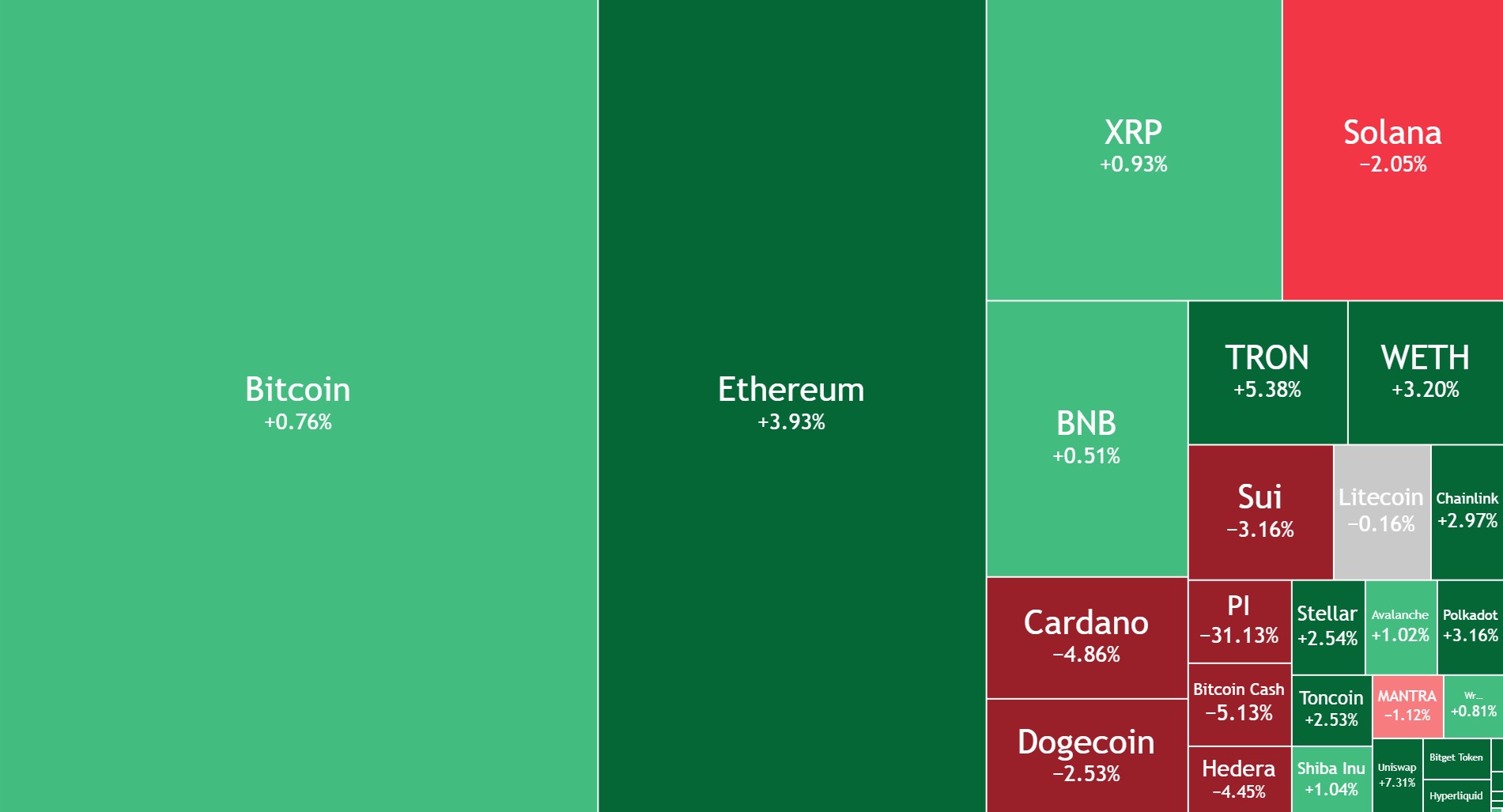

Crypto Market Weekly Performance:

Source: Tradingview

Bitcoin prices jumped to a high of $86,000, driven by optimism from the Federal Reserve’s decision to keep interest rates unchanged and consider potential rate cuts later this year.

However, momentum faded, and prices normalized below $86,000. Despite this, Bitcoin hit its highest point since early March, signaling possible bullish sentiment. The cryptocurrency remains 26% below its January peak of $109,000 but gained from traders’ increased risk appetite, expecting lower rates to boost market liquidity.

Technically, if bullish confirmations occur, BTC could rise toward the uptrend line. For further upward momentum, it must break the downtrend line with strong force. However, if the Fibonacci support near $80K fails, a further decline to the next Fibonacci support level is expected.

Next Week’s Outlook

Economic Events

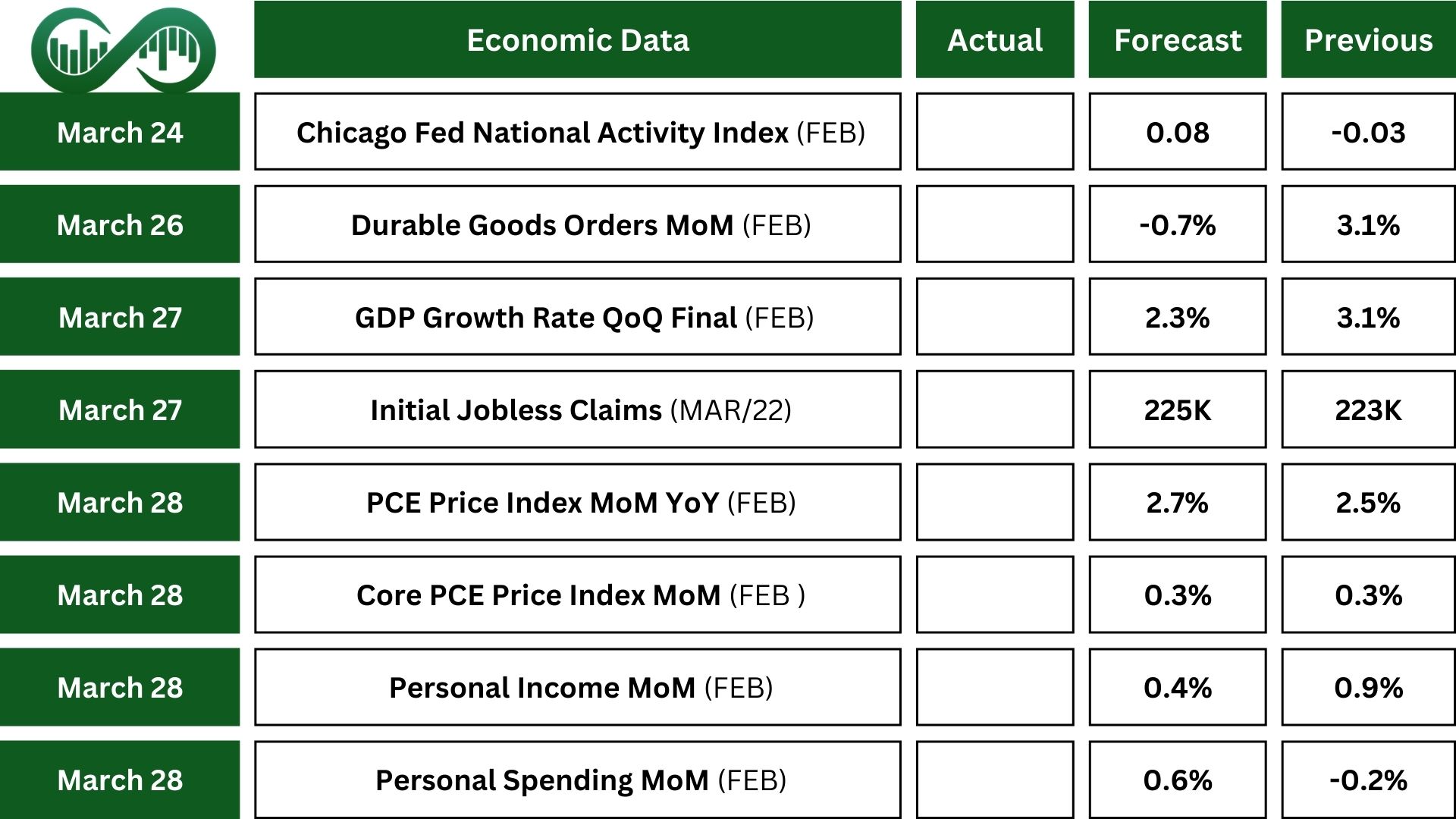

The February PCE report is a key focus in the US after the FOMC adjusted its outlook, lowering growth projections and increasing price expectations. Both overall and core PCE price indices likely rose by 0.3% again, just like the previous month. The report is expected to show strong growth in personal spending, even as personal income declines.

The BEA will also publish the final Q4 GDP reading, which is predicted to have grown by 2.3% annually.

Other data may show a drop in durable goods orders and a record-high trade deficit due to businesses cutting costs ahead of tariffs.

Flash S&P PMI data is expected to indicate further activity growth.

In housing, new and pending home sales might recover from last month’s declines, and the S&P/Case-Shiller index could reveal faster home price increases.

Earnings Events

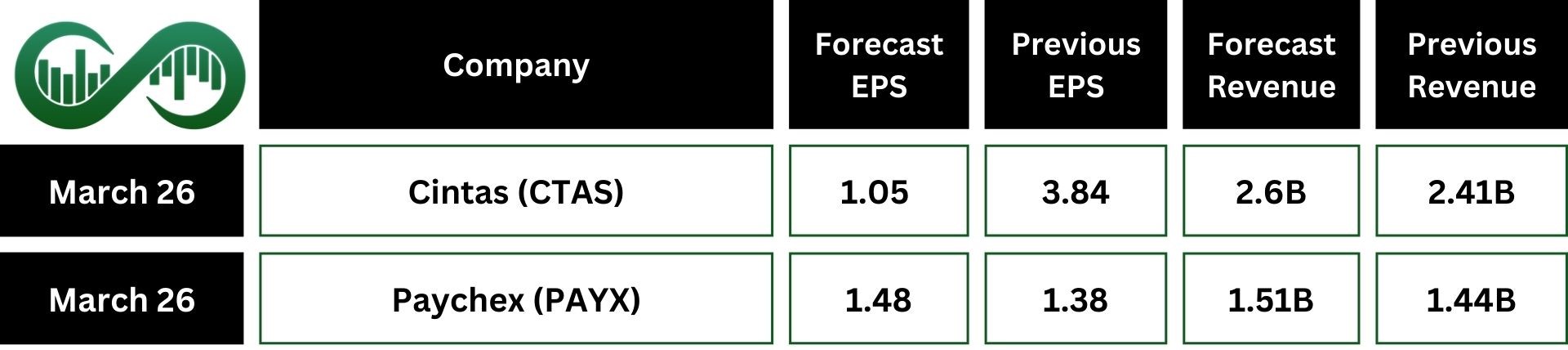

There aren’t any significant earnings reports scheduled this week, but two major companies, Cintas (CTAS) and Paychex (PAYX) , will be releasing their results.