What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

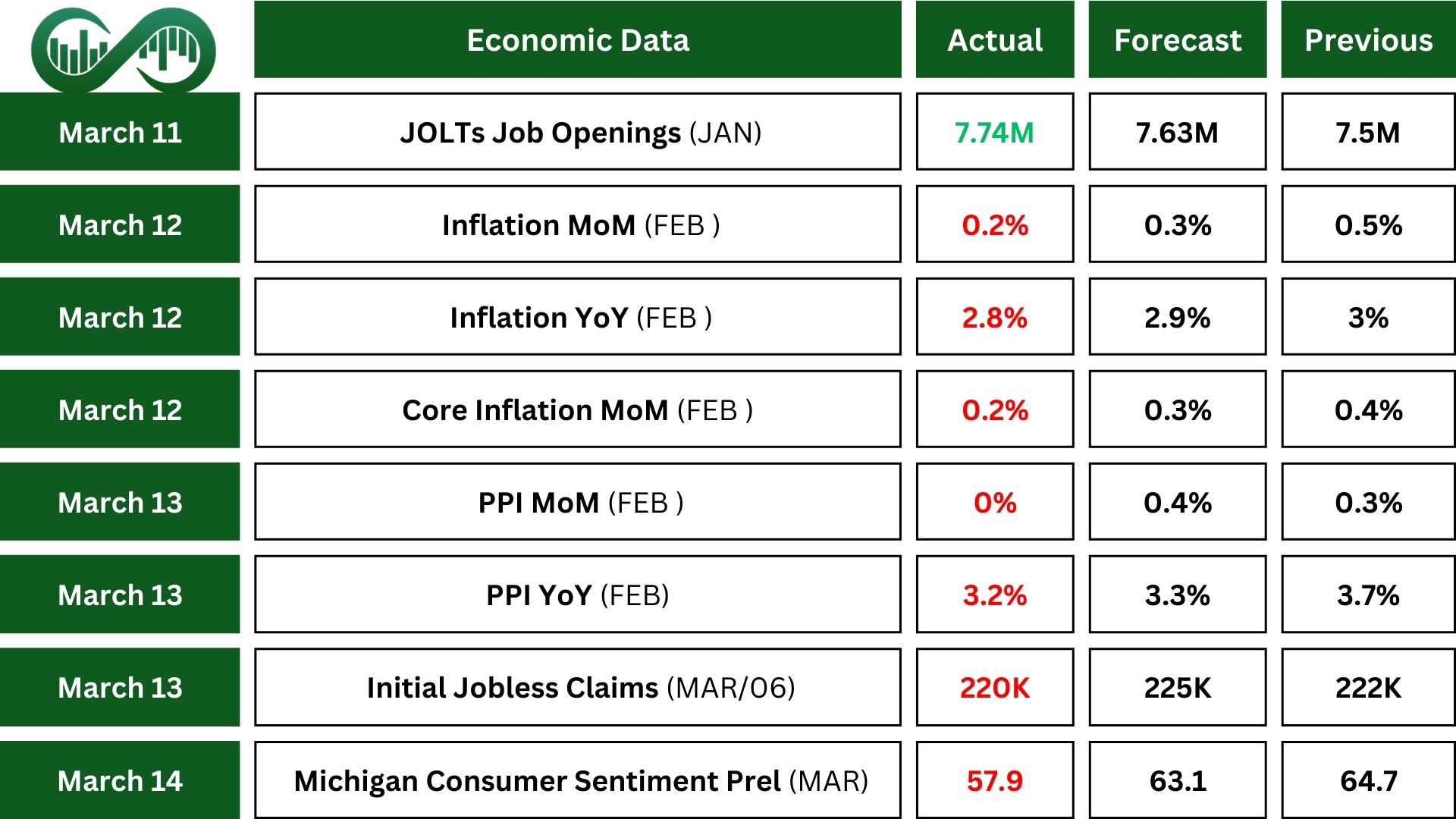

There are 7.7 million job openings, which stayed the same but are fewer than last year. Also, hiring overall stayed at 5.4 million, and 5.3 million people left their jobs (quitting, layoffs, or other reasons). The labor market is stable, with some ups and downs in different areas.

CPI inflation rose 0.2% in February, slower than the 0.5% increase in January and below expectations. Over the last year, prices grew 2.8% overall. Key price increases were in medical care and used cars, but airline fares and new cars got cheaper. Food prices went up by 2.6%, and energy prices dropped slightly.

Producer PPI inflation didn’t change in February but grew 3.2% over the past year. Goods prices rose 0.3%, with eggs going up 53.6%, while energy prices fell, including a 4.7% drop in gasoline. Service prices dropped 0.2%, mostly due to lower trade margins, though healthcare costs went up slightly. Without counting food, energy, and trade, prices increased 0.2% for the month and 3.3% over the year.

The University of Michigan consumer sentiment has dropped by 22% since December 2024, with people feeling less positive about their finances, jobs, inflation, and the economy. Many blame unclear economic policies.

Also, inflation worries are growing fast. Short-term inflation rose to 4.9% in March, the highest since 2022, and long-term inflation jumped to 3.9%, the biggest monthly increase since 1993.

Earnings Reports

Oracle

Oracle (ORCL) had a good Q3 2025, earning $14.1 billion, an 8% increase from last year.

Their cloud services did really well, Infrastructure as a Service (IaaS) grew 51%, and Software as a Service (SaaS) grew 10%. They also increased their backlog by 63% ($48 billion), raised operating income by 9%, and boosted their dividend by 25%.

However, they faced some issues, like delays in expanding cloud capacity, an 8% drop in software license revenue, and currency challenges. Some analysts lowered their price targets, worried about these problems.

Despite this, Oracle’s cloud business is growing fast, and they’ve partnered with big companies like OpenAI, xAI, Meta, NVIDIA, and AMD, showing their focus on the cloud sector.

Technically, ORCL is displaying significant divergence between its stock price and RSI. With the company reporting strong earnings, this could potentially drive the price higher from its current level. However, if bullish confirmations fail to materialize, the price may decline to the Fibonacci support level of $137.

Adobe

Adobe (ADBE) reported record Q1 2025 revenue of $5.71 billion, a 10% increase from last year. Earnings per share were $5.08, beating analyst expectations.

The Digital Media segment grew 11%, and the Digital Experience segment rose 10%. Adobe also confirmed its growth plans for fiscal year 2025.

Despite these strong results, Adobe’s stock dropped 12% after earning reported. This was due to their more cautious projections for Q2 and the full fiscal year, which worried investors about slower growth.

Technically, ADBE is exhibiting divergence between its RSI and price, currently positioned in oversold territory. This scenario suggests a potential rebound, with the stock possibly climbing to $440. However, if bearish confirmations persist, the stock could drop further, reaching Fibonacci support at $350.

Indices

Indices’ Weekly Performance:

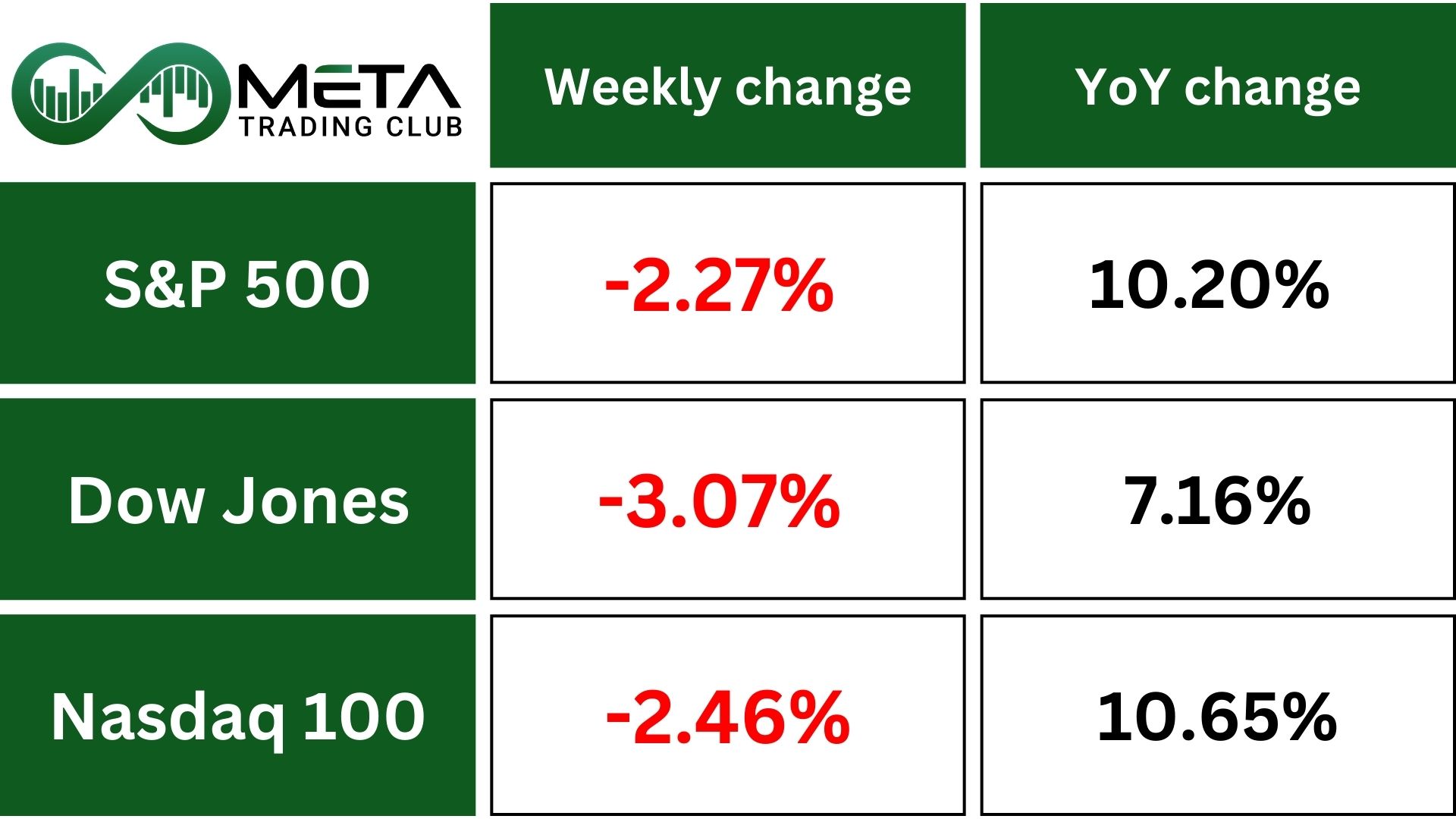

The S&P 500 (SPX) dropped 2.3% last week, marking its fourth week of losses. By the end of the week, the S&P 500 was down 8.2% from its high, the Dow was down 7.8%, and the Nasdaq was down 12%.

The U.S. stock market has entered a correction for the first time in over a year, with the S&P 500 dropping more than 10% from its February 19 high, losing about $5 trillion in market value.

The Nasdaq Composite has also confirmed a correction. This marks a sharp shift in sentiment from earlier in the year when Wall Street was optimistic about Trump’s policies. The Trump administration’s inconsistent tariff actions against Canada, Mexico, and China have reduced investor confidence, raising fears of inflation, slower economic growth, and even a recession.

Also, Wall Street is lowering its predictions for the S&P 500 after the U.S. stock market dropped sharply in early 2025. Analysts often adjust their predictions a few months after markets change. Recently, big firms reduced their targets due to worries about President Trump’s changing tariffs and possible trade wars with other countries, which have unsettled financial markets.

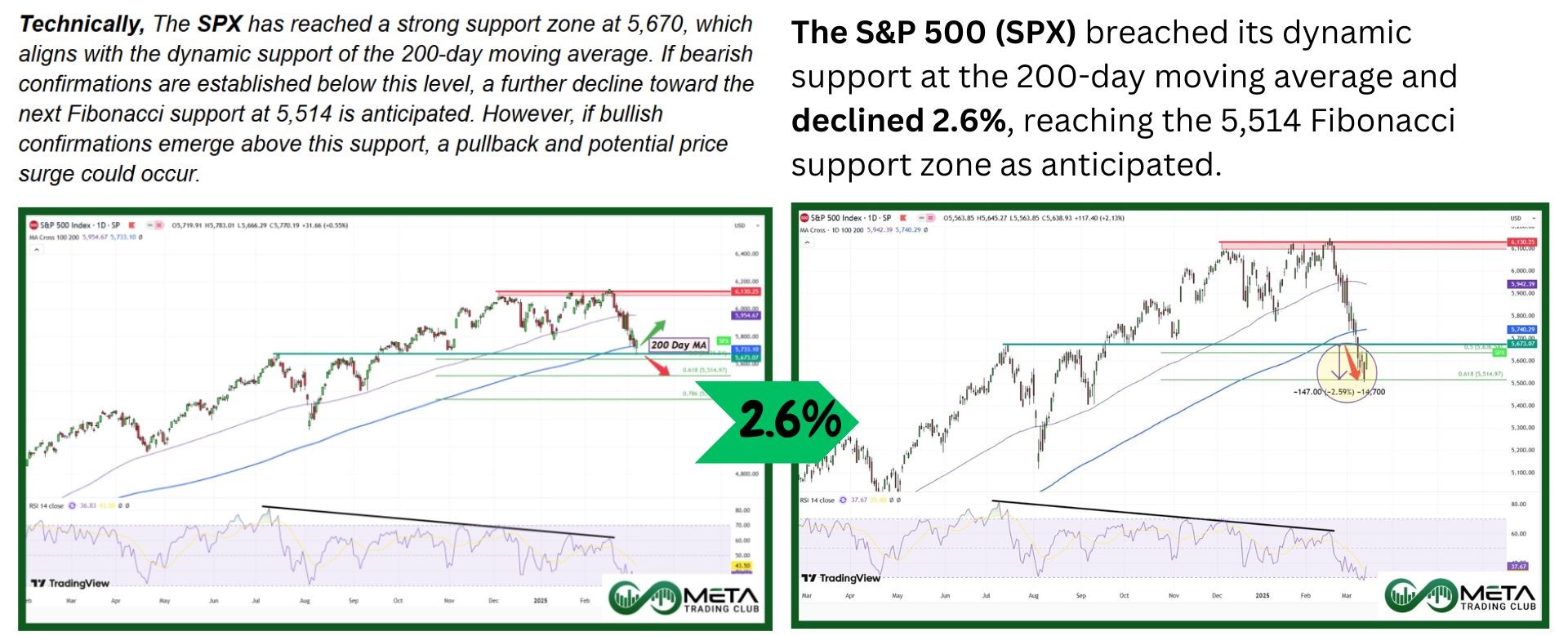

Technically, SPX has retraced to the 5514 level, which corresponds to the golden ratio in the Fibonacci retracement and is widely regarded as a robust support level. Currently in oversold territory, the index shows potential for a rebound from this support. However, if economic uncertainty leads to a breakdown of this level, the index could decline further to the next support at 5400.

Stocks

Sector’s Weekly Performance:

Source: Finviz

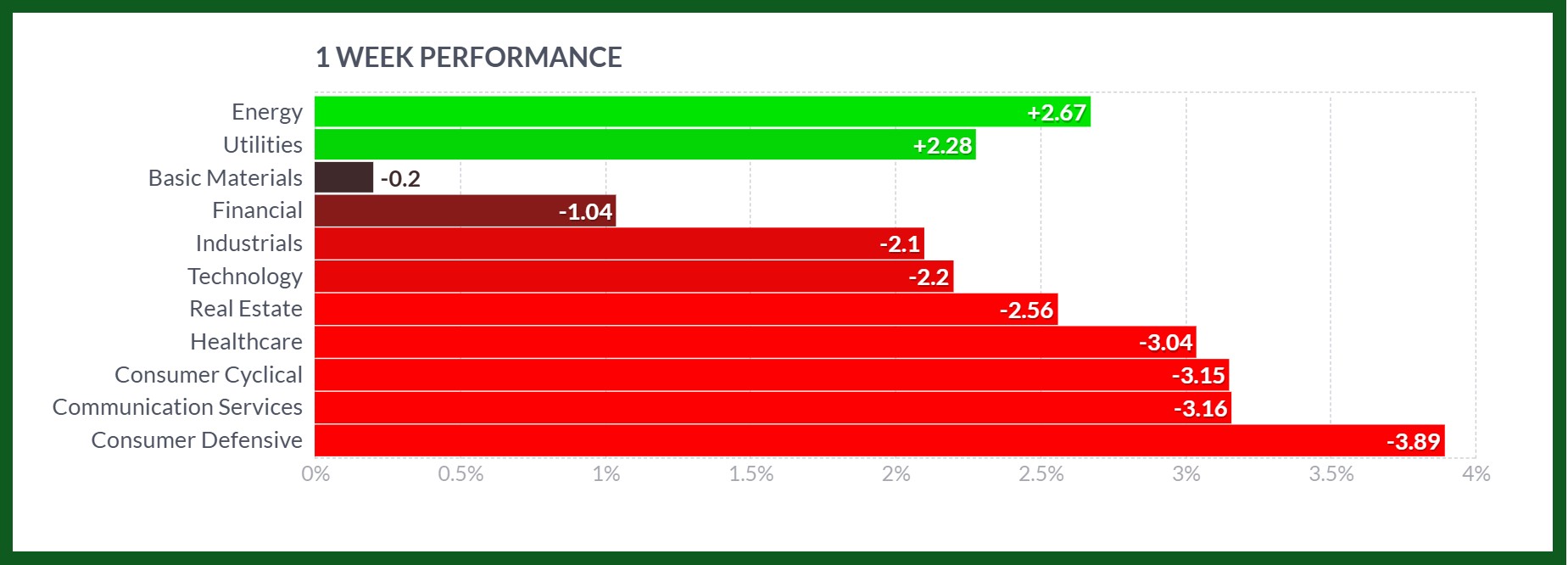

Over the past week, sector performance varied due to different market dynamics:

- Energy: Gained 2.7% due to rising oil prices and increased demand for energy stocks, driven by geopolitical tensions and supply concerns.

- Utilities: Rose 2.3% as investors sought safer, dividend-paying stocks amid market volatility.

- Financials: Dropped 1% as fears of high interest rates and tighter credit conditions weighed on banking and financial services.

- Industrials: Fell 2% due to concerns about supply chain disruptions.

- Technology: Lost 2.2% as higher interest rates made growth stocks less attractive, impacting tech valuations.

- Real Estate: Declined 2.5% due to high mortgage rates, which dampened demand for property investments.

- Healthcare: Dropped -3% as regulatory concerns from major companies affected investor sentiment.

- Consumer Cyclical: Fell 3% due to weaker retail sales data, signaling reduced consumer spending.

- Communication Services: Declined -3.16% affected by whole market sentiment.

- Consumer Defensive: Dropped 3.9%, the weakest performer, as inflation concerns, and higher costs pressured profit margins.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- Intel (INTC): Surged 16.5% due to positive investor confidence over the new CEO and joined U.S. delegation to Vietnam amid trade talks.

- ConocoPhillips (COP): Rose 9.2% following Odfjell technology secures contract with conocophillips.

- Micron (MU): Climbed 8.4% after Wells Fargo revises micron technology price target to $130.

- GE Vernova (GEV): Increased 8.4% as Petrovietnam Power wants to be partners with ge vernova for gas plant equipment

- Applovin (APP): Advanced 8.3% despite Applovin faces class action lawsuit over alleged securities fraud.

- NVIDIA (NVDA): Gained 8% as Nvidia’s GPU technology conference kicks off next week.

- CrowdStrike (CRWD): Rose 6.1% as it expands cybersecurity reach in Australia and New zealand.

- Boeing (BA): Jumped 5% due to news that the global drones market will surpass $60 billion by 2029.

- Berkshire Hathaway (BRK.B): Grew 3.8% as it held over $300 billion in cash and the market had fallen.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold hit a record high of $3,000 per ounce on Friday, driven by rising worries about risk and expectations of the U.S. Federal Reserve rate cuts. President Trump’s trade war escalated further, with him threatening a 200% tariff on European wine after the EU taxed American whiskey at 50%.

Economic data, showing slowing price growth in February, gave the Fed more flexibility to lower rates, making gold (a non-yielding asset) more attractive. Additional support for gold came from strong demand for gold-backed ETFs and ongoing central bank purchases, with China buying more for the fourth month in a row. For the week, gold prices climbed nearly 3%.

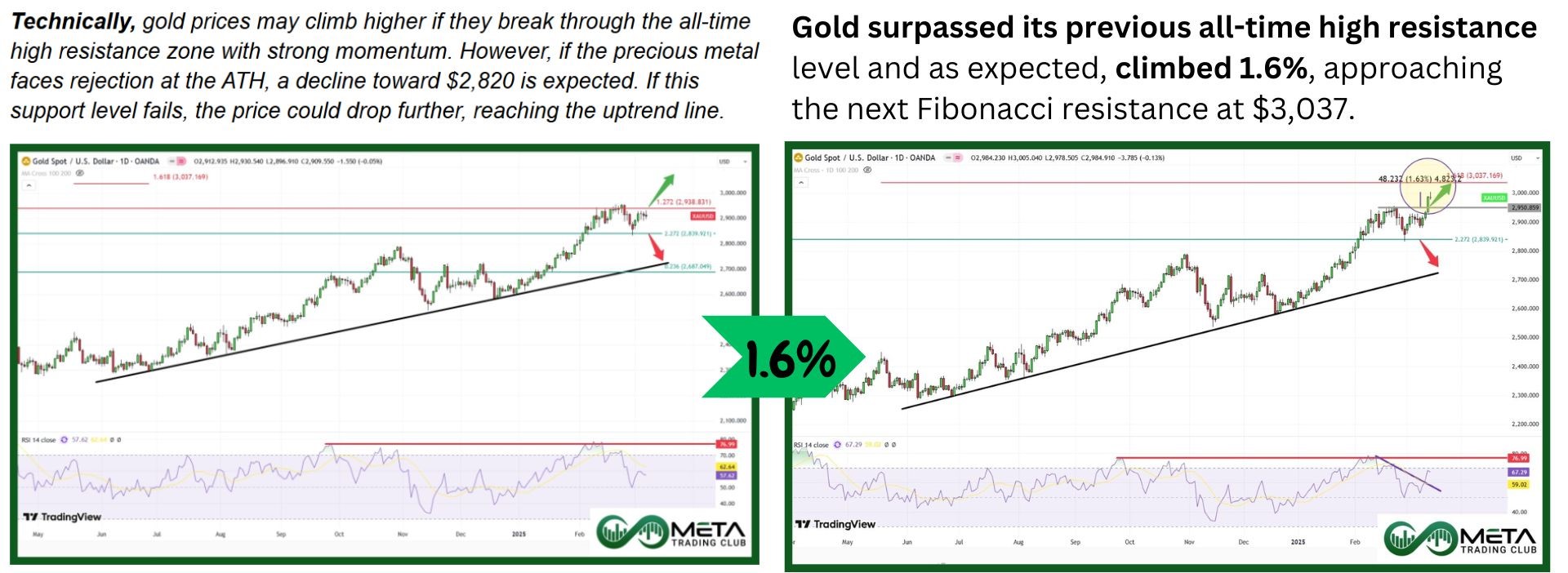

Technically, Gold prices have surpassed their previous all-time high resistance zone and are continuing to climb, approaching the $3037 level, which serves as a Fibonacci resistance zone.

WTI crude oil futures recovered slightly from a loss earlier in the week. Investors remain concerned about geopolitical uncertainties, such as the Ukraine war, China and Russia’s backing of Iran, and the expiration of a US energy sanctions license. While Russian President Putin has conditionally supported a ceasefire, hopes for a quick resolution are fading.

Economic factors are also affecting oil prices. The International Energy Agency warns of a growing oil surplus this year, as global demand growth slows and OPEC+ increases production. Despite these challenges, oil prices stayed relatively steady compared to last week’s levels.

Technically, Oil prices have reached a robust 4-year support zone. If this support is breached for any reason, a further decline toward lower support levels is expected. However, if bullish confirmations emerge on lower timeframes, the price could rebound from this support, potentially climbing back toward $70.

Forex

Weekly Performance of Major Foreign Exchange Pairs:

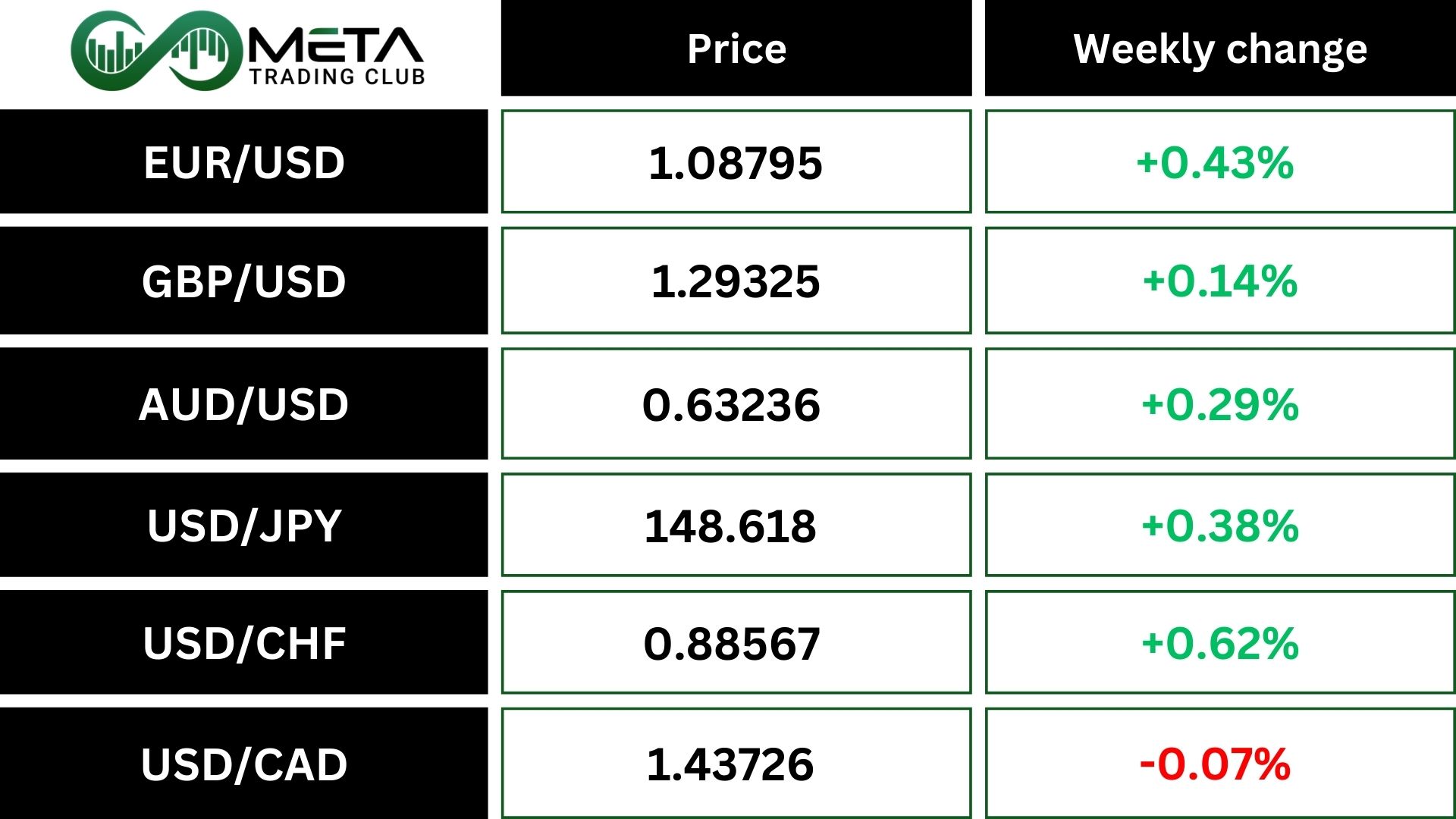

EUR/USD: The euro gained for the second straight week, rising against the dollar. This was driven by optimism over German fiscal reforms and expectations of steady ECB rates in April.

DXY: The dollar strengthened against the Swiss franc and against the yen. However, the dollar index fell 0.08%, marking its second consecutive week of losses, as inflation concerns and fiscal policy shifts weighed on sentiment.

USD/JPY: The yen weakened against the dollar for the week. Wage increases in Japan, the highest in 34 years, were a key focus, but the Bank of Japan is expected to maintain its current policy stance.

GBP/USD: The pound weakened against the dollar but still managed its second straight week of gains. This came despite a 0.1% contraction in the British economy in January.

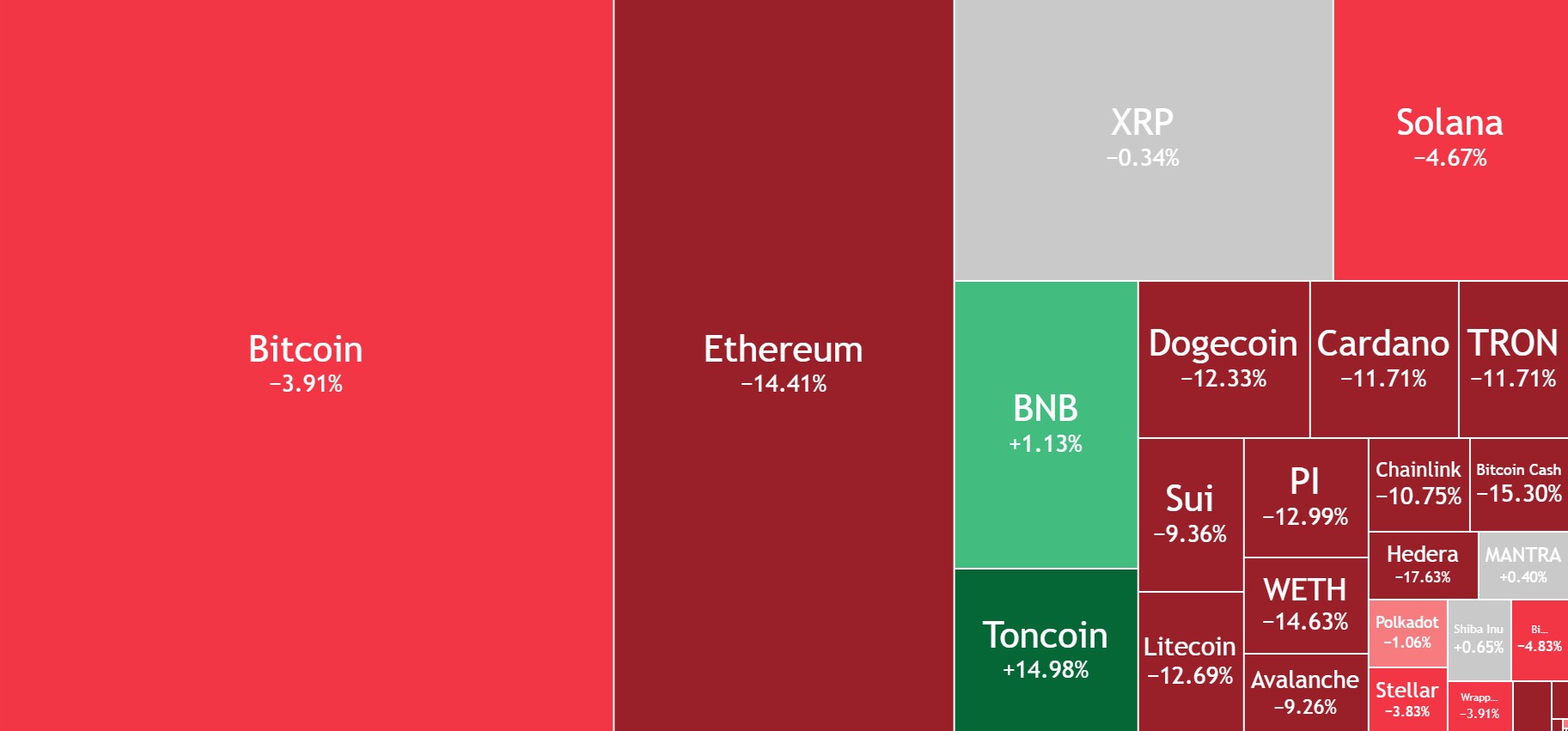

Crypto

Crypto Market Weekly Performance:

Source: Tradingview

Bitcoin dropped 22% from its all-time high of over $109,000 in January. This could be a temporary shakeout where prices drop before a quick recovery. Over the week, Bitcoin traded calmly around $82,000 after a volatile week that saw it dip to a four-month low of under $77,000 before recovering.

Toncoin surged over 20% following positive news about Telegram founder Pavel Durov, though it has slightly retracted.

Meanwhile, most altcoins, like XRP, DOGE, and ADA, are in the red. The total crypto market cap dropped by $30 billion and now sits below $2.840 trillion. Despite short-term fluctuations, Bitcoin’s dominance is close to 59%, and analysts remain optimistic about its long-term trajectory.

Technically, If bullish confirmations occur, BTC could rise toward the uptrend line. For further upward momentum, it must break the downtrend line with strong force. However, if the Fibonacci support near $80K fails, a further decline to the next Fibonacci support level is expected.

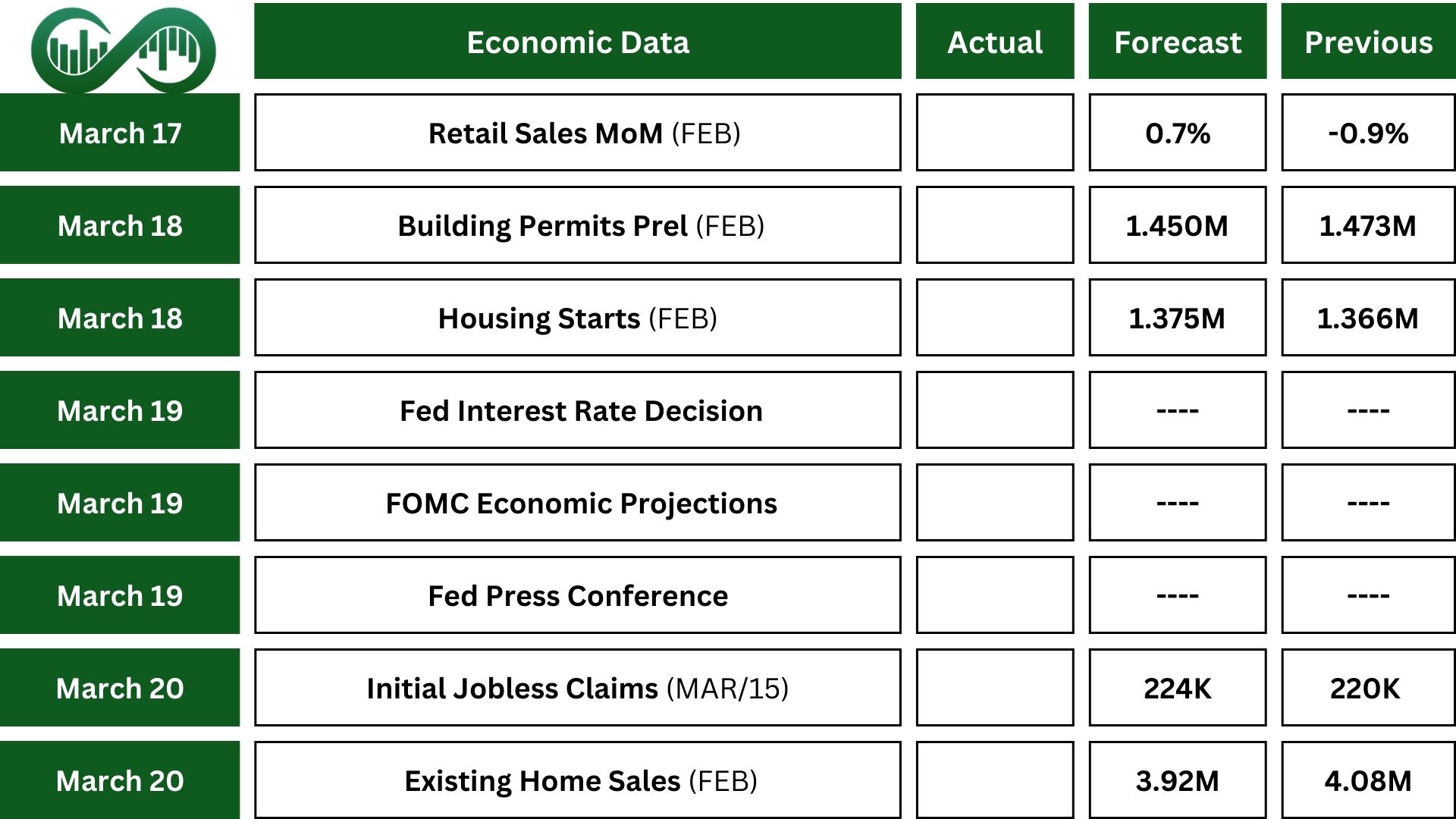

Next Week’s Outlook

Economic Events

This week, the Federal Reserve (FOMC) will make an important announcement about interest rates. They are expected to keep rates steady between 4.25% and 4.5%, continuing their pause on cutting rates, which started in January. The Fed will also share updated forecasts on key economic topics like growth, inflation, unemployment, and interest rates. Investors currently expect two small rate cuts this year.

In addition, February’s retail sales report will show how much consumers are spending, with a 0.7% increase predicted after a 0.9% drop in January. Other key updates will include data on industrial production, housing construction, home sales, export and import prices, and regional manufacturing trends. These reports will help give a clearer picture of the economy.

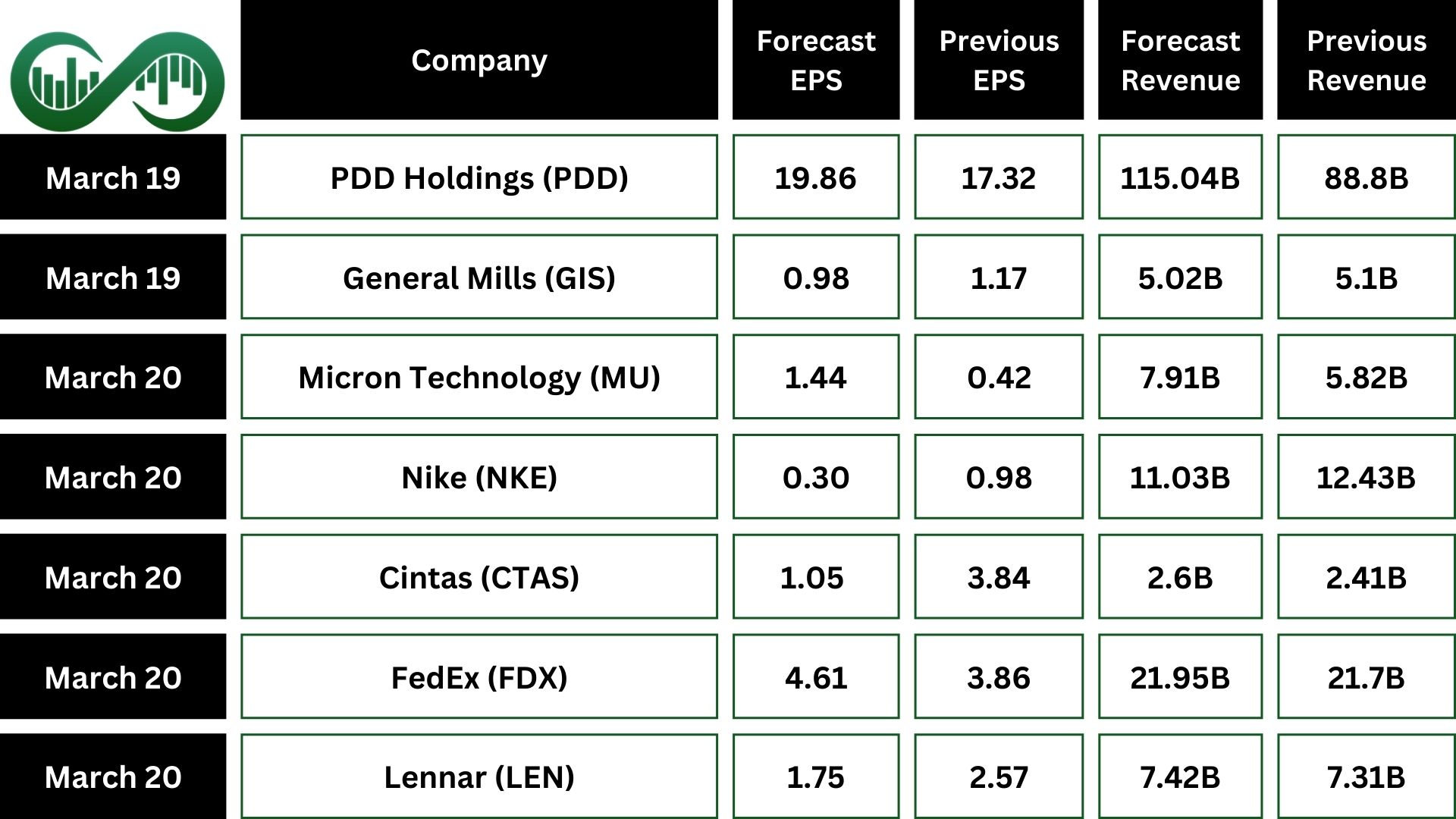

Earnings Events

On the corporate side, PPD Holdings (PDD), Micron (MU), Nike (NKE) and FedEx (FDX) will report their earnings.