Last Week’s report

Economic Reports

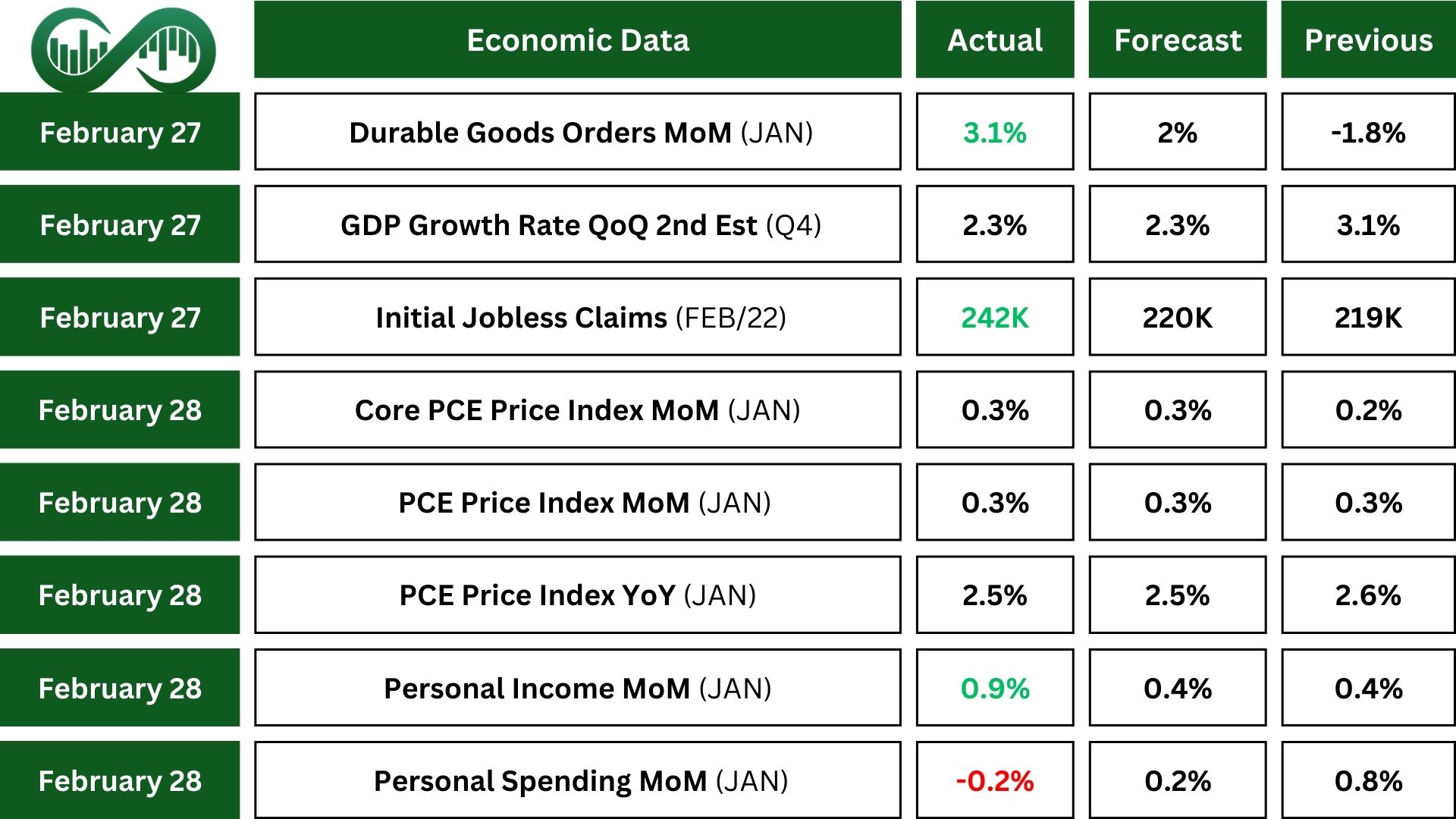

In January, U.S. orders for durable goods rose by 3.1% to $282.3 billion, the biggest jump in six months and better than expected. This could boost production, efficiency, and job growth, while increasing business confidence.

Unemployment claims in the U.S. rose sharply in late February, reaching 242,000, the highest in over two months. Continuing claims dropped slightly to 1,862,000, and 614 federal workers filed under a separate system. This points to a weakening job market.

In Q4 2024, the U.S. economy grew by 2.3%, its slowest pace in three quarters, down from 3.1% in Q3. Slower GDP growth might reduce consumer confidence and spending, impacting businesses reliant on sales.

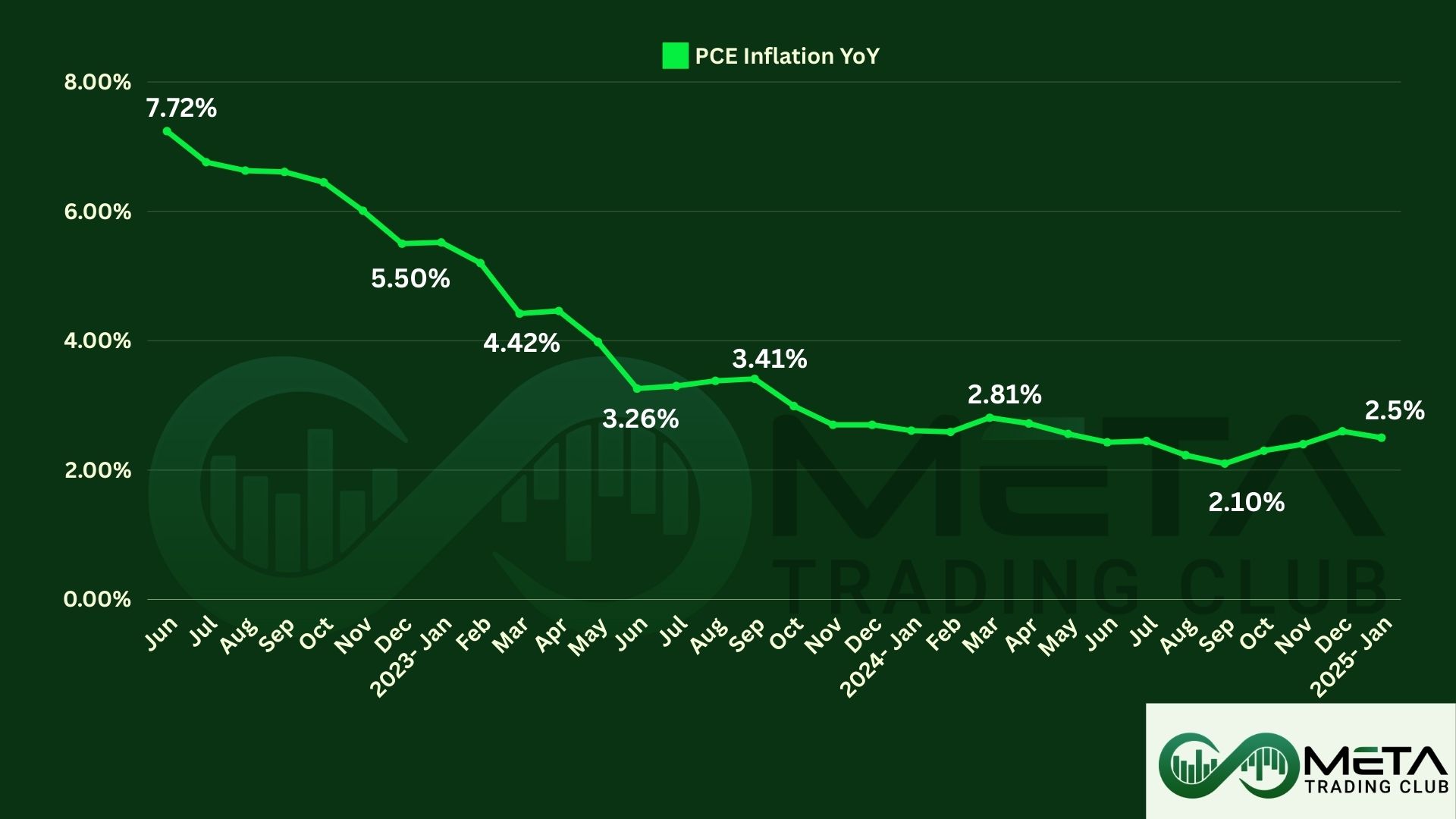

In January, U.S. personal income and disposable income both rose by 0.9%. Despite this, consumer spending fell by 0.2%. Meanwhile, the PCE price index increased by 0.3% monthly and 2.5% annually, remaining above the Federal Reserve’s 2% target. Both figures met expectations. These trends suggest ongoing inflation and potential challenges for economic growth, as consumer spending is a key GDP component.

Earnings Reports

Home Depot

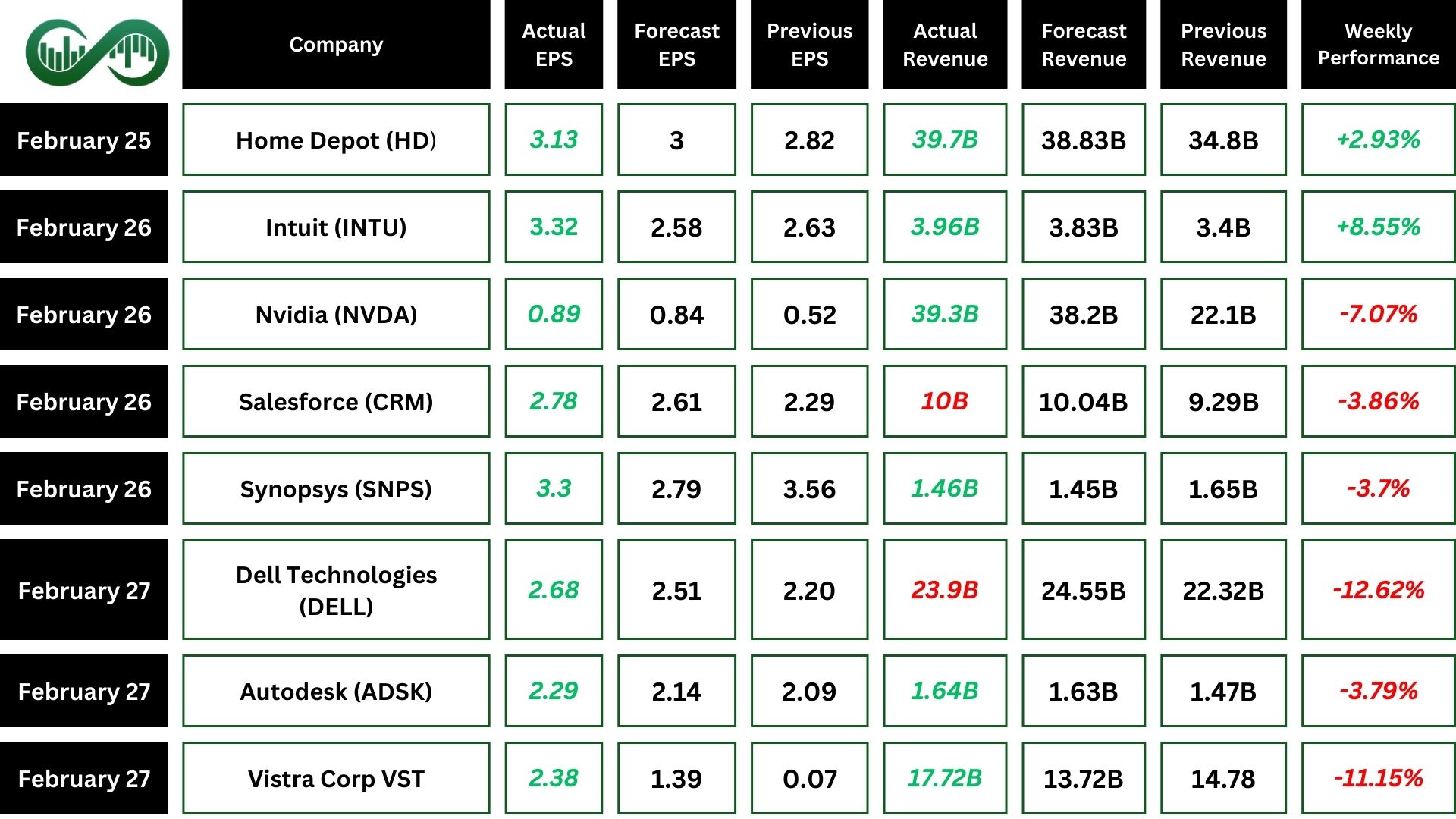

Home Depot (HD) Q4 revenue grew 14.1% to $39.7 billion, helped by an extra week in the quarter. U.S. sales increased by 1.3%, and net earnings were $3 billion, or $3.02 per share.

Also, adjusted earnings per share (EPS) were $3.13, beating expectations. The company also raised its dividend by 2.2% to $2.30 per share. Despite strong results, challenges like higher interest rates and economic uncertainty remain.

HD has been stuck in a triangle consolidation pattern, supported by a strong support zone. For the price to increase further, it needs to break through the downward trend line. However, if the stock loses this strong support, a further decline is anticipated.

Nvidia

Nvidia (NVDA) reported strong Q4 2025 results, with revenue up 78% and earnings up 80%, both exceeding expectations. Net income reached $20 billion.

Also, data center revenue set a record, rising 142% YoY, while automotive revenue grew 103% YoY. Gaming revenue declined by 11% YoY. Nvidia is partnering with Verizon on AI for 5G networks and collaborating with healthcare leaders on genomics and medical imaging AI.

Following the release of its fourth-quarter earnings results, Nvidia’s stock declined 8% and was supported from its long term uptrend line. NVDA is experiencing downward momentum and is currently within a consolidating triangle pattern. Breaking the short-term downward trendline could lead to a rise in price towards the strong resistance zone at $152. However, if the long-term upward trendline is broken, a future decline to the support zones is anticipated.

Salesforce

Salesforce (CRM) reported $10 billion in Q4 2025 revenue, an 8% increase, and $37.9 billion for FY25, up 9%. Operating cash flow hit a record $13.1 billion, up 28%. The company returned $9.3 billion to stockholders. However, lowered AI sales expectations led to a around 3% stock drop after disappointing guidance.

CRM broke through the strong resistance level of $320, but its momentum weakened, causing it to pull back to this level after a cautious outlook for the new fiscal year. The price has now dropped to the next Fibonacci support level at $291. If this support is lost, a further decline to $271 is anticipated.

Synopsys

Synopsys (SNPS) reported $1.46 billion in first-quarter revenue, just under estimates. There’s strong demand for its software, especially for AI chip design, with partners like Nvidia and Intel. It forecasts higher second-quarter revenue and earnings. Synopsys is also acquiring Ansys in a $35 billion deal, pending regulatory approval.

SNPS has reached strong support at $450, and following an above-estimate earnings report, a catalyst could drive the price higher from this point. However, this strong support of $450 breaks, further decline anticipated toward $420.

Indices

Indices’ Weekly Performance:

On Friday, U.S. stocks ended higher, but for the week, the S&P 500 fell 1%, the Nasdaq dropped 3.3%, while the Dow gained about 1%.

The market briefly dipped due to rising geopolitical concerns and Trump’s tariff threats, which added uncertainty for Big Tech. Economic data was mixed: core inflation eased by 0.3%, while consumer spending dropped by 0.2% in January.

S&P 500 and Nasdaq had their worst monthly declines since April 2024 and September 2023, respectively, with the S&P 500 down 1.4%, the Nasdaq down 4%, and the Dow down 2.2%.

The SPX indicates the S&P 500 is trending upwards, but the momentum is weakening. It’s being held up by a short-term upward trend line, but it’s currently in a consolidation phase. If the index breaks through its support levels, a further decline is expected. For the price to rise significantly, the index must break through its all-time high (ATH) resistance with strong momentum.

The NDX has reached a strong support level at 20,420. If the price falls below this support, the index could drop to 19,900. However, if the momentum is strong, the index might bounce back from this support level.

Stocks

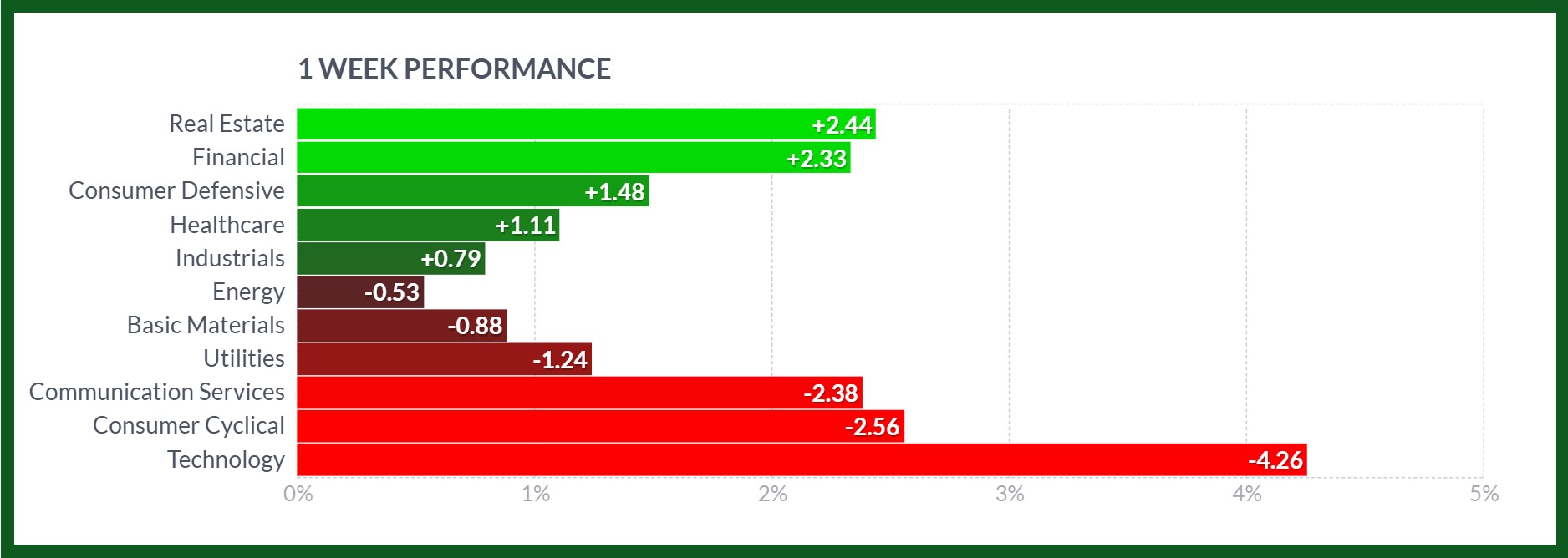

Sector’s Weekly Performance:

Source: Finviz

Stock Market Weekly Performance:

Last week, the Real Estate sector saw the biggest gain, going up by 2.4%, followed by the Financial sector, which increased by 2.3%.

Other sectors that did well include Consumer Defensive, Healthcare, and Industrials. These gains suggest that investors were more interested in stable and less risky sectors, possibly due to ongoing economic uncertainties or good news within those industries.

On the flip side, the Technology sector experienced the largest drop, falling by 4.3%. The Consumer Cyclical sector also dropped by 2.5%, followed by Communication Services (fell 2.4%), Utilities, Basic Materials, and Energy. The decline in the Technology sector might be due to profit-taking after previous gains, worries about tariffs and disappointing earnings outlooks.

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- Intuit (INTU): Surged 8.55% due to strong quarterly earnings, positive guidance and updates to their TurboTax or QuickBooks software.

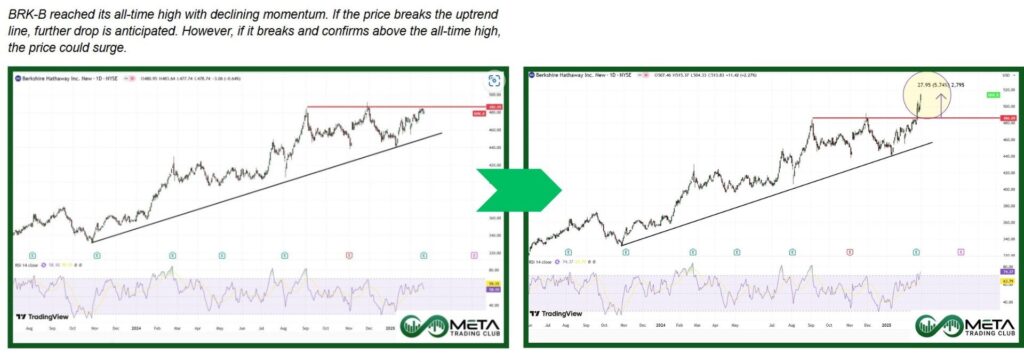

- Berkshire Hathaway (BRK.B): Up 7.33% due to strong quarterly performance in its diverse portfolio of businesses and positive market sentiment.

- Progressive (PGR): Increased 5.94% due to favorable industry conditions in the insurance sector.

- Eli Lilly (LLY): Up 5.37% after the company said Jaypirca recommended for EU approval to treat leukemia.

- Walt Disney (DIS): Rose 4.73% after announcement that Disney’s ESPN BET might close in 2026, following concerns raised by Penn Entertainment.

- Visa (V): Surged 4.07% due to positive investors confidence.

- Walmart (WMT): Up 4.04% due to solid performance and positive market sentiment towards retail giants.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold prices fell to $2,850 per ounce, heading for their biggest weekly drop since November, due to a stronger dollar and limited expectations for Fed rate cuts amid high inflation.

A surprising 0.2% drop in consumer spending, the first in nearly two years, and a 0.9% surge in income, the largest increase in a year, added to market concerns.

Attention shifted to US trade policy as President Trump confirmed 25% tariffs on Mexican and Canadian goods starting March 4, alongside a 10% duty on Chinese imports, and threatened 25% tariffs on EU goods.

For the week, gold lost 2.7% after eight consecutive weeks of gains, though it still rose 1.4% in February.

Technically, Gold is moving upwards overall, but it recently dropped from its all-time high. If it breaks below the $2,840 support level, it could decline even further.

WTI crude oil futures fell 0.9% last week, their first monthly decline since November. The drop was due to geopolitical tensions and economic uncertainty, including a heated argument between U.S. President Donald Trump and Ukrainian President Volodymyr Zelenskiy, which raised concerns about the Russia-Ukraine conflict.

Traders were also worried by Trump’s announcement of new tariffs on goods from Mexico, Canada, and China, leading to fears of weaker global demand. Investors were uncertain about the U.S. administration’s energy policies.

Additionally, Iraq planned to restart oil exports from Kurdistan, but international companies hesitated due to unresolved payment issues.

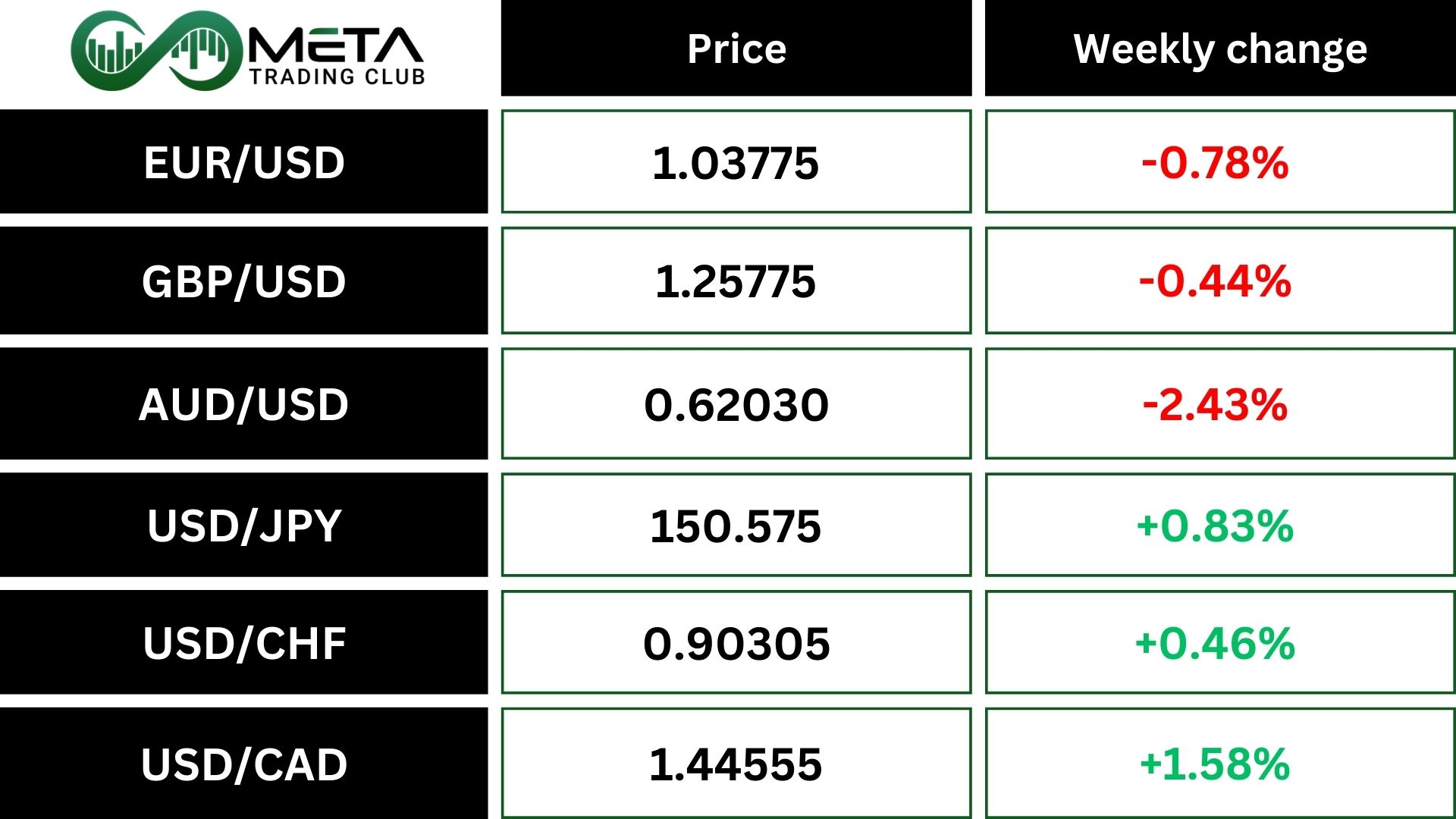

Forex

Weekly Performance of Major Foreign Exchange Pairs:

DXY: The dollar index rose a bit last week. Traders looked at the latest PCE report and new tariffs. PCE prices met expectations, easing inflation worries a bit. Personal income went up, but spending went down. This data supported the idea of two Fed rate cuts this year.

Also, trade tensions rose with new US tariffs on Mexican, Canadian, and Chinese imports.

EUR/USD: President Trump suggested a possible US-UK trade deal without tariffs and hinted at new EU tariffs. The dollar fell about 1% for the month. Also, January Eurozone inflation expectations dropped to 2.6% for the next year and stayed at 2.4% for three years. Inflation rates fell to 3.4%. Lower-income groups expected slightly higher inflation, while younger people predicted less than older ones. Because of these factors, the euro lost value against the dollar last week.

Crypto

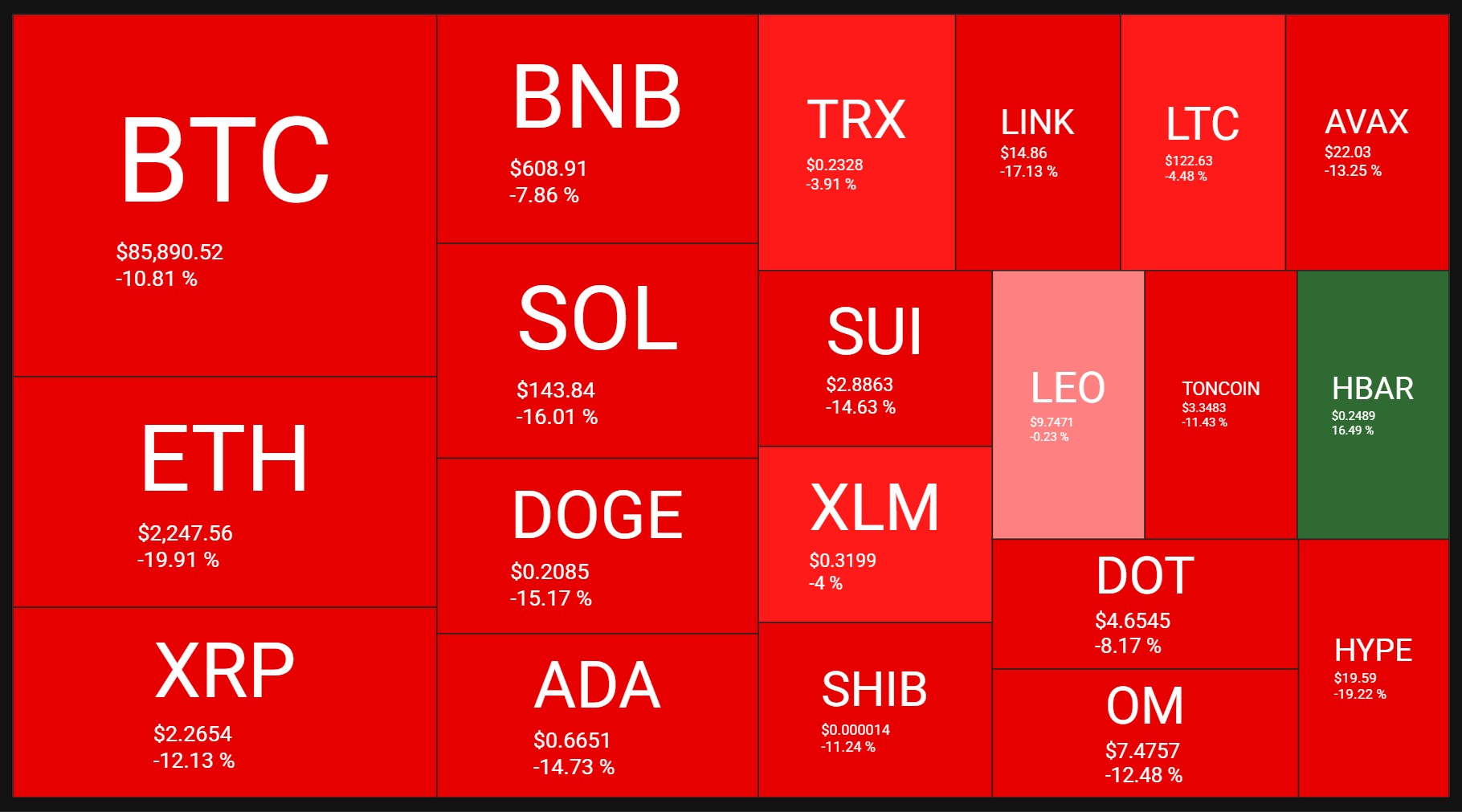

Crypto Market Weekly Performance:

Source: quantifycrypto

Bitcoin prices dropped sharply on Monday, falling 8% to $78,000, down nearly 30% from their record high of $109,000. The decline followed new tariffs and uncertainties, erasing all gains since the election. However, the crypto community had been hopeful about Trump’s promises for the industry.

For Bitcoin to rise further, it needs to break out the short-term downward trend line with strong momentum (RSI downtrend line break).

Other cryptocurrencies like Ethereum and XRP also saw significant drops. Traders are waiting for updates from the White House and favorable economic data.

Today’s news: President Trump announced that the President’s Working Group on Digital Assets will include XRP, Solana, and Cardano in the crypto strategic reserve. Later, Bitcoin and Ether were also added, described as being central to the reserve.

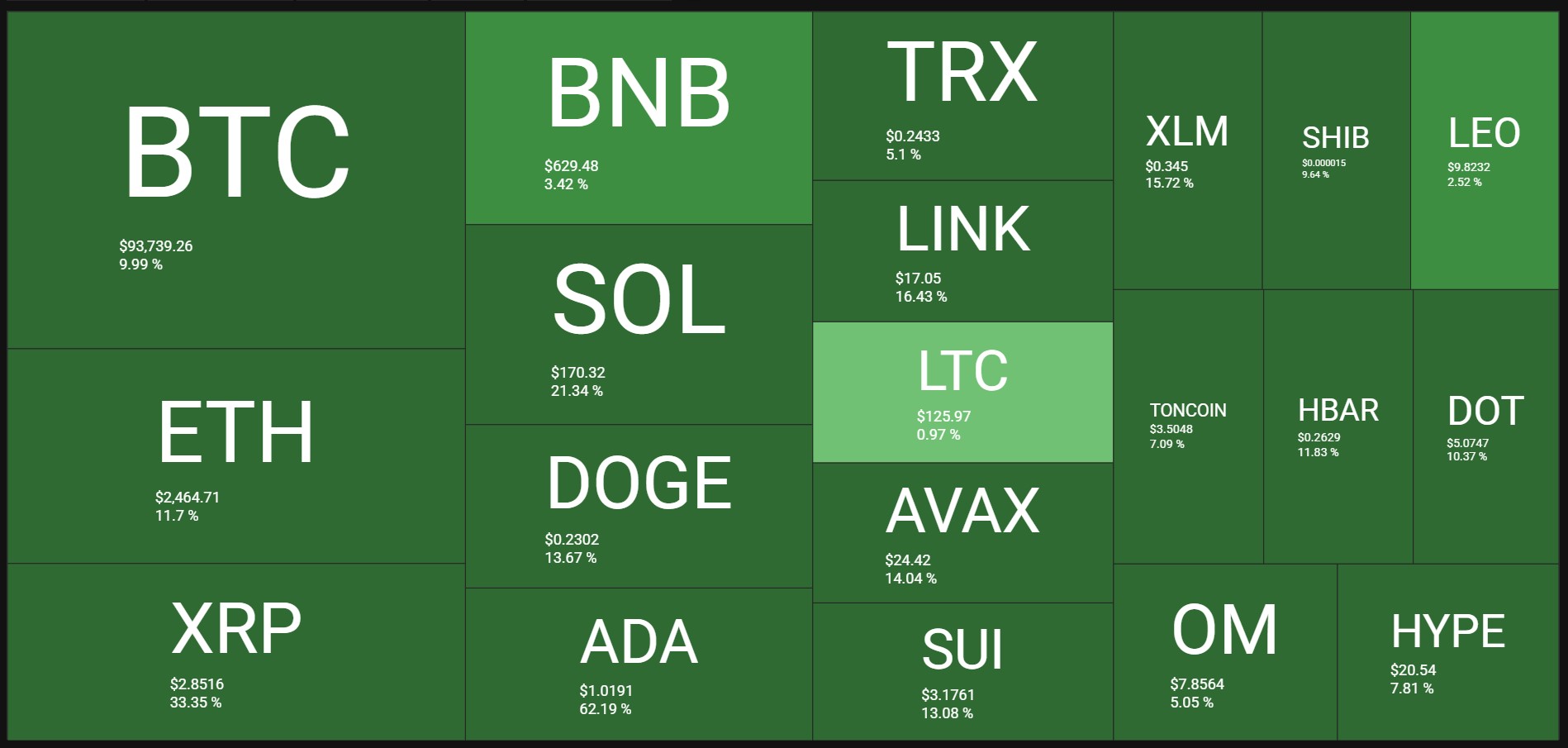

Today’s crypto market performance after this news:

Next Week’s Outlook

Economic Events

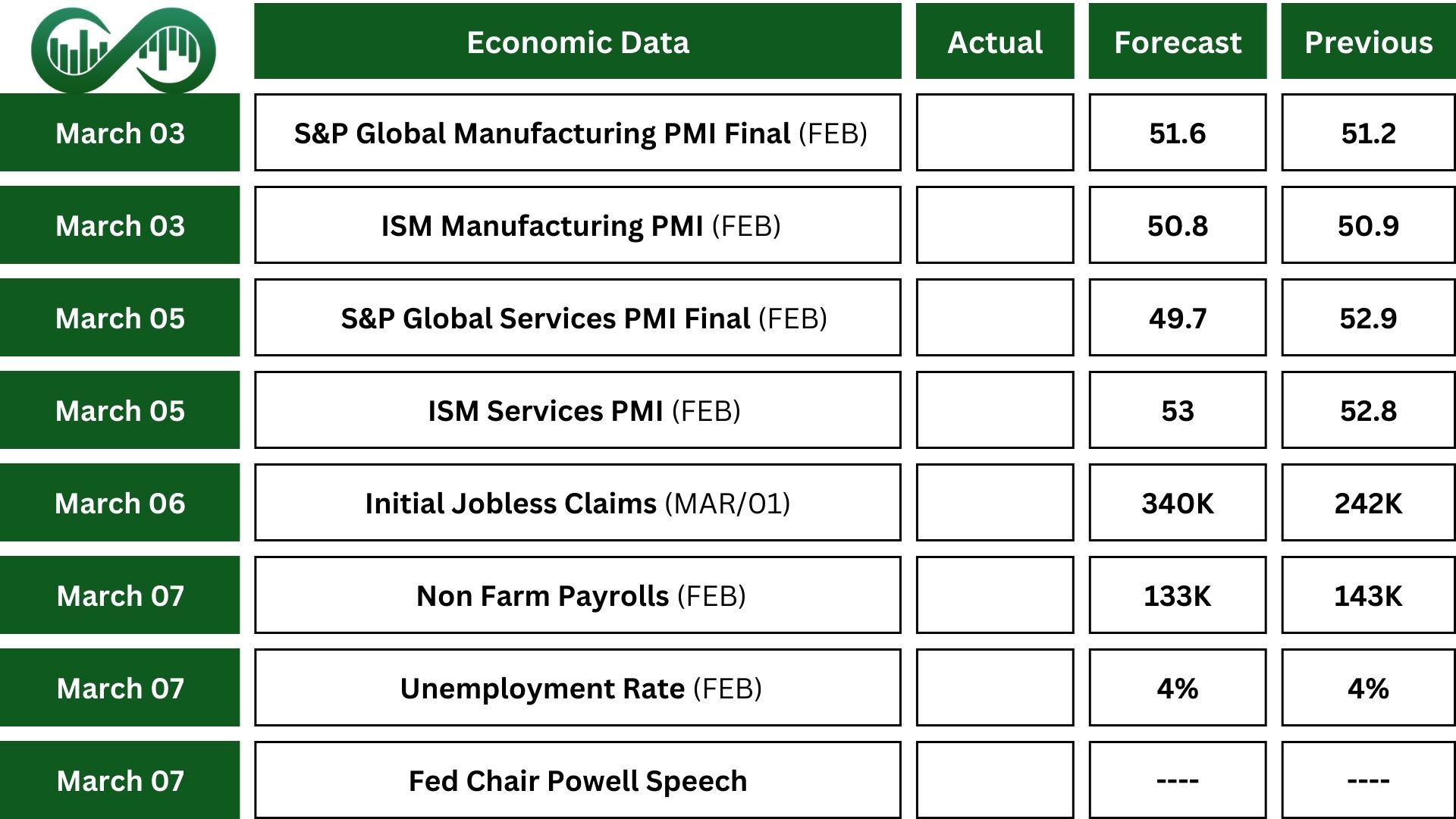

The US jobs report is the main focus. The economy is expected to have added 133,000 jobs in February, the lowest in four months. The unemployment rate is likely to stay at 4%, and wage growth is expected to slow down to 0.2% from 0.5%.

Other important labor market updates include the ADP Employment Change, Challenger job cuts, and final readings on productivity and unit labor costs.

The ISM Manufacturing PMI is expected to show a slight slowdown in factory growth, while the ISM Services PMI may indicate stronger expansion. Factory orders are likely to have rebounded by 1.5% after a 0.9% drop in January.

Traders will also watch final S&P Global PMIs, trade data, and speeches from several Fed officials, especially Chair Powell’s address at the 2025 US Monetary Policy Forum at the University of Chicago Booth School of Business.

Earnings Events

The earnings season is nearly over but results from Broadcom (AVGO) and Costco Wholesale (COST) are still important.