Last Week’s report

Economic Reports

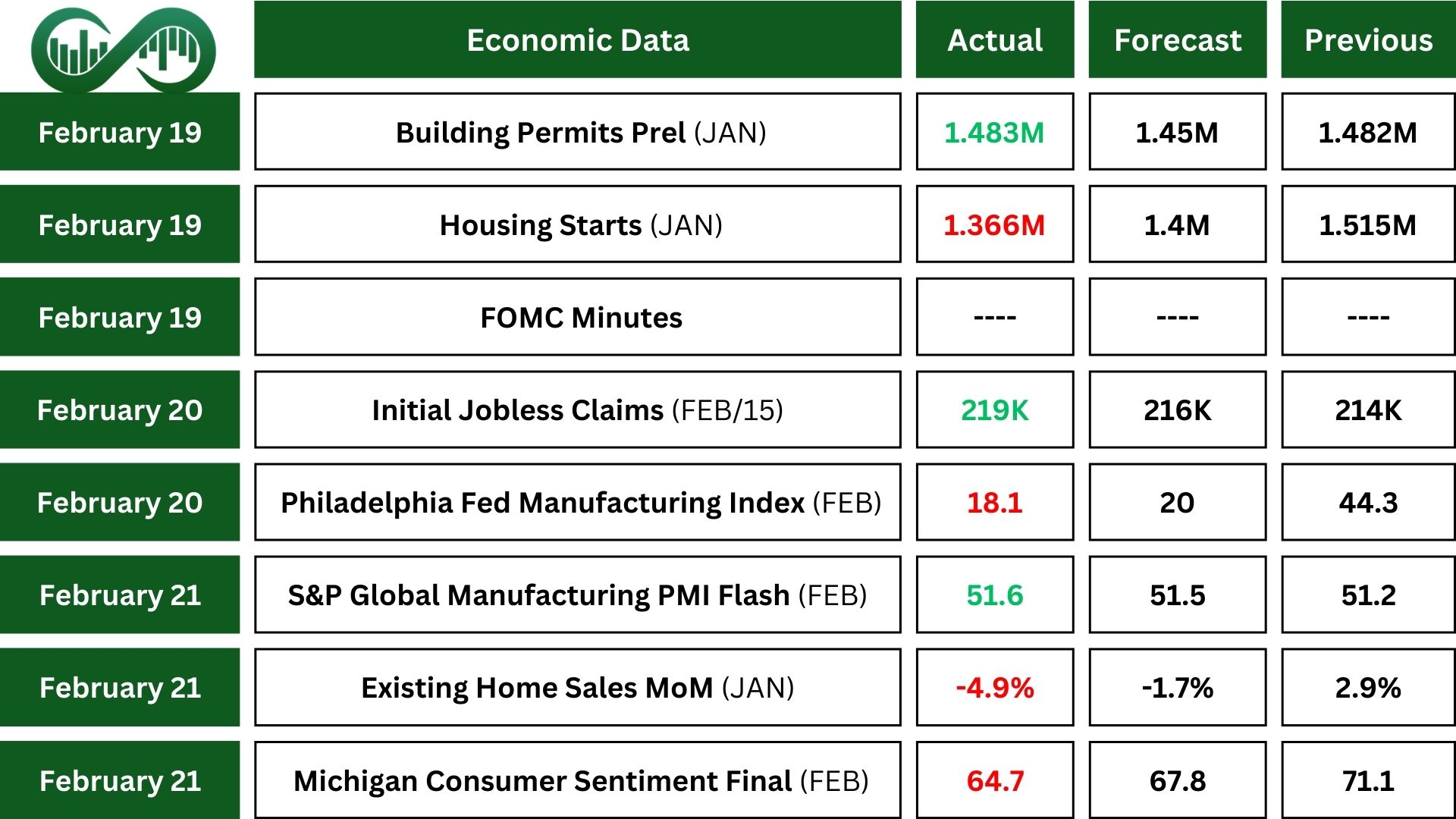

Building Permits: In January, building permits in the US slightly increased by 0.1% to an annual rate of 1.483 million, which is higher than the expected.

Housing Starts: Housing starts in the US dropped by 9.8% in January. This decline was greater than expected, as severe snowstorms and cold temperatures disrupted construction. Rising costs from import tariffs and high mortgage rates could also limit any recovery.

Existing Home Sales: US existing home sales fell by 4.9% in January, the biggest drop in seven months, missing market expectations. Despite interest rate cuts by the Federal Reserve, mortgage rates remained high, and with elevated home prices, housing affordability continues to be a major issue.

Fed Minutes: The Fed’s January 2025 meeting minutes showed that policymakers agreed to be cautious with changes to monetary policy due to high uncertainty. Many officials suggested keeping interest rates high if the economy and inflation remain strong. But they could lower rates if the job market weakens, the economy slows, or inflation drops faster than expected. The Fed kept the interest rate at 4.25%-4.5% in January, pausing rate cuts after three reductions in 2024.

Jobless Claims: Initial jobless claims in the US increased to 219K for the week ending February 15th, which was higher than expected. Continuing claims were close to expectations at 1,869K. The data shows the labor market remains tight despite some softening. Federal employees fired by the new Department of Government Efficiency are not included in the state claims data.

Consumer Sentiment: The University of Michigan consumer sentiment for the US dropped to 64.7 in February, the lowest since November 2023. This decline affected all age, income, and wealth groups, mainly due to fears of rising prices from tariffs.

Inflation expectations for the year ahead rose to 4.3%, the highest since November 2023.

Earnings Reports

Walmart

Walmart (WMT) Q4 2024 earnings showed strong performance, with revenue rising by 5.3% year-over-year to $182.6 billion and adjusted earnings per share increasing by 10% to $0.66.

However, the stock dropped by up to 7% due to cautious guidance for fiscal 2026. Walmart US same-store sales grew by 4.6%, and US e-commerce sales increased by 20% year-over-year.

The Walmart+ subscription service saw double-digit growth, and the US grocery business achieved mid-single-digit same-store sales growth. For the full year, Walmart’s net sales rose by 5.6% to $684.2 billion.

WMT fell from its all-time high and reached the uptrend line. If the price breaks this trend line, further decline is anticipated.

Berkshire Hathaway

Berkshire Hathaway (BRK.B) saw its operating earnings jump by over 70% in Q4 2024, reaching $14.53 billion, up from $8.48 billion in the same period last year.

For the entire year, the company’s operating earnings rose by 27% to $47.44 billion compared to $37.35 billion in 2023. This growth was driven by increase in insurance underwriting earnings and a nearly 50% rise in insurance investment income. By the end of 2024, Berkshire’s cash holdings reached a record $334.2 billion. However, over half of Berkshire’s 189 operating businesses reported a drop in earnings.

BRK-B reached its all-time high with declining momentum. If the price breaks the uptrend line, further drop is anticipated. However, if it breaks and confirms above the all-time high, the price could surge.

Arista Networks

Arista Networks (ANET) had strong Q4 2024 earnings. Their revenue increased by 25.3% from last year, reaching $1.93 billion. The company’s earnings per share for the quarter were $0.65.

They had an operating income of $907.1 million and a net income of $830.1 million. For the whole year, Arista’s revenue was $7 billion, which is a 19.5% increase from 2023. Their operating margin for 2024 was 47.5%. Despite the positive results, Arista’s shares went down after earnings were released.

ANET reached a strong dynamic support (uptrend line). The price could find reverse from here, but if it loses the uptrend, further decline is anticipated.

Indices

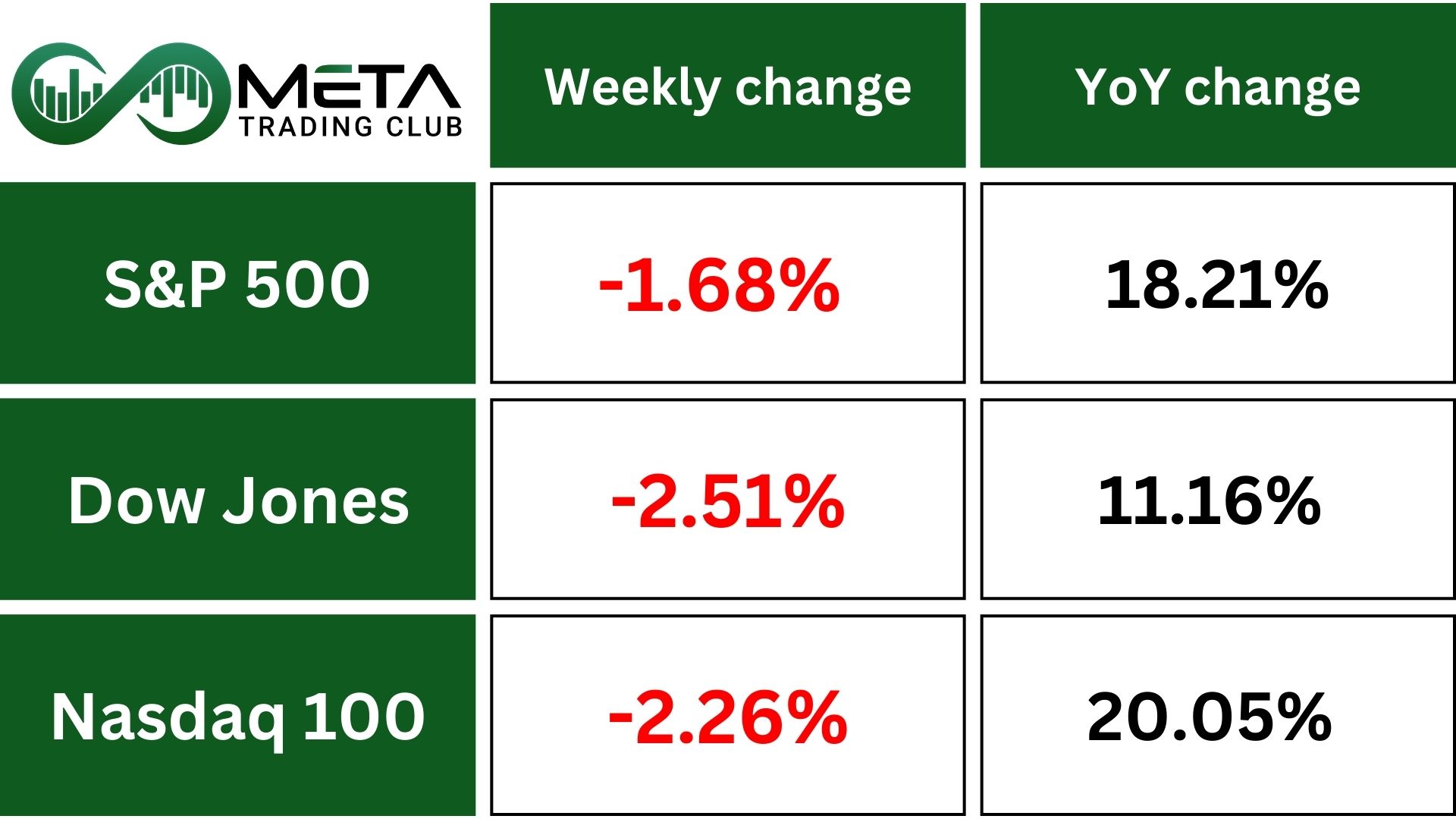

Indices’ Weekly Performance:

US stocks plunged last week due to concerns about a slowing economy and persistent inflation, leading investors to seek safer assets. For the week, the S&P 500 fell 1.6%, the Dow dropped 2.5%, and the Nasdaq slipped 2.4%, marking its biggest loss of the year.

UnitedHealth shares dropped 7.2% due to a Department of Justice investigation, making it the worst-performing Dow component. Consumer sentiment also declined, with the University of Michigan’s index falling to 64.7. Walmart’s disappointing outlook and fears over President Trump’s tariff policies added to the decline.

S&P 500 Index is in an uptrend but faces challenges at the resistance level of ATH. A break above this level could lead to further gains, while a break below the dynamic support (uptrend line) could indicate a trend reversal. You should monitor these key levels for potential future movements.

Stocks

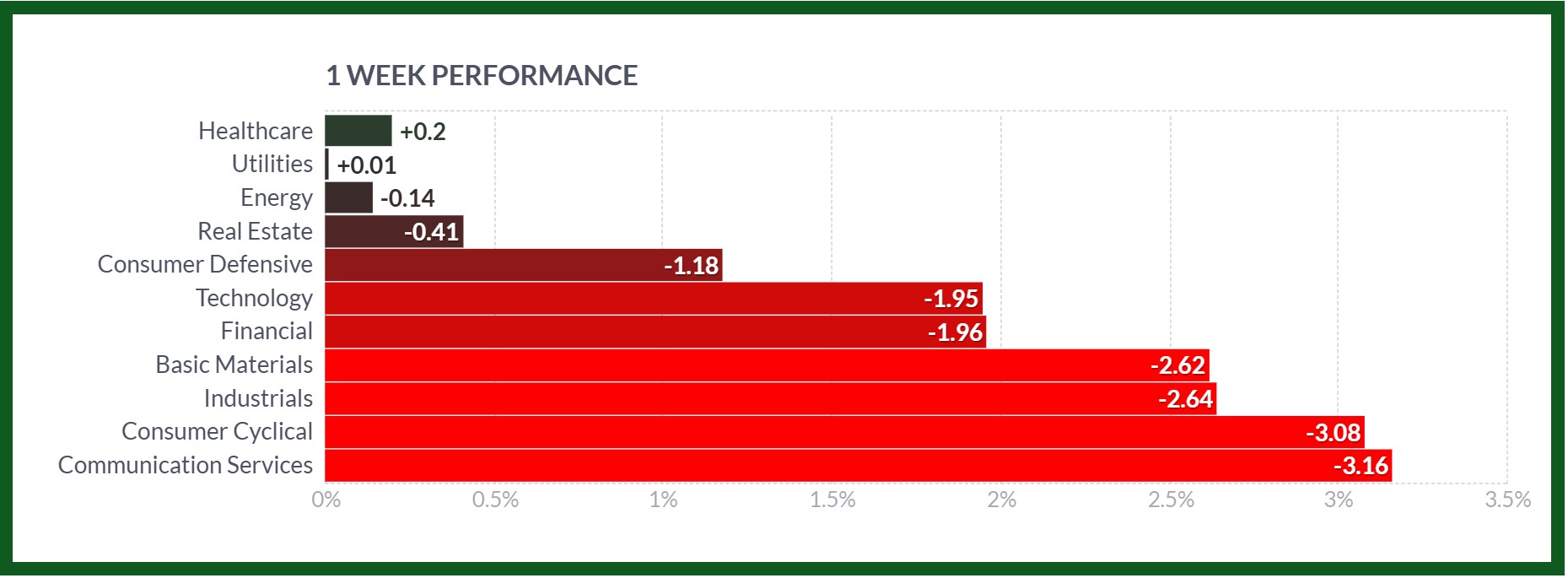

Sector’s Weekly Performance:

Source: Finviz

Over the past week, the Healthcare and Utilities sectors saw slight gains, increasing by 0.2% and 0.01% respectively, due to strong earnings and stable demand.

Conversely, the Communication Services and Consumer Cyclical sectors experienced significant declines of 3.16% and 3.08%, driven by weaker concerns about economic growth.

Other sectors like Technology, Financial, and Basic Materials also faced declines due to global demand concerns.

Overall, investor sentiment reflected cautiousness amidst economic uncertainties and sector-specific challenges.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- MercadoLibre (MELI): Surged 7% due to strong quarterly earnings that exceeded expectations, driven by growth in e-commerce and fintech segments in Latin America.

- PDD Holdings (PDD): Increased 5.6% after Chinese tech stocks in Hong Kong rose and marked their best weekly streak since 2020, driven by earnings surprises and optimism about the AI sector drawing attention from global investors.

- Moderna (MRNA): Climbed 5.3% after announcing Chinese researchers find bat virus enters human cells via the same pathway as COVID.

- Kenvue (KVUE): Rose 4.2% due to strong financial performance and a positive outlook, bolstered by strategic initiatives and successful product launches.

- The Hershey (HSY): Increased 4.1% thanks to higher-than-expected earnings and revenue, driven by effective cost management and strong product demand.

- Mondelez (MDLZ): Gained 4% due to solid quarterly results and optimistic future guidance, focusing on expanding its product portfolio and market share in emerging markets.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold stayed close to its record high at $2,930 per ounce and was set for its eighth weekly gain due to its safety appeal. President Trump announced new tariffs on several goods, increasing trade tensions.

Reports also suggested that Trump might pull US support for Ukraine, raising geopolitical risks. US Treasury Secretary Scott Bessent denied revaluing government gold holdings. Swiss customs data showed gold exports to the US reached their highest in over 13 years in January.

WTI crude oil futures set 0.5% weekly decline. Concerns over Russian supply disruptions supported prices, while uncertainty over a potential Ukraine peace deal added to the mix. Supply issues intensified after Russia reported a significant reduction in Caspian Pipeline Consortium oil flows due to a Ukrainian drone attack, but Kazakhstan achieved record-high output despite export route damage.

US crude inventories increased, while gasoline and distillate stocks fell due to refinery maintenance. Analysts expect cold US weather and increase industrial activity in China to boost oil demand soon.

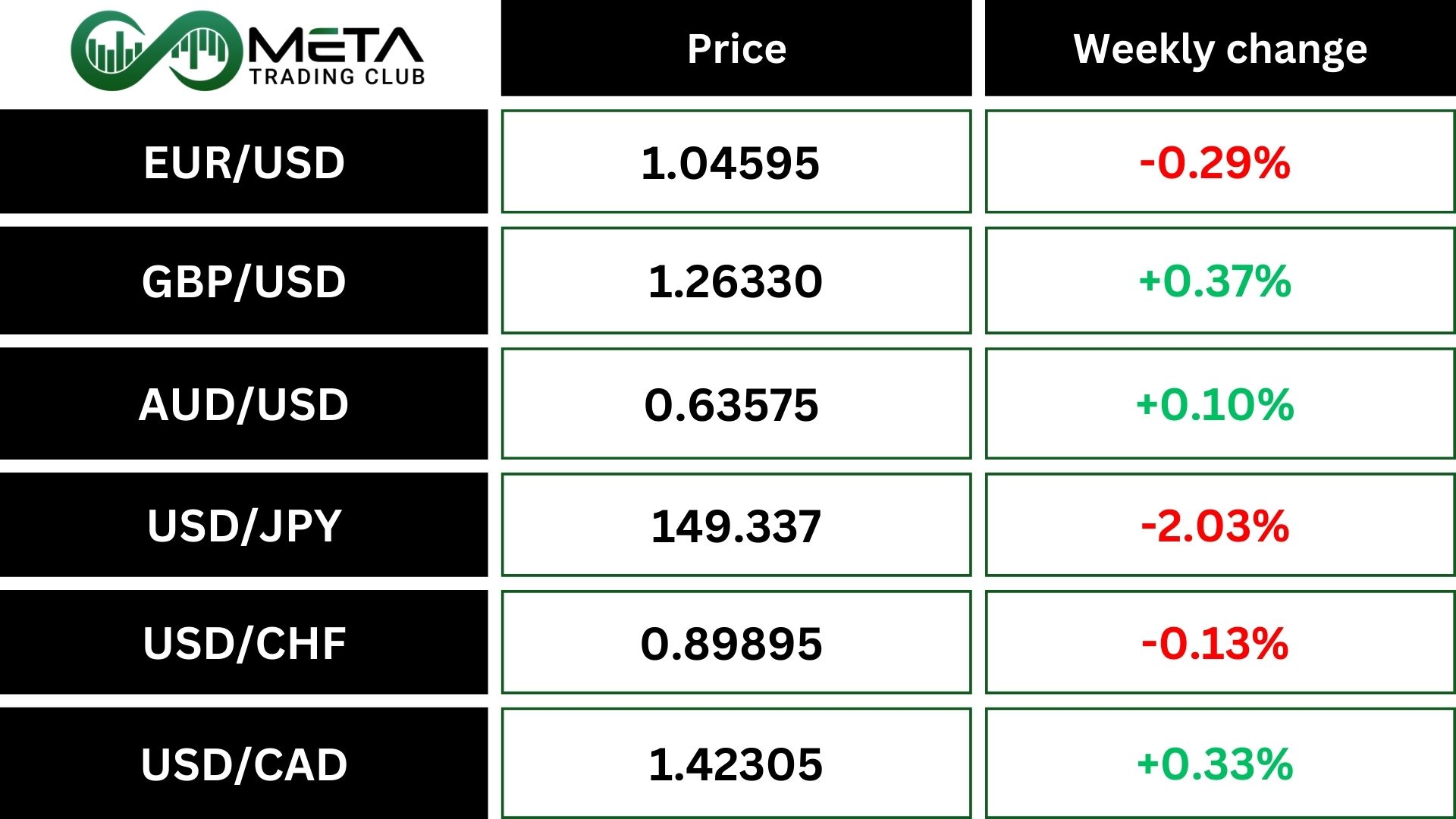

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The dollar index dropped and is set for a third weekly decline because of weaker US business sentiment. Flash PMI data showed business growth nearly stopped in February, with a drop in services offsetting a small manufacturing rebound. Concerns over aggressive US trade policies eased with limited tariffs from President Trump, reducing inflation risks and giving the Fed more room for rate cuts. FOMC minutes showed cautious policymakers, not rushing to ease policy due to economic uncertainty.

The British pound was up 0.5% for the week, hitting the highest point since December 17 after higher-than-expected inflation. UK retail sales beat expectations, and the UK had a budget surplus of £15.4 billion in January, though it was lower than estimated. Consumer confidence remained negative but showed improvement in February.

The Japanese yen fell despite higher-than-expected inflation figures. Core inflation rose to 3.2% in January, while headline inflation increased to 4%, the highest in two years. Bank of Japan Governor Kazuo Ueda mentioned that rising interest rates could improve financial institutions’ profits and stated that the central bank is ready to act if market shifts occur. BOJ board member Takata noted that real interest rates are deeply negative, implying potential future policy adjustments.

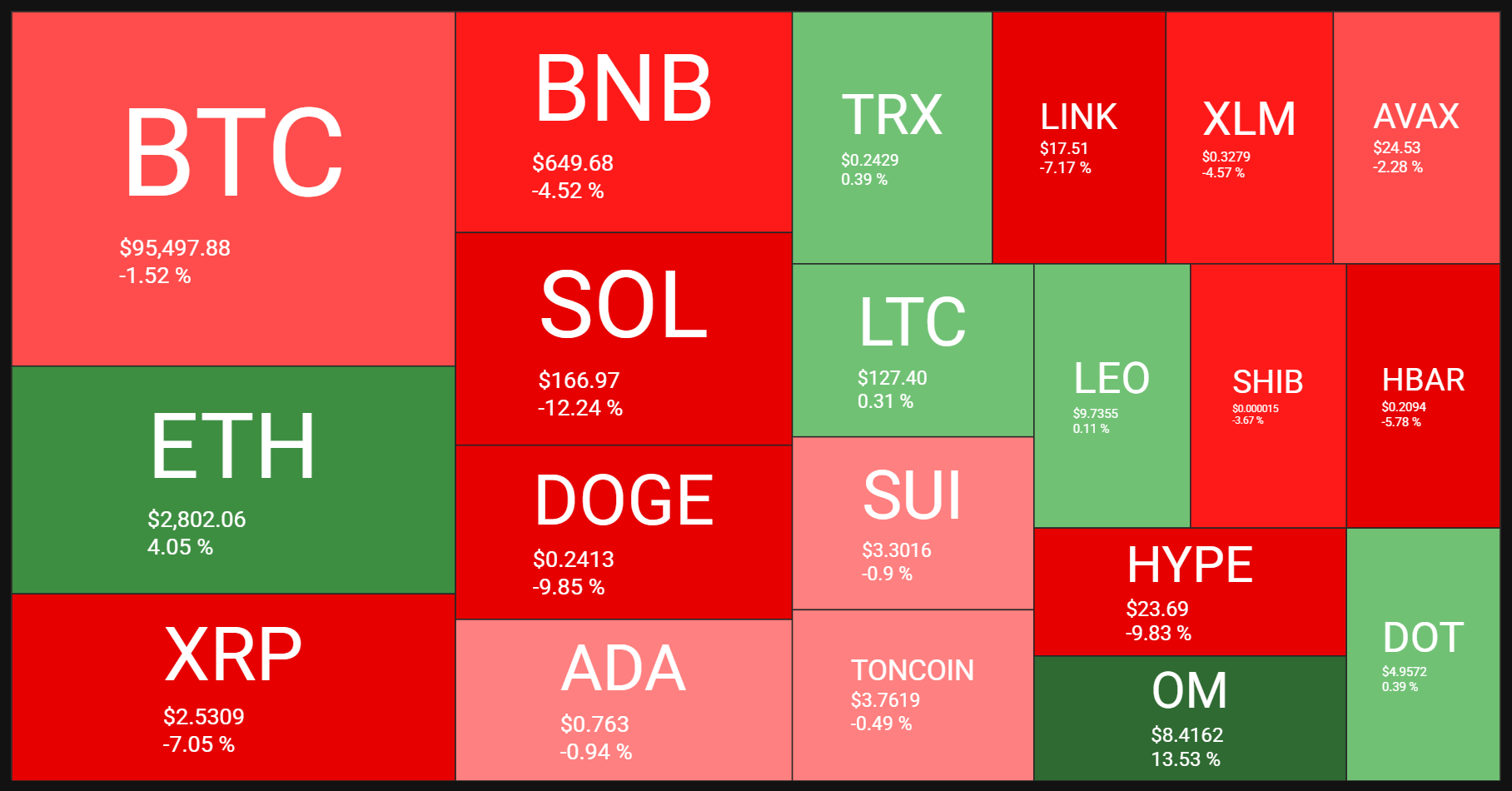

Crypto

Crypto Market Weekly Performance:

Source: quantifycrypto

Bitcoin’s price rose for several days but dropped over $4,000 on Friday after Bybit was hacked. It fell from $99,700 to $95,000, then recovered to above $96,000. Altcoins also saw significant losses. Earlier in the week, Bitcoin dropped to just over $93,000 before rebounding to $96,000. The peak was due to news of a potential lawsuit dismissal involving Coinbase, but the Bybit hack caused a sharp decline. The total market cap of all crypto assets fell from over $3.4 trillion to $3.3 trillion.

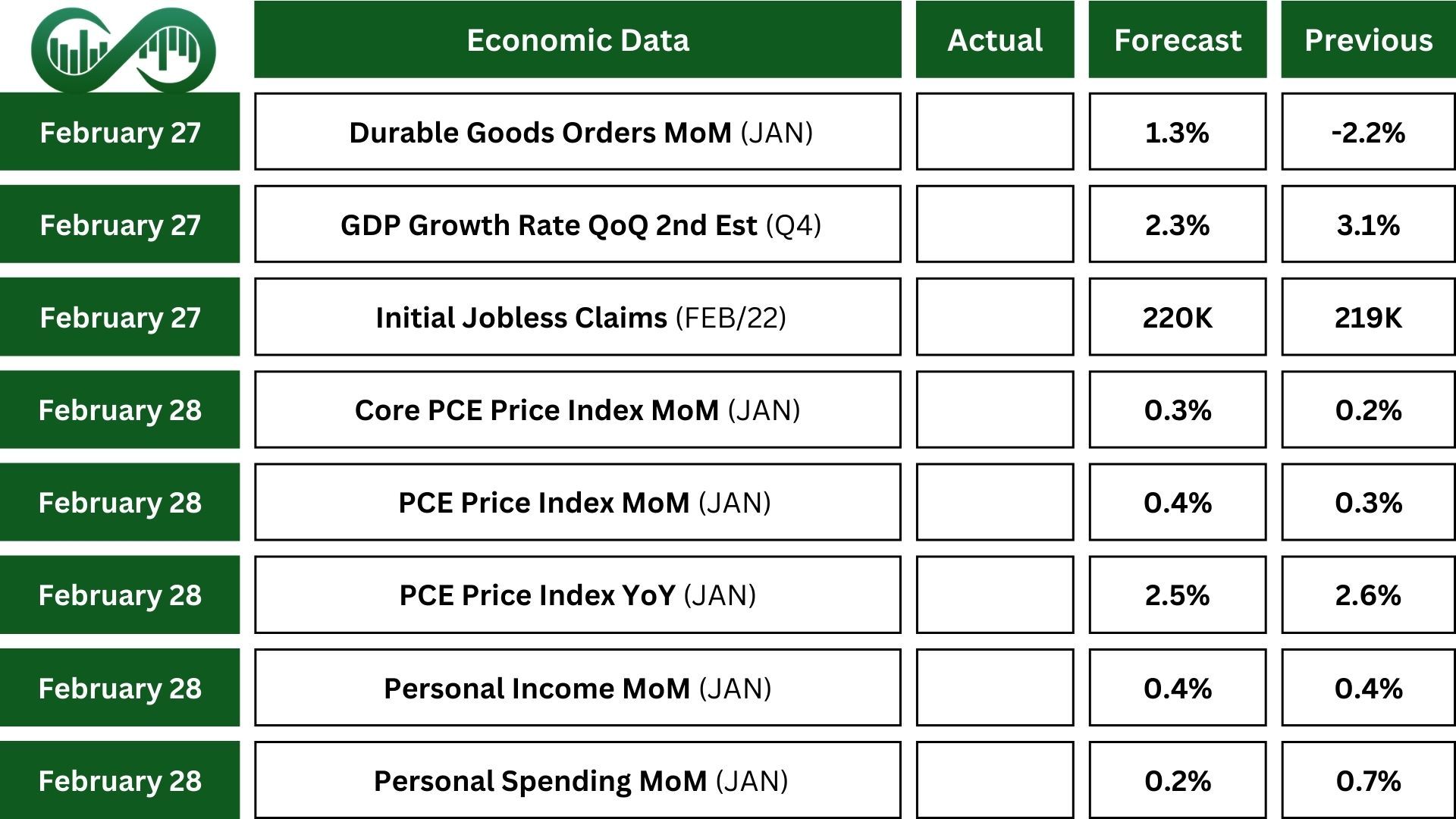

Next Week’s Outlook

Economic Events

In the US, the PCE report and Fed officials’ comments will be important.

The PCE prices will give important information about price changes, especially after higher-than-expected CPI and PPI numbers.

Personal spending growth is expected to slow to 0.2%, while personal income likely rose by 0.4%, just like in December.

The second estimate of Q1 2025 GDP growth is expected to confirm that the US economy grew at an annual rate of 2.3%, the same as the first estimate.

Also, durable goods orders are expected to increase by 1.3% after a 2.2% decline in December.

Other important releases include consumer confidence, various Fed activity indexes, the goods trade balance, and advance estimates for wholesale inventories. Housing market data, like house prices from FHFA and Case-Shiller, as well as reports on pending and new home sales, will also be important.

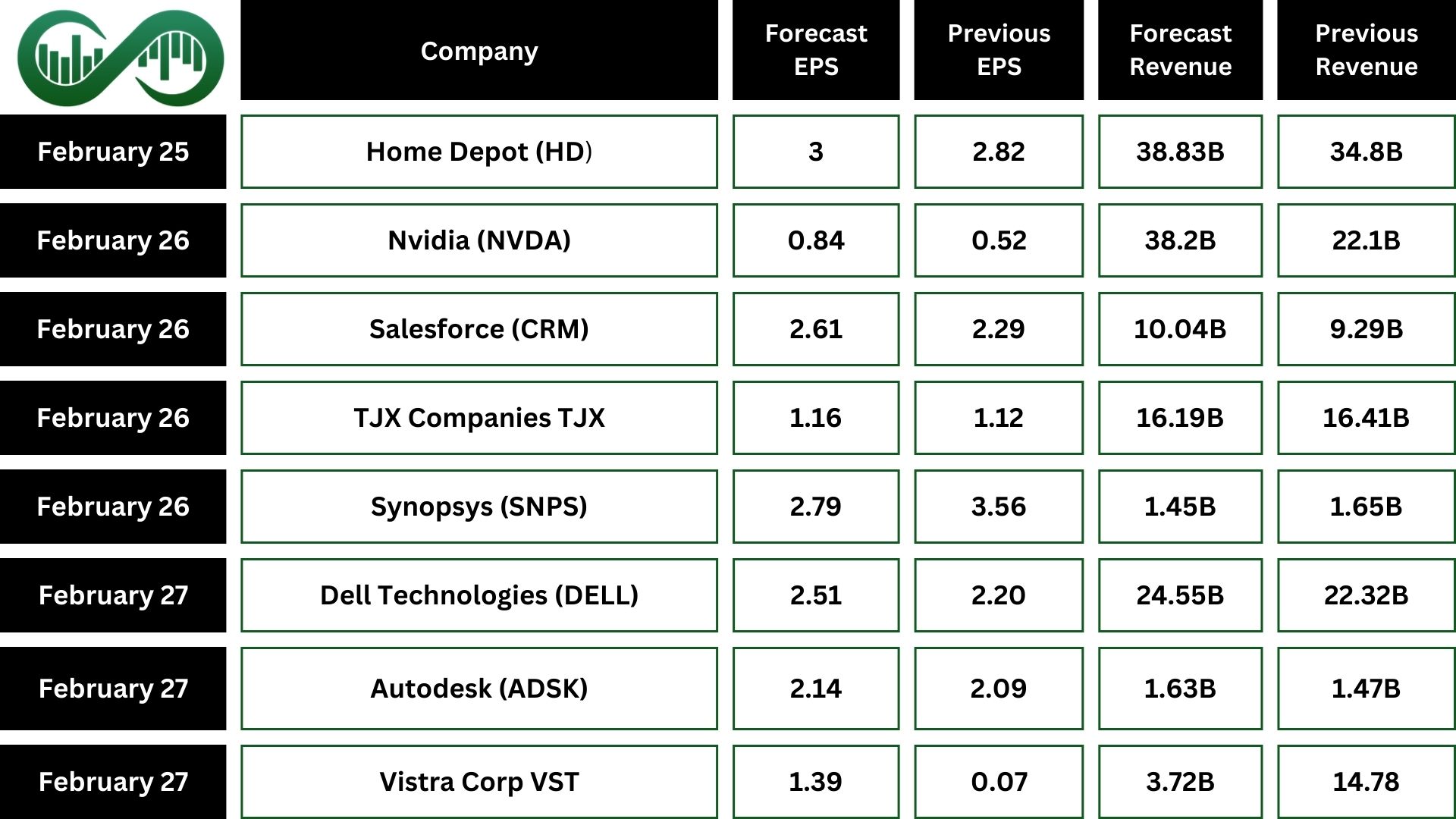

Earnings Events

On the corporate front, earnings season continues with Nvidia (NVDA), Home Depot (HD), Salesforce (CRM), Lowe’s Companies (LOW), and TJX Companies (TJX) set to report.