Economic Reports

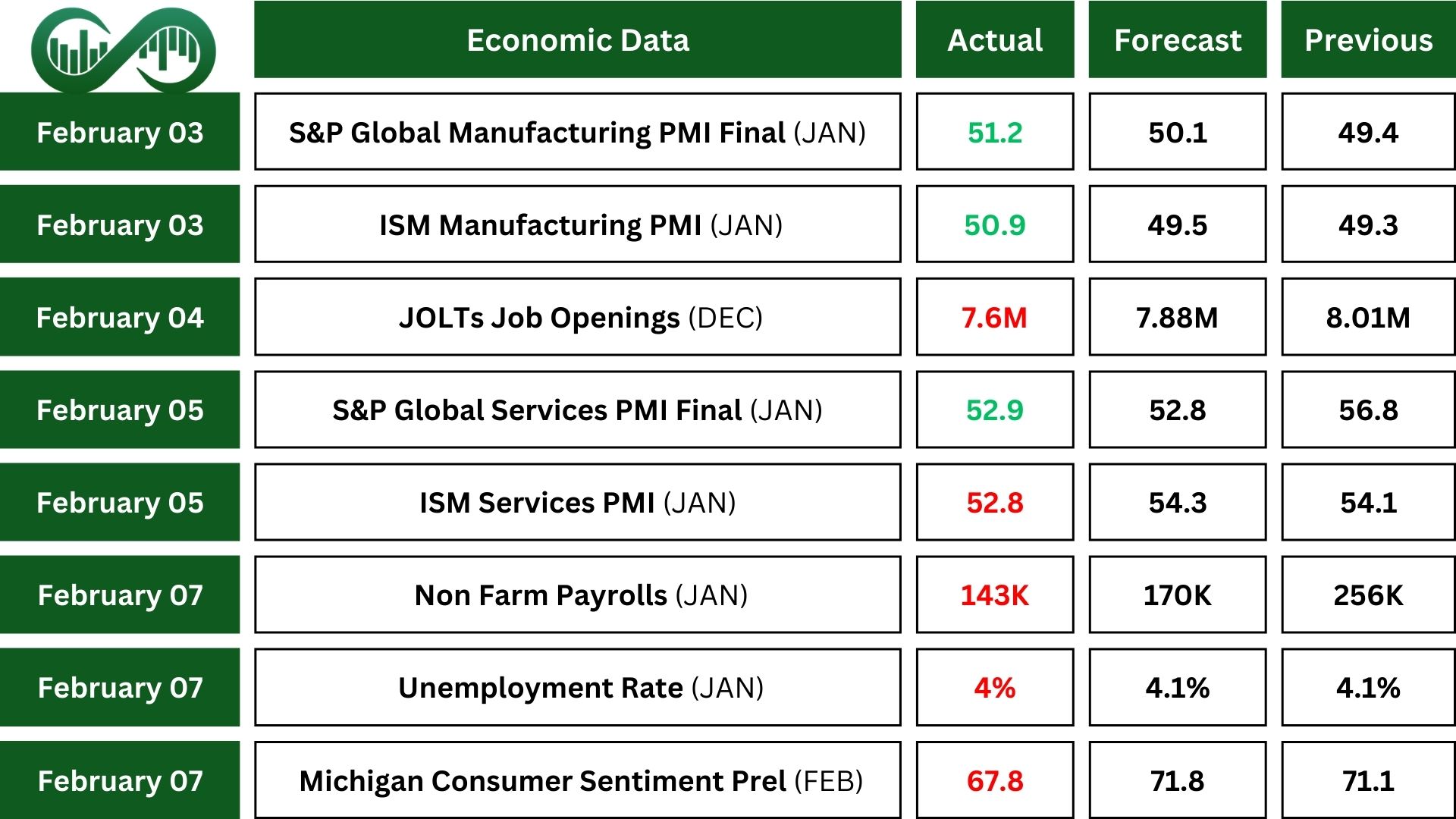

The ISM Manufacturing PMI in the United States rose to 50.9 in January, up from December. This surpasses expectations and indicates an expansion in manufacturing, marking the highest level in a year.

Overall, economic activity in the manufacturing sector expanded in January after 26 months of contraction. This improvement exceeded expectations, indicating that the manufacturing sector is not only in expansion mode but also demonstrating resilient growth.

ISM Services PMI The Services PMI was 52.8, showing continued growth but at a slower pace. Three industries, including Real Estate and Professional Services, reported contraction.

In December 2024, the number of Job Openings decreased by 556K, reaching 7.6 million, which was below the market expectation. Job openings decreased, while hires and total separations remained relatively unchanged.

In January, the US economy added 143K jobs, which is much lower than the NFP jobs added in December. Most new jobs were in health care, retail trade, and social assistance.

On the other hand, the unemployment rate in the United States edged down by 0.1% to 4%, the lowest level since last May and slightly below market expectations.

Consumer sentiment dropped by 5% in February, hitting its lowest since July 2024.

Year-ahead inflation expectations jumped to 4.3% this month, the highest since November 2023. This is only the fifth time in 14 years that such a large one-month rise has occurred.

Earnings Reports

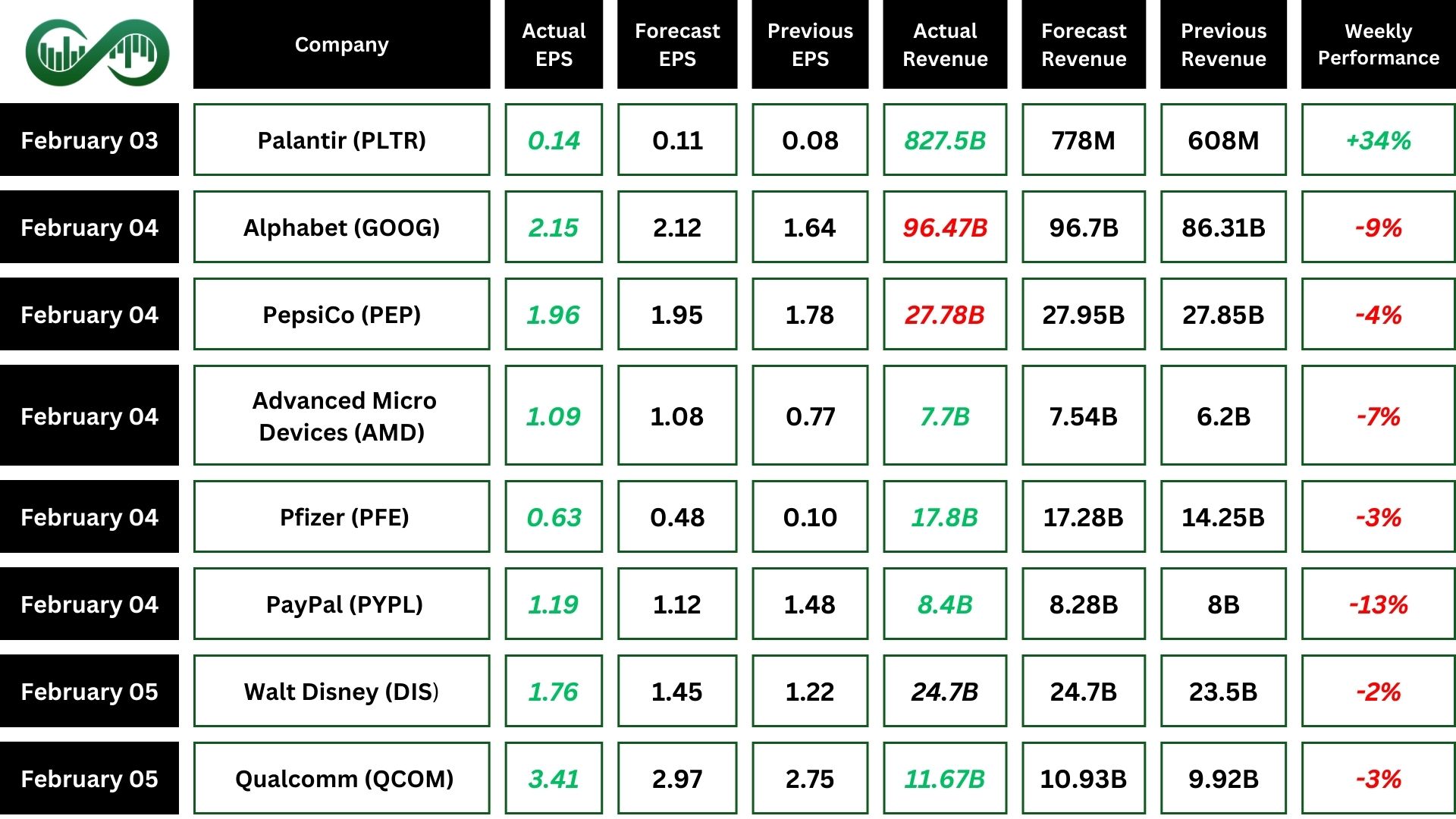

Palantir

In Q4 2024, Palantir Technologies (PLTR) reported $828 million in revenue, exceeding expectations.

The company’s GAAP earnings per share (EPS) was $0.03, above the forecasted.

U.S. revenue increased by 52% year-over-year and U.S. commercial revenue up 64%.

For Q1 2025, revenue is projected between $858 million and $862 million. These strong results and positive outlook have driven a more than 34% increase in Palantir’s stock.

Alphabet

Alphabet (GOOG) reported a Q4 2024 revenue of $96.5 billion, up 12% year-over-year but slightly below forecasts.

Earnings per share (EPS) exceeded expectations at $2.15.

Google Services revenue rose 10%, driven by strong Google Search and YouTube ad performance. Also, Google Cloud revenue grew 30% to $12 billion, fueled by success in GCP, AI Infrastructure, and Generative AI Solutions.

Alphabet plans to invest $75 billion in capital expenditures in 2025. Investor concerns over the revenue miss and high capital expenditure plans led to a 8% drop in Alphabet’s stock price.

Advanced Micro Devices

In Q4 2024, Advanced Micro Devices (AMD) reported a record revenue of $7.7 billion with a gross margin of 51%.

Despite the high revenue, GAAP net income and earnings per share (EPS) declined by around 38% due to higher operating expenses and a significant drop in the Gaming segment.

Additionally, AMD’s revenue guidance for 2025 fell short of expectations, leading to a drop in their stock.

Amazon

Amazon (AMZN) reported a 10% increase in net sales to $187.8 billion for Q4 2024, beating estimates.

Earnings per share rose to $1.86, an 88% increase from the previous year, and net income reached $20 billion.

Amazon Web Services (AWS) grew 19% in net sales to $28.79 billion, slightly below expectations.

Despite strong earnings, Amazon’s stock dropped 4% due to a cautious forecast for the next quarter.

Uber

In Q4 2024, Uber (UBER) reported an 18% year-over-year growth in Gross Bookings.

Revenue increased by 20% to $12 billion, driven by a 23% rise in combined Mobility and Delivery revenue.

The number of trips grew by 18% to 3.1 billion, averaging 33 million trips per day.

Following these strong earnings, Uber’s stock dropped due to regulations concerns. However, then stock jumped after billionaire hedge fund manager Bill Ackman disclosed a large stake in the company.

Eli Lilly

Eli Lilly (LLY) reported a Q4 profit of $4.41 billion and adjusted earnings of $5.32 per share beating expectations.

The company generated $13.53 billion in revenue, exceeding forecasts.

For the full year, Eli Lilly had a profit of $11.71 per share, and total revenue of $45.04 billion.

Looking ahead, the company expects earnings for next year to be between $22.50 and $24 per share, with revenue between $58 billion and $61 billion. The impressive results led to an 8% rise in Eli Lilly’s stock.

Indices

Indices’ Weekly Performance:

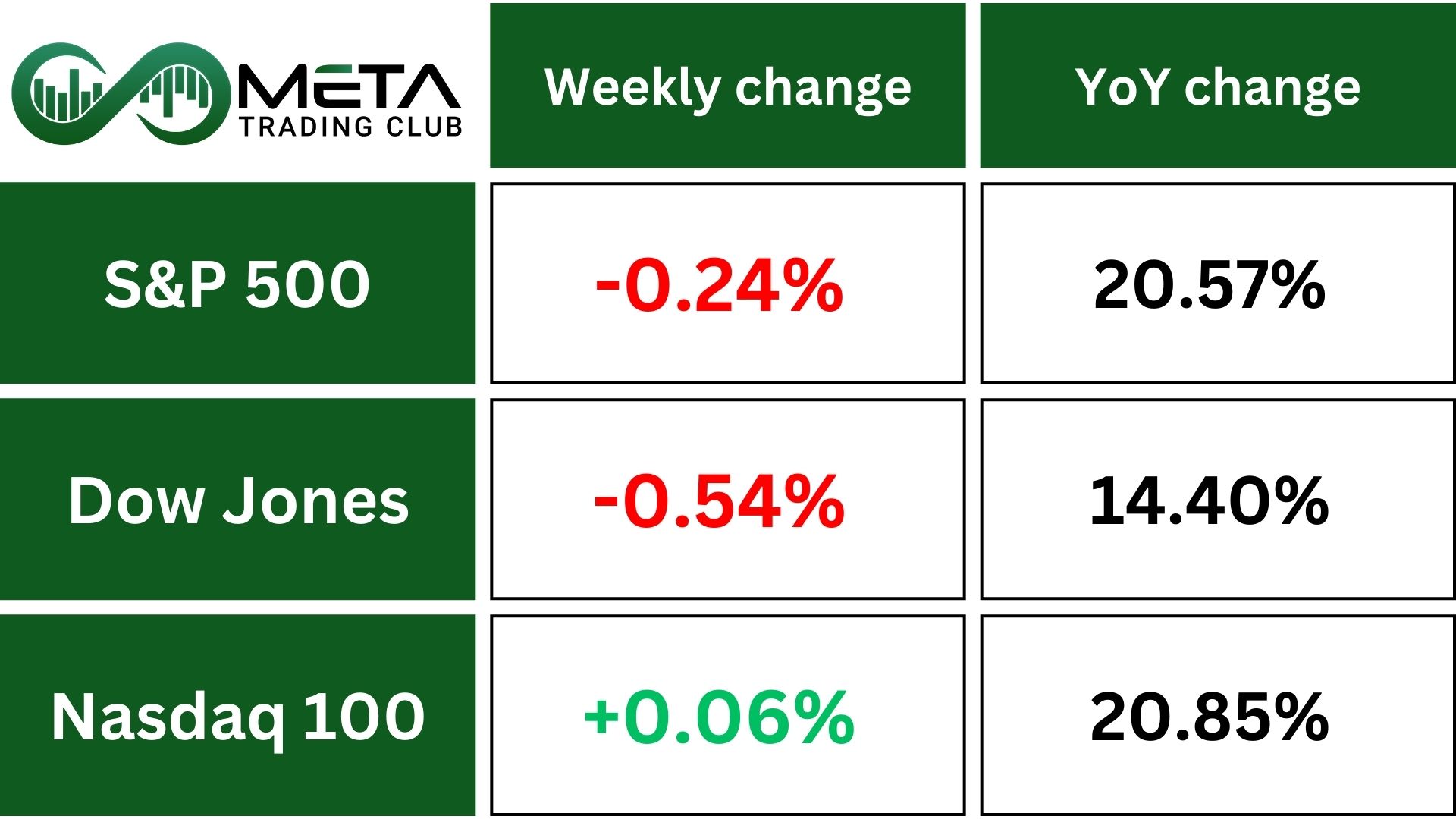

The S&P 500 closed down on Friday, resulting in a 0.24% loss for the week and back-to-back weekly declines.

Also, Dow breaking a three-week streak of gains and ending 0.54% lower.

Investors are concerned about potential trade-war escalation after President Trump announced plans for reciprocal tariffs next week. China retaliated with new 10% tariffs, raising fears of further economic impact.

The main risk for the U.S. economy is the potential retaliation affecting exporters, as reduced foreign purchases of U.S. goods could directly impact GDP.

Technically, SPX is in an uptrend but was rejected from its all-time high (around 6130) last week due to weak momentum (RSI trend line is declining). It has strong support around 5900. To rise further, it needs to break the RSI downward trend line and then the all-time high. If it breaks the uptrend line, further decline is anticipated.

Stocks

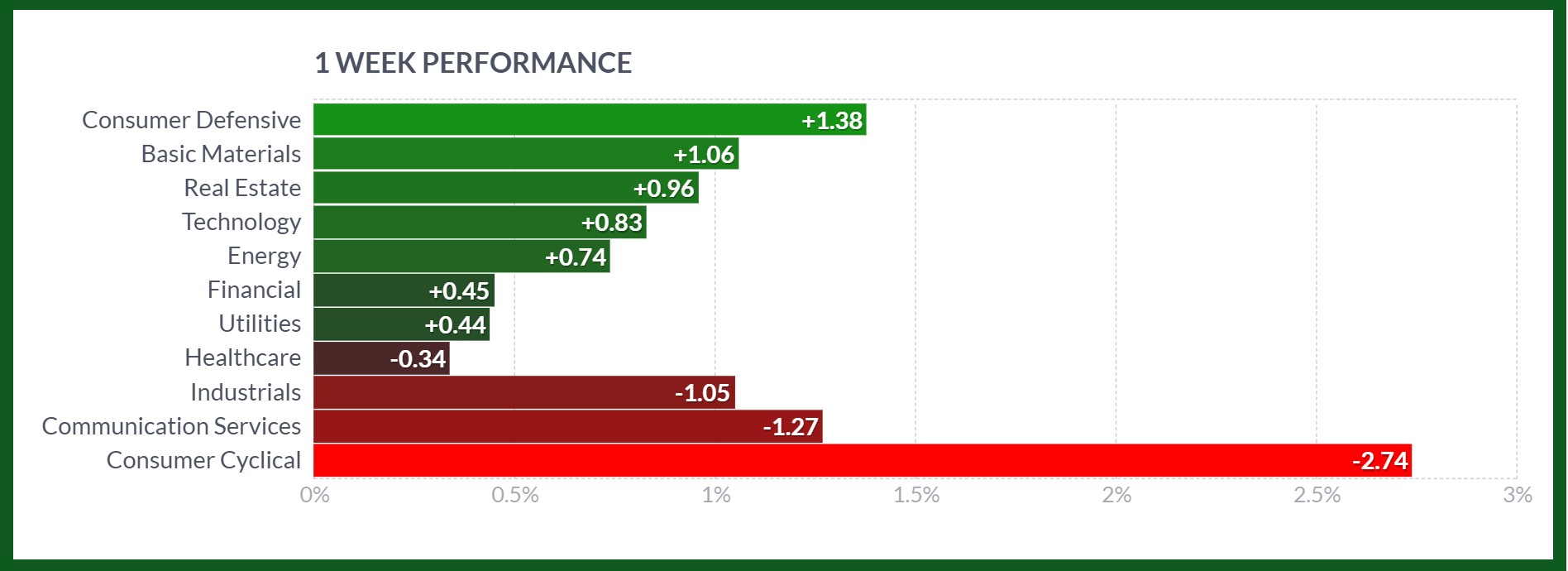

Sector’s Weekly Performance:

Source: Finviz

Last week had mixed sector performances like the whole market. Consumer Defensive, Basic Materials, Real Estate, Technology, Energy, Financial, and Utilities sectors gained. However, Healthcare, Industrials, Communication Services, and Consumer Cyclical sectors declined.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- Palantir Technologies (PLTR): Surged 34% due to strong quarterly earnings and positive analyst ratings.

- Super Micro Computer (SMCI): Soared 27% as investors favor AI push.

- Johnson Controls (JCI): Increased 12% due to strong earnings results and increased demand for its building efficiency solutions.

- Uber Technologies (UBER): Rose 11% due to strong earnings results driven by increase in gross bookings.

- Philip Morris (PM): Up 11% due to strong earnings results and increased demand for its reduced-risk products.

- Yum (YUM): Surged 10% driven by strong same-store sales growth and successful marketing campaigns which lead to positive earnings.

- Eli Lilly (LLY): Soared 8% driven by strong sales of its pharmaceutical products and positive clinical trial results.

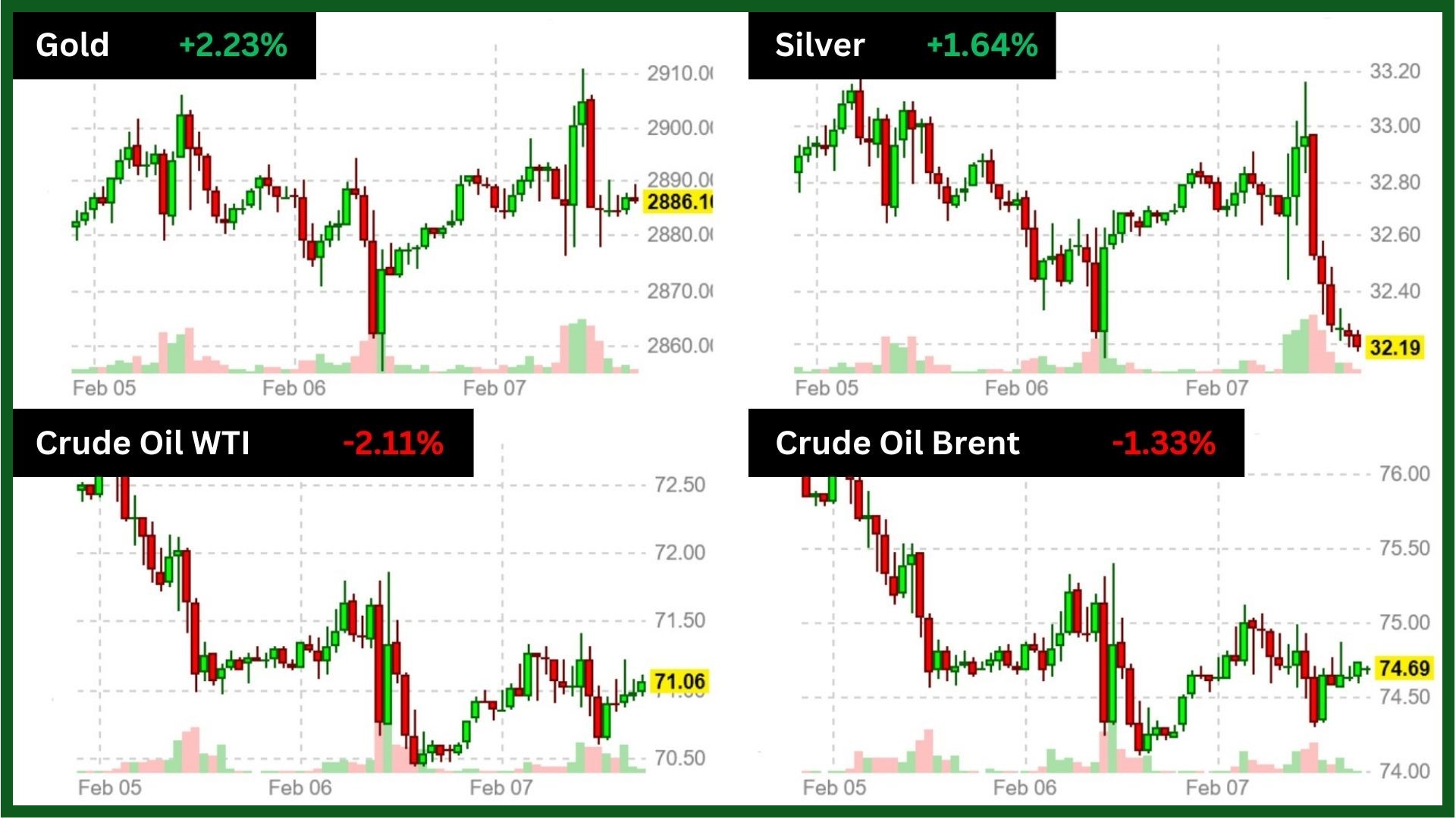

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold ended the week with an over 2% gain and closed just below the record high of $2,880. This marks the sixth consecutive week of gains for the precious metal, with continuous gold futures sitting up 9.4% in the year to date alone.

The increase in gold prices was driven by safe haven buying due to investor concerns over January’s jobs data and Trump’s tariff policies. Some Analysts set a price target of $3,000 per ounce, citing gold’s appeal as a store of value and hedge against uncertainty.

Technically, last week gold broke its all-time high with strong momentum, reaching and breaking the Fibonacci zone resistance at $2839. This level could act as support if gold stays above it. Further targets are $2938 and $3000.

Oil futures fell for the third week straight. This drop was due to postponed U.S. tariffs on Canadian and Mexican oil. Chinese retaliatory tariffs on U.S. oil and gas also contributed. OPEC+ plans to raise output in April. A large buildup in U.S. crude oil stocks added pressure.

Forex

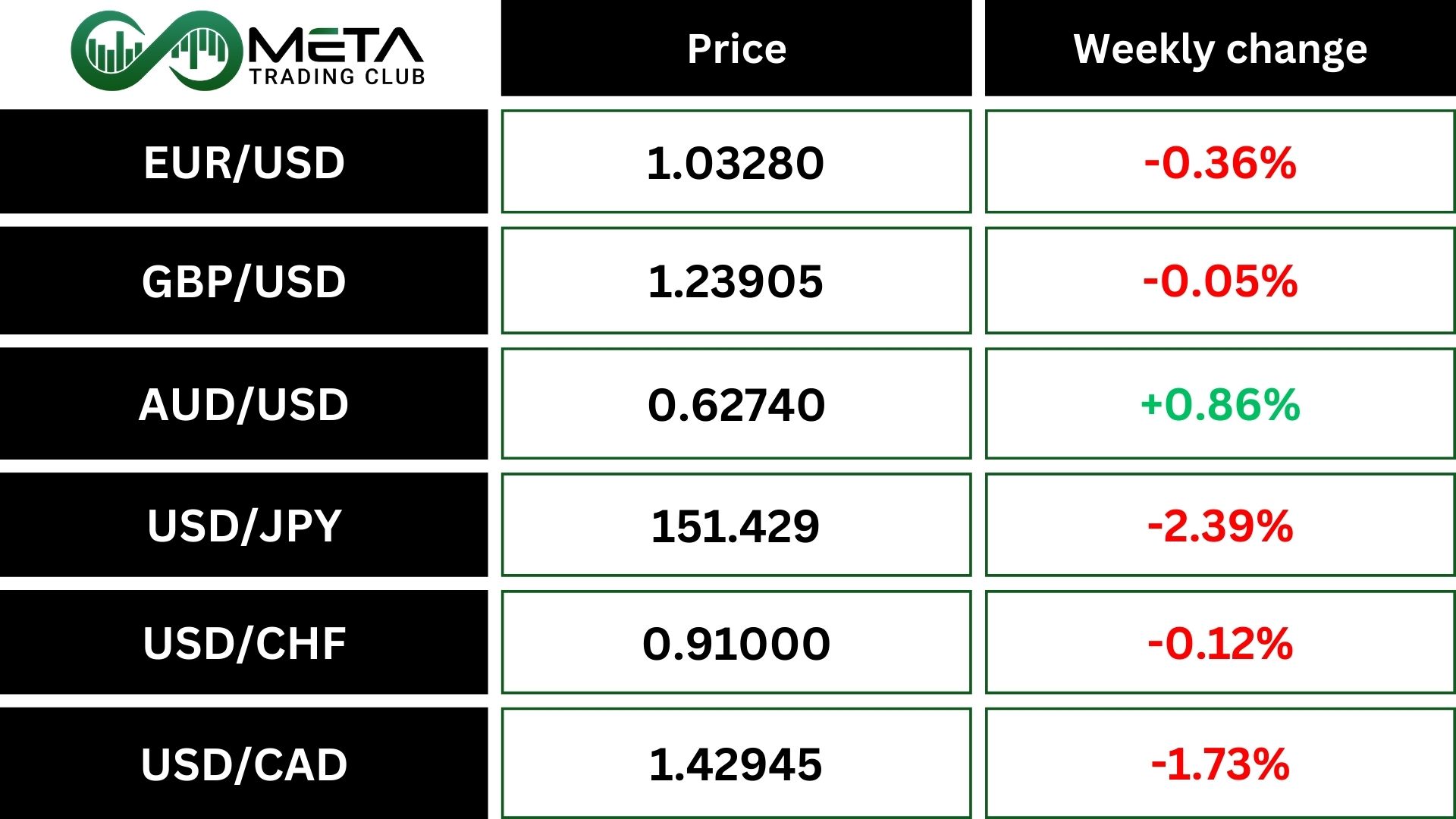

Weekly Performance of Major Foreign Exchange Pairs:

At the start of the week, the USD surged on Canada and Mexico tariff news but later fell after the tariffs were postponed. For the week, the USD dollar index (DXY), was on track for a weekly decline as fears of a global trade war eased.

Technically, DXY is in an uptrend but with weakening momentum. If DXY breaks the purple trend line, further decline is anticipated.

The only currency the USD gained against was the EUR, with EUR/USD down 0.36%.

The USD was weakest against the JPY due to hopes that the Bank of Japan would continue tightening, pushing USD/JPY to its lowest level since December. Additionally, the USD fell 2.4% against the JPY for the week.

The USD also declined against the CAD by 1.73%, despite initially reaching a high not seen since 2002.

Crypto

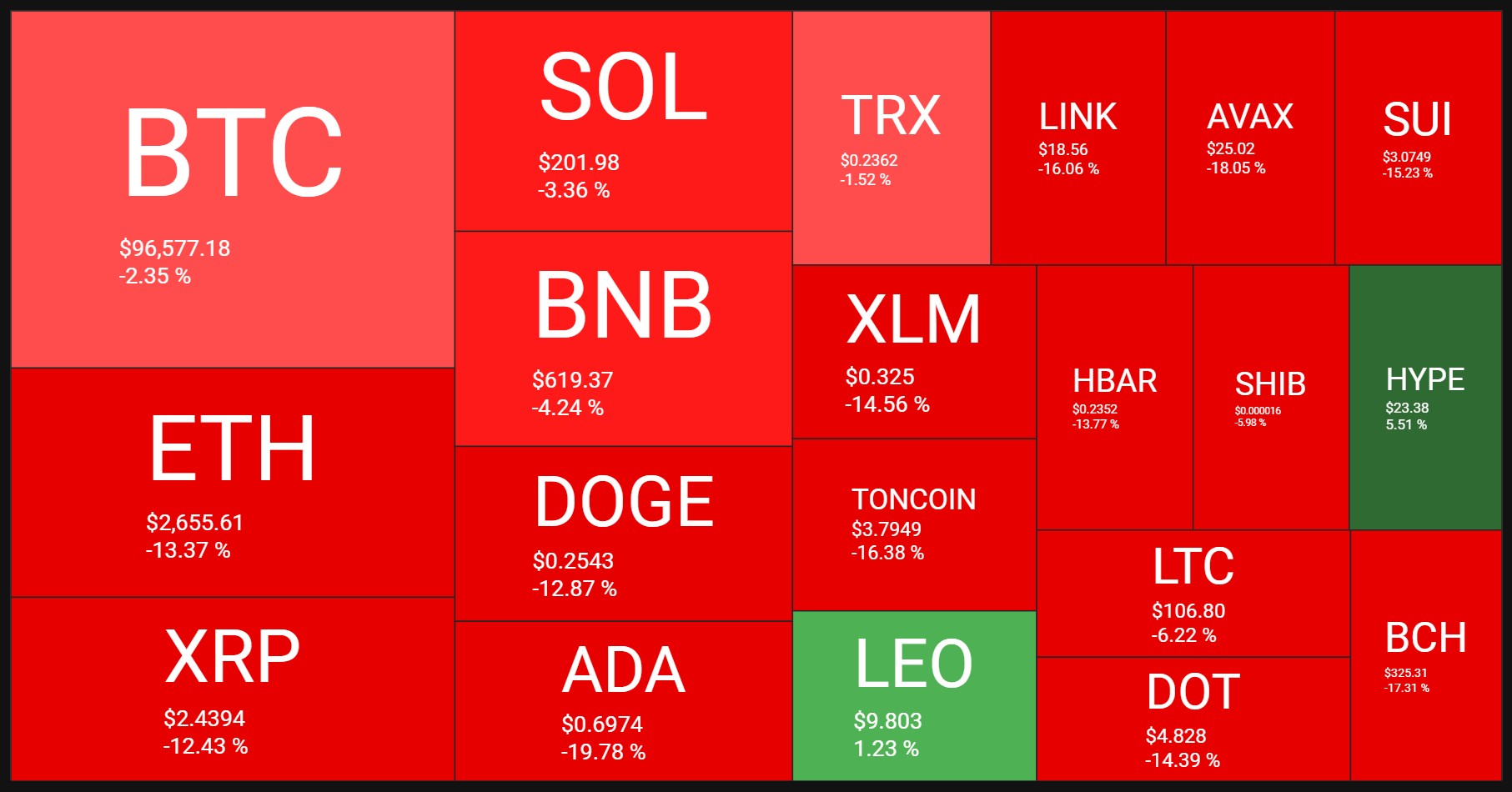

Crypto Market Weekly Performance:

Source: quantifycrypto

The previous weekend was tough for Bitcoin as President Trump’s trade war with China, Canada, and Mexico caused the crypto market to crash. BTC fell from $106,000 to $92,000 due to the new tariffs.

Bitcoin prices have stabilized between $92,000 and $102,000, sparking debates about its future direction.

Significant bearish pressure would be needed to lower the price. Bitcoin defended the $96,000 level during a recent correction and now sits above $97,000 in a calm market.

Next Week’s Outlook

Economic Events

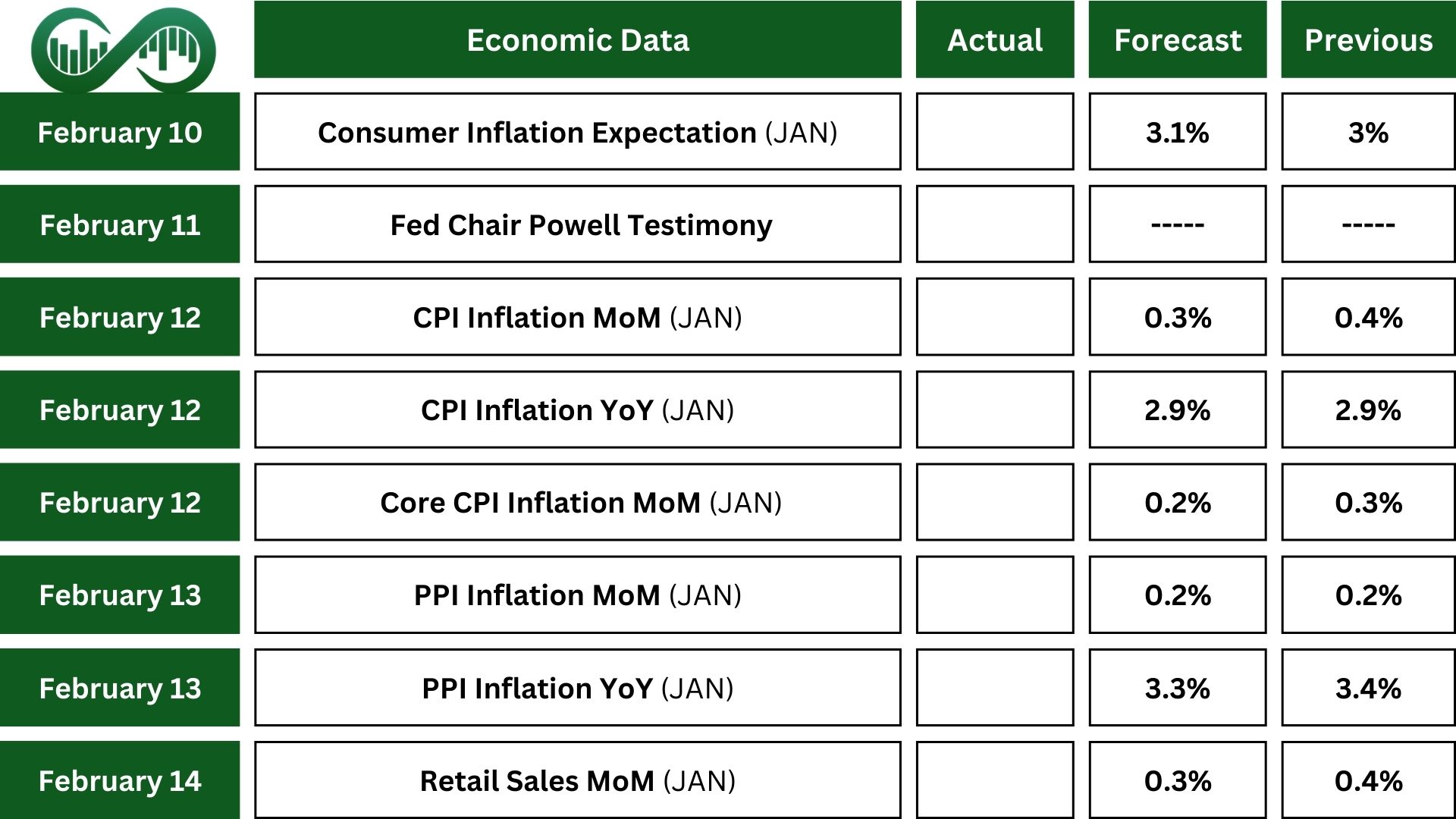

Key price indexes will reveal fresh insights into inflation and the Fed’s policy outlook.

CPI likely rose 0.3% in January, down from 0.4% in December, while core CPI probably increased to 0.3% from 0.2%.

PPI likely held steady at 0.2%, with retail sales stalling after a 0.4% rise in December.

Other releases include industrial production, budget statements, inflation expectations, export/import prices, and business inventories.

Fed Chair Jerome Powell will present the Semiannual Monetary Policy Report to Congress, with markets watching for future rate cut signals.

Earnings Events

On the corporate side, major earnings reports from McDonald’s (MCD), Vertex Pharmaceuticals (VRTX), Coca-Cola (KO), S&P Global (SPGI), Cisco Systems (CSCO), Applied Materials (AMAT), Deere & Co (DE), Airbnb (ABNB) and Coinbase (coin).