Economic Reports

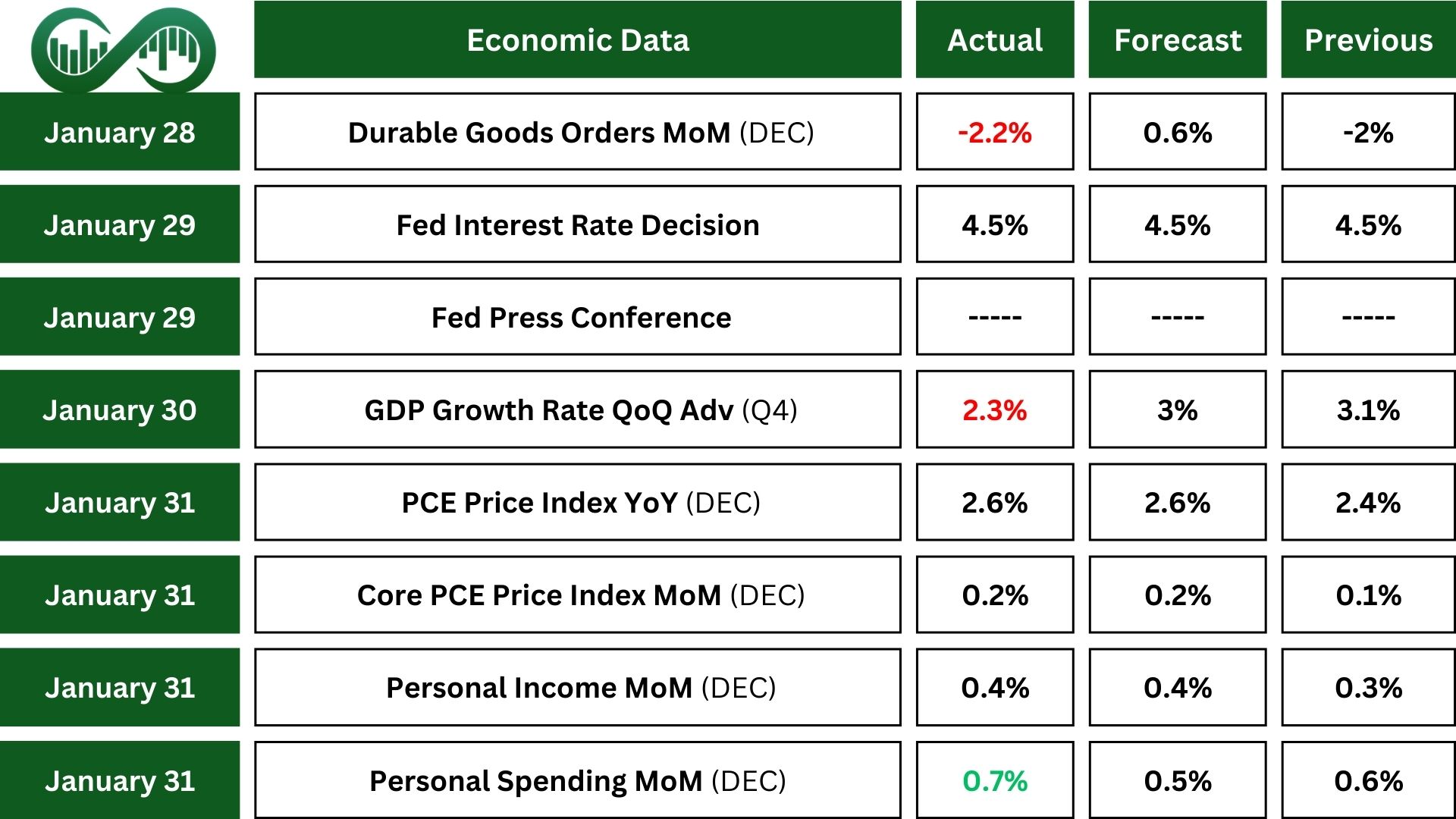

In December, new orders for durable goods fell by $6.3 billion (-2.2%), marking the fourth decline in five months.

The Federal reserve keeps interest rates steady, maintaining the federal funds rate range at 4.25% to 4.5% and reducing holdings of Treasury and mortgage-backed securities.

Fed Chair Powell emphasized balancing employment and inflation risks, with a strong labor market for those employed but challenging for the unemployed.

The European Central Bank (ECB) lowered interest rates by 25 basis points to 2.75% in January 2025, marking the fifth reduction since June 2024.

Initial jobless claims in the US dropped by 16K to 207K for the week ending January 25th, while continuing claims fell by 42K to 1,858K.

The real GDP increased at an annual rate of 2.3% in the fourth quarter of 2024, below expectations. Consumer and government spending were key drivers of economic activity.

In December 2024, the core PCE price index, excluding food and energy, rose by 0.2%, maintaining an annual rate of 2.8%, above the Federal Reserve’s target of 2%. Higher inflation may prompt the Federal Reserve to keep interest rates high, affecting borrowing costs and potentially slowing economic growth.

Earnings Reports

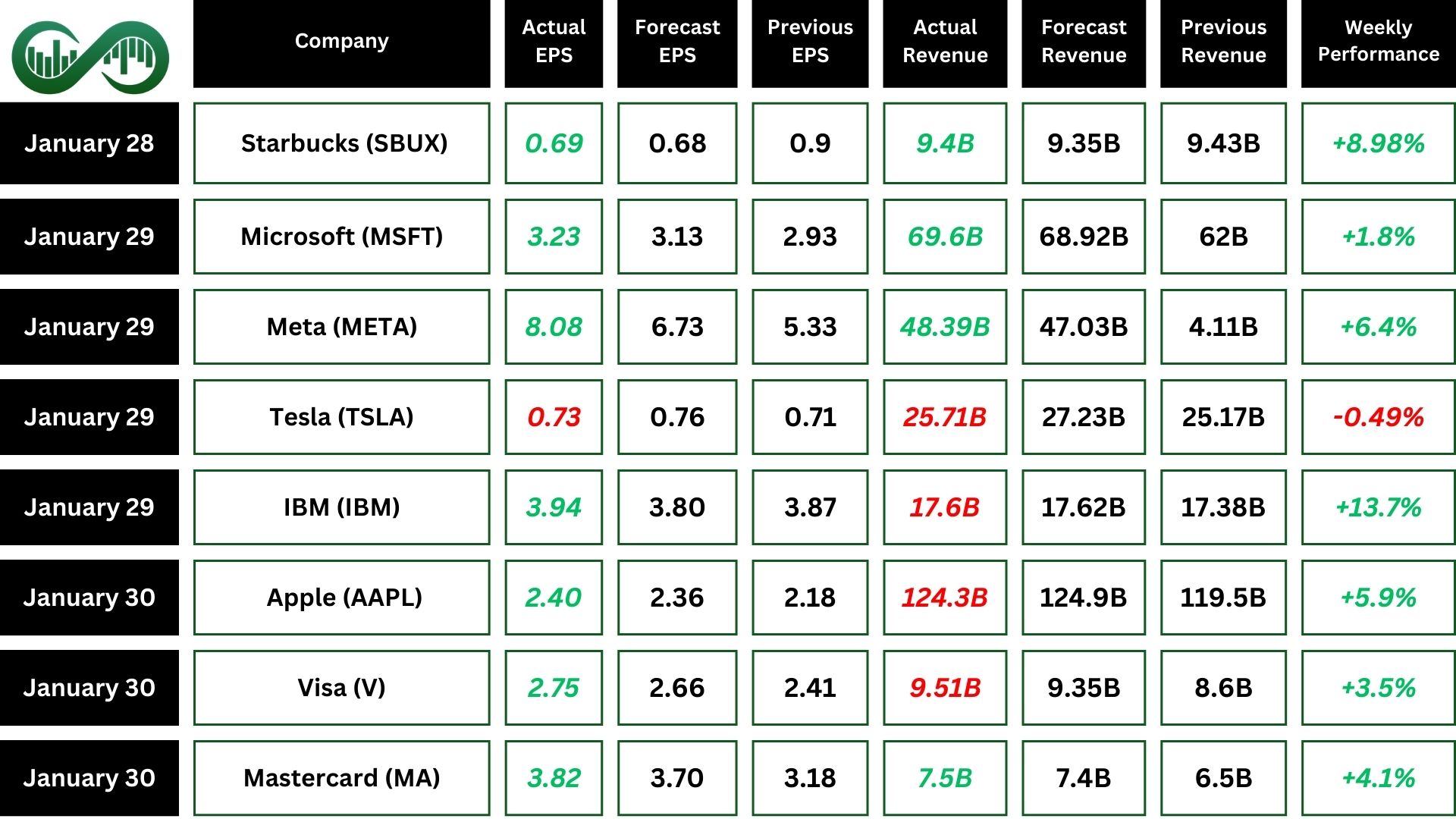

Microsoft

Microsoft (MSFT) Q2 FY25 revenue increased by 12% year-over-year, but it missed estimates. Also, operating income grew by 17%, net income rose by 10%, and diluted earnings per share also increased by 10%.

Meanwhile, AI business achieved $13 billion in annual revenue, up 175% year-over-year. Microsoft Cloud revenue for the quarter was a 21% increase.

The company returned $9.7 billion to shareholders and expects continued growth with investments in cloud and AI infrastructure.

However, cloud revenue of $40.9 billion was slightly below expectations, causing investor concerns. Microsoft’s stock fell after the Q2 report due to slower growth in Azure and worries about high AI spending.

Meta

Meta Platforms (META) reported strong financial results for Q4 and the entire year of 2024. The company experienced significant growth in both revenue and net income, driven by an increase in ad impressions and higher average ad prices.

Earnings highlights include a 22% year-over-year revenue increase and a 59% rise in net income. Diluted earnings per share grew by 60% year-over-year and the operating margin for the full year was 42%.

Also, daily active users increased, and the company maintained robust capital expenditures and a strong cash position.

Looking forward to 2025, Meta expects continued revenue growth, investing heavily in AI, infrastructure, and talent, even amid regulatory challenges. They are optimistic about their investments in AI, augmented reality glasses, and the future of social media, aiming for sustained growth.

Tesla

Tesla (TSLA) reported an operating income of $7.1 billion for 2024, including $1.6 billion in Q4. Despite an EPS of $0.73 missing estimates, the company achieved a revenue of $25.7 billion, beating expectations.

Q4 was a record quarter for vehicle deliveries and energy storage deployments.

Tesla invested heavily in infrastructure, focusing on new vehicle manufacturing, AI training, and energy storage. They achieved an all-time low cost of goods sold per vehicle at about $32,500 in Q4.

Elon Musk shared positive plans for 2025, including new affordable electric cars and a self-driving car service in Austin, Texas.

Apple

Apple (AAPL) reported the first quarter of 202 and made $124.3 billion in revenue, which is 4% more than last year. Their earnings per share (EPS) went up by 10% to $2.40.

CEO Tim Cook said this was their best quarter ever, thanks to popular products and services during the holiday season.

Strong revenue and operating margins led to double-digit EPS growth, allowing Apple to return over $30 billion to shareholders. The number of active Apple devices also hit a new high.

Apple’s board declared a cash dividend of $0.25 per share.

Visa

Visa (V) started 2025 strong with $9.5 billion in revenue, a 10% increase from last year, and a 14% rise in earnings per share.

Operating expenses went up by 11%. Visa bought back $3.9 billion in stock and paid $1.2 billion in dividends. Despite challenges like the strong US dollar, Visa renewed important partnerships and expanded services.

The company is focused on growth in payments, new revenue streams, and value-added services. Their innovative work and strategic partnerships position them for continued success. Overall, Visa had a great start to 2025, showing solid growth and optimism for the future.

Mastercard

Mastercard (MA) Q4 2024 earnings report showed a 14% increase in net revenue, driven by an expanding payment network and value-added services.

The effective tax rate dropped to 14%. The company issued 3.5 billion Mastercard and Maestro-branded cards by the end of 2024.

Adjusted earnings per share were $3.82, beating expectations and leading to increase in stock price.

News of the Week

Deep Seek

Last week, China’s Deep Seek AI model caused a significant impact on the U.S. stock market. Investors worried that this powerful and affordable model could reduce the need for expensive AI hardware, negatively affecting companies like Nvidia and Broadcom.

The tech sector overall declined, marking the biggest drop in four months. However, some companies, like Meta Platforms, saw gains. Meta’s stock rose due to the success of Deep Seek’s open-source model, which aligns with Meta’s AI strategy.

Deep Seek’s emergence has sparked debates about economic and geopolitical competition between the U.S. and China in AI technology. It has raised questions about the future of AI investments and the need for more efficient models. Overall, Deep Seek’s entry has shaken the tech industry and highlighted ongoing competition in AI development.

Tariff

Global markets are expected to be impacted on Monday due to U.S. President Donald Trump’s new tariffs on Canada, Mexico, and China. These tariffs could hurt economic growth and increase inflation. Mexico and Canada, the U.S.’s top trading partners, promised to retaliate immediately, and China said it would take countermeasures. This sets the stage for market turbulence.

A global trade war could harm U.S. corporate profits, increase inflation, and affect U.S. interest rate cut expectations. It could also weaken currencies like the Canadian dollar and China’s yuan. Markets might react strongly to this, potentially challenging Trump’s previous market support.

Additionally, last week, markets were already affected by the launch of China’s Deep Seek AI model, which impacted tech stocks and added to broader market worries.

Indices

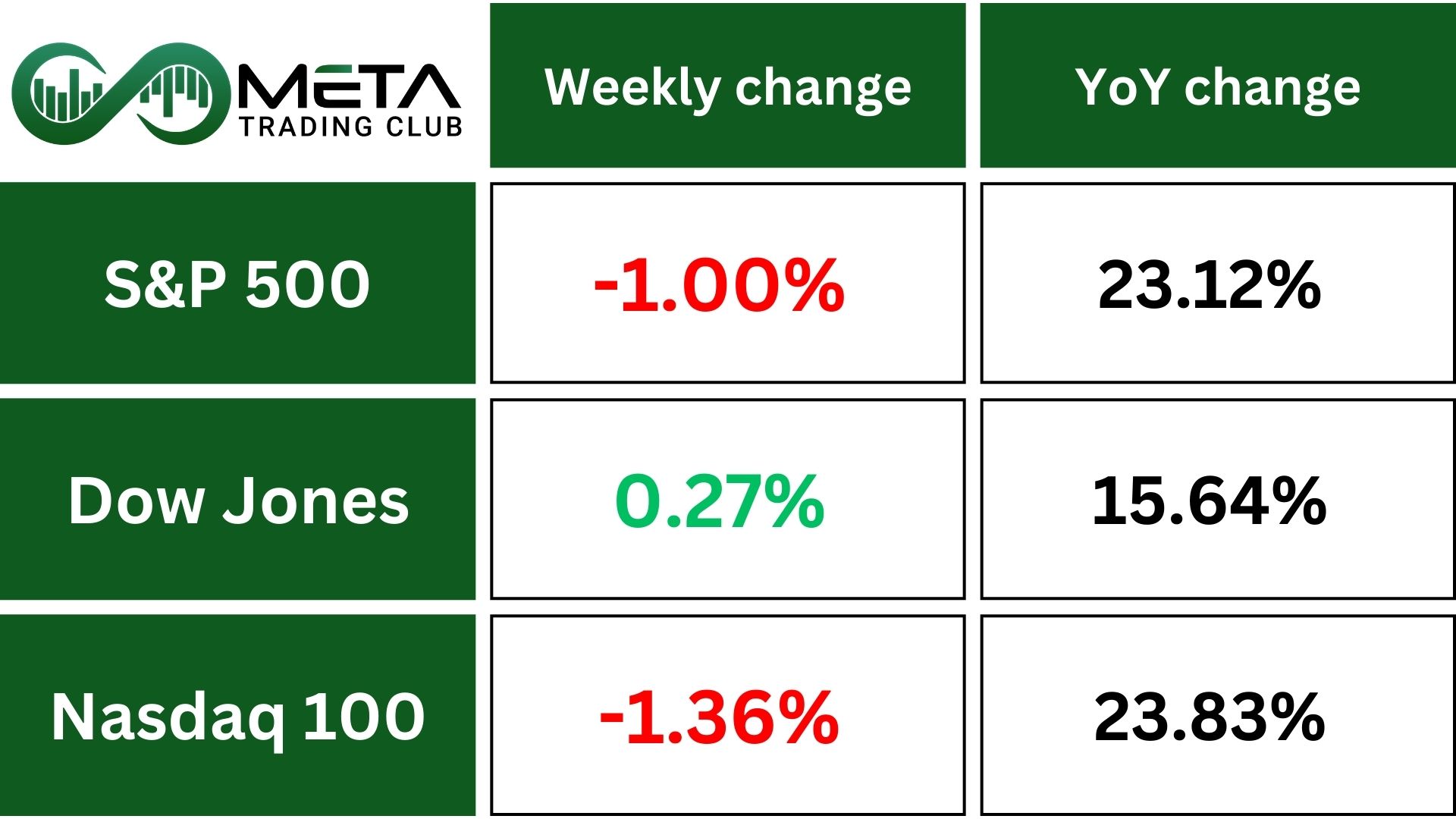

Indices’ Weekly Performance:

The S&P 500 index fell by 1% this week because of worries about competition in technology and new tariffs planned by the Trump administration. Despite this, the index ended January with a gain.

The index closed at 6,040.53, which is down from last week but still close to its record high. It has risen 2.7% since the end of 2024 and 24% from a year ago.

Many companies, like Apple and Visa, reported better-than-expected earnings. The Federal Reserve’s preferred inflation measure showed a 0.3% increase in December, and the central bank kept its policy rate the same while noting that inflation is still high.

There are also worries about the US tech sector’s ability to compete with a new AI model from Chinese startup Deep Seek.

The S&P 500 Index is in an upward trend but faces its ATH resistance. The RSI’s bearish divergence suggests weakening momentum, so traders should watch for potential consolidation or pullback.

Stocks

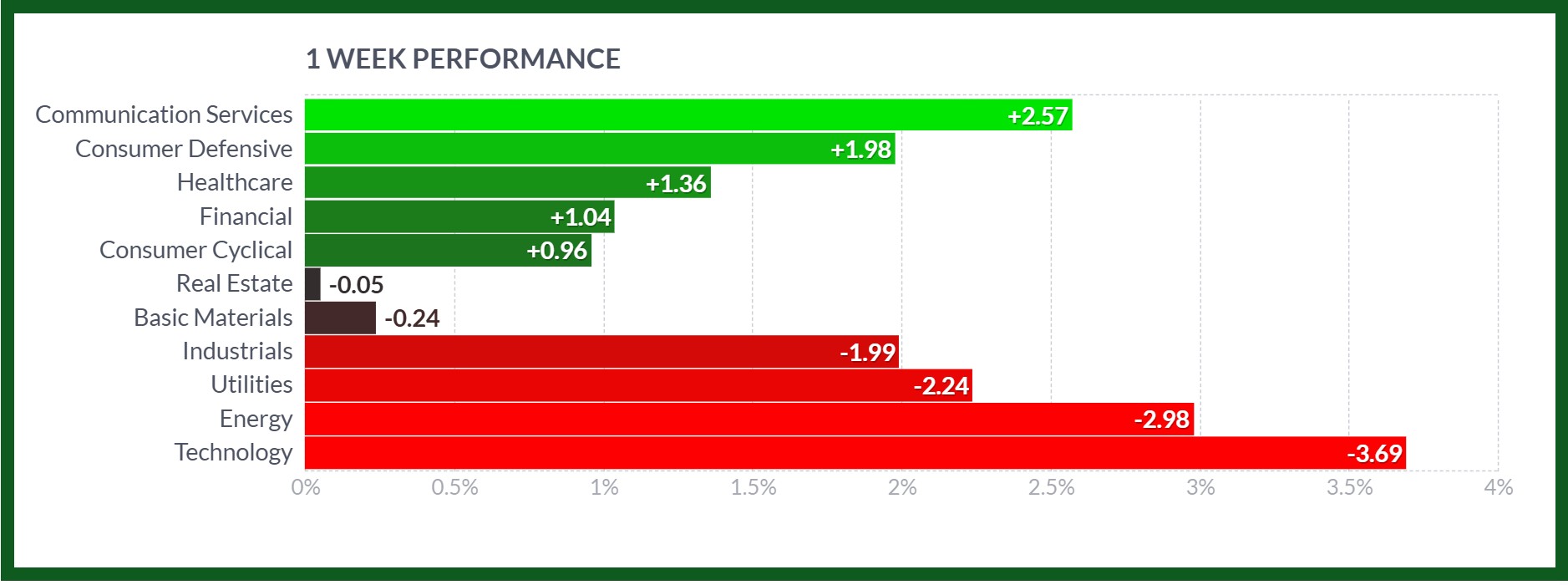

Sector’s Weekly Performance:

Source: Finviz

Communication Services led the gains with a 2.57% increase, followed by Consumer Defensive at 1.98% and Healthcare at 1.36%. Financials also saw a modest rise of 1.04%.

On the downside, Industrials and Utilities experienced notable declines, with -1.99% and -2.24% respectively. Energy also struggled, dropping -2.98%. Technology was the worst performer, falling -3.69%.

Overall, while some sectors like Communication Services and Consumer Defensive performed well, others like Technology and Energy faced significant challenges.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- International Business Machines (IBM): IBM saw a significant rise in its stock price due to positive earnings and outlooks.

- Starbucks (SBUX): Starbucks experienced a stock increase due to better-than-expected same-store sales growth.

- AbbVie (ABBV): AbbVie’s stock rose on positive earning and revenue growth.

- T-Mobile US (TMUS): T-Mobile’s stock gained as a result of positive earnings and strong subscriber growth.

- Meta Platforms (META): Meta Platforms saw an increase in its stock price due to positive outlook and strong earnings reported.

- CrowdStrike (CRWD): CrowdStrike experienced a stock surge after announcing a perfect score on an industry test for ransomware detection, protection, and accuracy.

- Apple (AAPL): Apple experienced a stock surge due to positive quarterly earnings and strong growth

- BlackRock (BLK): BlackRock saw an increase due to positive investor sentiment around its financial outlook made by high interest rates.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold prices (XAUUSD) soared to a record high of $2,800 last week after President Trump announced a 25% tariff on imports from Canada and Mexico. This caused traders to buy gold as a safe haven amid trade war fears.

The Federal Reserve recently kept interest rates steady, and inflation concerns are rising. Lower rates make gold more attractive because it doesn’t earn interest, so there’s less cost to hold it.

Gold has been in an upward trend, breaking previous resistance levels and reaching new highs. The recent close near the all-time high indicates strong bullish momentum.

WTI crude oil prices fell last week because traders were uncertain about whether the Trump Administration would include oil imports in its 25% tariffs on Canada and Mexico. This uncertainty and the potential impact on U.S. gasoline prices caused the drop.

There were concerns that higher U.S. gasoline prices, particularly in the Midwest, could result from the tariffs.

The energy industry worried about disruptions, leading to uncertainty and market reactions.

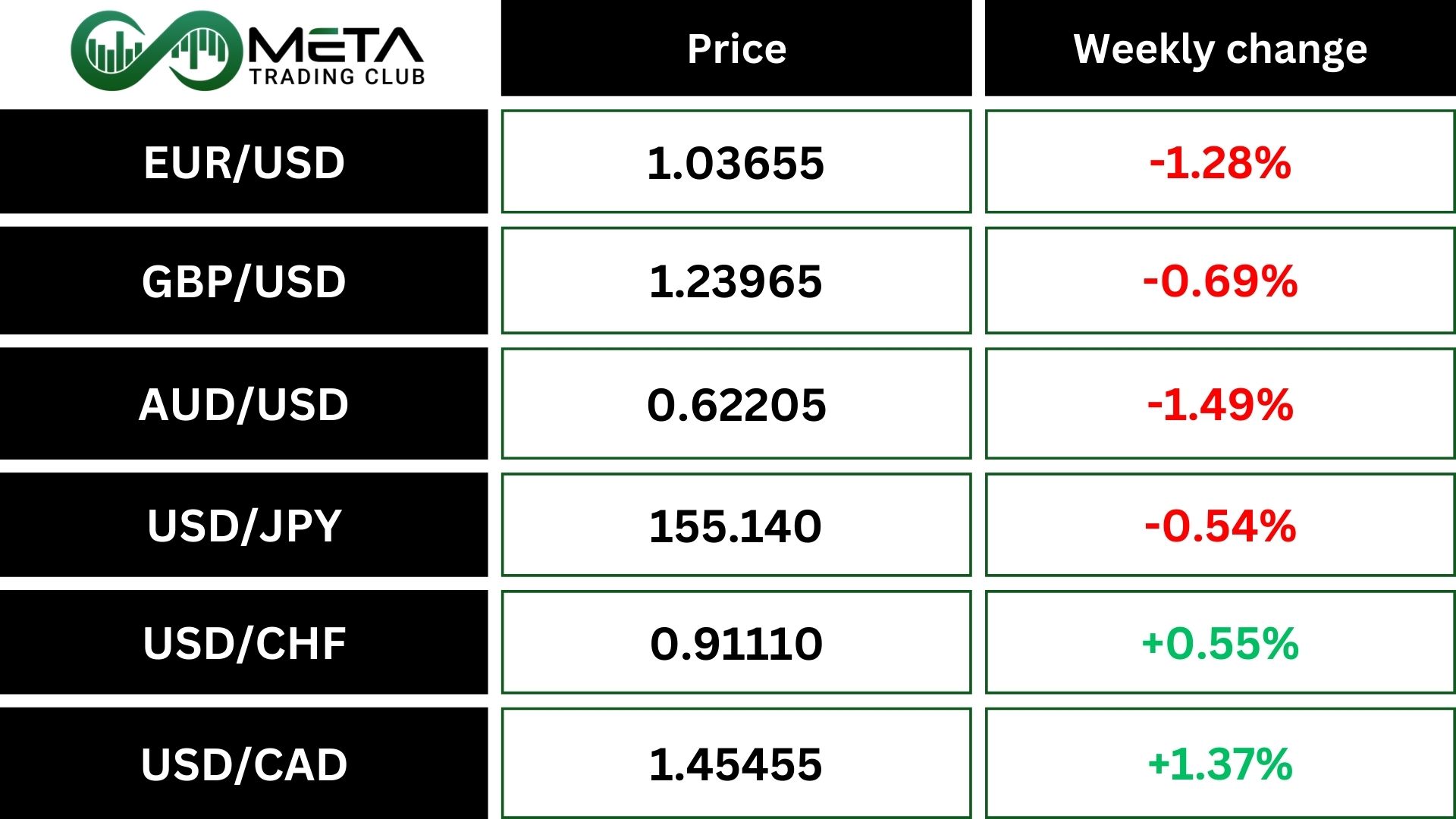

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The EUR/USD pair dropped below $1.04 last week. It passed the 50-day moving average, showing short-term weakness. The Federal Reserve kept interest rates the same but is worried about inflation.

The European Central Bank cut its interest rate to 2.75% and warned of economic problems. European GDP data showed no growth, missing expectations. The US, however, reported 2.3% GDP growth, showing a strong economy.

The dollar index (DXY) went above 108.2 because strong economic data showed that the Federal Reserve will likely keep rates high. The core PCE price index, which the Fed uses to measure inflation, increased and personal spending went up.

Wages grew at the slowest pace since 2021. The Fed kept rates the same, but Chair Powell said more progress on reaching the 2% inflation goal is needed before cutting rates.

Trump imposed 25% tariffs on Mexico and Canada, and possibly 10% on China, is also a concern for the market.

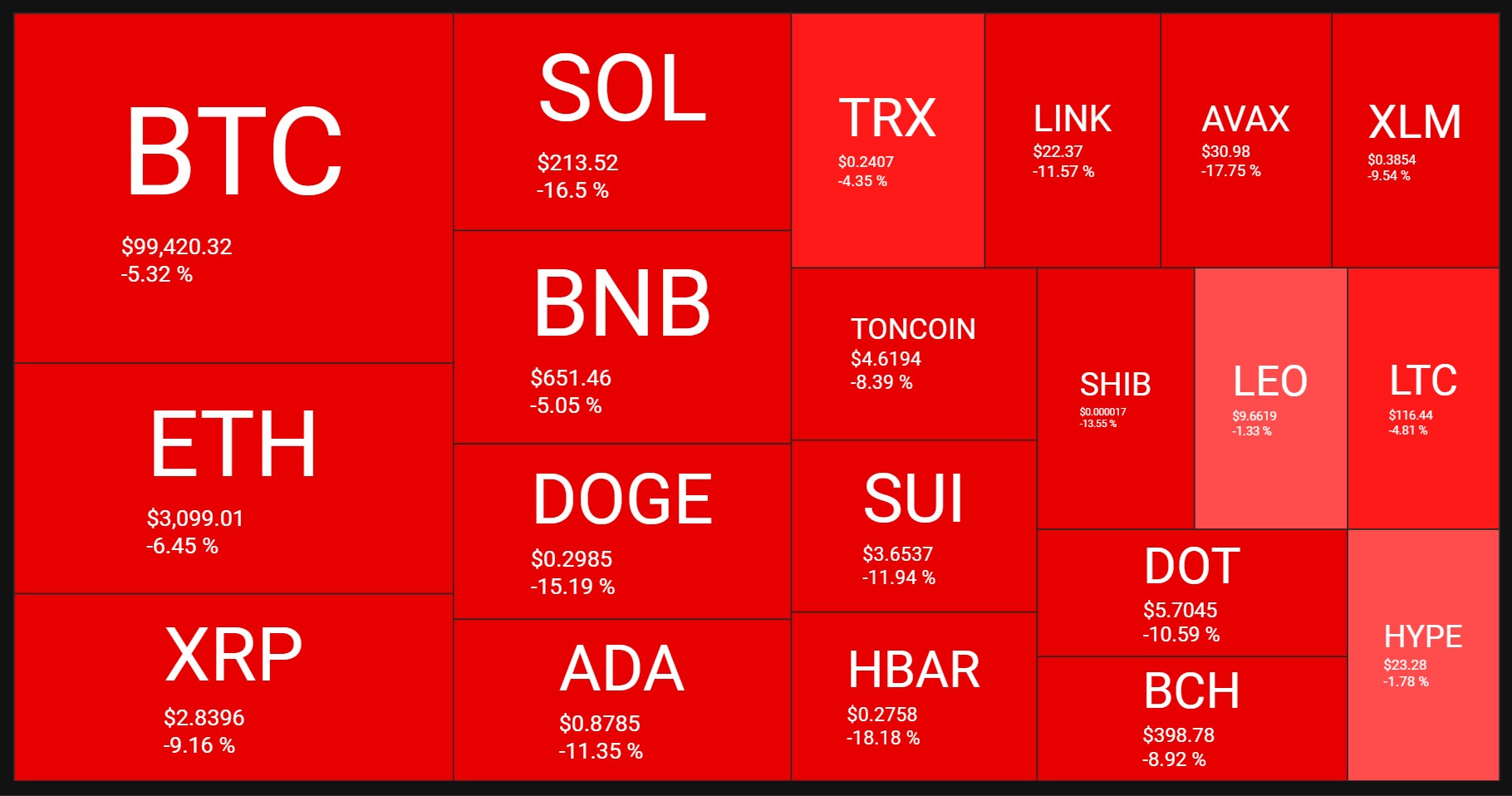

Crypto

Crypto Market Weekly Performance:

Source: quantifycrypto

The crypto market experienced a rough week overall, with many cryptocurrencies seeing significant declines.

The political landscape worsened over the weekend as Trump signed orders on Saturday, imposing tariffs on Canada, Mexico, and China. This led to a significant drop in Bitcoin price, which fell from over $106,000 to under $98,500.

Bitcoin is staying above its upward trend line, but the RSI indicator shows decreasing momentum, meaning buying strength is weakening.

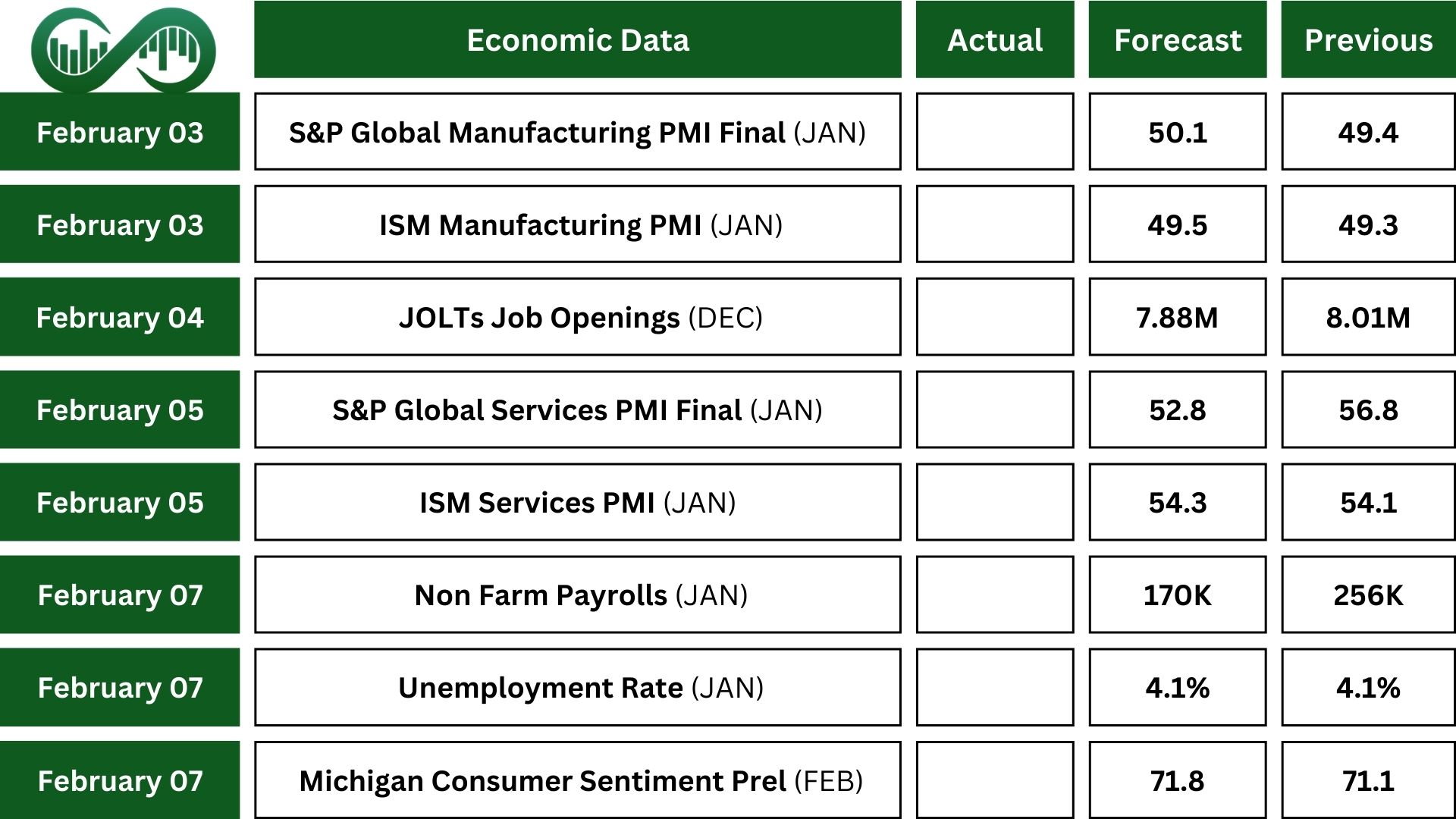

Next Week’s Outlook

Economic Events

It’s going to be a busy week in the US. The economy is expected to add 170,000 jobs in January, which is fewer than the 256,000 added in December. The unemployment rate is expected to stay at 4.1%, and wage growth at 0.3%.

Other important reports include job openings, private sector employment, and planned job cuts. The ISM reports will show how the economy performed in January, with services growing a bit and manufacturing shrinking less. Consumer confidence for February is expected to improve slightly.

Other key data includes factory orders, trade balance, labor costs and productivity, construction spending, and consumer credit. The Treasury Department will announce its plans for issuing debt. Several Federal Reserve officials will speak, as investors look for clues about the next rate cut.

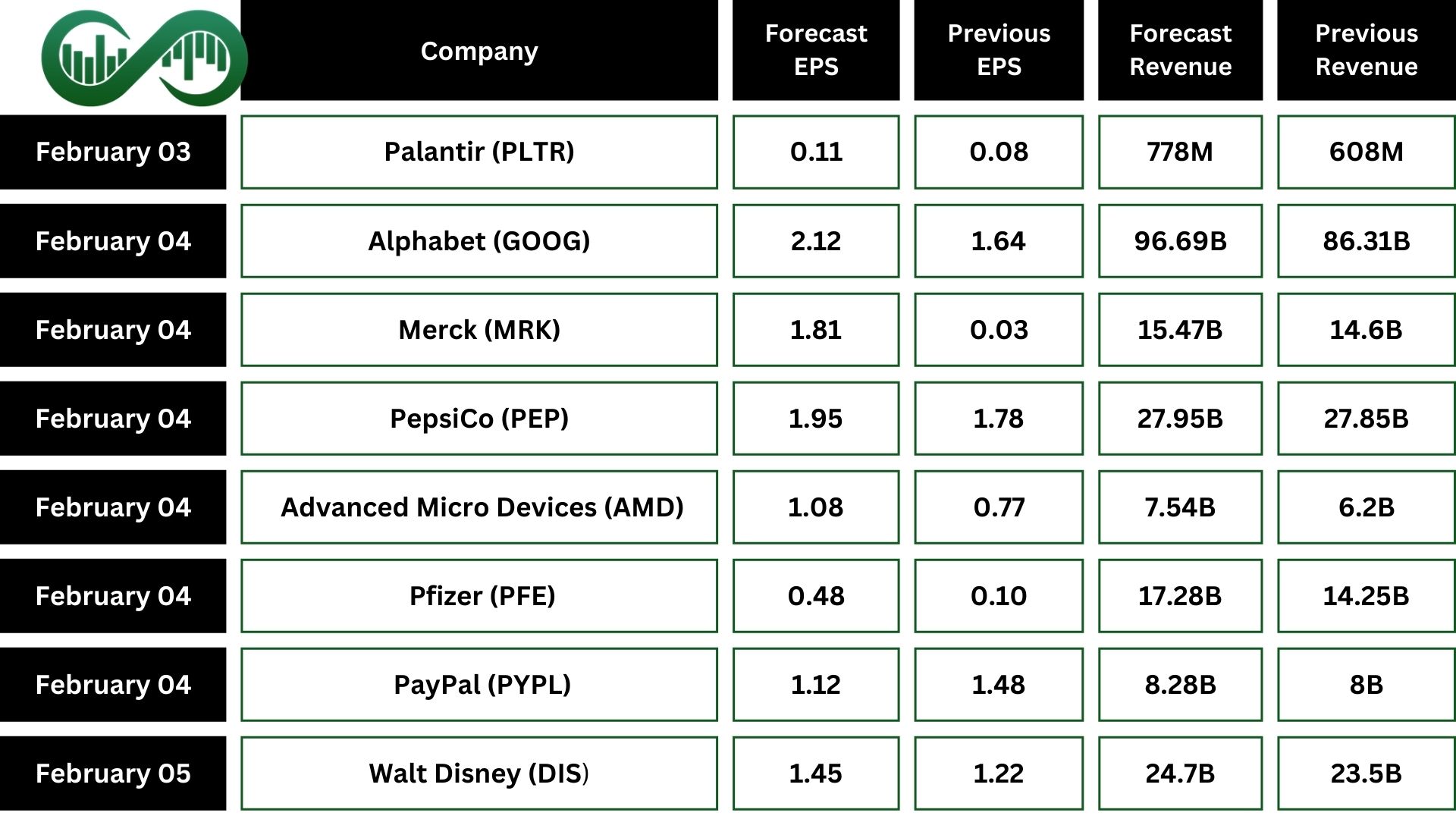

Earnings Events

Several big companies will report their earnings this week, including Amazon (AMZN), Alphabet (GOOG), Palantir Technologies (PLTR), Merck (MRK), PepsiCo (PEP), Advanced Micro Devices (AMD), Uber (UBER), Pfizer (PFE), Walt Disney (DIS), Qualcomm (QCOM), PayPal (PYPL), Eli Lilly (LLY), Philip Morris International (PM), and Honeywell (HON).