Last Week’s Reports

Economic Reports

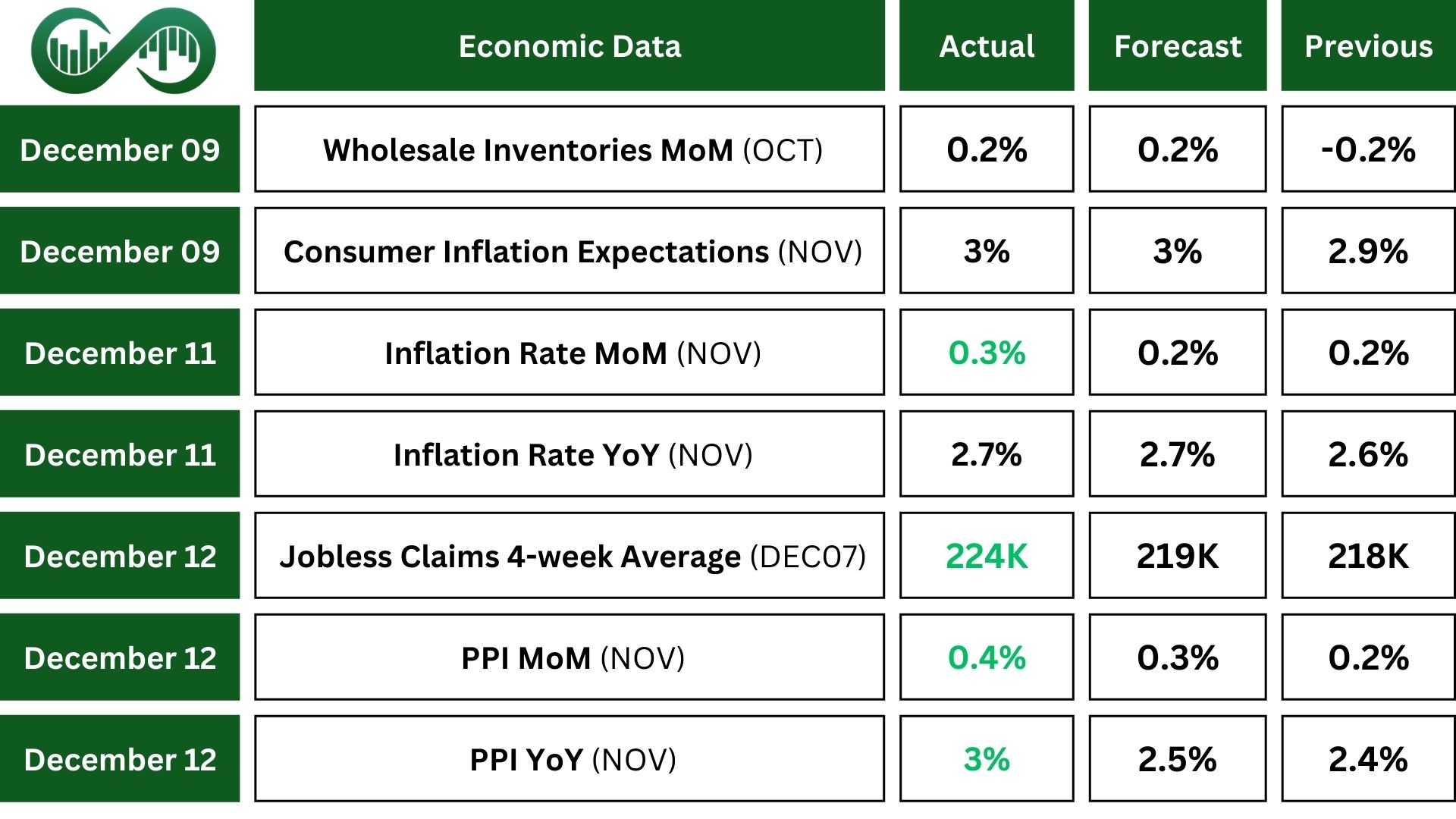

Wholesale inventories rose by 0.2% month-over-month to $905 billion, in line with estimates. Wholesale inventories increased by 0.9% year-over-year. These changes highlight significant growth in specific sectors, contributing to the overall rise in inventories.

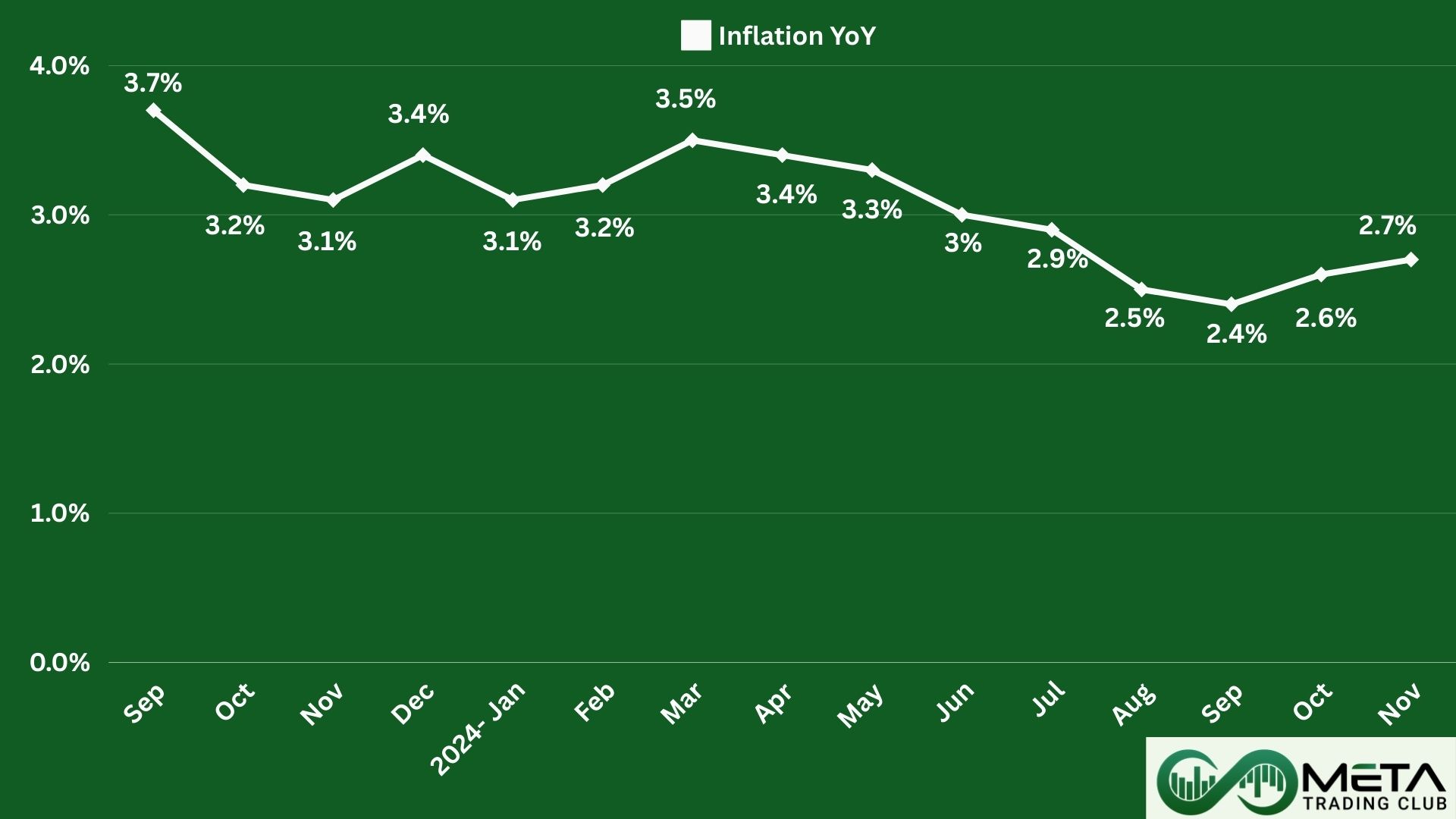

The November Consumer Price Index (CPI) for All Urban Consumers in the U.S. increased by 0.3%. Over the past year, this inflation index rose by 2.7%.

Also, in November, the Producer Price Index (PPI) for final demand in the U.S. increased by 0.4% on a monthly basis. Meanwhile, on a yearly basis, the PPI rose by 3%, which was higher than the expected 2.6%. This increase indicates a rise in producer prices, reflecting higher costs for goods and services.

In the first week of December, US initial jobless claims rose by 17,000 to 242,000, much higher than the expected 220,000. This is the highest number of new claims since October. Continuing claims also increased by 15,000 to 1,886,000, close to the three-year high from November. These results challenge recent hopes of a tight labor market, supporting the idea of more rate cuts by the Fed next year.

Earning Reports

Oracle

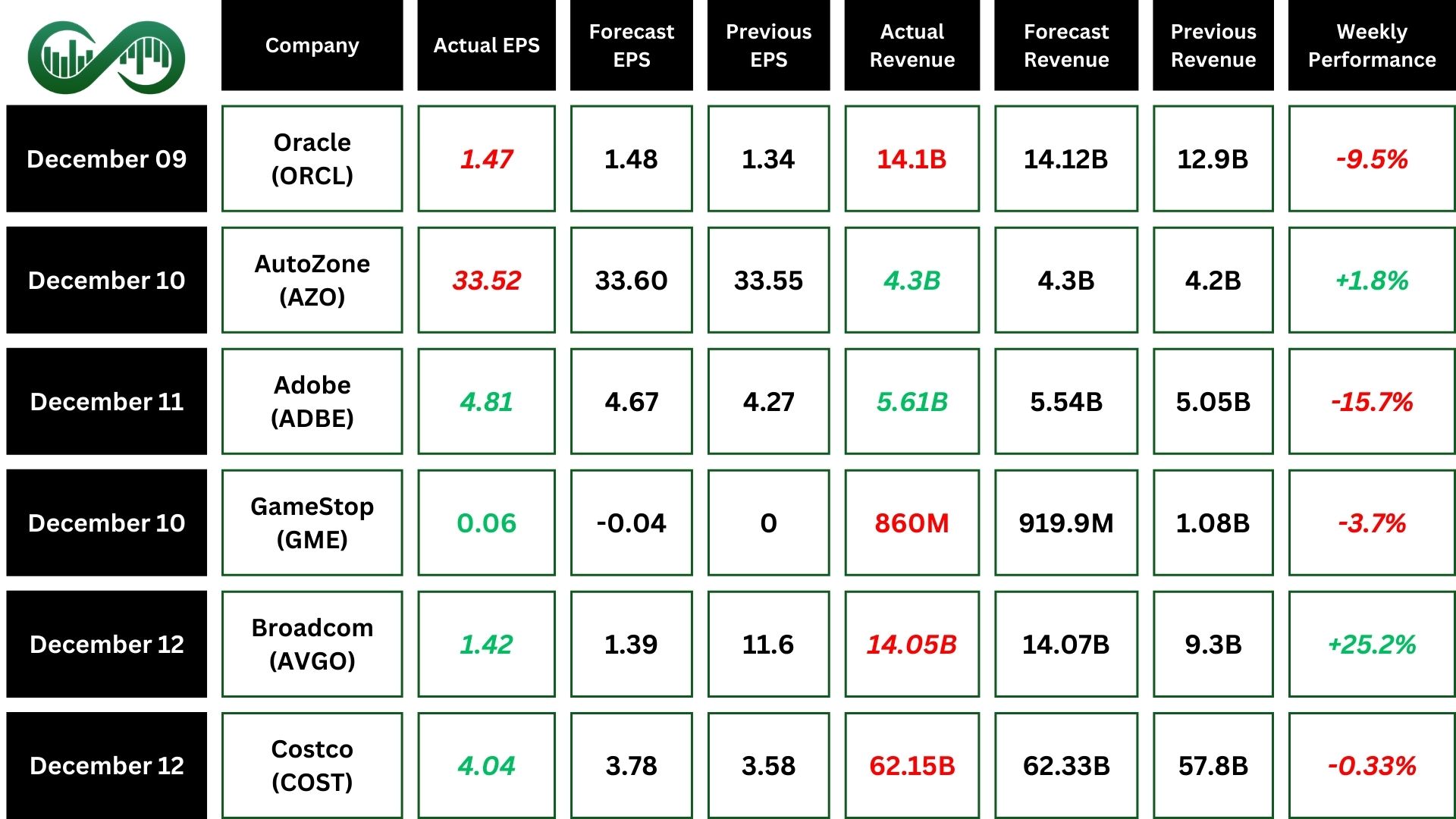

Oracle (ORCL) Q2 2025 fiscal report showed GAAP earnings per share (EPS) of $1.10, which was below expectations. Also, the company’s total revenue was $14.1 billion, slightly missing the forecasts of $14.12 billion.

Oracle’s investments in cloud infrastructure and AI are driving growth but lead to high capital expenditures, which can be a concern for investors worried about profitability and cash flow. Oracle fell about 10% after earnings were released.

Technically, ORCL recently broke its uptrend line and, after a pullback to the break point at 181, started to decline. The RSI indicates oversold conditions, and there’s a hidden divergence between the price and RSI, which remains valid as long as the price stays above 167. If the price holds above 167, it could signal a bullish rise to the trend line or even the all-time high around 198. However, if the price breaks below 167 and stays there, it could lead to further declines to the next support zone around 145.

AutoZone

AutoZone (AZO) reported its Q1, 2025 revenue of $4.3 billion, a 2.1% increase year-over-year, but slightly below expectations of $4.31 billion. The company’s earnings per share (EPS) were $32.52, missing the forecasts.

On the positive side, AutoZone’s international same-store sales grew by 1%, and the company opened 34 new stores during the quarter. However, domestic same-store sales growth of 0.3% fell short of the 0.74% growth expected.

The stock’s rise of 2%, indicates that investors are optimistic about the company’s performance and future prospects despite some areas where expectations were missed. It seems the positive aspects, such as international same-store sales growth and new store openings, outweighed the negatives for now.

The AZO stock broke strong ATH resistance.

Adobe

Adobe (ADBE) Q4, 2024 revenue reaching $5.61 billion, an 11% year-over-year growth, beats the forecasts. Also, the company also reported strong earnings, with GAAP EPS at $3.79 and non-GAAP EPS at $4.81, both exceeding estimates.

However, Adobe’s revenue forecast for 2025 fell slightly below expectations, causing some concern among investors. Adobe stocks fell 15% after earnings were reported.

Technically, ADBE recently broke an important level at 475, which has now become a resistance level. The recent price drop also filled a previous gap. Currently, there is key support around 433. In a broader view, the price has been ranging between 587 and 433, forming a significant trading range. As long as the price remains above 433, we can expect this range to continue.

Costco

Costco (COST) Q1 2025 reports showed net sales of $60.99 billion, 7.5% increase year-over-year, but slightly below the forecasted $62.1 billion. However, earning per share (EPS) exceeded expectations, achieving $4.04.

The company’s plans to open 20 more warehouses and raise membership fees further support positive market sentiment. Costco’s Q1 2025 earnings report didn’t have a significant impact on the stock price.

Broadcom

Broadcom (AVGO) reported Q4, 2024 revenue of $14.05 billion, marking a 51% yearly increase, slightly missing the forecasted revenue. Also, the company’s $1.42 EPS exceeded expectations.

For Q1 2025, Broadcom projects a revenue growth of 22% year-over-year, driven by strong demand for its AI chips. Broadcom rose significantly after announcing collaboration with Apple on developing an AI chip, reaching a $1 trillion market value with a 25% weekly gain.

Technically, AVGO recently broke a key resistance level at 186 by a gap and closed the weekly candle significantly above it, establishing 186 as a key support zone. There’s a Fibonacci cluster around 220 and 230, which might cause a retracement or consolidation in this area. As long as the price remains above 186, this level acts as support. If the price breaks above 235 and holds, it could lead to further increases.

Indices

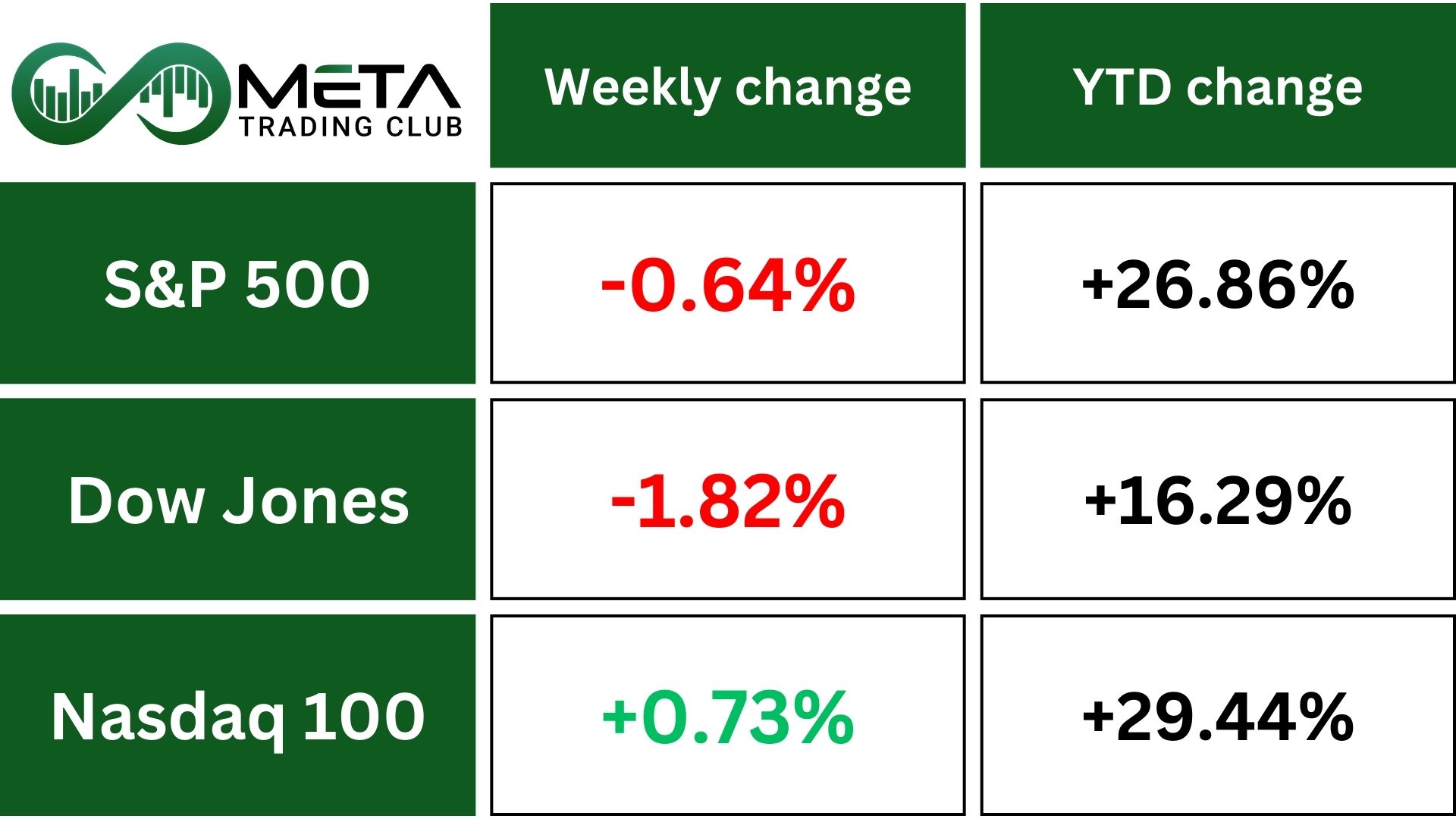

Indices’ Weekly Performance:

The S&P 500 snapped its three-week winning streak, ending down 0.6%. The Nasdaq Composite broke above 20,000 for the first time and achieved its fourth straight weekly gain, while the Dow fell by 1.8%, extending its losing streak to three weeks.

This week’s economic data showed that consumer inflation in November rose as expected, while producer prices increased more than predicted. There is now a 97% chance that the Federal Open Market Committee will cut interest rates by 25 basis points this week.

SPX currently has a major support level around 5853 and a key resistance at the Fibonacci level around 6151. If the index falls below 6029, it could potentially start a retracement. However, if it breaks up to 6100 and holds, it could lead to a further rise towards 6151.

Stocks

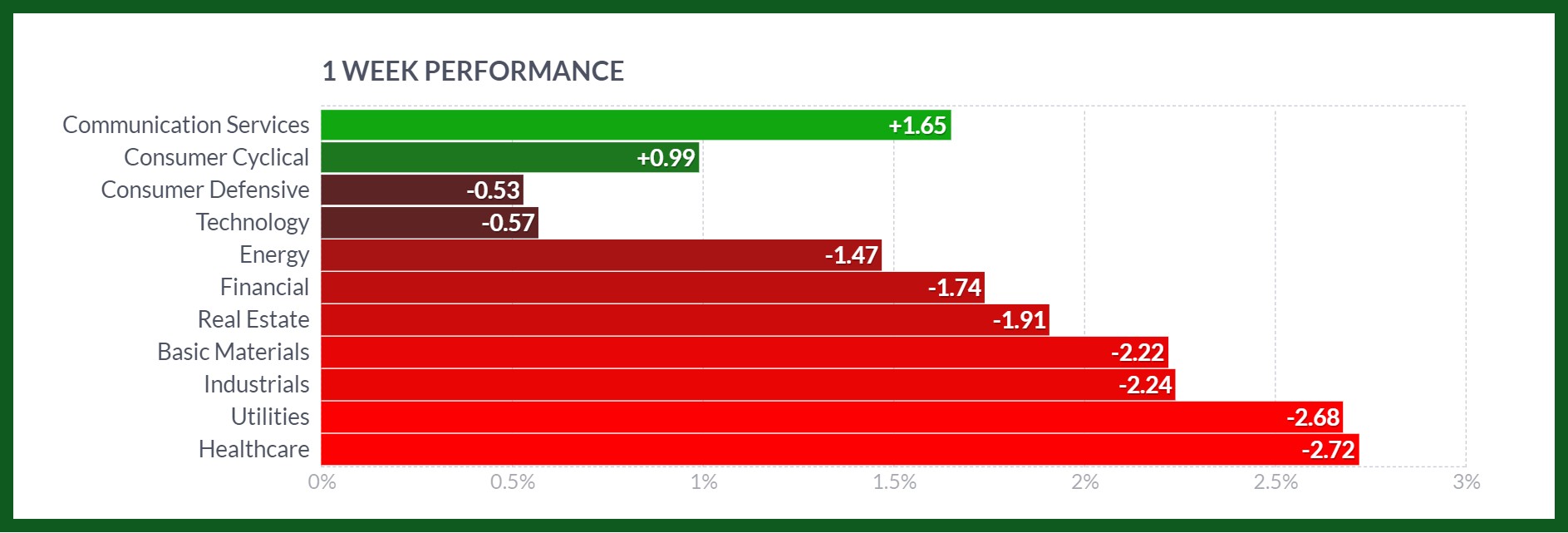

Sector’s Weekly Performance:

Source: Finviz

Gainers:

- Communication Services: This sector led the pack with a 1.65% increase, driven by Alphabet unveiling a new quantum-computing chip called Willow.

- Consumer Cyclical: This sector also performed well, rising by 1%, buoyed by favorable economic indicators.

Losers:

- Healthcare: The healthcare sector faced the steepest decline, dropping by 2.7%. As health insurers Cigna and CVS Health both dropped around 11% due to concerns over potential legislation.

- Utilities: This sector saw a 2.9% decrease, impacted by regulatory issues and market volatility.

- Industrials: The industrials sector declined by 2.24%. As GE Vernova declined after forecasting lower 2025 revenue in its wind segment. However, Boeing rose by 10% for the week after committing $1 billion to increase jet production.

- Basic Materials: This sector experienced a 2.22% drop, after UBS downgraded Steelmakers.

Stock Market Weekly Performance:

Source: Finviz

Top Gainers in the S&P 500

- Broadcom (AVGO): Experienced a significant 25% surge, driven by strong quarterly earnings and positive outlook in the semiconductor sector.

- Warner Bros. Discovery (WBD): Saw a notable 13% jump on plans to split its TV and streaming units.

- Tesla (TSLA): Climbed 12% which hit a record high, benefiting from its CEO Musk’s perceived relationship with the new U.S. President.

- Boeing Company (BA): Rose by 10% for the week after committing $1 billion to increase 787 jet production.

- Alphabet (GOOGL): Surged over 8% after unveiling a new quantum-computing chip called Willow.

- Arm Holdings (ARM): Saw a 7.8% increase, possibly due to the surging Broadcom which pushed the semiconductor sector up.

- Marvell Technology (MRVL): Rose by 6.4%, driven by surging Broadcom which pushed the semiconductor sector up.

Commodity

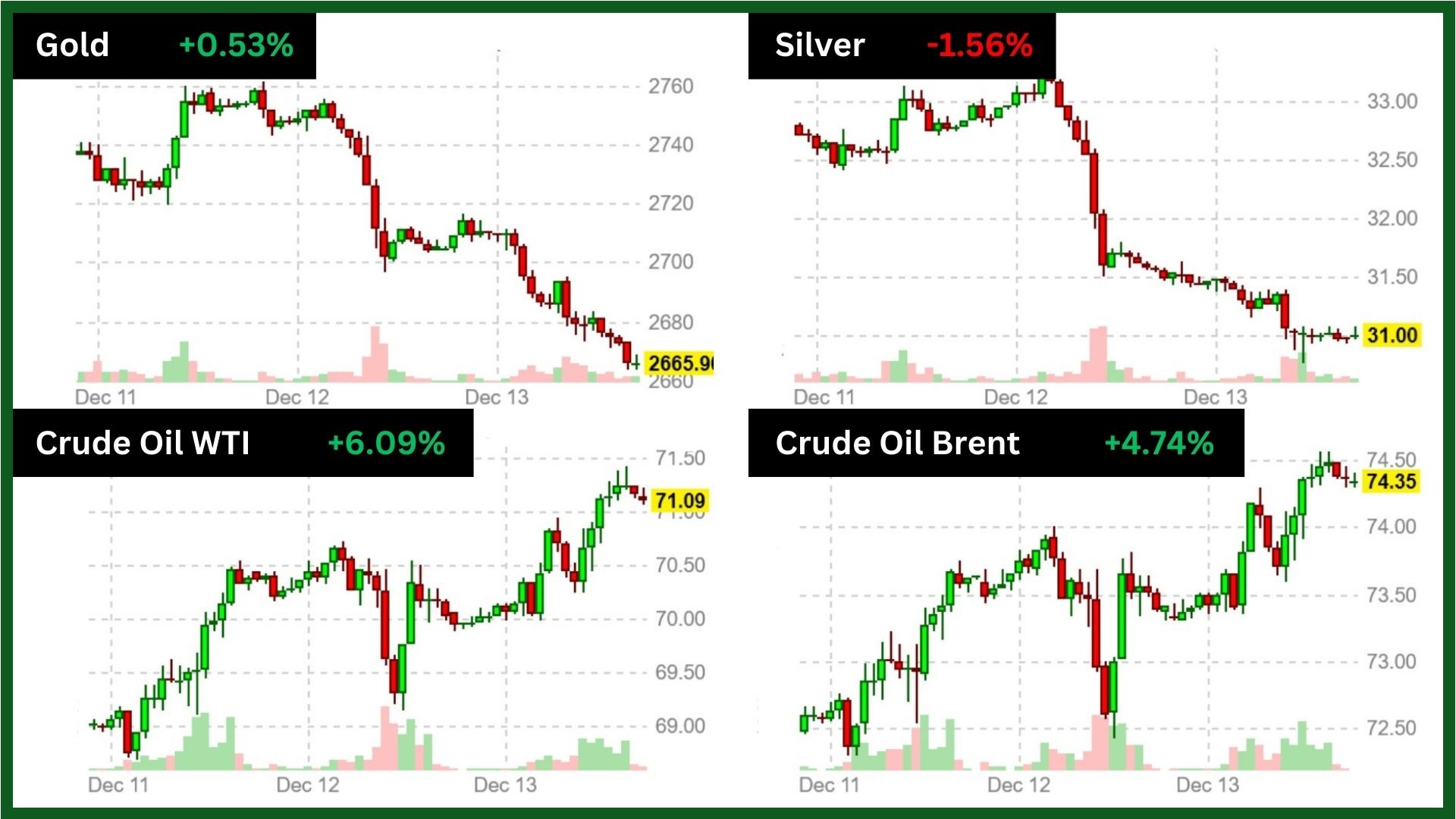

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold prices dropped after US factory gate costs (PPI) rose faster than expected in November, raising worries about persistent inflation and countering the lack of surprises in this week’s CPI report. However, the dovish stance of major central banks supported gold enough for a small weekly increase.

Currently, the price of XAU/USD is ranging between a support zone around 2605 and a resistance zone around 2730. From a broader perspective, the price remains neutral as long as it stays above 2536 and below 2790. Within this range, it isn’t decidedly bullish or bearish but merely fluctuating. Monitoring these key levels will be crucial for understanding the future direction of gold prices.

WTI crude oil marks the highest close since November 7 and a 6% gain for the week, driven by tightening global supplies and rising fuel demand.

The rally was influenced by expected sanctions on Russia and Iran, lower interest rate forecasts in the U.S. and Europe, and support from China’s economy. Also, the EU imposed new sanctions on Russia’s tanker fleet, and the U.S. is considering similar measures.

Meanwhile, China saw an increase in crude imports in November, prompting the IEA to raise its global oil demand outlook. Additionally, the U.S. Federal Reserve is expected to cut rates, with further reductions anticipated through 2025.

Forex

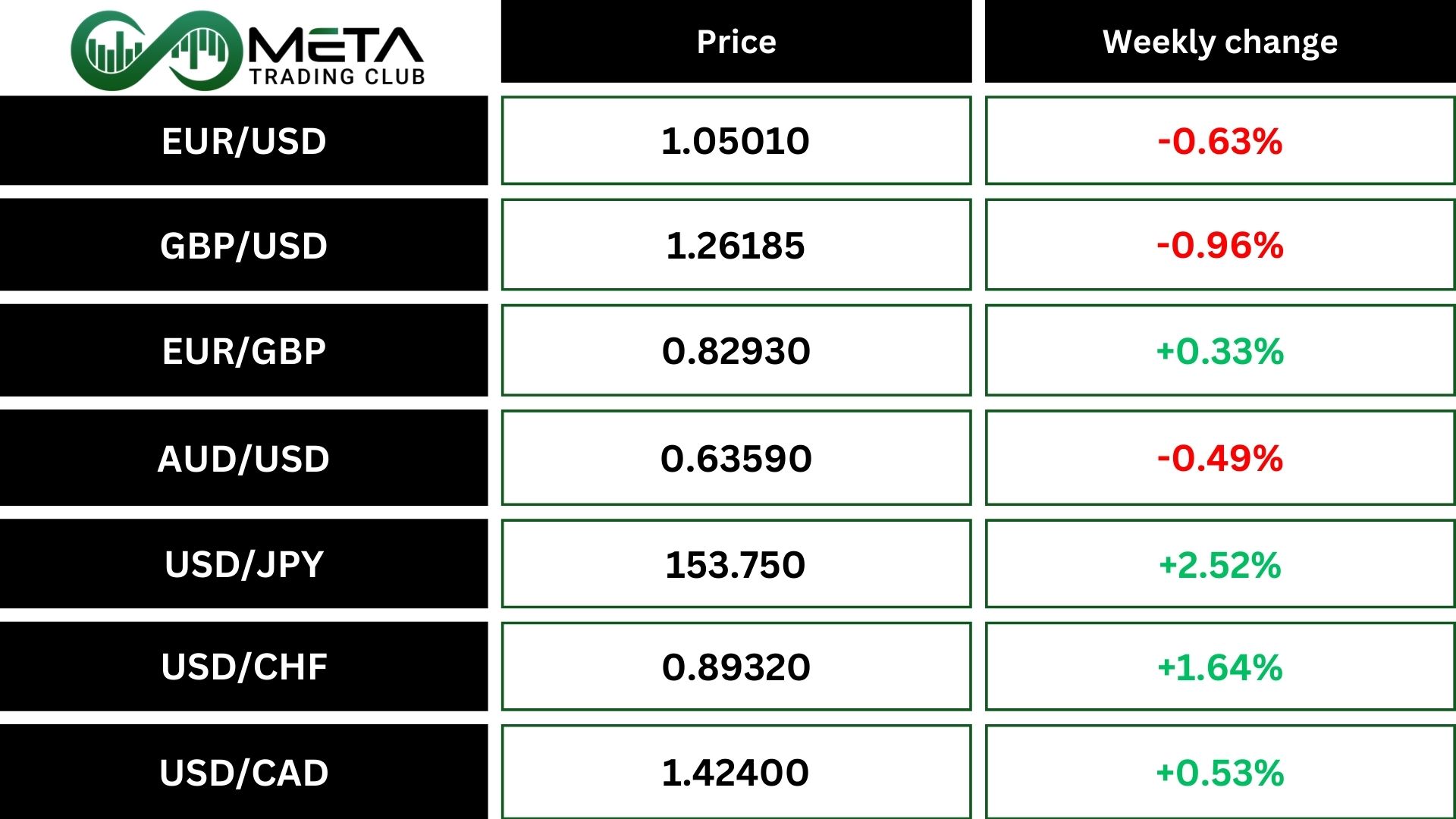

Weekly Performance of Major Foreign Exchange Pairs:

DXY: The dollar is on track for its best weekly performance, with investors expecting the Federal Reserve to cut rates more slowly next year. The dollar index is set for a nearly 1% weekly gain, its largest in a month.

USD/JPY: This week, the yen has been the worst performer against the dollar, which gained 2% on the Japanese currency. This drop is due to uncertainty on the Bank of Japan interest rate decision on Dec 19.

GBP/USD: The pound dropped because data showed the UK economy unexpectedly shrank in October, indicating a larger slowdown than expected.

EUR/USD: The euro fell against the dollar last week. On Thursday, the European Central Bank cut rates by 0.25% and signaled more cuts could come. Four European Central Bank policymakers support more interest rate cuts if inflation meets the ECB’s 2% target as expected.

USD/CHF: The Swiss franc was also under pressure after a surprise half-point rate cut by the central bank.

USD/CAD: Rate cuts and the potential for U.S. tariffs have pushed Canada’s dollar to a 4.5-year low.

USD/CNH:The Chinese yuan dropped per dollar in the offshore market. China might let its currency drop further to offset the effects of any U.S. trade war. Reports showed new bank lending in China increased much less than expected in November.

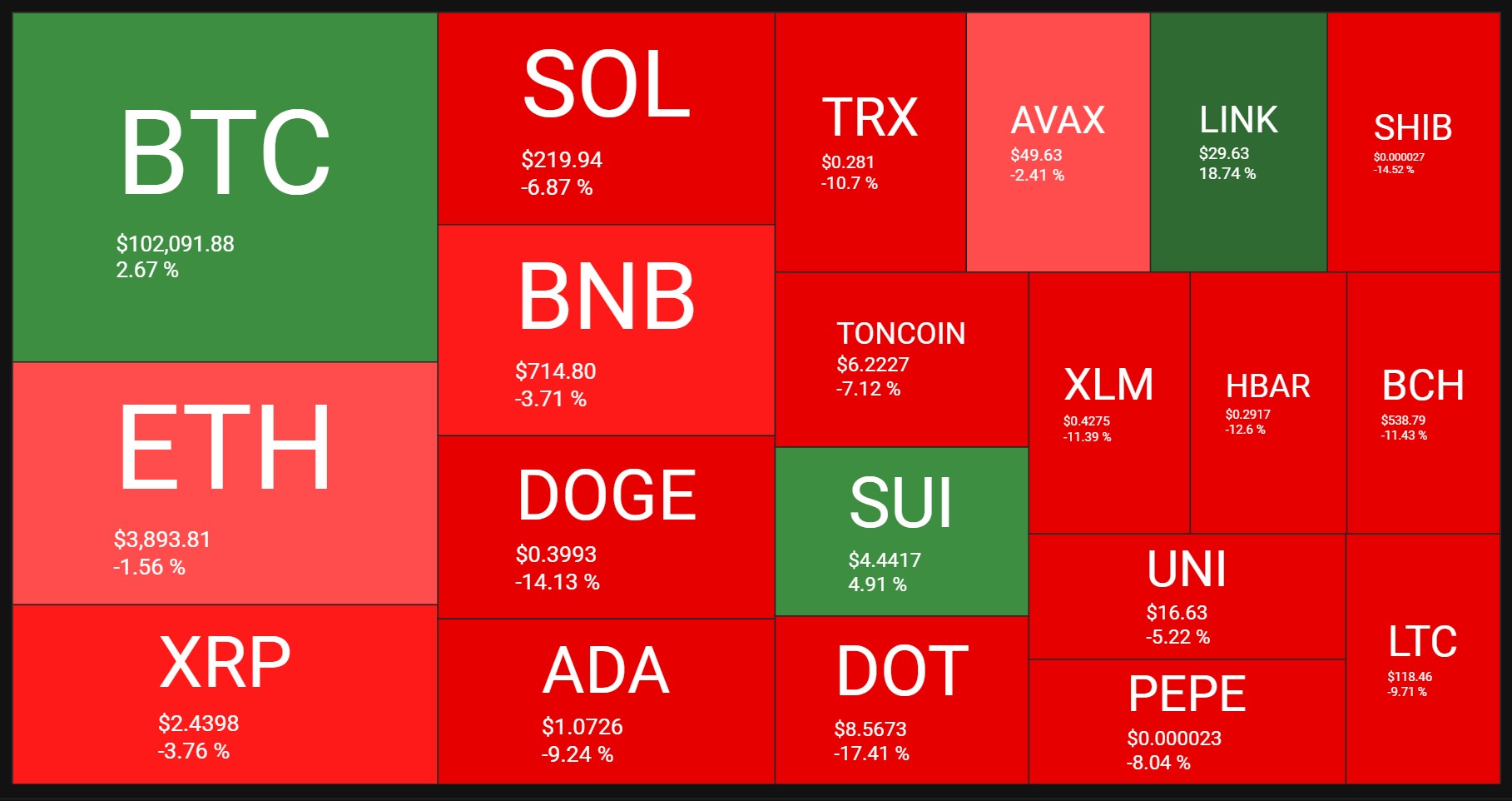

Crypto

Crypto Market Weekly Performance:

Source: quantifycrypto

Ethereum, the second-largest digital asset by market value has fallen more than 1% this week.

Ethereum is trying to break past the important $4,000 level as it nears its all-time high. Some analysts are doubtful about Ethereum’s performance in this cycle, thinking it might not do as well as in previous bullish phases. Despite this, Ethereum has shown strength, consistently finding buyers at key support levels and keeping a positive price trend.

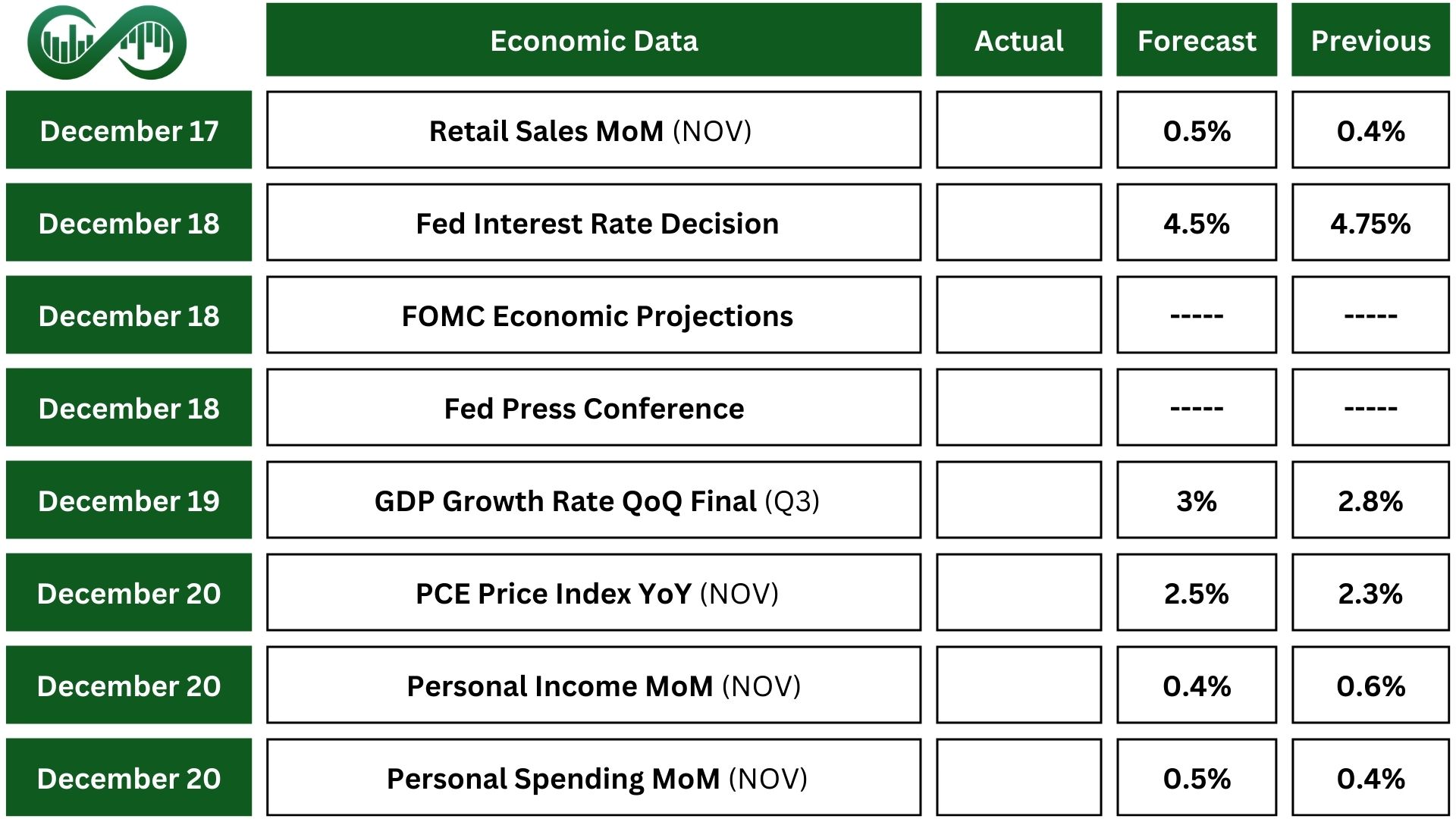

Next Week’s Outlook

Economic Events

In the US, all eyes will be on the Federal Reserve’s decision on monetary policy. The Fed is likely to reduce the federal funds rate by 0.25%, bringing it to a range of 4.25%-4.5%. This would be the third rate cut this year. Traders will also pay attention to the updated economic projections and any hints about the policy for 2025. Markets now expect the pace of rate cuts to slow down, with only three cuts anticipated next year.

Other key economic data to watch includes the November PCE inflation that is forecasted to be 2.5%. Also, expected 0.5% rise in personal spending, with income growth slowing to 0.4%.

Retail sales are predicted to grow by 0.5% in November, up from October’s 0.4%.

Industrial production expects to rebound with a 0.1% increase after a 0.3% decline.

Also, Flash S&P Global PMIs for December anticipate a slight slowdown in private sector activity.

Other notable releases are Final GDP growth for third quarter, housing starts, building permits, Philadelphia Fed Manufacturing Index, existing home sales, and final Michigan Consumer Sentiment figures.

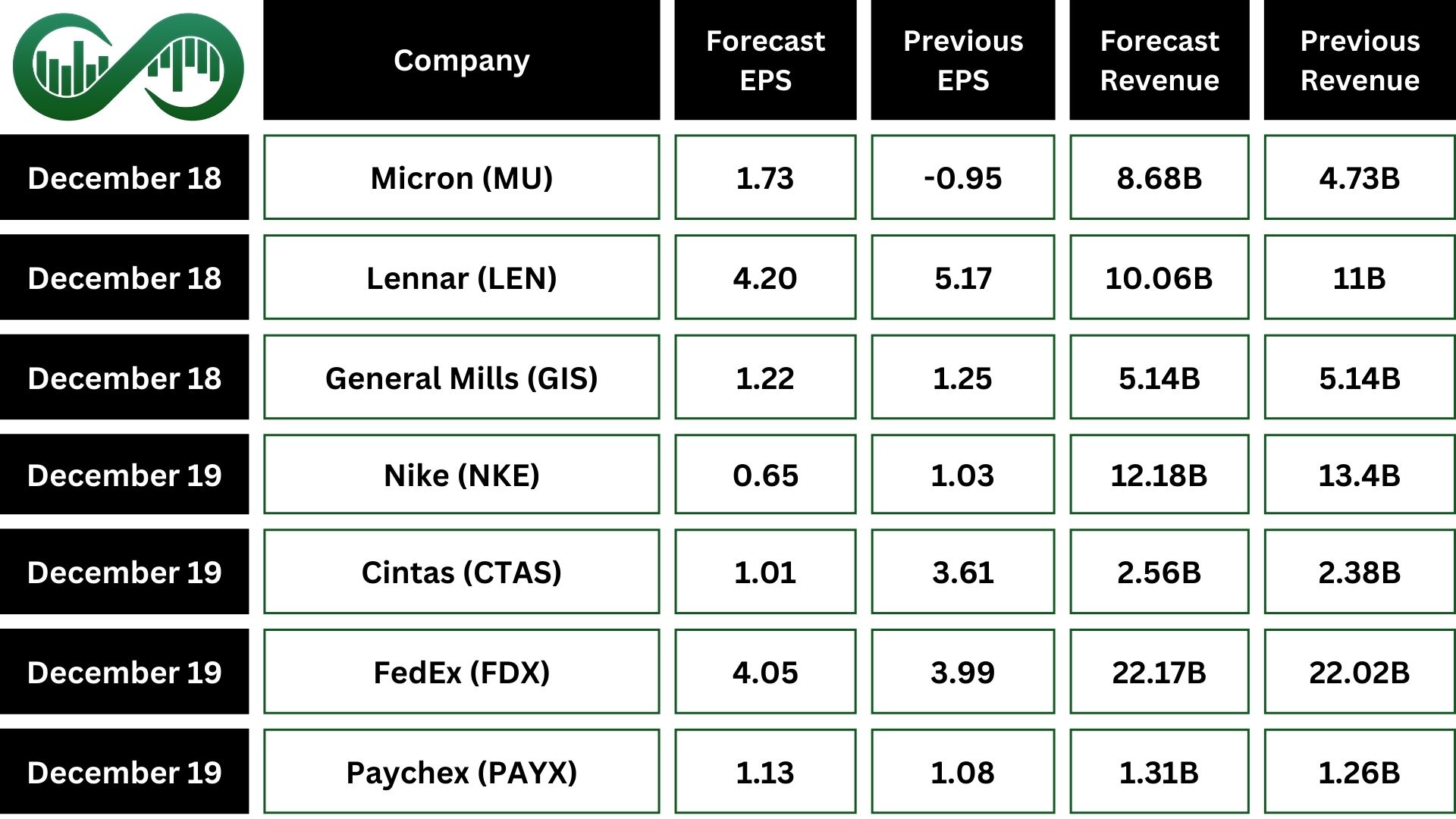

Earning Events

Earnings reports are expected from companies including Nike (NKE), Micron (MU), Lennar (LEN) and FedEx (FDX)