Last Week’s Reports

Economic Reports

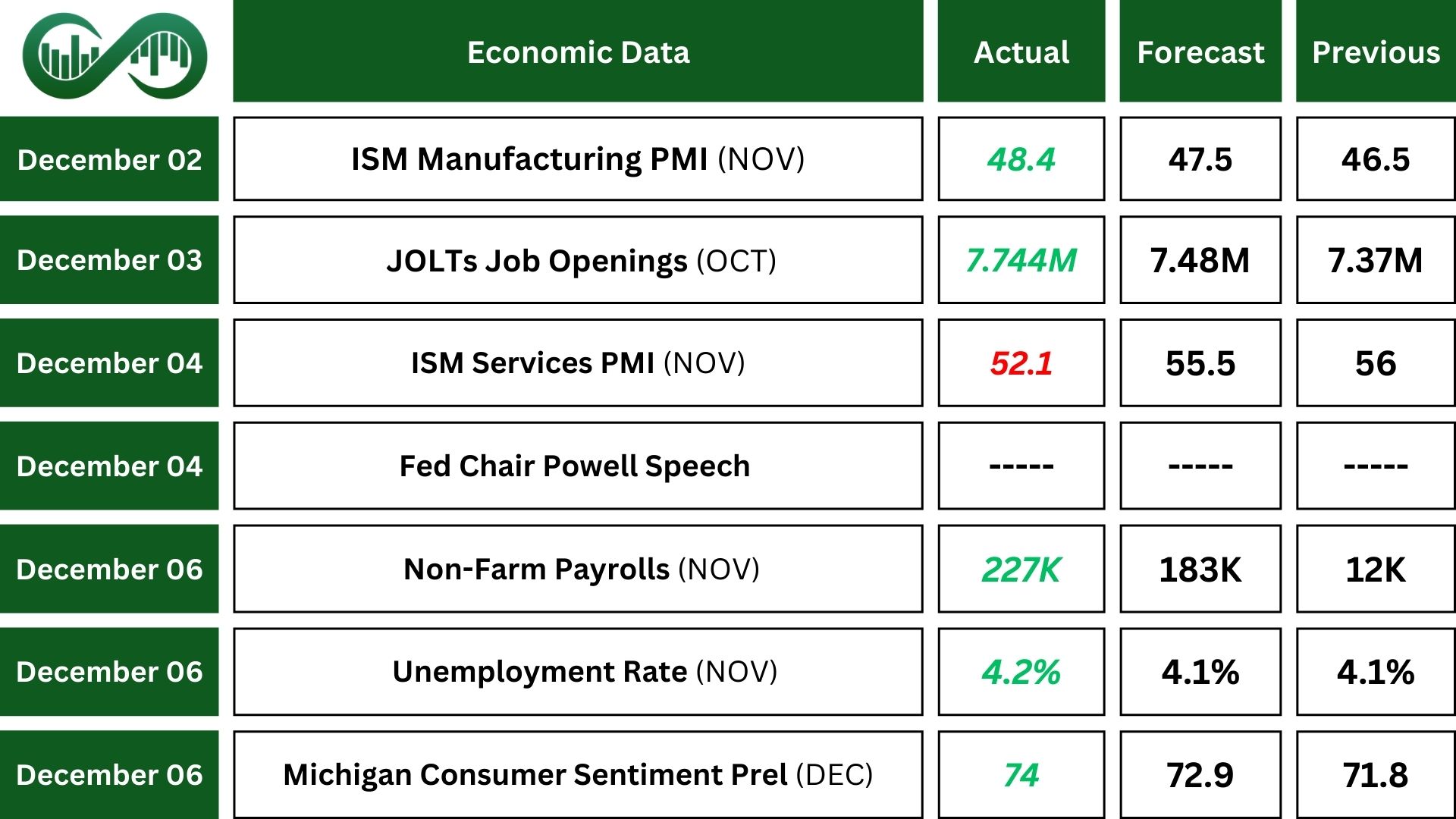

In November, the Manufacturing ISM Report showed an improvement, with the PMI rising to 48.4, indicating slower contraction. New Orders moved into expansion at 50.4%, but Production still contracted at 46.8%.

The S&P Global PMI showed the US Manufacturing PMI at 49.7, up from 48.8, suggesting near stabilization. New orders declined less, and firms were more optimistic, hiring more staff.

In October, there were 7.7 million job openings, and both hires and separations remained steady at 5.3 million. The quits rate slightly increased to 2.1%, meaning more people voluntarily left their jobs. Layoffs stayed the same at 1%. Over the past year, job openings have decreased, showing a cooling labor market.

In November, the S&P Global US Composite PMI was 55.3, up from October, showing strong business growth.

The ISM US Services PMI was 52.1, down from October, indicating slower growth but still expanding. This signifies a slowdown in services.

On December 4, Fed chair Powell spoke about the strength of the U.S. economy, stating it was performing better than expected. This allows the Fed to be cautious with further rate cuts. He hinted at a possible rate cut in the December 17 meeting to maintain economic stability.

In November, the U.S. added 227,000 jobs, surpassing expectations. The unemployment rate rose a bit to 4.2%. Significant job gains were seen in health care , leisure and hospitality , and government.

In December, U.S. Michigan consumer sentiment reached 74, the highest since April, up from 71.8 in November and surpassing the expected 73. Short-term inflation expectations rose to 2.9%, the highest in five months, while the five-year outlook slightly decreased to 3.1% from 3.2%.

Earning Reports

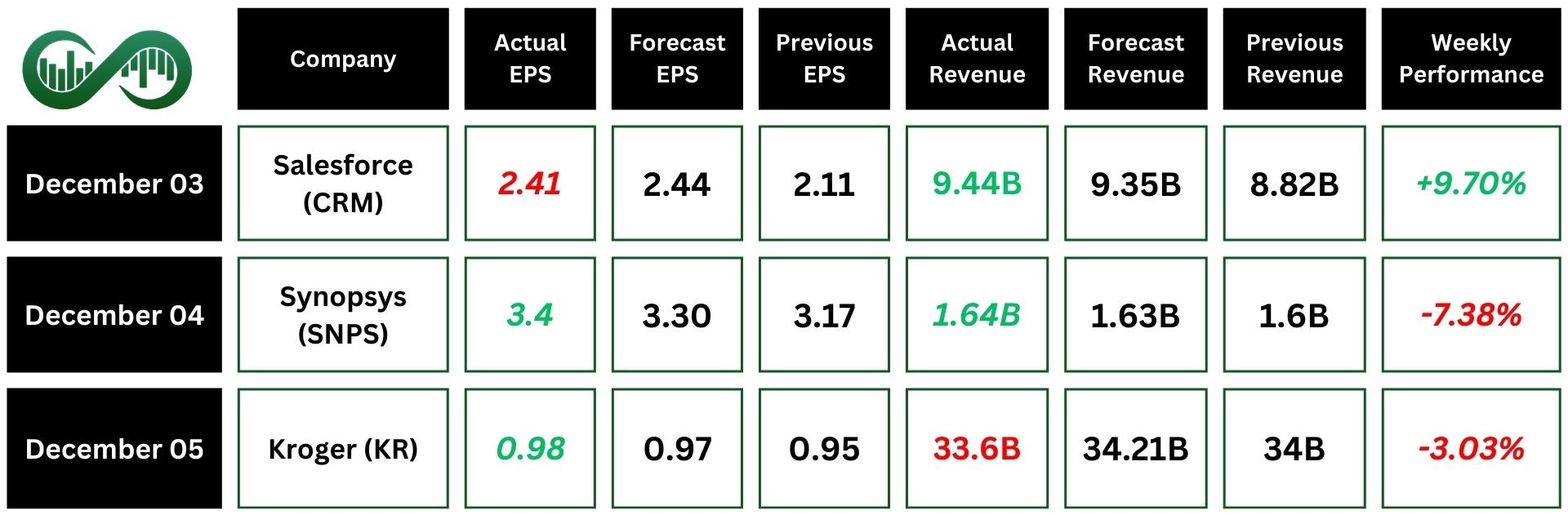

Salesforce

In Q3 2025, Salesforce (CRM) reported a revenue of $9.44 billion, surpassing the estimated. The company also reported an earnings per share (EPS) of $2.44, slightly below the forecasted $2.44.

Salesforce highlighted an 8% year-over-year increase in revenue, with net income rising 25% increase from the previous year.

Key factors for Salesforce’s strong performance included progress in their AI projects, especially the “Agentforce” platform for creating and deploying AI agents. They also raised their full-year revenue forecast to $37.8 – $38 billion, which was higher than expected. Operating cash flow increased by 29% compared to the previous year.

Following the earnings report, Salesforce’s stock jumped 9.7%, thanks to the positive revenue numbers, optimistic outlook, and advancements in AI that boosted investor confidence.

Salesforce stock is in a bullish trend with major supports of 348 and 318. CRM could show us more rise in the price as long as the price keeps its uptrend line or the last higher low around 323.

Synopsys

Synopsys (SNPS) reported record quarterly revenue of $1.636 billion for Q4 2024, up 11% year-over-year, surpassing estimates. Also, EPS was $3.40, exceeding expectations.

Key highlights from the earnings call included the successful sale of Synopsys’ Software Integrity business and the pending acquisition of Ansys, expected to close in the first half of 2025.

However, despite these strong results, Synopsys’ stock dropped 7% due to weaker-than-expected revenue guidance for Q1 2025, projected at $1.435-$1.465 billion, below estimates. The company also cited a change in its fiscal year calendar as a factor.

SNPS’s major supports are 457 and 450 and major resistances are 625 and 630. The price is currently breaking down an uptrend line and as long as it stays below that trend line, it could decline more down to the support zone.

Kroger

Kroger (KR) Q3 2024 earnings report showed a revenue of $34.3 billion, slightly below the estimates.

The company’s earnings per share (EPS) came in at $0.84, missing the estimates.

Key highlights from the earnings call included strong digital sales growth of 11%, an increase in total households, and the successful execution of Kroger’s go-to-market strategy.

However, the stock dropped by 3% post-earnings report due to concerns over the sale of Kroger’s specialty pharmacy business, which reduced total sales by $340 million and impacted margins. Additionally, investors were worried about the uncertain macroeconomic environment and potential risks from operating expenses.

Kroger’s major support is around 58 and major resistance is around 63. The price is in a bullish trend. As long as the price remains above the trend line or above the support zone around 58, it could rise up to its all-time high around 63.

Indices

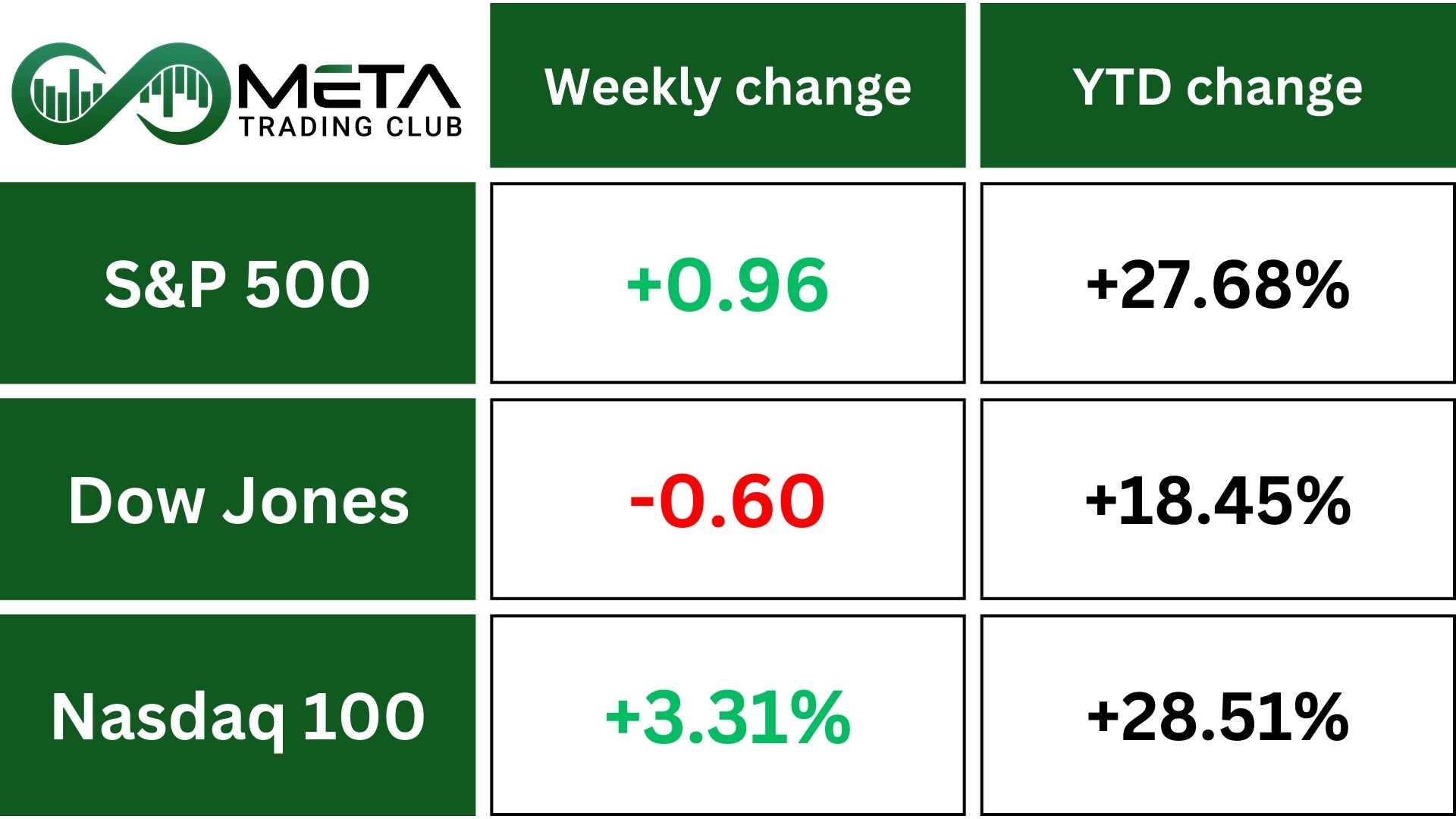

Indices’ Weekly Performance:

Throughout the week, the Nasdaq surged by 3.3%, the S&P 500 gained 1%, while the Dow declined by 0.6%.

SPX’s major support is around 5853. Also, has a major resistance at fibonacci level around 6151. The index is currently in a bullish trend. As long as it keeps the support, it could surge more. However, if it loses the support, it might be a potential bearish signal for retracement.

NDX has two major supports at 21180 and 20315. The index is in a bullish trend. As long as it remains above the uptrend line or keeps the support of 20315, the bullish trend remains strong. However, if the index breaks the trend line or falls below the support, it could be a bearish signal to the market.

Stocks

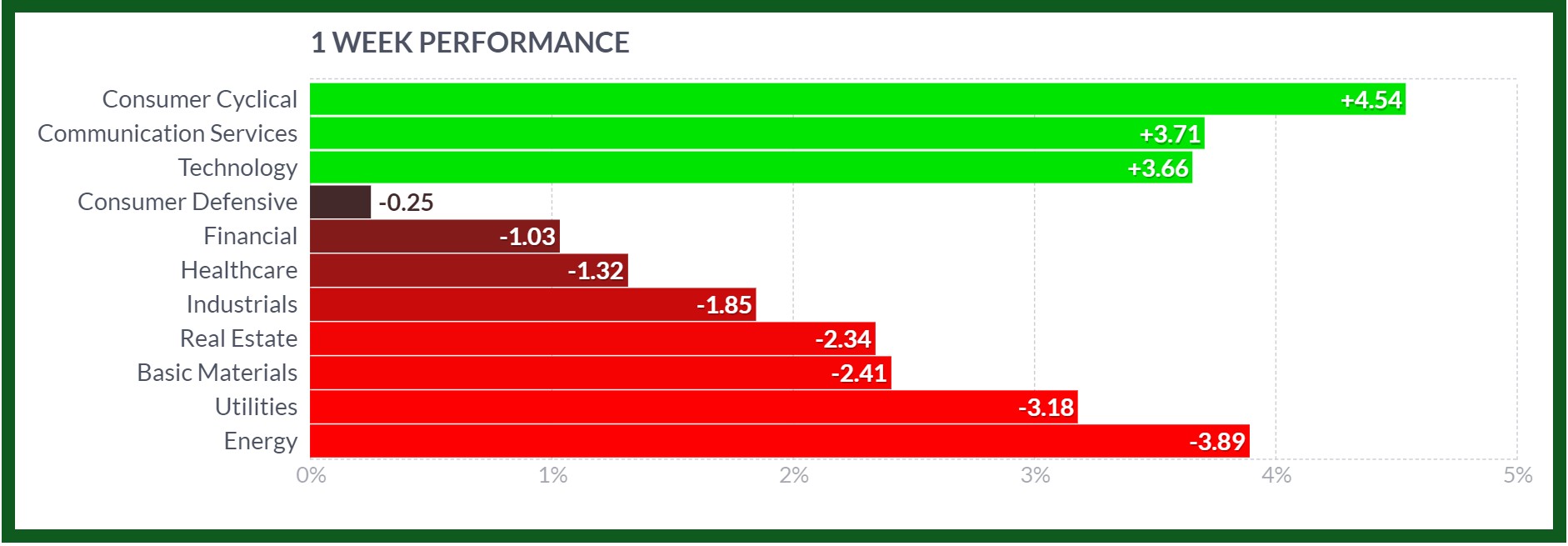

Stock Market Sector’s Weekly Performance:

Source: Finviz

Consumer Discretionary, Communication Services and Technology lift, while Utilities and Energy descend most.

Last week’s sector performance:

- Consumer Cyclical: This sector had the best performance, increasing by 4.54%. Strong retail sales and optimistic holiday spending projections contributed to this growth.

- Communication Services: Up 3.71%, driven by gains in media and telecom companies. Increased advertising revenue and the rollout of new 5G services played a significant role.

- Technology: Experienced a 3.66% rise, supported by ongoing demand for innovative solutions. Also, the semiconductor sector advances 2.7% on the week.

- Healthcare: Dropped by 1.32%. Regulatory uncertainties and mixed performance across biotech and pharmaceutical companies were contributing factors.

- Utilities: Declined by 3.18%, with higher energy costs and regulatory challenges weighing on the sector.

- Energy: Experienced the biggest drop, down 3.89%, due to falling oil prices and concerns about future demand.

Stock Market Weekly Performance:

Source: Finviz

S&P 500 Top Gainers

- Super Micro Computer (SMCI): The stock price surged by 34.59% after the panel found no evidence of fraud regarding accounting practices.

- lululemon athletica (LULU): jumps 24.6% on week after raising annual forecasts on strong holiday demand,

- Marvell Technology (MRVL): The stock price rose by 22.46% after positive earnings reports.

- Applovin Corporation (APP): The stock price went up by 19.23%, likely due to traders’ optimistic look.

- Palantir Technologies (PLTR): The stock price saw a 13.80% rise driven after expanded collaboration with AI shield.

- Tesla (TSLA): The stock price went up by 12.77%, driven by rises on 2025 growth optimism.

- Broadcom (AVGO): The stock price rose by 10.77%, after the company launched new technology targeting AI customers.

- Ulta Beauty (ULTA): The stock price saw a 10.74% rise driven by annual profit forecast raise.

- Salesforce (CRM): The stock price experienced a 9.70% rise due to a strong earnings report.

- Amazon.com (AMZN): The stock price increased by 9.21%, driven by a boost in Amazon Web service.

- Meta Platforms (META): The stock price saw an 8.61% rise, reaching its all-time record after a US appeals court upheld the TikTok ban.

Commodity

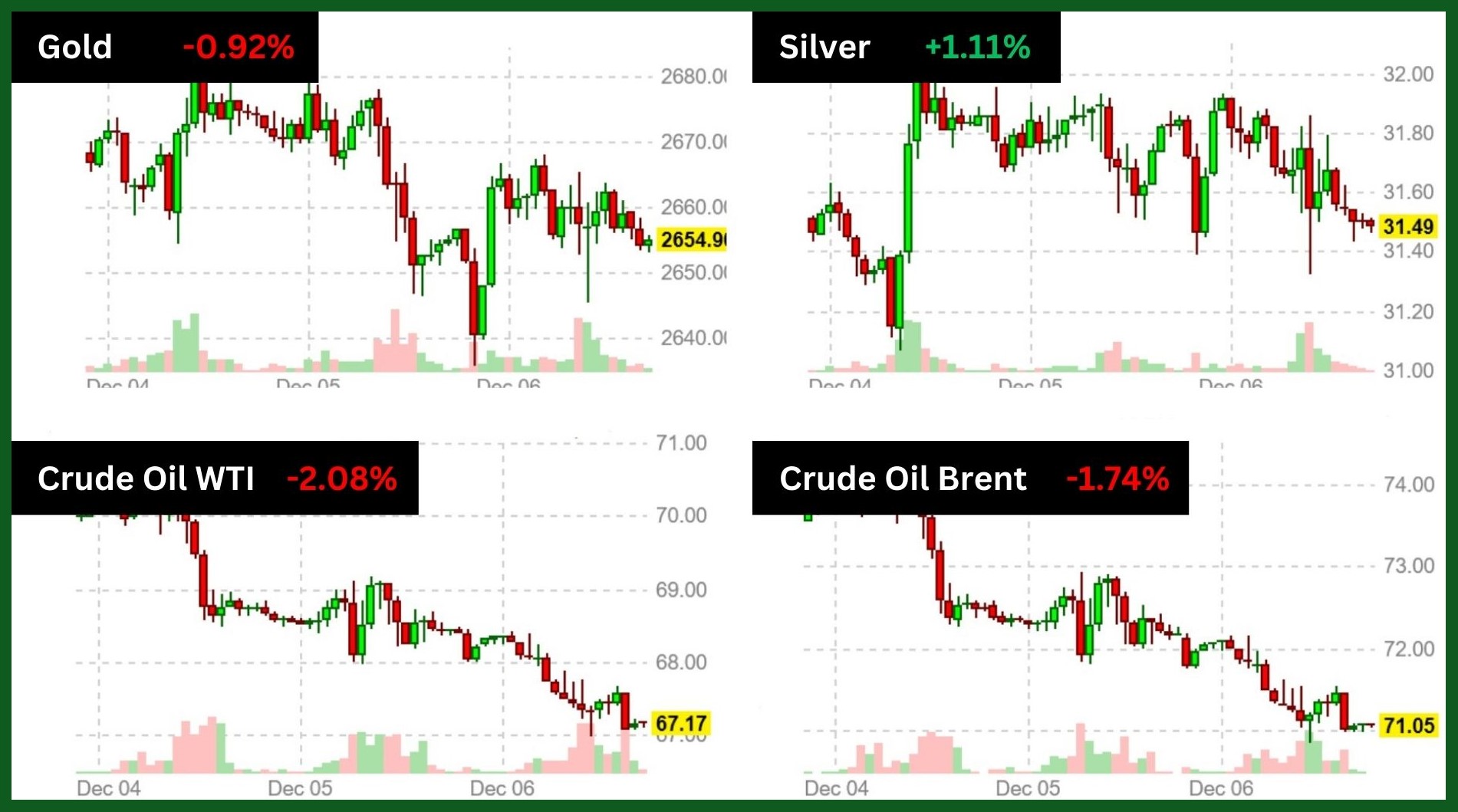

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Oil prices dropped 2% last week due to rising concerns about weak demand, following the decision by OPEC and its allies to delay planned supply increases and extend major output cuts until the end of 2026.

GOLD has support around 2605 and 2535. Resistances are around 2722 and 2790. After breaking the uptrend line, the price started a retracement phase. As long as the price remains above 2535 and below 2722, it is consolidating.

Forex

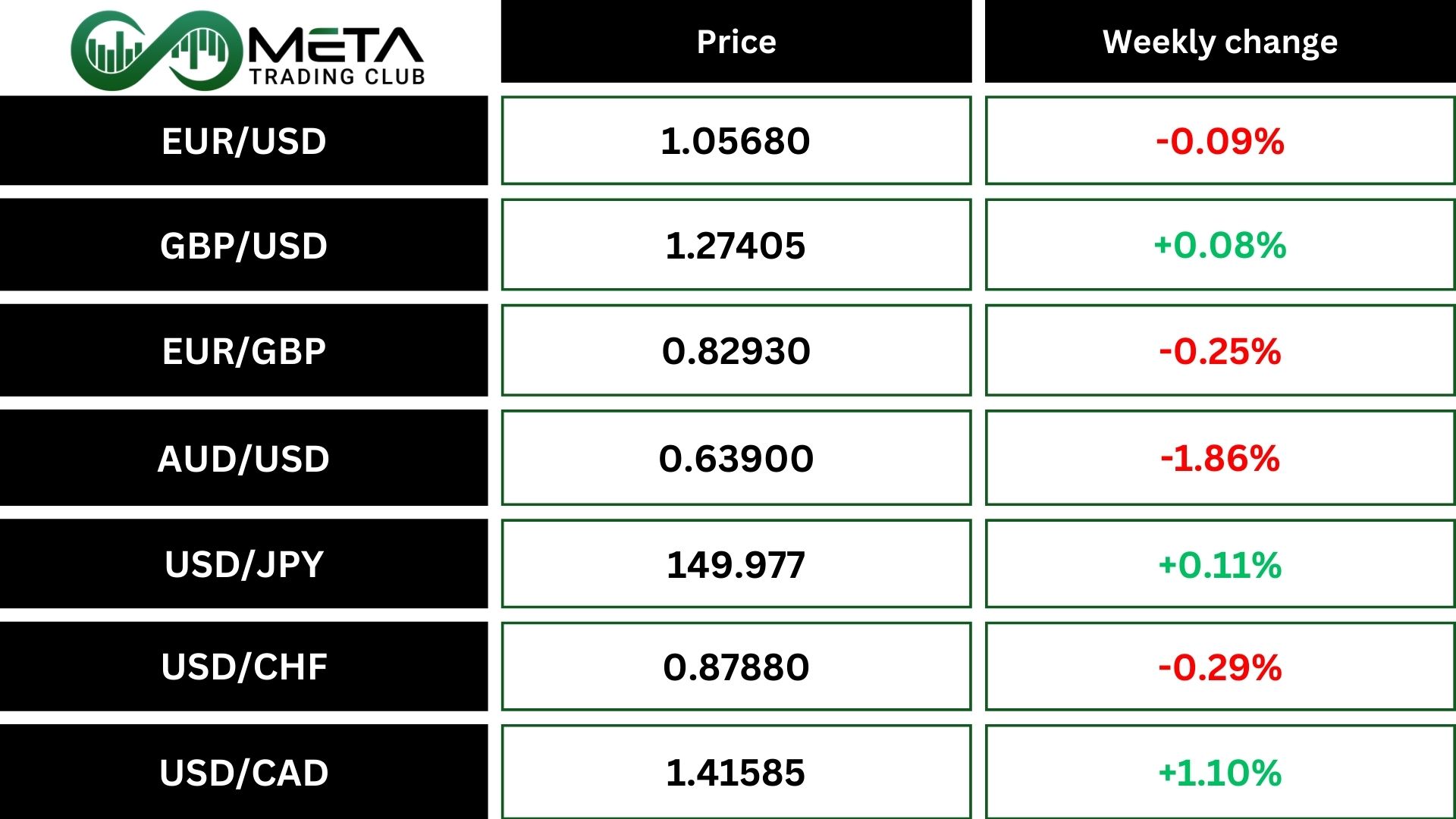

Weekly Performance of Major Foreign Exchange Pairs:

EUR/USD: The greenback recovered from a three-week low against the euro, which last week dropped 0.1% to $1.05680. The euro was set to end the week lower, posting losses in four of the last five weeks.

USD/JPY: Against the yen, the dollar rose from session lows to trade around 150 yen. The U.S. currency will end the week up 0.11% versus the yen, gaining in three of the last four weeks.

Crypto

Crypto Market Weekly Performance:

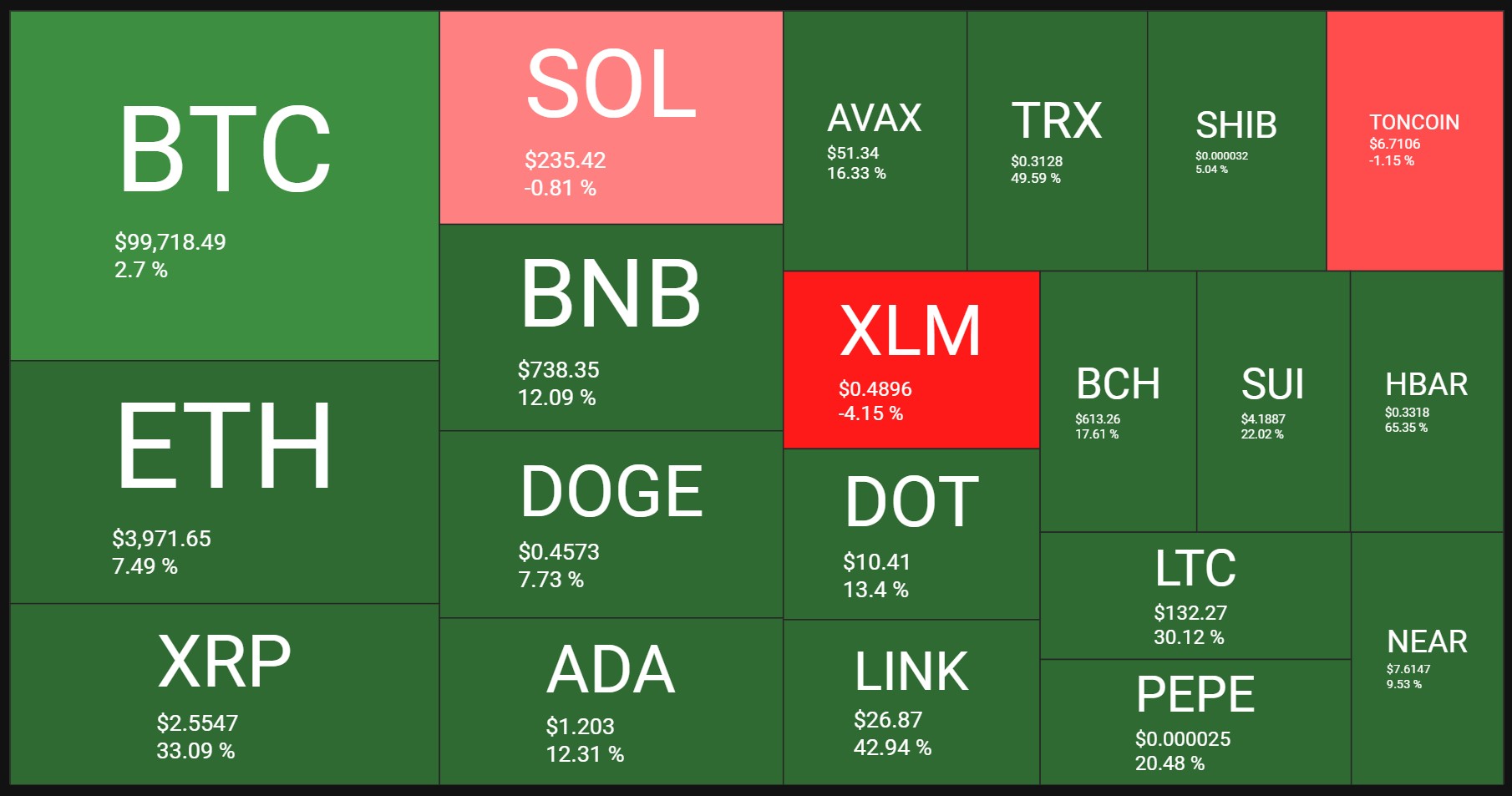

Source: quantifycrypto

Bitcoin soars above $100K as Trump’s return sparks excitement in the crypto market. Individual investors are optimistic, while those betting against the market are retreating. The US earnings outlook is in focus with high stock valuations.

Bitcoin fell below $100,000 after hitting a new all-time high of $103,700. Traders are still waiting for a consistent close above $100,000.

Ethereum has surged till $4,000 for the first time since March 2024, indicating a potential start of the altcoin season. The ETH/BTC trading pair has increased, showing ETH’s strength against Bitcoin. Sustained gains against BTC are crucial for the anticipated altcoin season, where altcoins outperform BTC.

Next Week’s Outlook

Economic Events

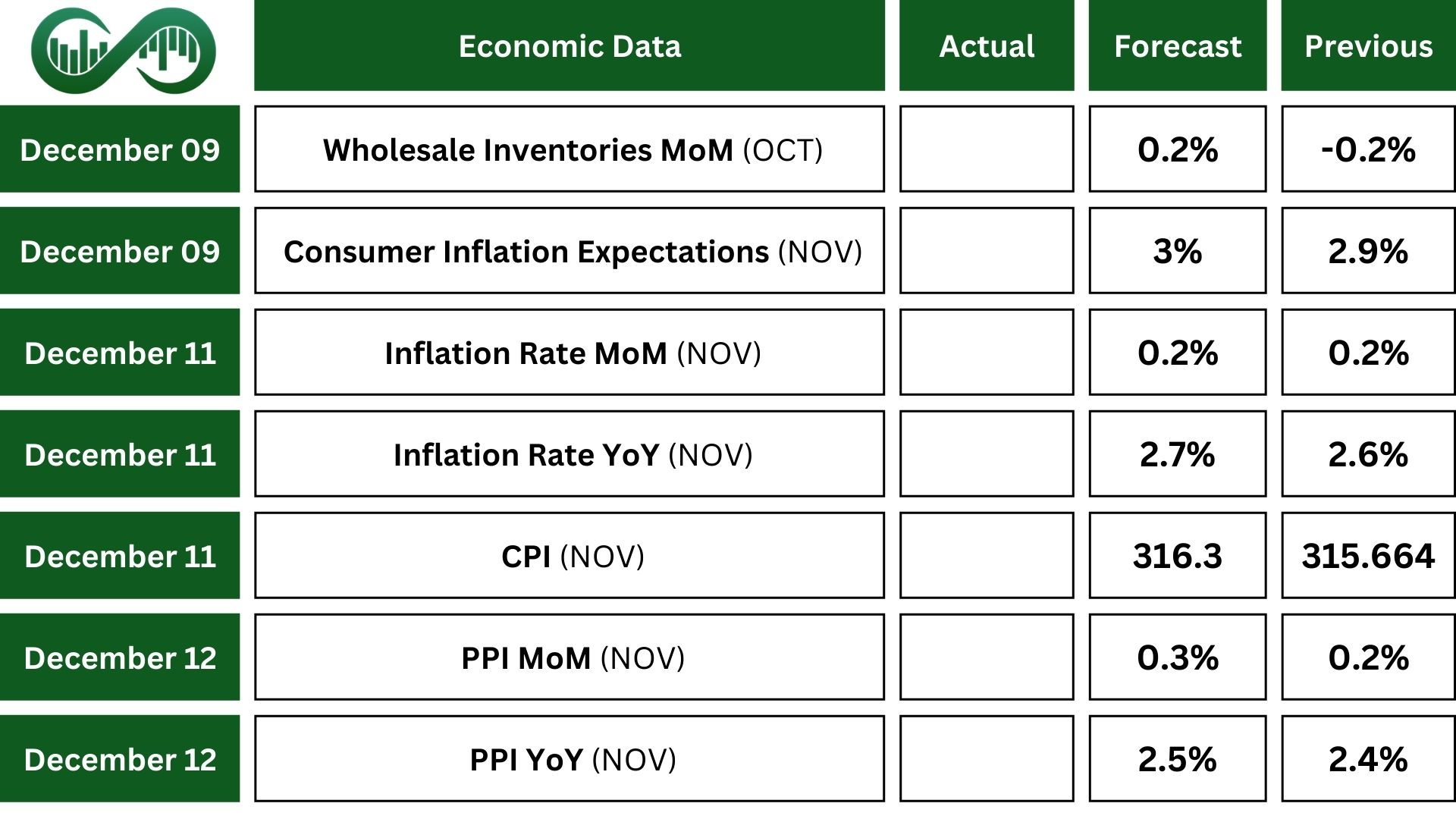

The focus in the US is on the upcoming CPI report. Annual inflation is expected to rise to 2.7%, the highest in four months, up from 2.6% in October.

The focus in the US is on the upcoming CPI report. Annual inflation is expected to rise to 2.7%, the highest in four months, up from 2.6% in October.

However, monthly inflation is projected to stay at 0.2%, and core inflation is likely to remain at 3.3% annually and 0.3% monthly.

Annual producer inflation is forecast to increase to 2.5% from 2.4%, with the monthly rate expected to rise to 0.3% from 0.2%.

Core PPI is predicted to go up to 3.3% annually from 3.1%, while the monthly rate may stay at 0.3%.

Other important releases include data on wholesale inventories, consumer inflation expectations data, the monthly budget statement, and prices for exports and imports.

Earning Events

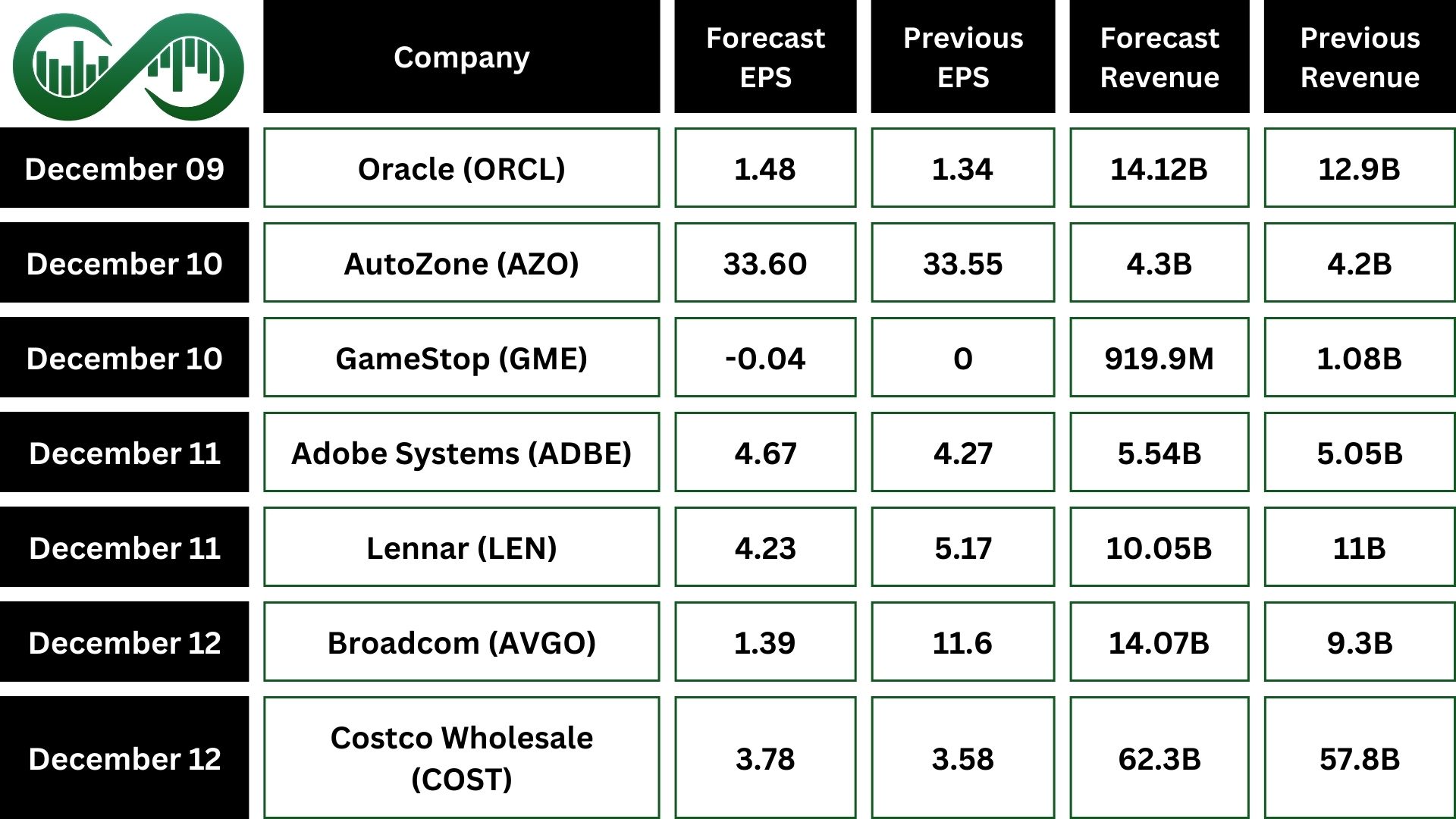

Earnings reports are expected from companies including Oracle (ORCL), Adobe (ADBE), Broadcom (AVGO) and Costco (COST).