Last Week’s Reports

Economic Reports

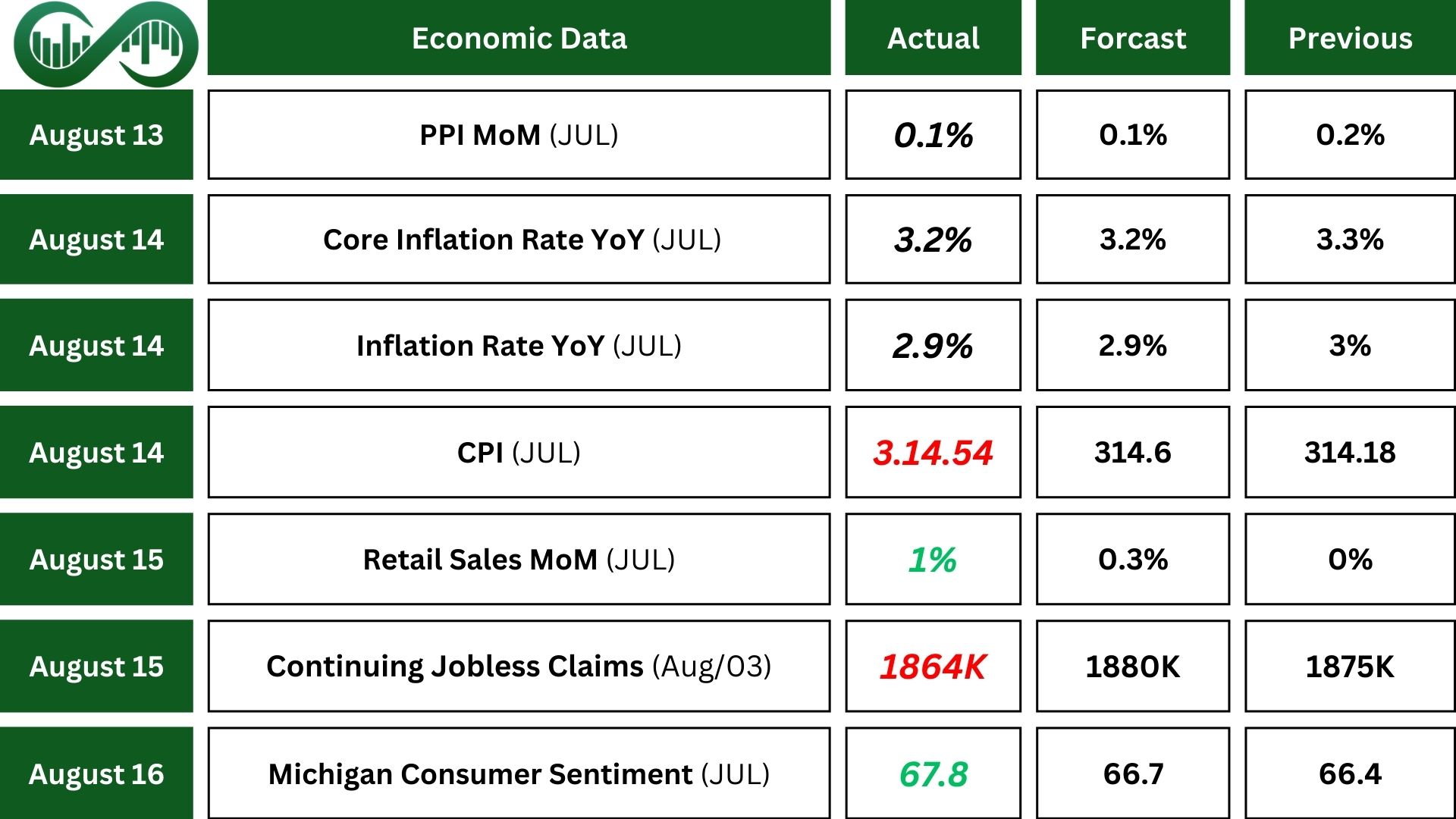

The Producer Price Index (PPI) for July showed a modest 0.1% MoM increase, signaling a slowdown in inflationary pressures. This report has heightened market expectations that the Fed may opt for a more substantial rate cut in its upcoming meeting.

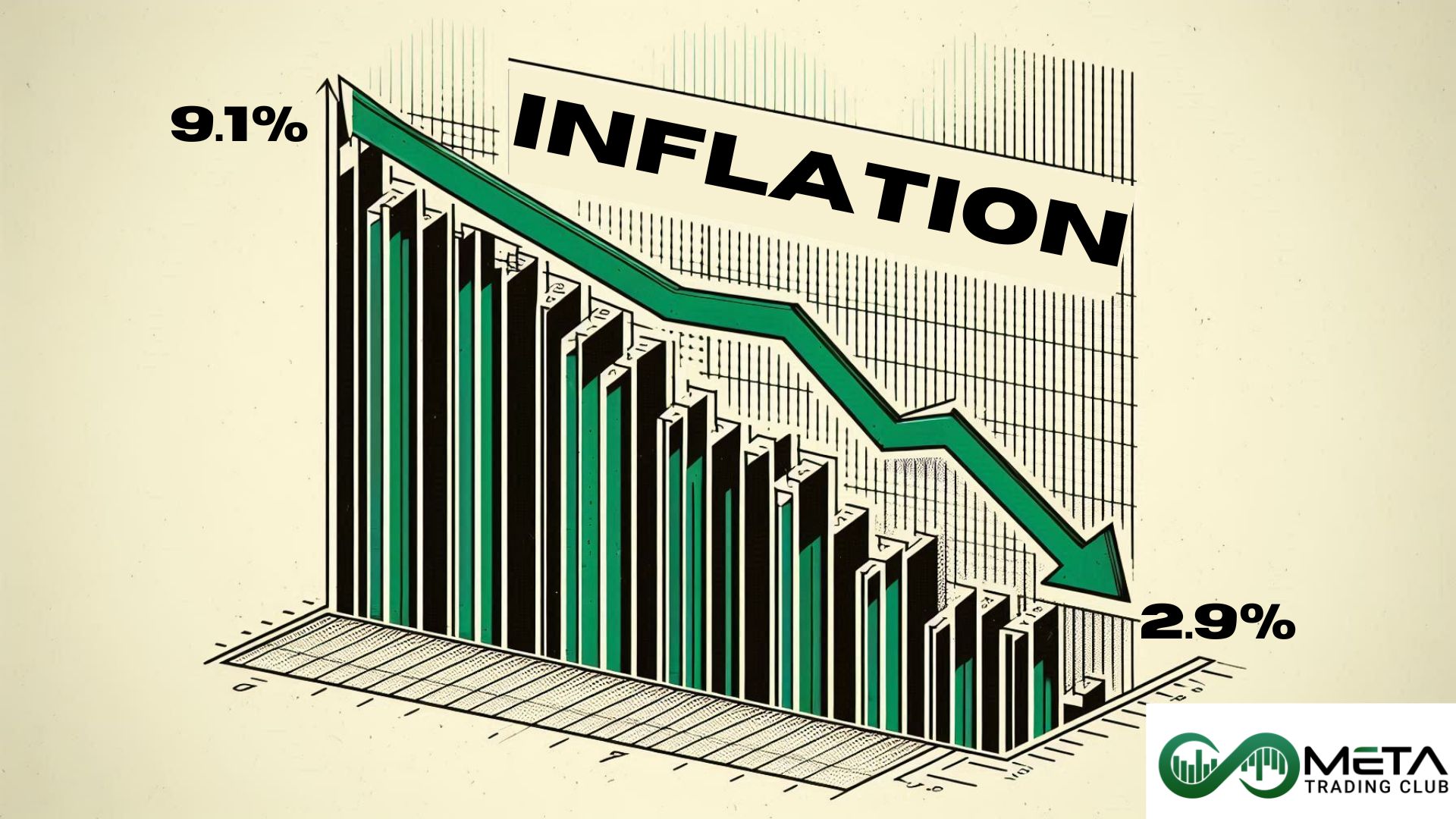

The annual inflation rate in the US slowed for a fourth consecutive month to 2.9% in July (the lowest since March 2021).

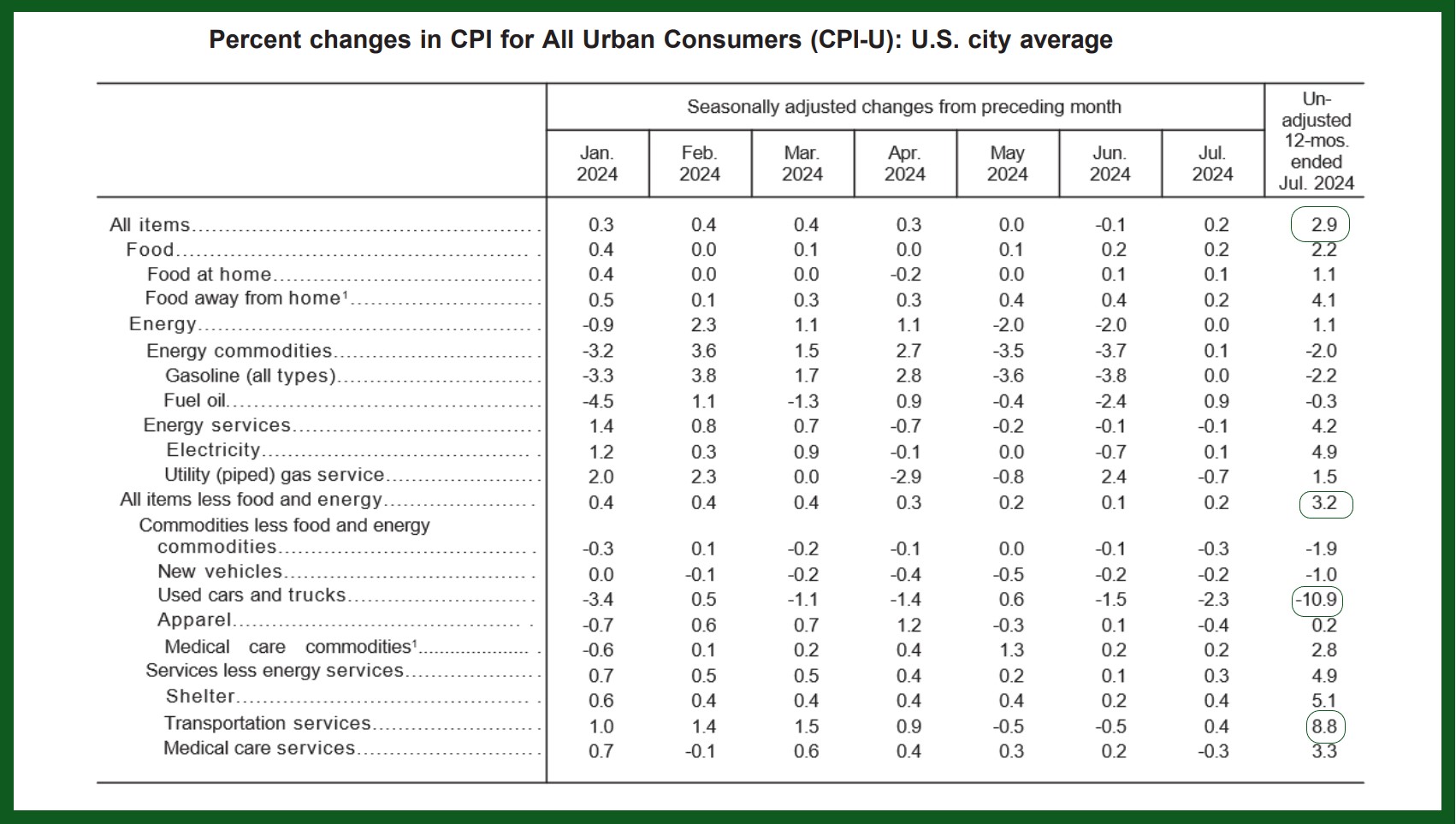

Compared to the previous month, the Consumer Price Index (CPI) increased 0.2%, rebounding from a 0.1% drop in June. However, shelter increased 0.4%, which includes rents (90% of the rise in the CPI is because of that).

Source: U.S. Bureau of Labor Statistics

An uptick in shelter prices in Wednesday’s CPI report is adding to uncertainty over whether the Federal Reserve is likely to cut rates by 25 or 50 basis points at its next meeting in September.

Retail sales in the US soared 1% MoM in July 2024 way better than forecasts of a 0.3% gain. It is the biggest increase since January 2023.

The initial jobless claim in the US fell to 227K. The recent data reflected a slowdown in the US labor market. In the meantime, the continuous jobless claim counts fell to 1,864K against expectations of an increase to a high of 1,880,000.

Building permits in the United States fell by 4% to a seasonally adjusted annual rate of 1.396 million in July (the lowest in four years) and below market estimates of 1.43 million. The report shows the consequences of the high mortgage rate.

Economic expectations strengthened for both personal finances and the five-year outlook (reached its highest reading in four months) consistent with the fact that election developments can influence future expectations but are unlikely to alter current assessments.

Earning Reports

UBS

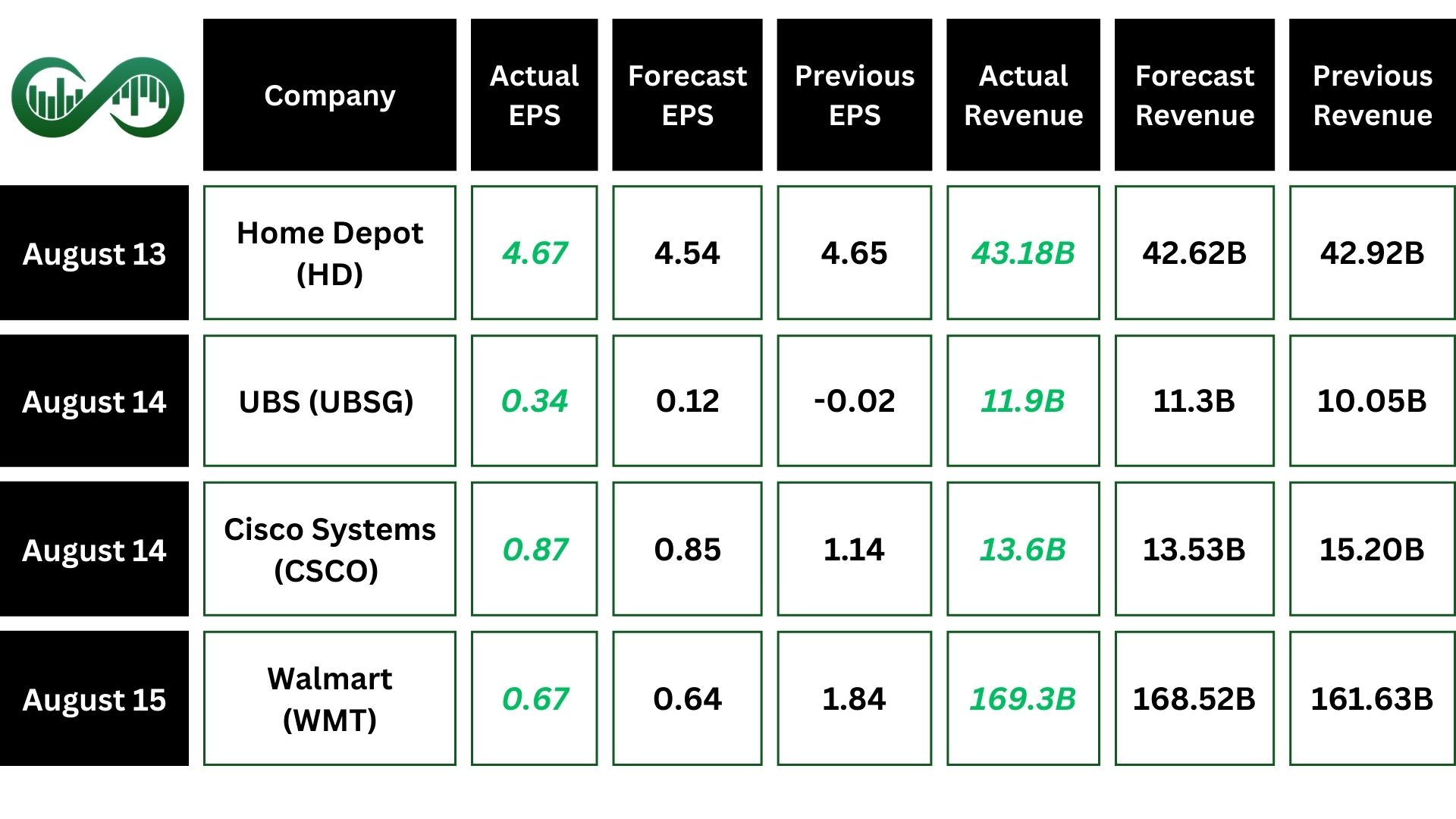

Shares of UBS Group (UBSG) rose during Wednesday’s session following strong second-quarter earnings.

UBS Group reported second-quarter revenue of $11.9 billion, up 25% YoY, beating the estimates. Also, EPS of 34 cents beat the estimate of 12 cents.

Underlying operating profit before tax reached $2.06 billion, significantly higher than $891 million a year ago. Moreover, UBS now anticipates achieving around $7 billion in gross cost savings by the end of 2024.

UBS shares gained 6.5% last week.

In the third quarter of 2024, UBS anticipates integration expenses of approximately $1.1 billion. While the rate of gross cost savings is expected to modestly decline sequentially.

Cisco

Shares of Cisco Systems (CSCO) rose sharply during Thursday’s session following better-than-expected quarterly earnings.

Cisco reported fiscal Q4 revenue of $13.64 billion, beating the consensus estimate of $13.537 billion. The company reported adjusted earnings of 87 cents per share, beating analyst estimates of 85 cents per share.

Cisco plans to cut 7% of its workforce, or over 6,300 jobs, to refocus on cybersecurity, cloud, and AI.

According to Chief Financial Officer Scott Herren, layoffs are not just about strengthening profits. Cisco needs to turn further into cybersecurity, cloud systems and artificial intelligence-related products, so it’s releasing resources to do that, Herren said in an interview.

Cisco shares jumped 8.7% last week.

Walmart

Shares of Walmart (WMT) gained 6.6% on Thursday after the company posted better-than-expected earnings and revenue

Walmart (WMT) reported $169.34 billion in revenue, representing a YoY increase of 4.8%. Also, EPS of $0.67 beat the estimate of $0.65.

Operating income was up $0.6 billion, or 8.5%, and adjusted operating income was up 7.2% YoY on higher gross margins, growth in membership income, and reduced eCommerce losses.

Walmart shares jumped 8% last week.

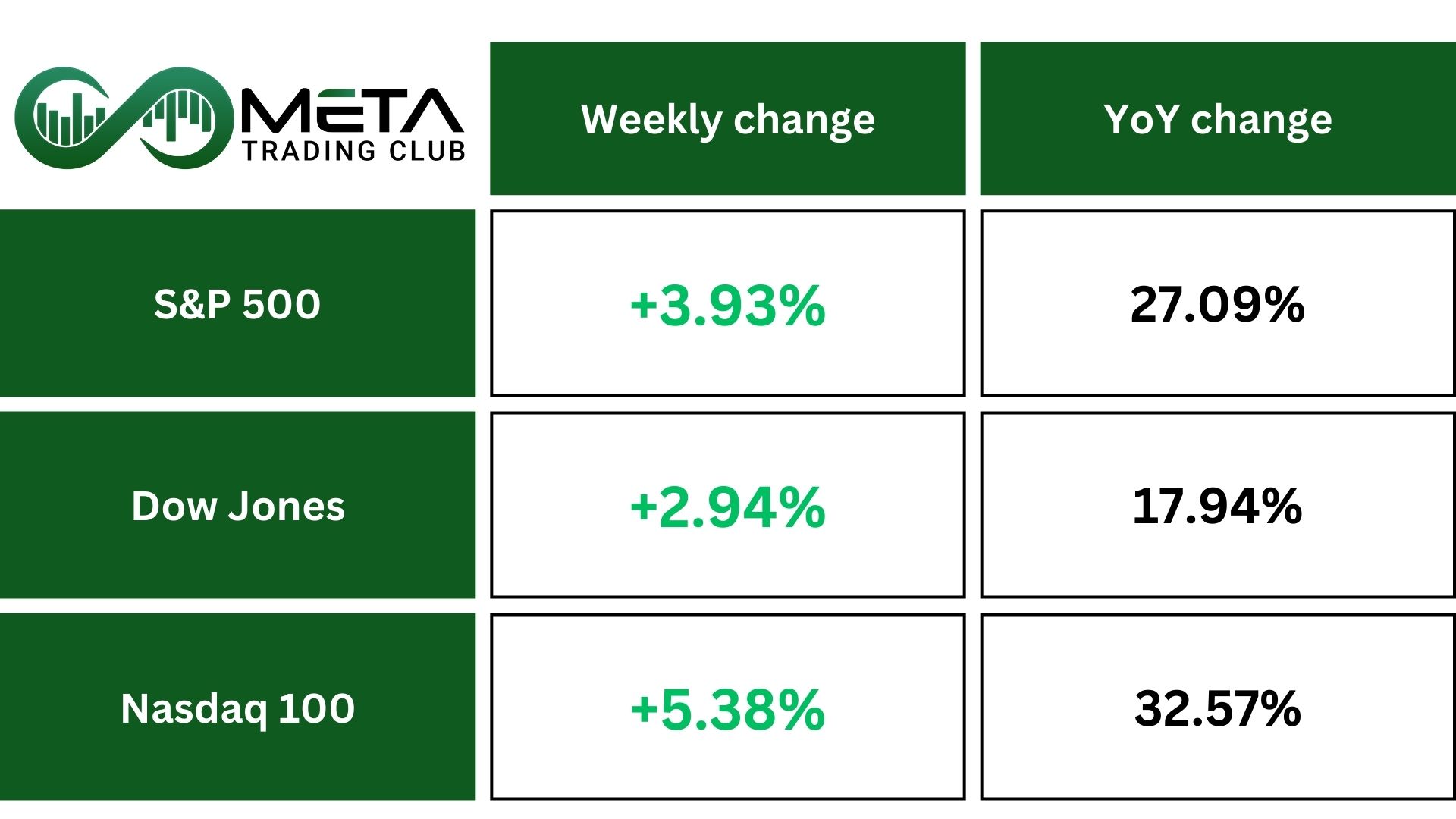

Indices

Indices’ Weekly Performance:

The S&P 500 index posted a sharp rise last week after data showed the American consumer remains in good shape. The S&P 500 added 3.93% on week, outpacing the Dow Jones Industrial Average with its 2.94%, but getting outpaced by the Nasdaq 100, which soared 5.38%. A powerful comeback swept markets but left a few big players out of the picture.

Retail sales, which is a measure of spending at stores, online and in restaurants, pumped at a seasonally adjusted 1% in July from June, overshooting estimates. The data surprised markets where lingering recession fears had clouded the outlook and knocked optimism. Also, Strong Walmart earnings helped improve the sentiment.

From a technical point of view, the S&P 500 index has been rebounding from the Fibonacci retrace support zone and has reached a resistance area.

There is a good possibility in the long-term view for the index to surge till 5,800 after it breaks its all time high 5,670.

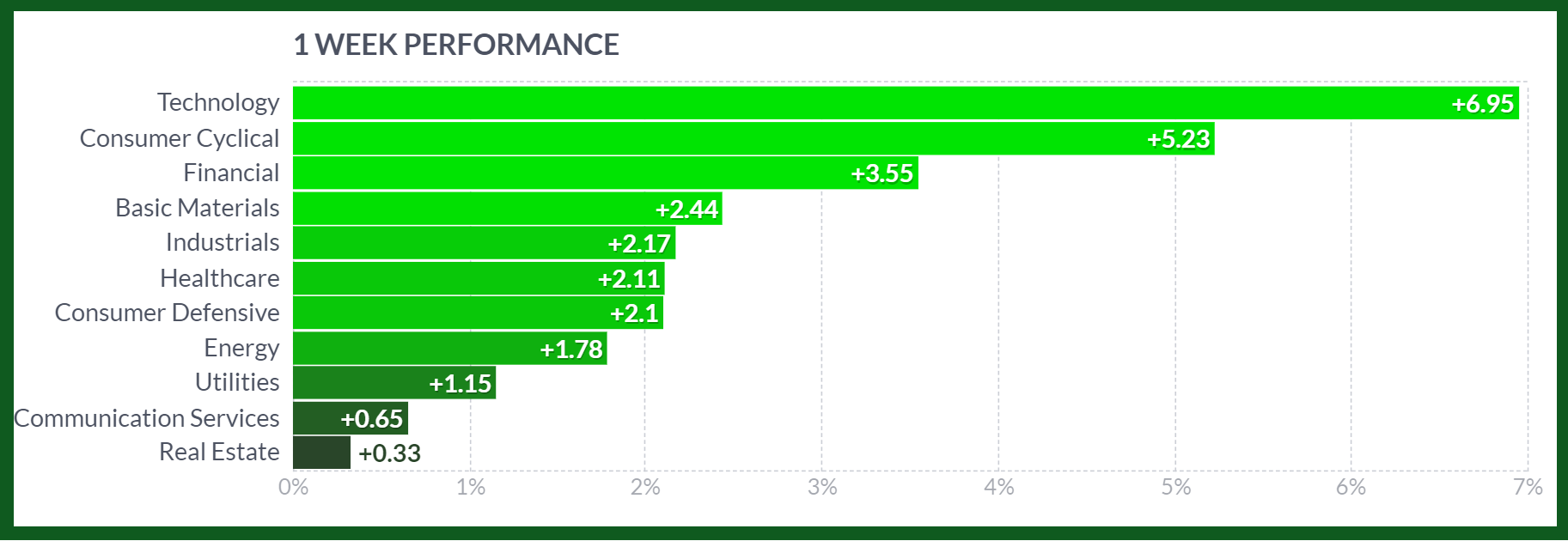

Stocks

Stock Market Sector’s Weekly Performance:

Source: Finviz

Technology was the leading sector with a gain of 7%. Also, communication services and the financial sector followed the gains of the week while real estate dragged the most. Among stocks, Nvidia rose 19%, Amazon gained 6%, Tesla added 8% and Starbucks jumped 26%.

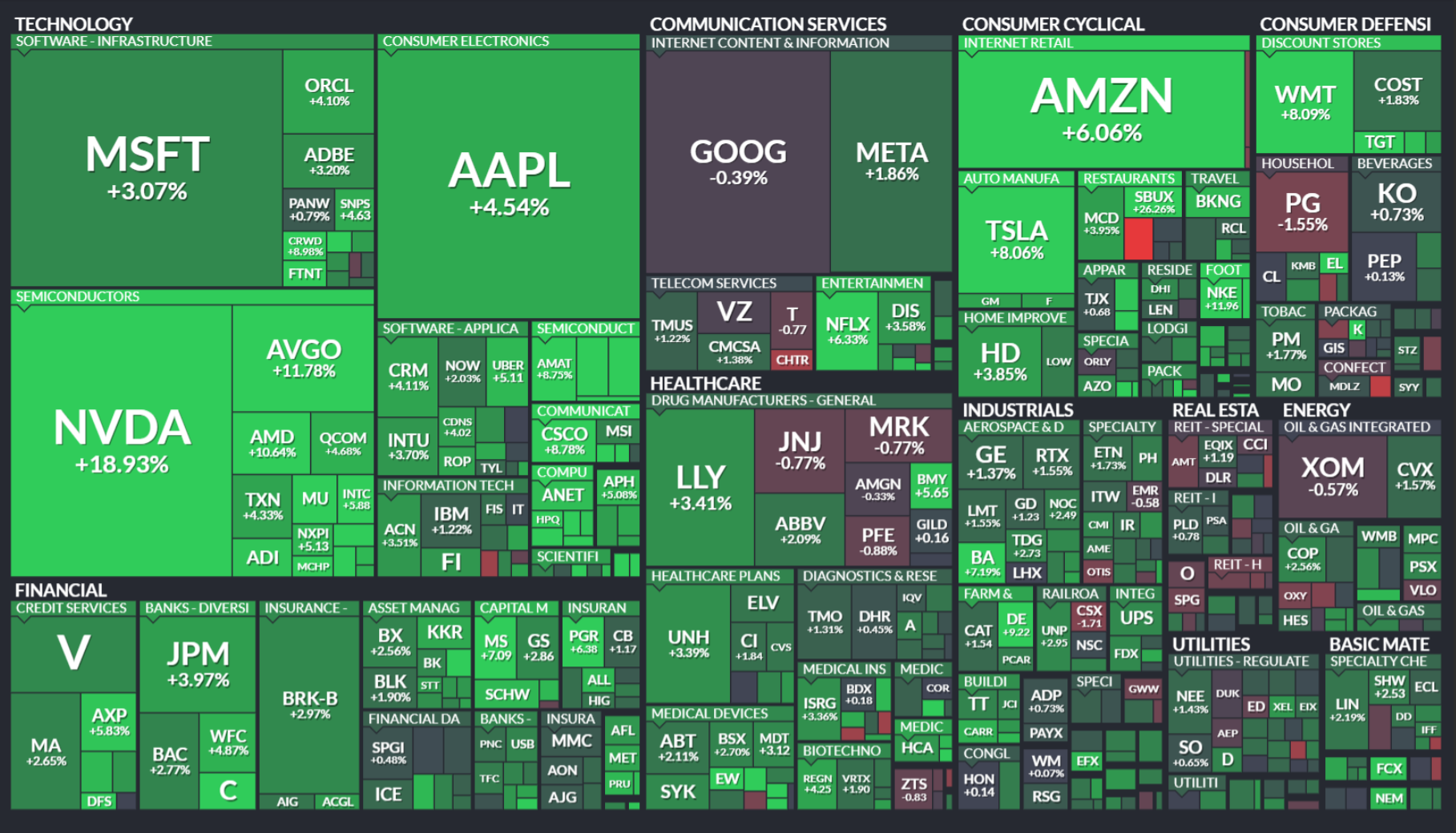

Stock Market Weekly Performance:

Source: Finviz

Source: Finviz

Stocks in the US finished higher on Friday, as the S&P 500 and the Nasdaq added 0.2% each. A busy week of economic data helped the market’s recovery from earlier losses in August. Softer inflation, robust retail sales, and fewer unemployment claims helped calm concerns about potential recession. Additionally, investor sentiment was boosted by signals from Federal Reserve officials suggesting a possible rate cut in September, sustaining the week’s momentum.

Starbucks (SBUX) added a record 25% single-day gain on Tuesday after the company announced a surprise swap in the upper management echelons. Niccol is a highly respected top-level manager, especially after his successful turnaround of Chipotle. He took charge of the struggling burrito maker in 2018 and has since overseen its revival to an 800% share-price increase. The change at the top was met with great enthusiasm, leading to the share-price surge.

Nvidia (NVDA) gained 19% last week. The upcoming earnings release of Nvidia will be of great interest to investors. The company’s earnings report is expected on August 28. The company’s earnings per share (EPS) are projected to be $0.63, reflecting a 133.33% increase from the same quarter last year. At the same time, our most recent estimate is projecting a revenue of $28.24 billion. There is a strong resistance zone in $130-$140.

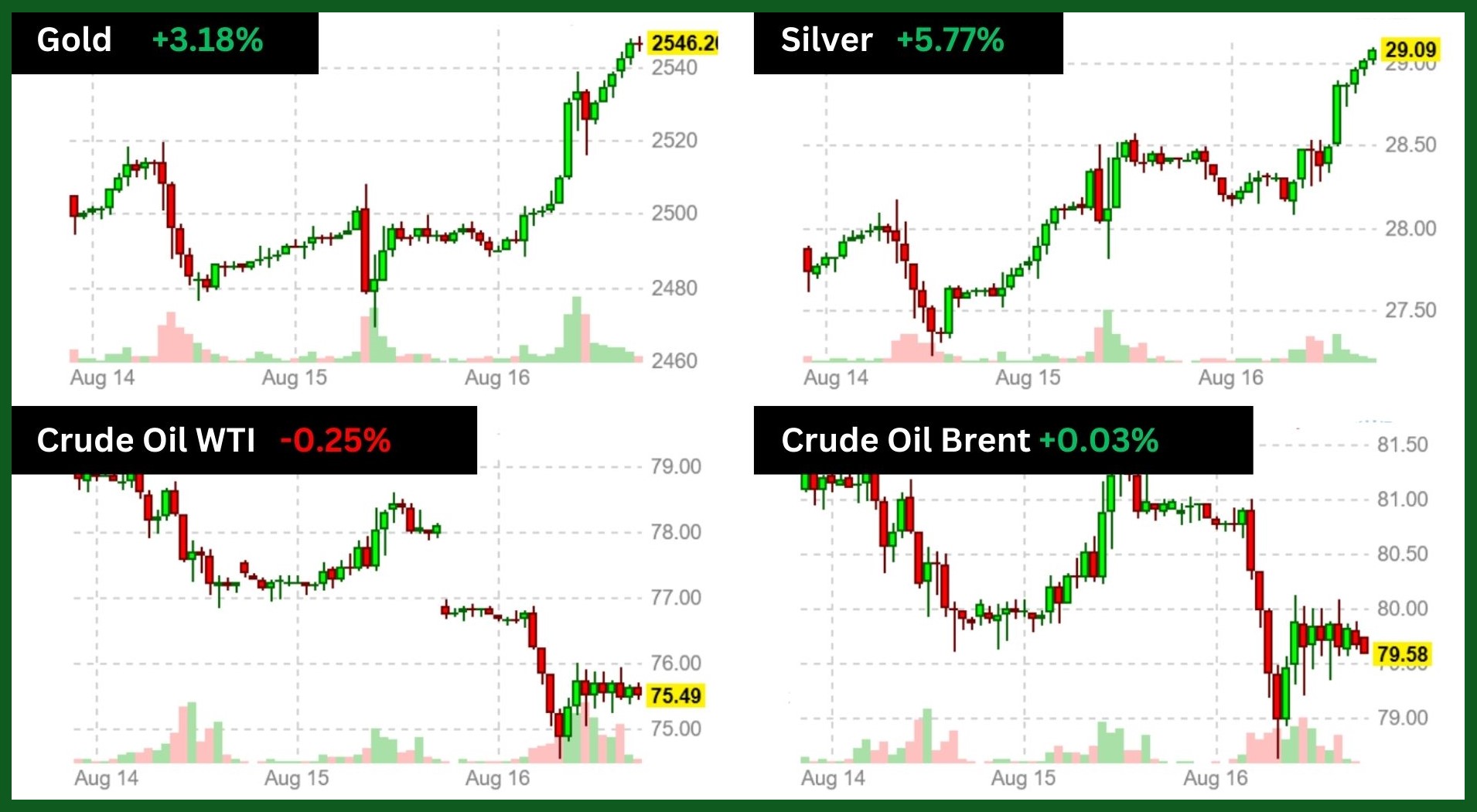

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold reached a new record high on rising hopes for a U.S. interest-rate cut and geopolitical tensions, rapidly reclaiming lost ground after a market crash and selloff in early August. Gold reached as high as $2,509 last week. Meanwhile, spot gold broke and closed above the $2,450 barrier for the first time.

The latest U.S. data also makes a good case for an interest-rate cut by the Federal Reserve next month, though it is likely to be a modest 25 basis point cut rather than the market’s previously hoped for 50 basis points.

Also, buying has firmed up from sources other than financial funds. The U.S. dollar and yields have broken significant support levels and market deleveraging has stopped, ending any gold selling.

Moreover, the U.S. presidential election continues to add to gold’s upward momentum through to the end of the year, while strong central bank demand should offer further support.

The continued central bank demand and sovereign buying, alongside Chinese demand, are likely either at or very close to exhausting the free-floating inventory of tradable gold.

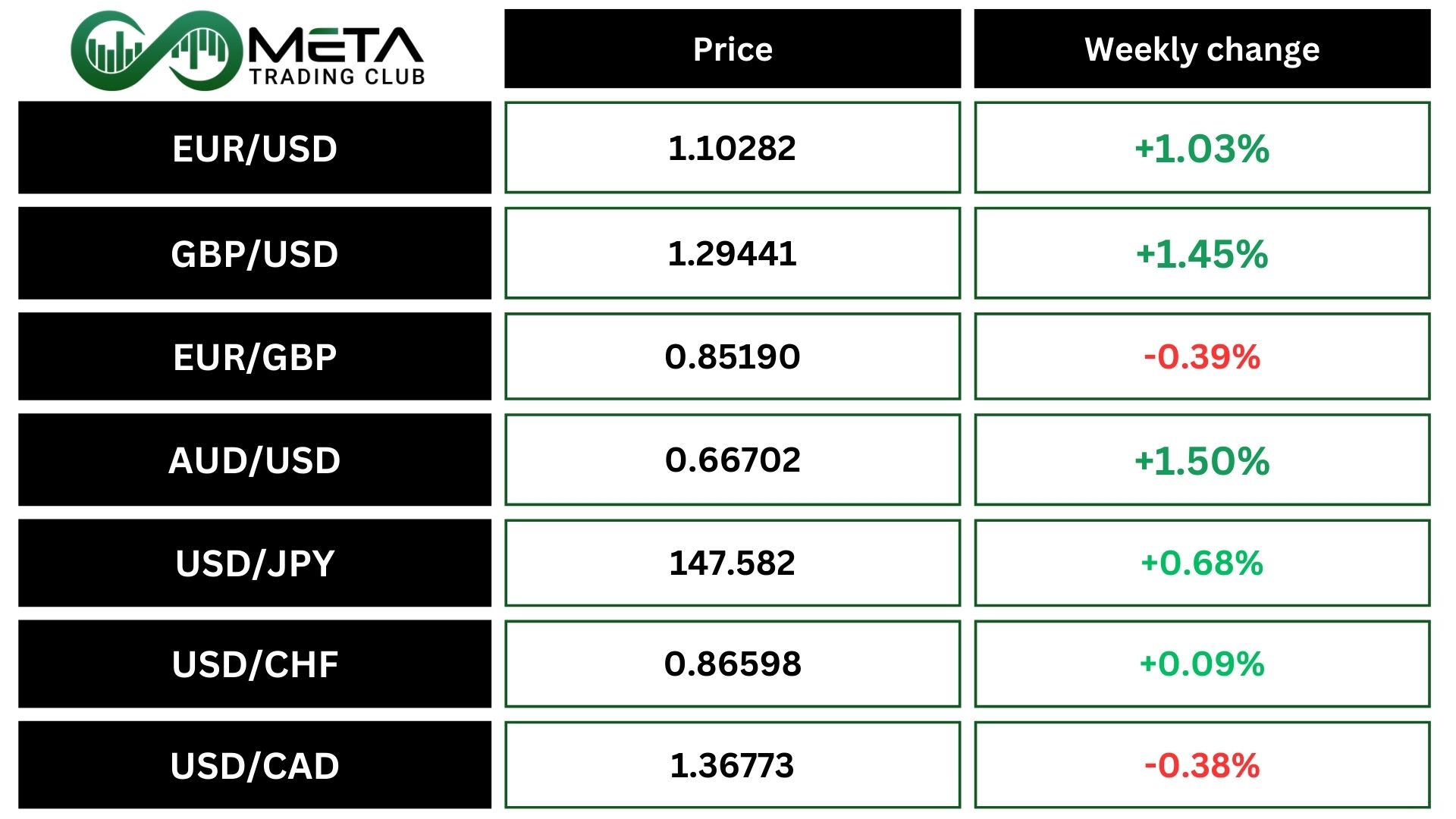

Forex

Weekly Performance of Major Foreign Exchange Pairs:

Sterling (GBPUSD) rose to $1.2941 after data showed British retail sales edged up in July, boosted in part by extra spending during the men’s Euros soccer championship after an unusually cool and wet June had kept shoppers away. The pound was on track for a 1.2% weekly rise, its best performance in more than a month.

The EUR/USD pair jumped to a fresh high of the year after positive US inflation data spurred a mild selloff in the US dollar. The euro advanced to $1.1050, breaking beyond its January 2 high to notch the milestone.

The consumer price index for July, or CPI, showed price pressures dived under 3% for the first time in three years. Traders were excited to celebrate lowering inflation, which came in below the 3% rate in June, and dumped the US dollar which weakens if inflation is moving to the downside. This dynamic suggests that the Federal Reserve may gain the confidence to cut interest rates.

The dollar index (DXY), which measures the greenback against six other major currencies, fell 0.85% to 102.40 last week. The U.S. dollar has broken significant support levels and closed on a very important support. If the support breaks, further decline is predicted.

Traders are now looking to Fed Chairman Jerome Powell’s upcoming Jackson Hole speech, but Weller does not expect any pre-commitment to either a 25 bps or 50 bps cut next month.

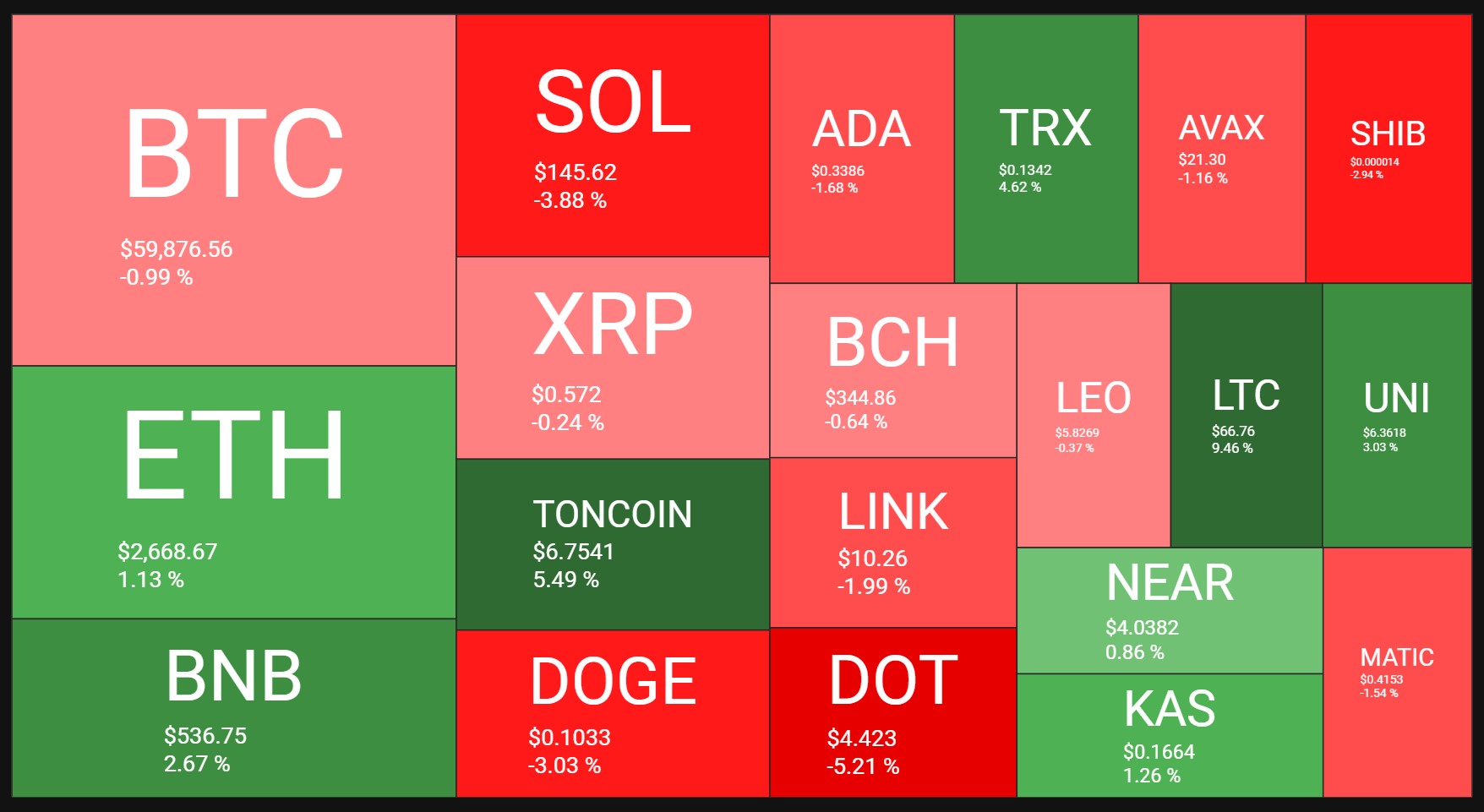

Crypto

Crypto Market Weekly Performance:

Source: quantifycrypto

Bitcoin’s price is consolidating in a tight range as market participants are uncertain about the future direction of the price.

On the daily chart, the price has recently rebounded from the $50K area, following the significant drop below the 200-day moving average. Currently, the market is consolidating below the moving average, which is located around the $63K, failing to climb back above.

Meanwhile, the $56K support level currently holds the market, preventing the price from dropping further. Therefore, a breakout from either this level or the 200-day moving average could determine the short-term price action of BTC and the crypto market.

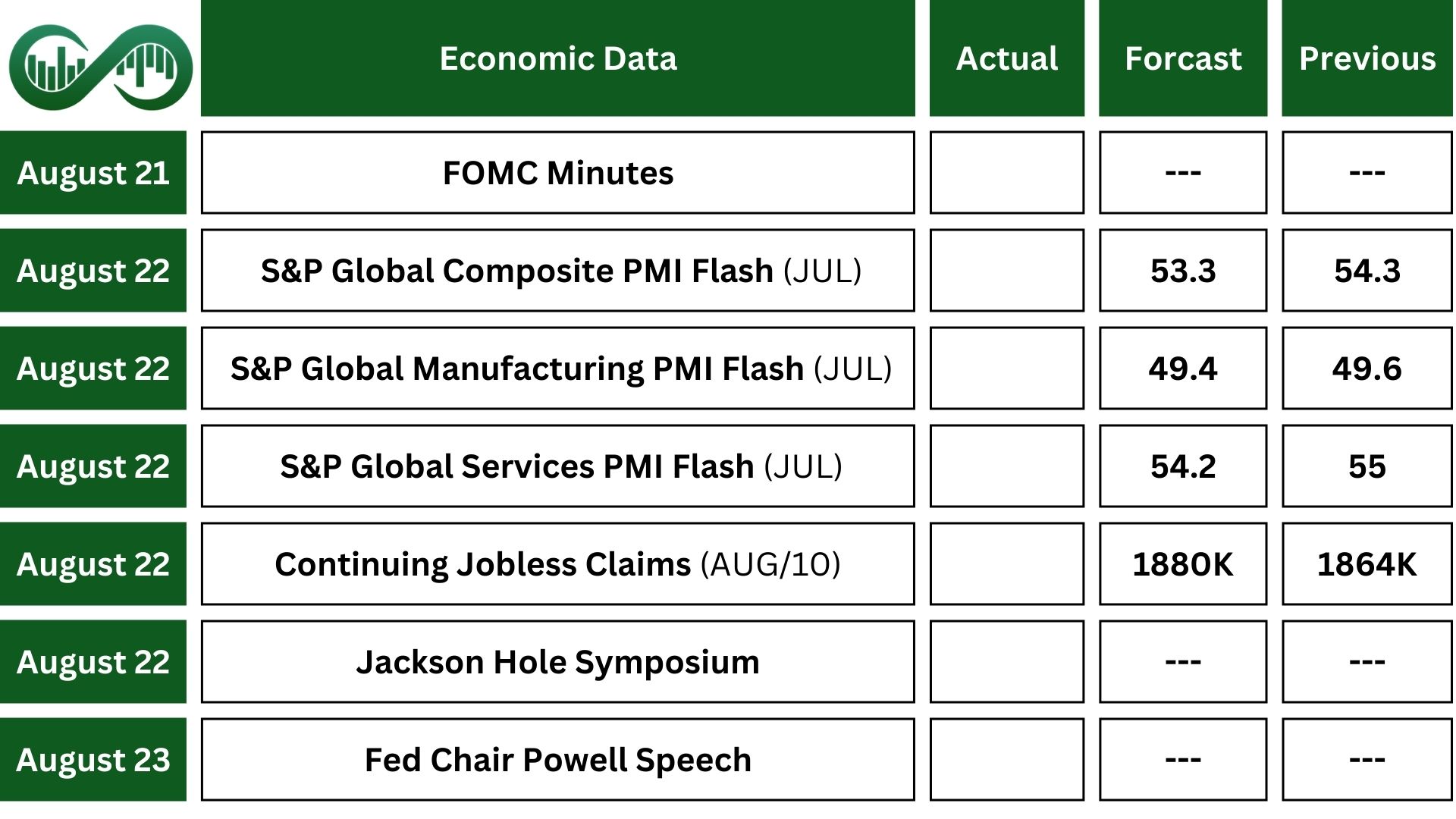

Next Week’s Outlook

Economic Events

An uptick in shelter prices report is adding to uncertainty over whether the Federal Reserve is likely to cut rates by 25 or 50 basis points at its next meeting in September. For new clues on the thinking of Fed policymakers, traders will be closely watching next week’s economic symposium in Jackson Hole.

Fed Chair Jerome Powell is expected to use the Jackson Hole symposium to more strongly signal that a September rate cut is on the way.

The key data releases to keep an eye on include S&P composite, manufacturing and services PMI.

Earning Events

On the corporate side, there is no significant earnings upcoming this week.