What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

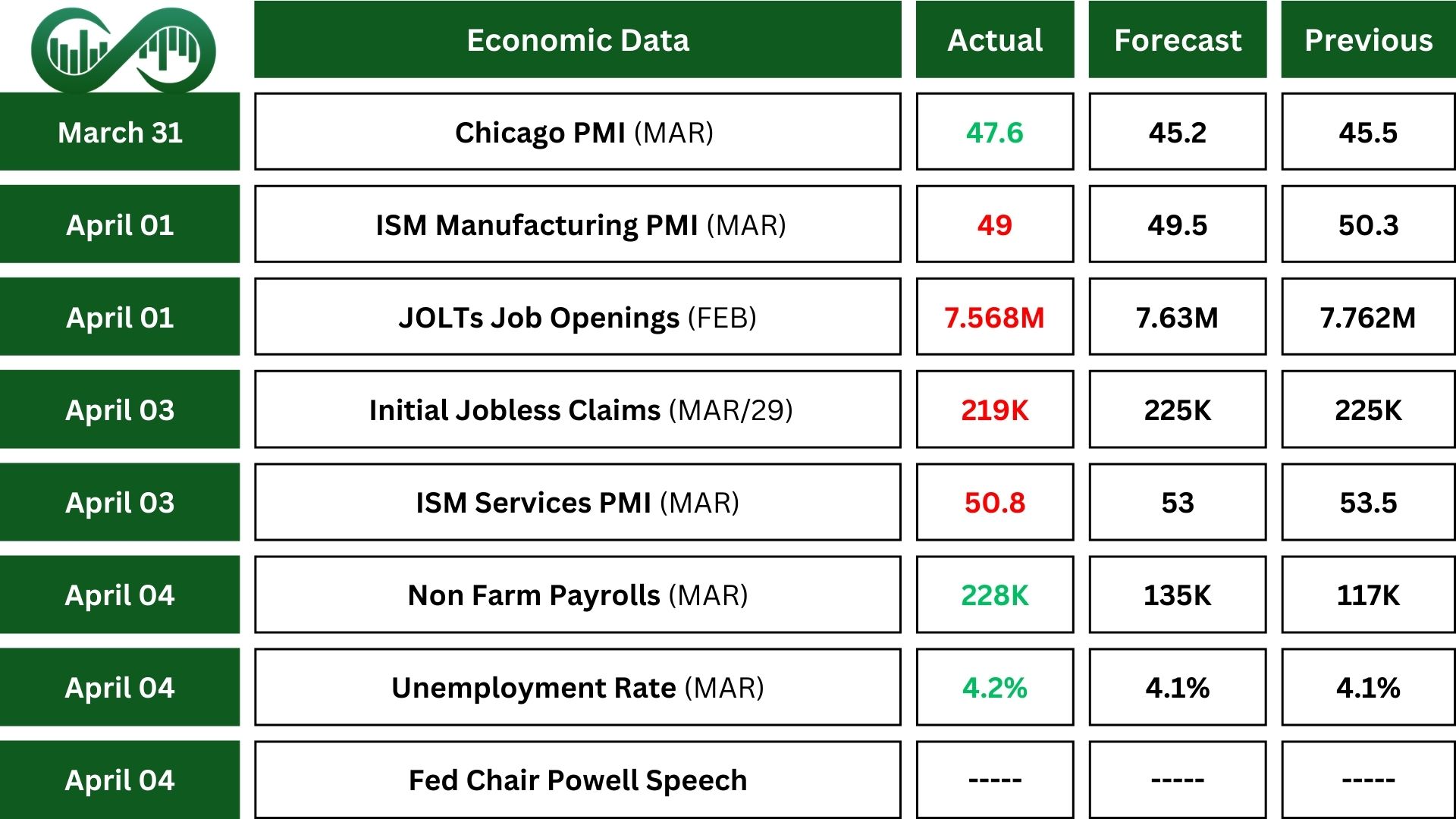

US manufacturing started 2025 on a strong note but faced struggles in March. Confidence plummeted, hiring paused, and tariffs drove up costs while slowing supply chains. Material shortages, worsened by China’s restrictions, increased prices and limited supplies. Retaliatory tariffs hurt sales in Canada and Europe, while some sectors saw weaker demand. The Manufacturing PMI drop in March signals a shrinking manufacturing sector and economic slowdown. Despite challenges, some manufacturers remain hopeful that tariffs will boost domestic demand in the future.

The February JOLTs report shows a steady labor market overall. Job openings remained stable but declined year-over-year. Hiring and separations, including quits and layoffs, showed little change. The report highlights consistent labor activity with sector-specific challenges.

The services PMI showed mixed results. The S&P Global report pointed to growth supported by customer demand and favorable conditions. In contrast, the ISM report highlighted issues like slower growth, fewer jobs, and higher costs from tariffs. These reports reveal a delicate balance of progress and challenges reflecting economic uncertainty.

Nonfarm payroll employment increased by 228K in March, higher than the average gain over the past year. The unemployment rate edged up slightly to 4.2. The rate has stayed between 4% and 4.2% since May 2024. While job growth is strong, concerns about trade tensions may overshadow these positive trends.

Federal Reserve Chair Jerome Powell discussed economic challenges, including tariffs, inflation, and policy uncertainties, at a recent conference. He highlighted slower but steady growth, stable unemployment at 4.2%, and inflation concerns due to tariffs. Also, Powell emphasized the need for clarity on trade policies before cutting rates.

Investors grew uneasy after Powell’s cautious stance on rate cuts and the economic uncertainty from new tariffs. Optimism faded, leading to market volatility and increased fears of a potential recession.

Tariff Report

On April 2, 2025, President Donald Trump announced reciprocal tariffs, calling it “Liberation Day.” These tariffs aim to address trade imbalances with a baseline 10% tariff on all imports and higher rates for nations contributing significantly to the U.S. trade deficit, such as China (34%) and the EU (20%). While Russia is excluded due to sanctions, Ukraine and other former Soviet republics face a 10% tariff.

While intended to boost domestic production, the announcement triggered a 10% drop in the S&P 500, with investors humorously referring to “Liberation Day” as “Liquidation Day.” Concerns over higher costs for global supply chain-dependent industries and trade tensions fueled market volatility. Although some sectors may gain, others risk losing competitiveness. Long-term effects remain uncertain, potentially reshaping global trade relationships and economic growth.

Indices

Indices’ Weekly Performance:

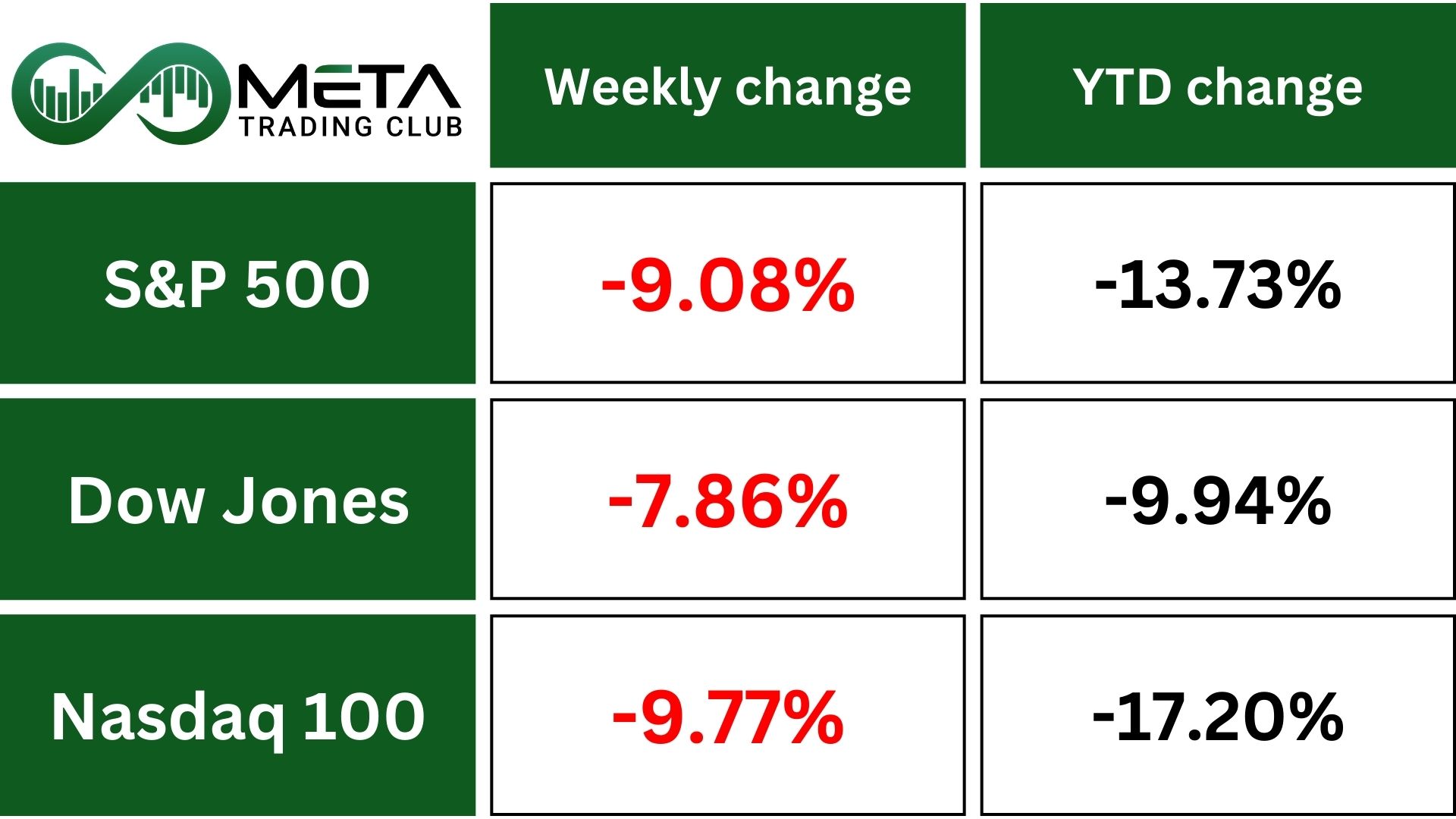

Wall Street plunged on Thursday Friday, with the Nasdaq officially entering a bear market and the Dow slipping into a correction. The escalating global trade war triggered the biggest losses since the pandemic.

Over two days, the Dow dropped 9.3%, the S&P 500 fell 10.5%, and the Nasdaq tumbled 11.4%, marking the steepest two-day decline since the early COVID-19 panic during President Trump’s first term.

Global governments reacted to President Trump’s tariff announcement, worsening investor sentiment and raising recession fears. JP Morgan increased its recession forecast to 60% by year-end. China announced 34% tariffs on U.S. goods starting April 10, while leaders from Britain, Australia, and Italy discussed responses.

The S&P 500 has fallen 13.73% since the beginning of 2025, while the Dow dropped 10% and the Nasdaq plunged 17.2%, reflecting the escalating trade war’s impact.

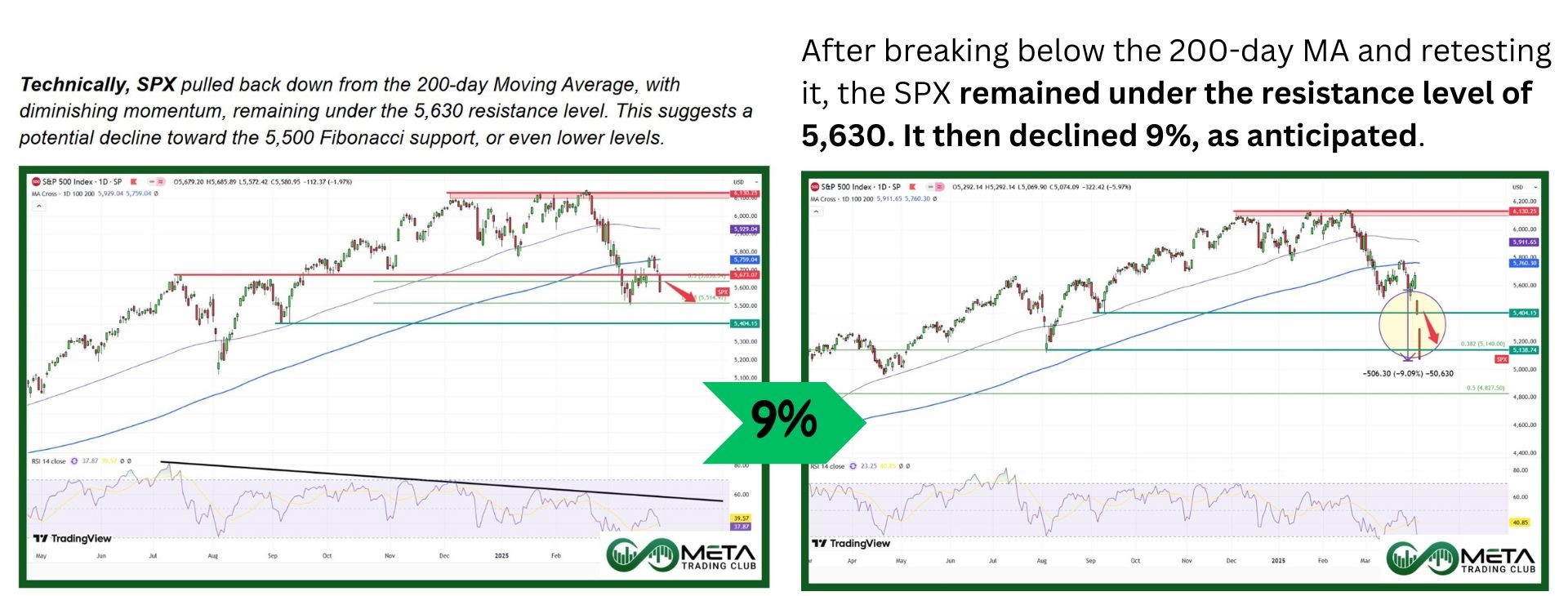

Technically, The SPX has reached a key support level at 5130 and is in the oversold zone on the weekly RSI. If trade war uncertainties persist this week, the index might drop further to support levels at 5000 or 4800. However, if it manages to hold at 5130, it could rebound to higher levels.

Stocks

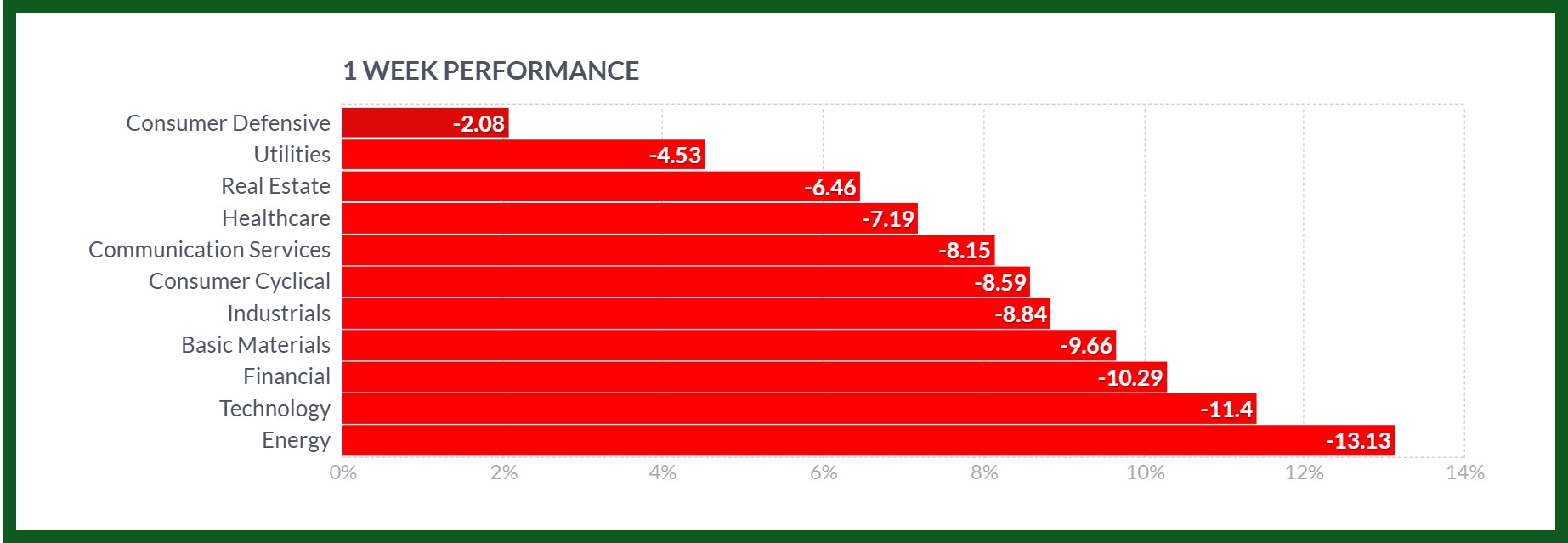

Sector’s Weekly Performance:

Source: Finviz

All sectors of the S&P 500 declined last week. Energy saw the biggest drop, falling 13%, followed by Technology (-11%) and Financials (-10%), and Industrials.

- In the energy sector, APA‘s stock plunged 27% after analysts lowered their price targets, though they maintained positive ratings.

- For technology, Micron Technology dropped 26%, as investors worried about pressure on U.S. chip companies, like Micron and others, to expand domestic production or risk losing government funding.

- In financials, KKR fell 19% after leading a $500 million investment in ReliaQuest, aimed at expanding its AI-powered cybersecurity platform and international growth, raising concerns among investors.

The market’s overall decline of 9% last week was reflected in the widespread losses across sectors. Defensive sectors like Consumer Defensive and Utilities fared better, while cyclical and growth-oriented sectors such as Technology and Energy faced the steepest declines.

Stock Market Weekly Performance:

Source: Finviz

Top Performers

Despite a challenging week where indexes fell sharply, several stocks managed to outperform the market and deliver impressive gains. Here’s last week’s top-performing stocks:

- Ross Stores (ROST): Rose 3.9% as Citigroup has upgraded Ross Stores from Neutral to Buy.

- TJX Companies (TJX): Increased 3.3% after recently increasing its dividend despite market volatility.

- McKesson (MCK): Climbed 2.2% benefiting from its U.S.-focused operations as tariff impacts remain minimal for the drug distribution sectors.

- American Tower (AMT): Gained 2.1% as property investors believe that, during a trade war, American consumers will prioritize rent and cell phone bill payments over other expenses.

- UnitedHealth (UNH): Rose 1.7% as this drug distributor and insurer primarily focused on U.S. markets so the impact of tariffs on it is minimal.

- MicroStrategy (MSTR): Gained 1.4% as Bitcoin remained stable despite tariff uncertainties.

Action Point

GOOG has declined after breaking its long-term uptrend line and is now at a significant support zone between $146 and $149. Should bearish confirmation persist, the stock might drop to the Fibonacci support level of $131. Conversely, if the current support level holds, it could trigger a rebound from this 50% Fibonacci retracement level.

NVDA dropped to a static support level at $91. If trade war uncertainties continue, the stock might break this support fall further to a lower support at $78. However, if it maintains the $91 level, it could potentially rebound and rise again.

META has broken its uptrend line, dropping to Fibonacci support at $490. If trade war tensions intensify and the price breaks this support, it could decline further to $450. However, if the $490 support level holds, the price may rebound from this point.

Commodity

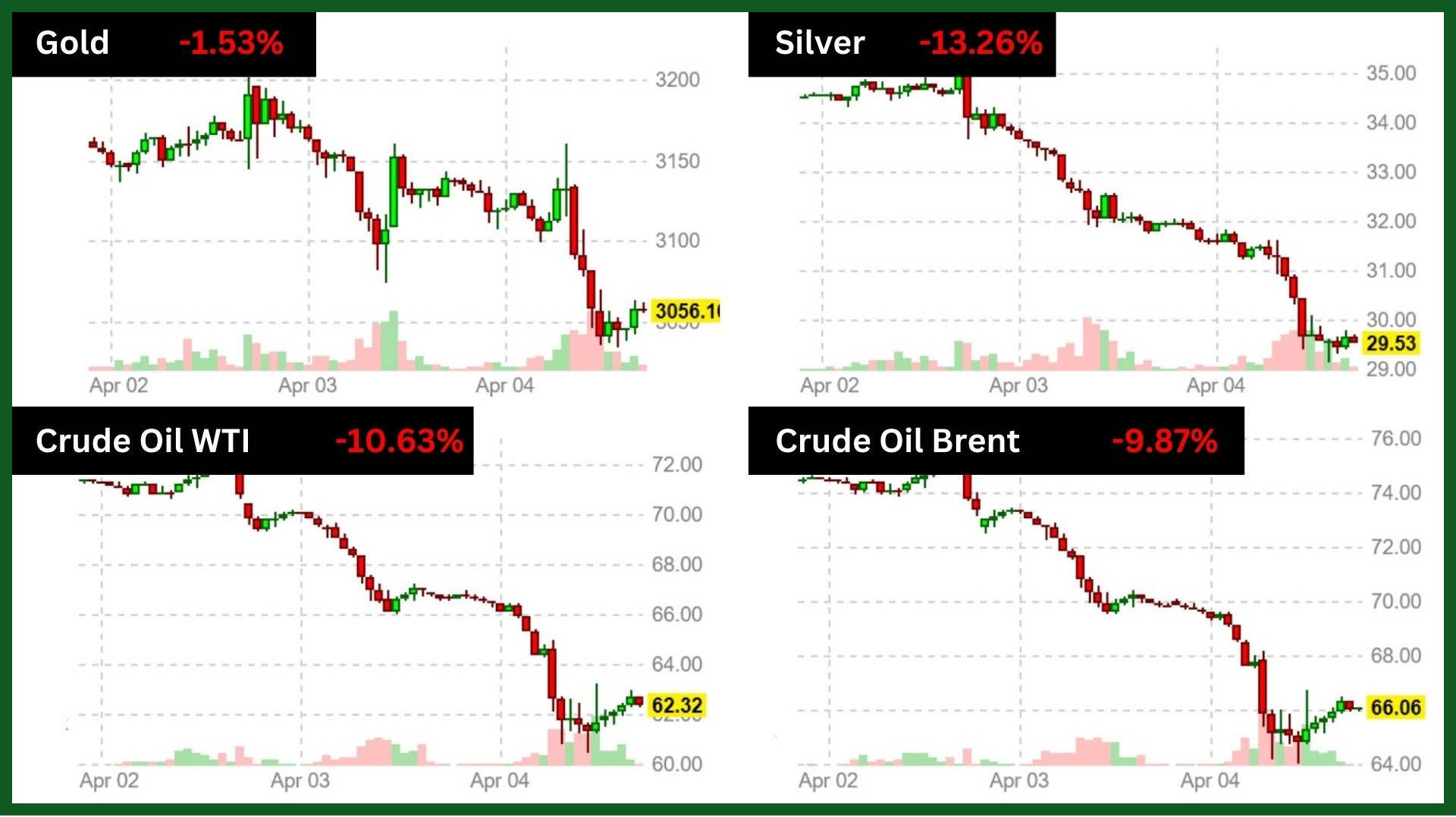

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold (XAUUSD) prices saw a pullback after reaching a record high of $3,200 earlier in the week. This correction is attributed to market volatility sparked by the U.S. President Trump’s tariff agenda and the worst stock sell-off since the Covid-19 pandemic.

Despite profit-taking and technical adjustments, gold remains a safe-haven asset with demand from central banks and ETFs expected to support prices. Persistent trade tensions, inflation worries, and a weakening U.S. dollar may limit the downturn, ensuring gold’s long-term stability and appeal.

Technically, Gold pulled back after hitting a record high of $3,200, finding Fibonacci support at $3,017. If the decline persists, prices could reach lower support at $2,930. However, the combination of an uptrend’s dynamic support and Fibonacci support might trigger a rebound as market uncertainties grow.

Crude oil prices hit a 4-year low, with both major benchmarks dropping nearly 11% in their worst weekly decline since 2023.

While crude prices fell sharply, U.S. gasoline prices declined by about 8%. New tariffs are intensifying a trade war, weakening the global economy and refined product consumption.

The refining sector, already oversupplied, depends on demand growth for margin recovery. With much lower demand growth expected in 2025 and 2026, tariffs may not only stall refining margin recovery but could push margins back to 2021 levels.

Technically, WTI has reached a strong support zone not seen in about four years. If this support level is broken, oil prices could drop significantly in the long term. However, if the support holds, there is potential for a rebound from this level.

Forex

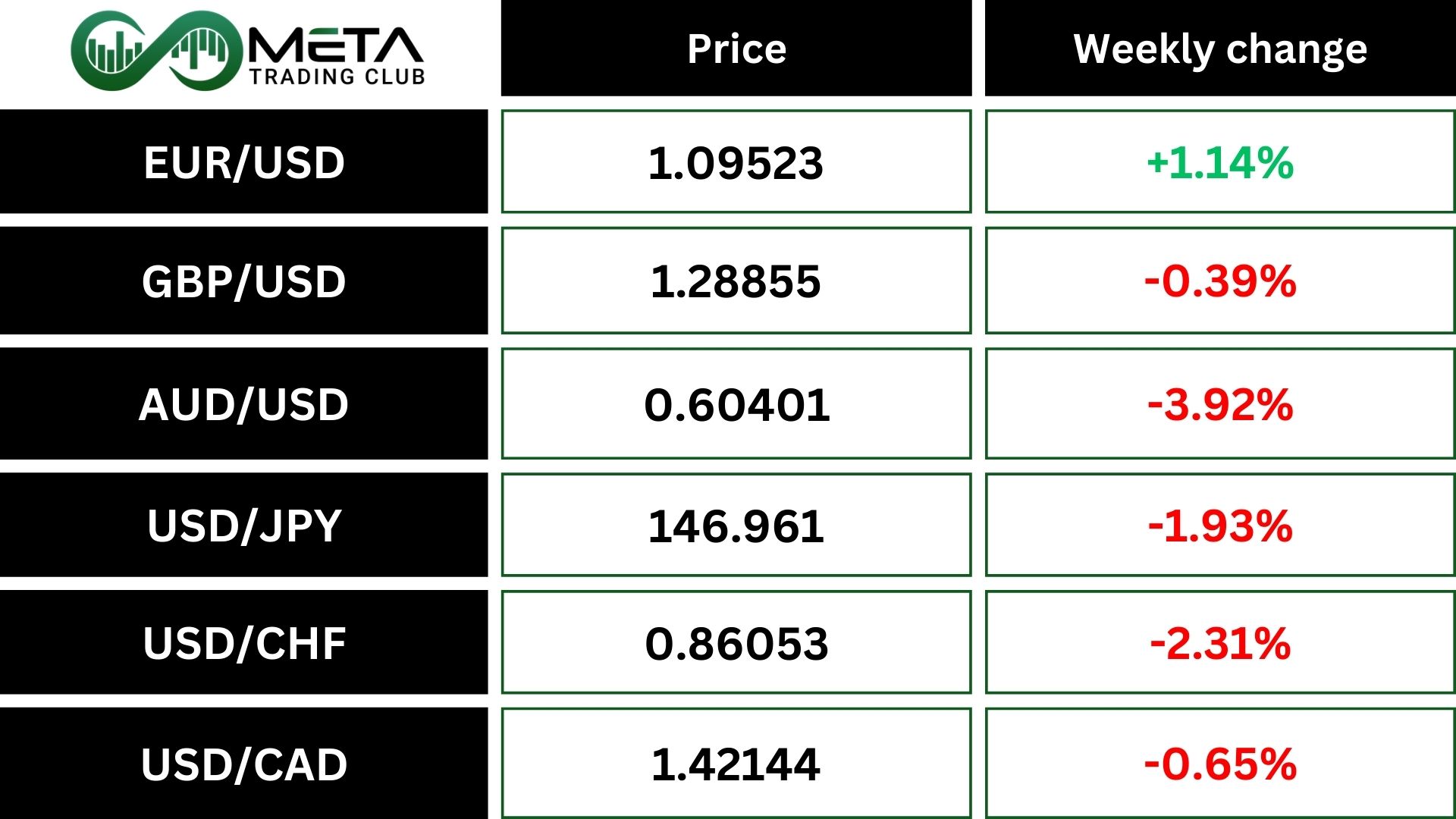

Weekly Performance of Major Foreign Exchange Pairs:

Trump’s tariffs have significantly impacted the forex market.

DXY: the U.S. dollar (greenback) dropping to a six-month low against a basket of six major currencies.

GBP/USD:The British pound dropped below $1.29 because of concerns over President Trump’s tariffs. Even though the UK got a lower 10% tariff, there’s fear that extra tariffs on countries like China could hurt UK exports. Officials warned this trade policy might shrink the economy and strain government finances.

USD/JPY: The pair dropped 2% last week, after President Trump revealed a harsher-than-expected tariff plan. Fears of slower growth caused the dollar to weaken, while the yen gained favor. This temporary boost might encourage the Bank of Japan to take bolder steps on interest rate hikes to manage inflation without harming the economy.

Crypto

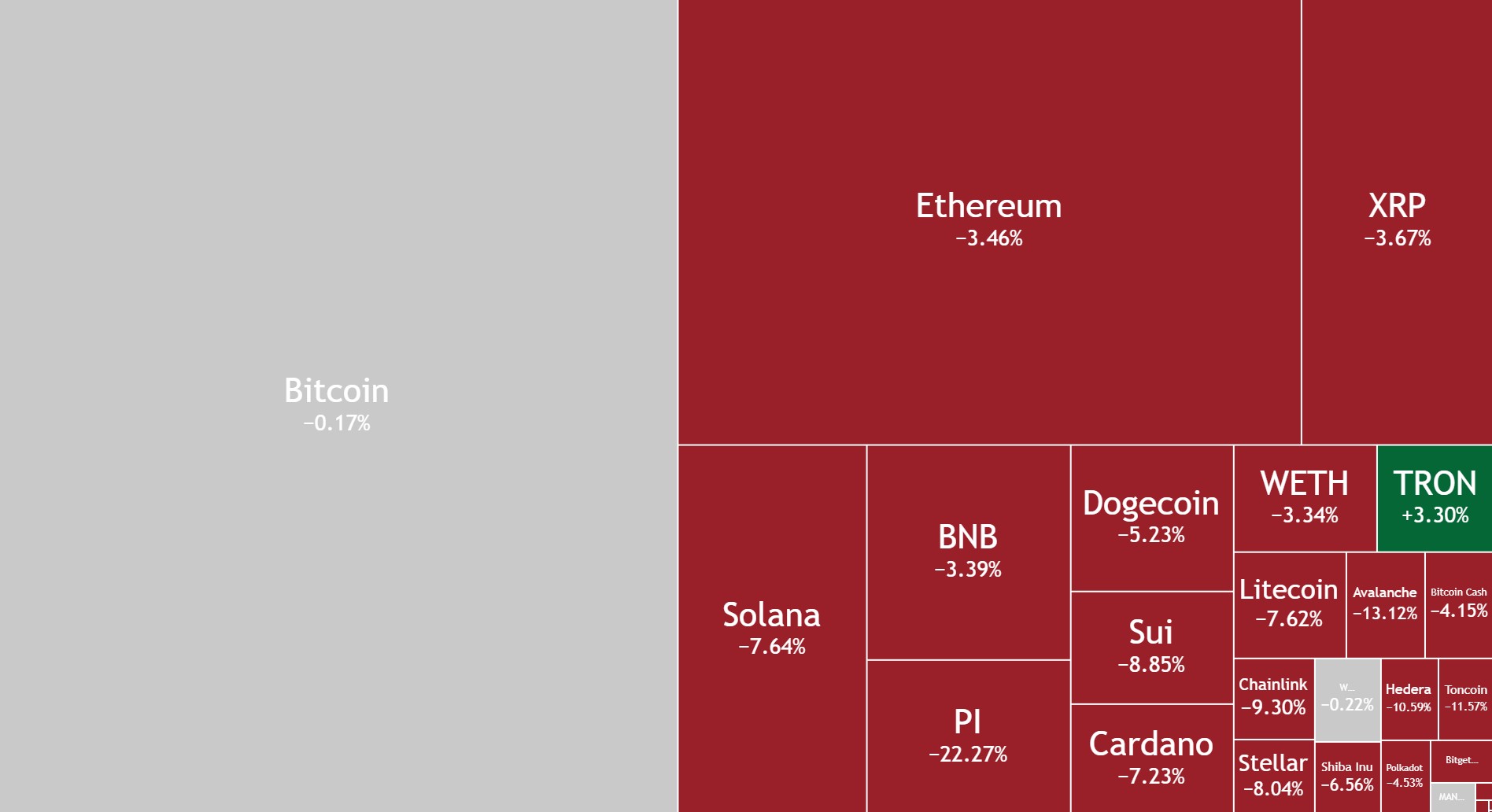

Crypto Market Weekly Performance:

Source: Tradingview

Despite a massive $6.1 trillion sell-off in US stocks last week, Bitcoin remained stable, at around $83K.

Bitcoin’s stable price may be due to increased institutional buying, including Strategy’s resumed weekly acquisitions and GameStop‘s decision to use Bitcoin as its primary treasury asset while planning to raise $1.3 billion to buy more. These trends suggest strong demand from major companies, reinforcing confidence in Bitcoin as a reliable store of value despite market pressures.

This sparked discussions about Bitcoin’s shifting role compared to traditional risk assets. While stock investors withdrew billions amid tariff-related uncertainty, the crypto market attracted $5.4 billion in fresh investments, hinting at changing investor sentiment during economic turbulence.

Technically, if BTC breaks the short-term downtrend line with strong momentum, it leads to a price increase. However, if the Fibonacci support around $80K fails, Bitcoin could drop further to the next support level.

Next Week’s Outlook

Economic Events

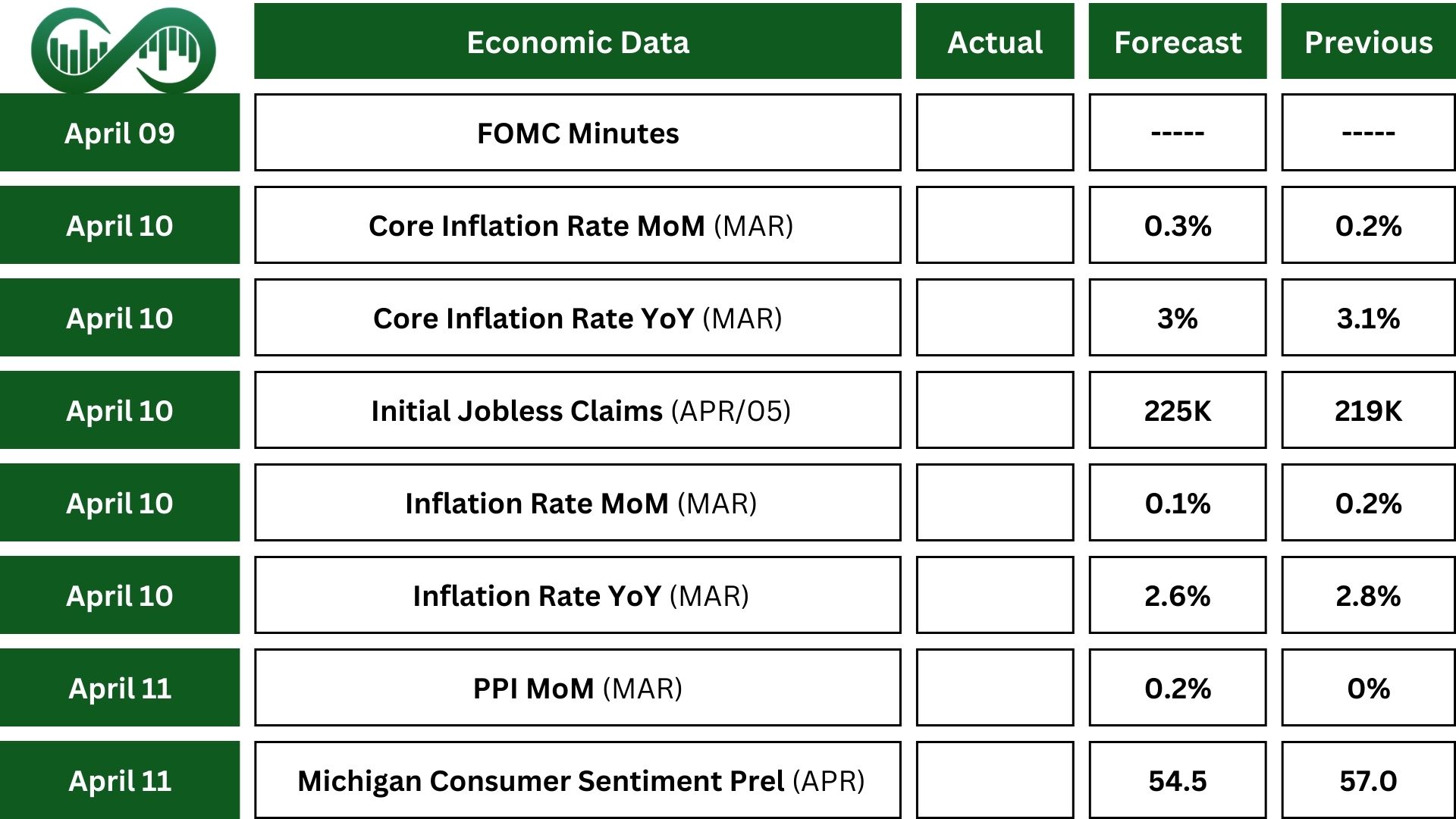

This week, the focus will be on the trade war, as traders assess the impact of U.S. tariffs and potential responses from other nations.

In the U.S., March inflation data and the FOMC minutes will be key.

Headline inflation is expected to drop to 2.6%, the lowest in five months, from 2.8% in February. Core inflation may also ease to 3% from 3.1%. However, producer prices are predicted to rise faster, with annual growth of 3.3% and core PPI expected to increase to 3.6% from 3.4%.

Consumer confidence is likely to fall for the fourth straight month, as indicated by the Michigan Consumer Sentiment Index.

The FOMC minutes may shed light on the Fed’s economic outlook, interest rates, and views on trade and fiscal policies. While the Fed left rates unchanged in March, it raised inflation projections, cut growth forecasts, and cited tariffs as a major risk.

Earnings Events

This week, the earnings season begins, with reports expected from JP Morgan Chase (JPM), Wells Fargo (WFC), Progressive (PGR), BlackRock (BLK), Constellation Brands (STZ) , and Delta Air Lines (DAL).