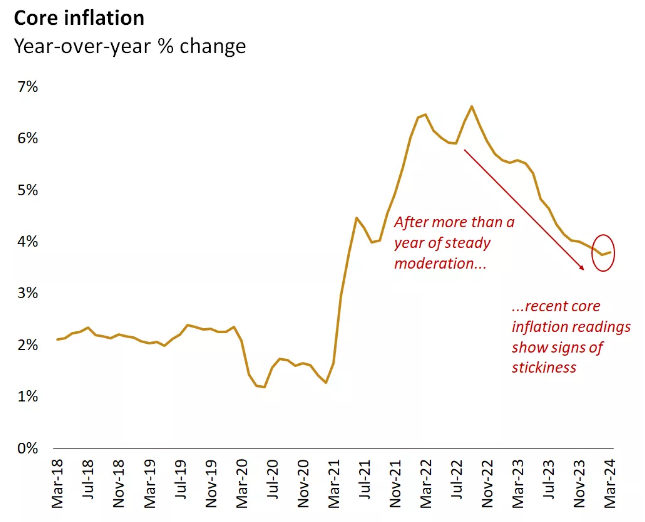

Since the begining of 2024, the pulse of inflation continues to echo, refusing to yield to resolution. Despite the Federal Reserve’s decision to maintain interest rates unchanged last week, it remains evident that the economic landscape is not evolving at a pace conducive to immediate policy adjustments. While the expectation lingers for an eventual Fed rate cut, recent indicators suggest that such a move may be postponed until later in the year, necessitating a more cautious approach to monetary policy forecasting.

The labor market, a multifaceted player in last week’s market dynamics, assumed contrasting roles of both protagonist and antagonist. Early-week labor cost data fueled apprehensions regarding persistent inflationary pressures. However, the conclusion of the week brought a sense of relief as the jobs report unveiled a cooler-than-expected scenario, allaying concerns while affirming the underlying strength of employment conditions, crucial for consumer resilience.

With a significant portion of S&P 500 entities having disclosed their first-quarter performances, the narrative of profitability continues to evolve positively. Amidst the backdrop of Federal Reserve deliberations and labor market observations dominating headlines, corporate earnings announcements have predominantly surpassed forecasts. Moreover, management outlooks have exuded optimism, contributing to upward revisions in profit growth projections for 2024.

After a five-month streak characterized by robust and consistent market gains commencing last November, recent weeks have witnessed a perceptible shift in market sentiment. Fed policy, labor market dynamics, and corporate earnings emerged as primary drivers of this transformation. Although equities concluded the previous week with gains, initiating May on a positive note after April’s downturn, the market’s recent fluctuations underscore a new narrative shaped by evolving data trends.

Economic Events:

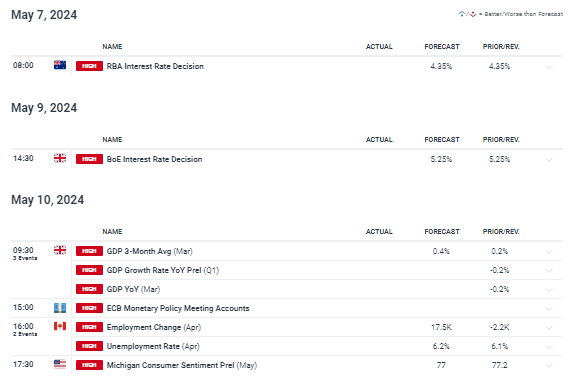

Last week’s economic indicators provided a nuanced view of the current economic landscape. The focal point was Friday morning’s release of the nonfarm payrolls report, revealing that employers added 175,000 jobs in April. This figure fell short of expectations and marked the lowest number since November. While signaling a cooling in the labor market, the report also indicated a surprise slowdown in monthly wage increases, from 0.3% in March to 0.2% in April. Furthermore, the year-over-year wage gain dropped to 3.9%, the slowest increase in nearly two years. Additionally, average weekly hours worked saw a slight decline, with the unemployment rate ticking up to 3.9%.

This news was particularly notable following earlier in the week reports, which showed an unexpected increase in employment costs and a notable slowdown in business activity in the Chicago area. Moreover, the Conference Board’s measure of consumer confidence declined to its lowest point in nearly two years in April, while the Labor Department’s tally of March job openings fell more than anticipated to the lowest level in over three years. The Institute for Supply Management also reported a contraction in its gauge of services sector activity for the first time since December 2022.

Source : Factset

Investors found some reassurance in Federal Reserve Chair Jerome Powell’s response to the data during the Fed’s policy meeting press conference. Powell pushed back against concerns of stagflation, emphasizing current growth and inflation rates of around 3%. Although the Fed kept rates steady at the meeting, Powell’s remarks suggested policymakers were not inclined to adjust rates given the current stance of monetary policy.

These developments led to a decline in the yield on the benchmark 10-year U.S. Treasury note to its lowest level in nearly a month, with a subdued primary calendar further supporting returns in the municipal bond market. In the corporate bond market, issuance remained light, with all issues being oversubscribed, and earnings reports continued to influence returns.

Looking ahead, while the possibility of Fed rate cuts remains on the horizon, it is contingent on consecutive months of improving inflation readings. This suggests a potential cut later in the year, with market direction being the primary focus amidst ongoing economic recalibration.

Source : Dailyfx

Earnings:

As we near the end of the first-quarter earnings season, the S&P 500 companies have shown remarkable resilience, with 77% beating consensus expectations, according to LSEG data. Notable among these is tech giant Apple, which saw its shares surge by 6.0% after unveiling a record $110 billion share buyback program and surpassing quarterly expectations.

Biotech firm Amgen also made waves, with its shares jumping 11.8% following positive interim data on its experimental weight-loss drug MariTide and strong first-quarter earnings. However, not all companies experienced positive outcomes, as travel platform Expedia cut its full-year revenue growth forecast, leading to a 15.3% slide in its shares.

Looking deeper into the data, of the 397 S&P 500 companies reporting earnings through Friday morning, an impressive 76.8% exceeded analyst expectations. This surpasses the historical beat rate since 1997 and underscores the resilience of corporate America in navigating the current economic landscape.

In the world of investments, Berkshire Hathaway, led by Warren Buffett, made headlines by significantly reducing its stake in Apple during the first quarter, despite posting a record operating profit exceeding $11 billion. While Berkshire’s cash reserves reached a record $189 billion, the value of its stake in Apple saw a notable decline, raising eyebrows among investors.

Buffett’s decision to trim Berkshire’s Apple holdings comes amidst a shifting investment landscape, with the legendary investor seeing the tech giant as a consumer goods powerhouse. Despite concerns from some quarters about over-reliance on Apple, Buffett remains confident in the company’s long-term prospects.

The first quarter also saw Berkshire actively repurchasing its own stock, further reflecting its commitment to capital allocation strategies. Despite a significant drop in net income compared to the previous year, Buffett remains bullish on Berkshire’s diversified portfolio and its ability to weather economic uncertainties.

Looking ahead, Buffett sees potential for Berkshire’s cash reserves to exceed $200 billion by the end of June, highlighting the company’s cautious approach in deploying capital amidst global uncertainties. As Berkshire continues to evolve under Buffett’s leadership, its stable of businesses remains a cornerstone of long-term investment strategies for many investors.

Gold (XAUUSD):

The recent surge in gold prices is largely fueled by robust demand from global central banks and households in Asia.

In China, despite economic recovery challenges post-pandemic and the yuan’s depreciation against the US dollar, local consumers remain keen on gold. The People’s Bank of China (PBOC) has consistently increased its gold reserves for 17 consecutive months, adding 160,000 ounces in March alone.

Other countries like Turkey, India, Kazakhstan, and some in Eastern Europe have also been active gold buyers this year, reflecting a broader trend among central banks to diversify their reserves and reduce reliance on the US dollar.

Gold prices experienced a slight pullback at the end of April but regained bullish momentum this week after Federal Reserve policymakers hinted at potential rate cuts. At its latest policy meeting, the Fed maintained its interest rate stance, with Chair Jerome Powell signaling that a rate hike was unlikely at this juncture. This assurance from Powell, coupled with geopolitical tensions, particularly in the Middle East, has sustained investor interest in gold, a traditional safe-haven asset.

Indices :

The markets ended the week on a positive note, marking their second consecutive Friday-to-Friday gains. This upward trend was spurred by Federal Reserve Chair Jerome Powell’s unexpectedly dovish statements following Wednesday’s rate decision, which reassured investors.

Despite the U.S. economy adding fewer jobs than anticipated, and a slight uptick in the unemployment rate coupled with cooled wage growth, the report seemed to strike a balance that the Fed found favorable. It hinted at a softening labor market, a factor Powell views as crucial for stabilizing inflation while maintaining overall economic health.

On Wall Street, all three major indexes saw significant gains, with the Nasdaq leading the charge with an impressive 2% jump. The technology sector, in particular, flourished, boosted further by Apple’s stellar performance following its quarterly earnings announcement and announcement of a record $110 billion stock buyback plan.

In terms of earnings, the majority of S&P 500 companies have exceeded analyst expectations, reinforcing positive sentiment among investors. The Dow Jones Industrial Average rose by 1.18%, the S&P 500 gained 1.26%, and the Nasdaq Composite climbed by nearly 2%.

Following the payrolls report, Treasury yields and the dollar experienced declines as investors adjusted their expectations for a potential rate cut by the Fed in September. The 10-year U.S. Treasury note yield dropped significantly, marking its largest weekly decline since mid-December.

Overall, global stocks also saw positive momentum, with MSCI’s gauge of stocks rising by 1.14% and on track for its second consecutive weekly gain.

US500 :

US100 :

Us30 :

Bitcoin (BTC):

A single Bitcoin (BTC) transaction has stirred significant interest due to its substantial gas fee. According to Whale Alert, a blockchain analytics platform, a fee of 1.5 BTC was paid for a single transaction, amounting to $100,254 based on the current market value of Bitcoin. This fee notably surpasses the average transaction cost.

The user opted to pay this substantial fee to ensure their transfer would be included in a standard Bitcoin block. While such transactions have been observed in the past, they remain rare. For instance, in September 2023, a Bitcoin user paid a transaction fee of 19 BTC, equivalent to $509,563 at the time when Bitcoin was trading at $26,000. Similarly, in January, another BTC account paid over 4 BTC, resulting in a staggering fee of 1,800,890 sat/vB to secure their transfer’s inclusion in a regular Bitcoin block.

The reason behind such high transaction fees could be attributed to several factors. Network congestion, a common occurrence in cryptocurrency ecosystems, can cause transaction fees to fluctuate significantly. For instance, during the 2017 cryptocurrency boom, transaction fees soared to as high as $60. Therefore, the recent exorbitant transaction fee might be due to a mistake, misconfiguration in transaction software, or motives known only to the transaction initiator. Alternatively, it could potentially be linked to a money laundering scheme, although this remains speculative.

Bitcoin is currently trading around its fair price. In the event of further accumulation by smart money, the price could rise to as high as $66,500. On the other hand, the support range for Bitcoin is at $57,000.

US Crude Oil WTI :

In the Market Morning reports, we delved into the potential scenario for oil prices. There’s a strong likelihood that oil prices could shift their trajectory with easing tensions in the Middle East and recent economic data indicating a cooling U.S. labor market. The support level at 77.42 is now within reach.

The decline in the dollar, spurred by hopes of interest rate cuts following weaker-than-expected job gains and wage growth in April, has influenced our outlook. Morgan Stanley’s recent analysis suggests that while we still anticipate three 25 basis point cuts this year, beginning in July, the likelihood of a cut in July has slightly diminished given the reflationary trends observed in first-quarter 2024 data.

A weaker dollar typically stimulates demand for oil among non-dollar investors. However, despite the dollar’s decline, oil prices experienced significant pressure earlier in the week due to unexpected increases in U.S. inventories and higher U.S. production levels. These factors were compounded by easing concerns about supply disruptions in the Middle East amid ongoing negotiations between Israel and Hamas for a potential ceasefire.

For the stock market in the upcoming week, positive movement is anticipated, taking into account the remarks of the head of the Federal Reserve and the employment data released on Friday. However, as earnings reports approach their end, the dollar pricing may act as a market driver.

Regarding gold, there is currently an expectation of a slight increase in price due to the weakening dollar, but it’s important to note that the trend for gold in higher time frames is currently negative.

As for oil, it appears to have strong downward momentum, and if this momentum is not curbed by buyers, the price of oil could penetrate much lower levels.

In the cryptocurrency market, during the time when global markets were closed, namely over the weekend, there was a favorable upward momentum, and if demand continues to increase, this upward momentum could be sustained.

Wishing everyone a profitable week ahead with the Meta Trading Club!

Disclaimer: The views and opinions expressed in the blog posts on this website are those of the respective authors and do not necessarily reflect the official policy or position of Meta Trading Club Inc. The content provided in these blog posts is for informational purposes only and should not be considered as financial advice. Readers are encouraged to conduct their own research and consult with a qualified financial advisor before making any investment decisions. Meta Trading Club Inc shall not be held liable for any losses or damages arising from the use of information presented in the blog posts.