Economic Reports

Trump Orders Tax on Imports: Starting March 4, President Trump imposes a 25% tax on steel and aluminum imports with no exceptions. The US mainly imports steel from Canada, Brazil, Mexico, and South Korea, and aluminum from Canada and the UAE.

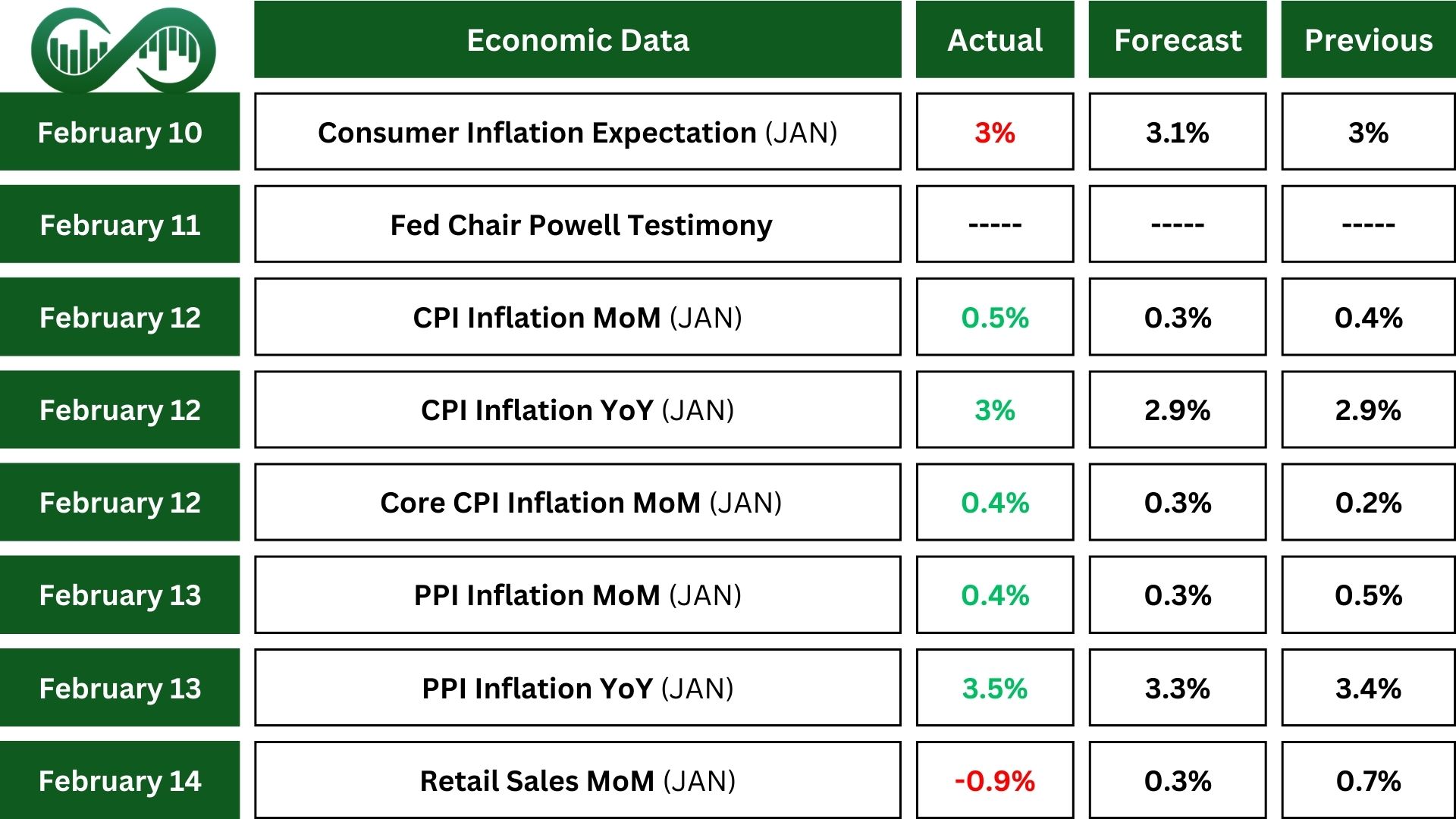

Federal Reserve’s Testimony: Since September, the FOMC lowered the policy rate by a full percentage point. The recalibration was in response to progress on inflation and labor market cooling. The current policy stance is less restrictive, given the strong economy. With the policy stance now significantly less restrictive and the economy remaining strong, there is no immediate need to adjust the policy stance hastily.

Consumer Inflation Report: In January, CPI increased by 0.5% and made a 3% increase over the year. Also, core inflation, excluding food and energy, rose by 0.4% in January and 3.3% annually. These figures were higher than expected, suggesting easing inflation and potentially leading the Federal Reserve to pause interest rate cuts, which could affect borrowing costs and stock prices.

Producer Inflation Report: PPI in the US rose to 0.4% in January and exceeded estimates. Producer prices increased by 3.5% compared to January 2024, However, core producer prices, excluding food and energy, rose by 0.3% in January 2025, aligning with forecasts. This signals the Federal Reserve might delay lowering interest rates, keeping borrowing costs high.

Retail Sales Report: US retail sales dropped by 0.9% in January, a larger decline than the expected 0.1%. This followed a revised gain of 0.7% in December, signaling weaker consumer spending and potentially slowing economic growth.

Earnings Reports

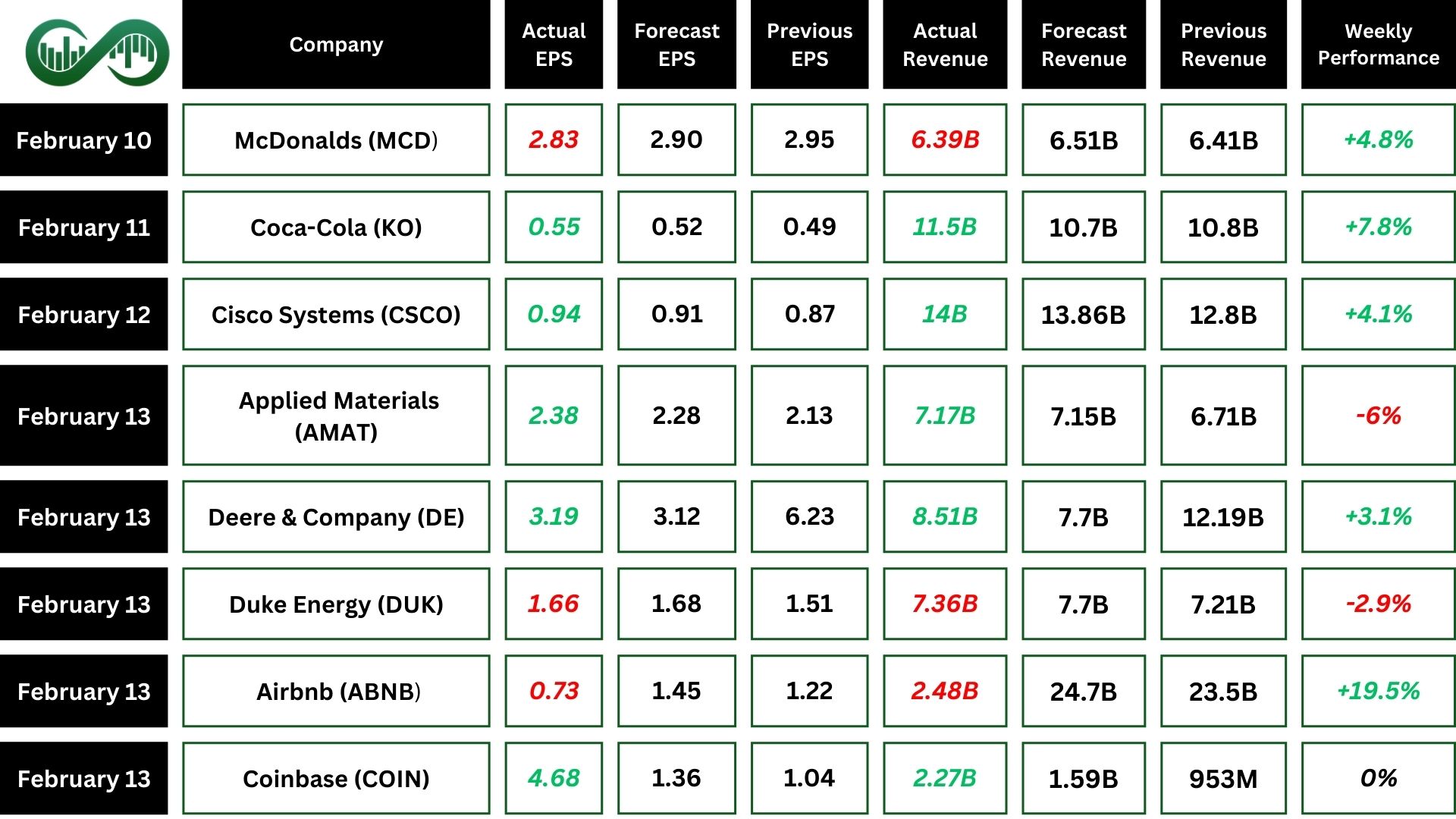

McDonalds

McDonald (MCD) reported their Q4 and full-year 2024 results. They made over $130 billion in sales for the year, with a $1 billion increase from last year.

Sales to loyalty members grew to $30 billion for the year and $8 billion for the quarter, showing a 30% increase.

By the end of 2024, they had over 175 million active loyalty users, up by 15%.

Technically, following a rise in the stock price due to an earnings gap, the price has remained above a key level around $303. As long as it holds this support, there is a possibility for the stock to reach its all-time high at $317.9 or even higher. However, if the stock price falls and fills the earnings gap, it could either range or decline further to the next support level around $280.

Coca-Cola

Coca-Cola (KO) reported its financial results for the fourth quarter and full year of 2024.

In the fourth quarter, net revenues increased by 6%, and organic revenues rose by 14%. Operating income went up by 19%, and earnings per share (EPS) grew by 12% to $0.51.

For the full year, net revenues increased by 3% but operating income declined by 12%, and EPS slightly decreased.

Overall, Coca-Cola experienced quarterly growth but faced some challenges throughout the year.

Technically, the stock price is at a critical zone. If it breaks above the significant downtrend line and stays above it, this could be a bullish signal, potentially leading to an increase up to its all-time high around $73.5. However, if the stock price remains below this trend line, it may engage in ranging or retracement actions.

Cisco Systems

Cisco (CSCO) reported Q2 2025 earnings with $14 billion in revenue. The company’s net income was $2.4 billion ($0.61 per share), above estimates.

They increased the quarterly dividend to $0.41 per share and authorized an additional $15 billion for stock repurchases, returning $2.8 billion to shareholders. Product orders grew 29% year-over-year, 11% excluding Splunk, with growth in all regions and markets.

AI infrastructure orders exceeded $350 million, totaling about $700 million for the first half of fiscal year 2025, and are expected to surpass $1 billion for the year.

Following this positive report, Cisco’s stock reached a new all-time high.

Technically, the stock is demonstrating a solid bullish trend. As long as it maintains the last higher low around $61, the trend remains favorable. Additionally, there is a critical support level at $64, which was a former all-time high and has now become an important support. As long as the stock remains above these two key levels, it has the potential to rise up to the Fibonacci levels from $68 to $86. However, if the stock price falls below $58, an important level, it could signal further decreases.

Airbnb

Airbnb (ABNB) made a profit of $461 million in the fourth quarter, bouncing back from a $349 million loss the previous year.

The company’s revenue jumped by 12%, surpassing expectations. Gross booking value also rose by 13%.

However, Airbnb predicts its first-quarter revenue in 2025 will be between $2.23 billion and $2.27 billion, slightly below expectations. This is due to an exceptionally strong quarter the previous year because of the timing of Easter and Leap Day.

Technically, after breaking a significant downtrend line, ABNB’s price stayed above a crucial static and dynamic resistance around $155. This suggests the potential to reach higher resistance levels around $170 and $180. However, if the price drops and fills the earnings gap, it might decline further to approximately $125.

AppLovin

AppLovin (APP) reported $1.37 billion in revenue for Q4 2024, a 44% increase from the previous year. Earnings per share (EPS) increased to $1.73 from $0.49 a year ago. Revenue and EPS surpassed estimates.

For the entire year of 2024, AppLovin’s advertising revenue grew by 75% compared to 2023. Total revenue rose by 43%, and net income saw an impressive 343% increase compared to the previous year.

These numbers demonstrate the company’s strong growth and financial performance over the past year.

Technically, APP broke its previous all-time high after reporting strong quarterly earnings, reaching a significant Fibonacci resistance zone at $500. If it breaks and holds above this level with confirmation, it could lead to higher prices. However, if it gets rejected from this area, the price may bounce back to the former all-time high at $394.

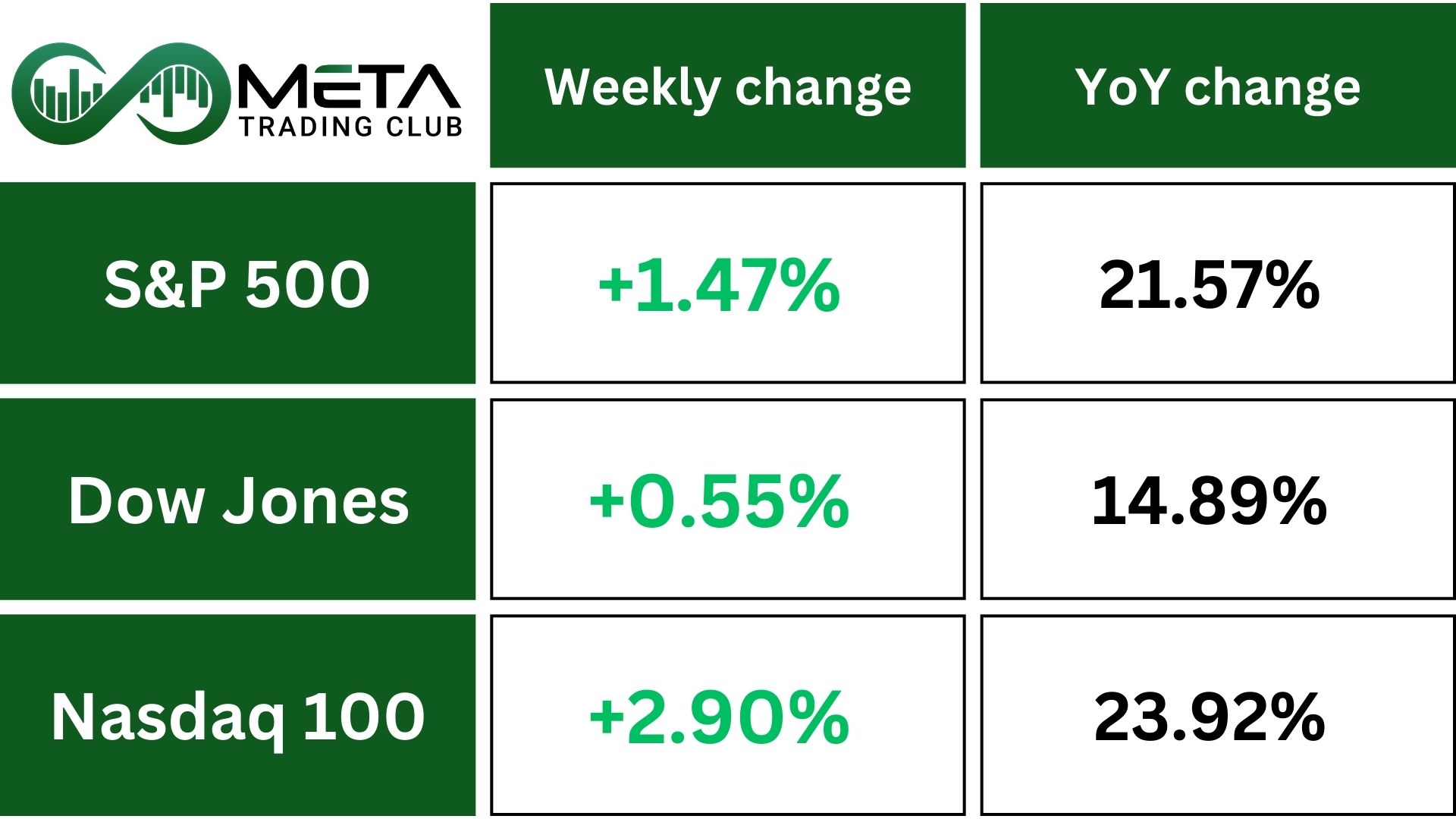

Indices

Indices’ Weekly Performance:

Last week, the NASDAQ index had its best week of the year with a 2.58% increase. It performed better than the smaller gains seen in the Dow Industrial Average and the S&P 500 indices.

Expectations for a 25 basis point rate cut by the Federal Reserve in June have risen to 51.3%, up from 40.3%..

Dallas Fed President Lorie Logan stated on Friday that even if inflation data improves in the coming months, the U.S. central bank should not automatically lower short-term borrowing costs.

The S&P 500 reached its all-time high resistance zone at 6136. If the RSI can break its downward trend line with strong momentum and the price can overcome the 6,136 resistance, a further surge is anticipated.

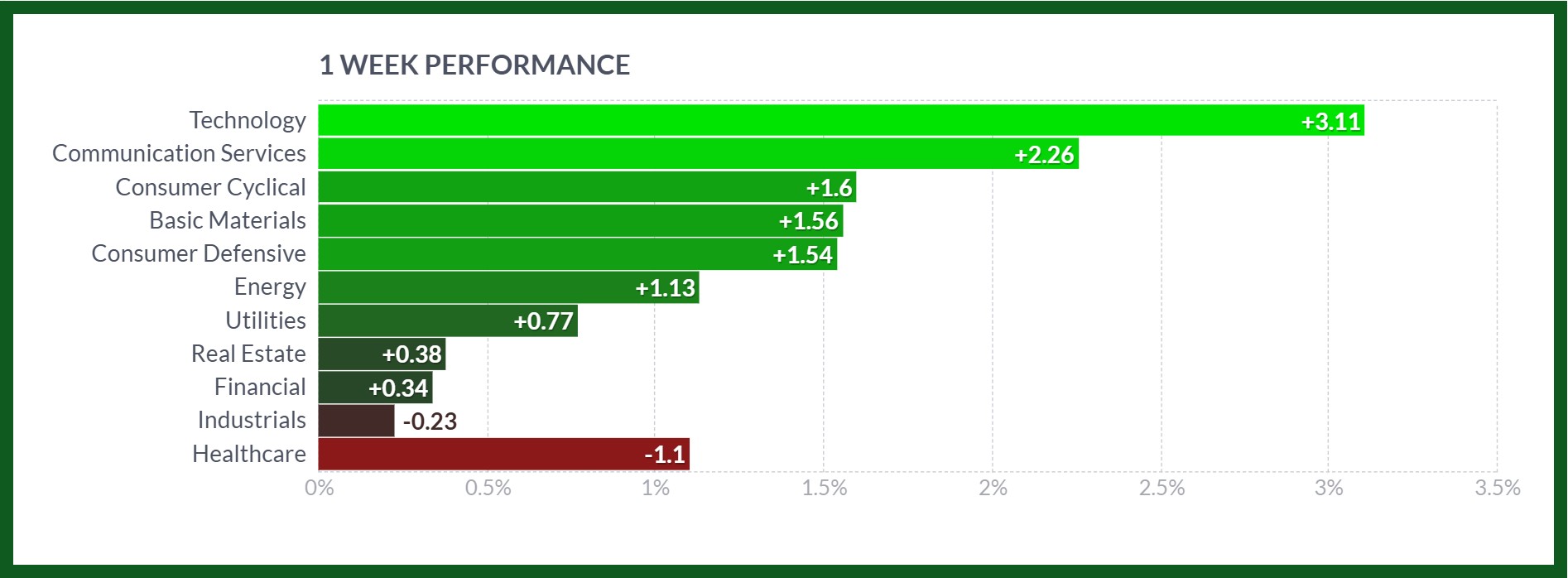

Stocks

Sector’s Weekly Performance:

Source: Finviz

- The technology sector saw strong 3.11% gains, driven by positive performance in semiconductors.

- The communication services sector experienced a 2.26% increase due to increased demand for digital communication and media services.

- The consumer cyclical sector rose by 1.6%, thanks to higher consumer spending and confidence.

- The basic materials sector climbed by 1.56%, supported by industrial demand and rising commodity prices.

- The consumer defensive sector increased by 1.54%, benefiting from steady demand for essential goods.

- The energy sector gained 1.13%, fueled by increased energy consumption.

- The healthcare sector dropped by 1.1%, impacted by regulatory concerns and lower-than-expected earnings.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- Applovin (APP): The stock surged by 35% due to strong earnings reports and positive investor sentiment about the company’s growth prospects.

- Intel (INTC): Shares rose by 23.5% amid comments from US Vice President JD Vance that the “most powerful” artificial intelligence systems will be built in the US.

- Airbnb (ABNB): The stock increased by 19.5% as travel demand rebounded and the company reported strong quarterly earnings.

- T-Mobile US (TMUS): Shares gained 10% after the company said it has launched its satellite-powered T-Mobile Starlink service in beta mode.

- PDD Holdings (PDD): The stock climbed by 8% due to strong sales growth and positive market sentiment.

- Coca-Cola (KO): The stock increased by 7.9% as the company reported better-than-expected guidance.

- Micron (MU): Shares gained 7.8% due to strong demand for memory chips and positive industry outlook.

- Palantir (PLTR): The stock rose by 7.5% following strong quarterly results and positive analyst recommendations.

- Apple (AAPL): Shares increased by 7% as the company made a notable market breakthrough in China through its new partnership with Alibaba.

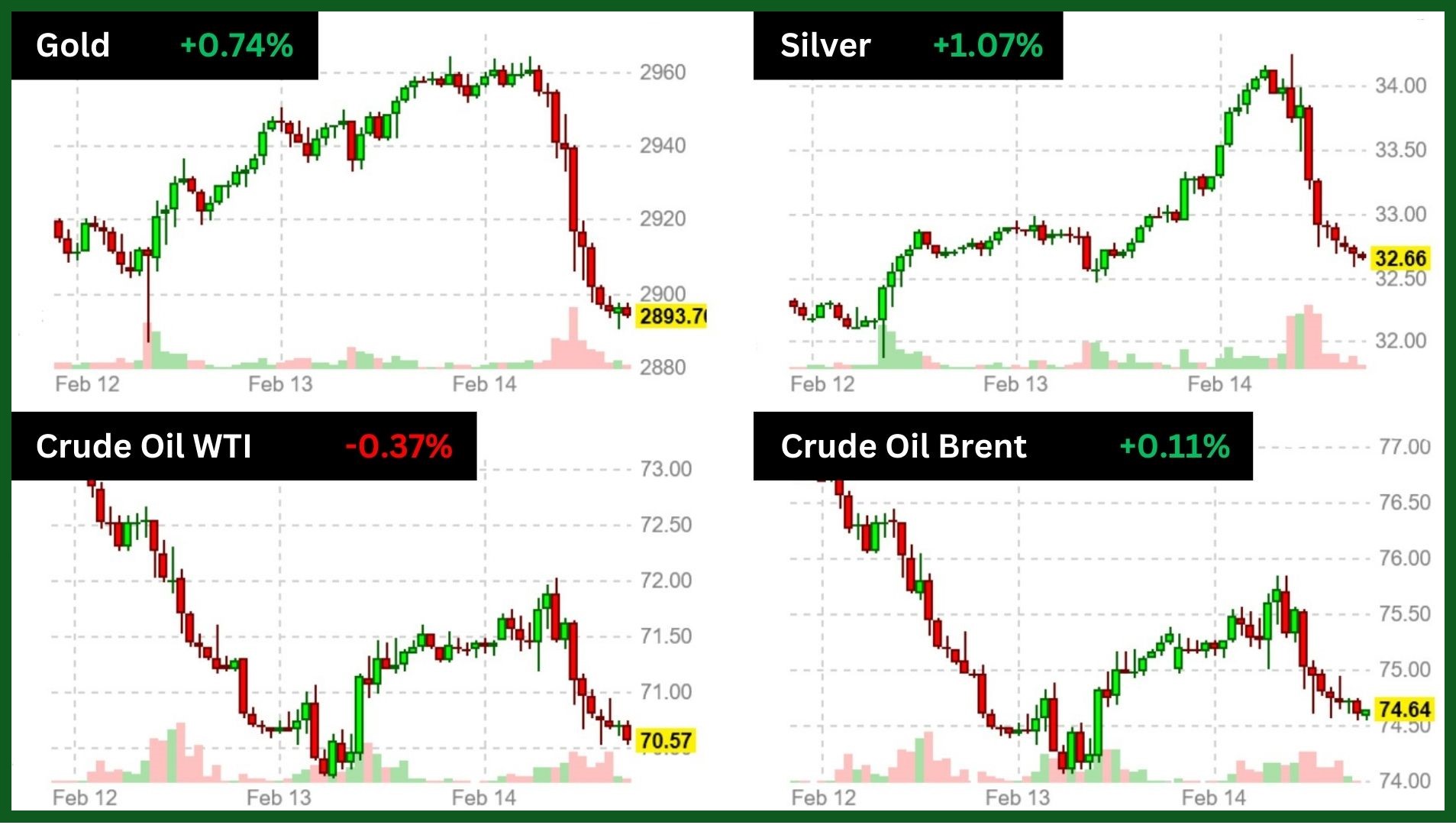

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold futures had another positive week, marking their seventh consecutive weekly gain. For the week, gold increased by 0.6% to $2,883.60 per troy ounce.

President Trump’s decision to have agency heads study potential reciprocal tariffs lowered gold sentiment.

WTI crude futures are set for their fourth consecutive weekly loss, while Brent looks to break a three-week losing streak.

The International Energy Agency forecasts global oil demand growth will rise to 1.1 million barrels per day in 2025, with supply increasing by 1.6 million barrels per day this year but noted uncertainties from potential tariffs.

President Donald Trump has ordered the development of “reciprocal tariffs” on other countries, seeking a comprehensive report on each trading partner by April. This move is expected to target key countries with significant trade deficits, including the European Union.

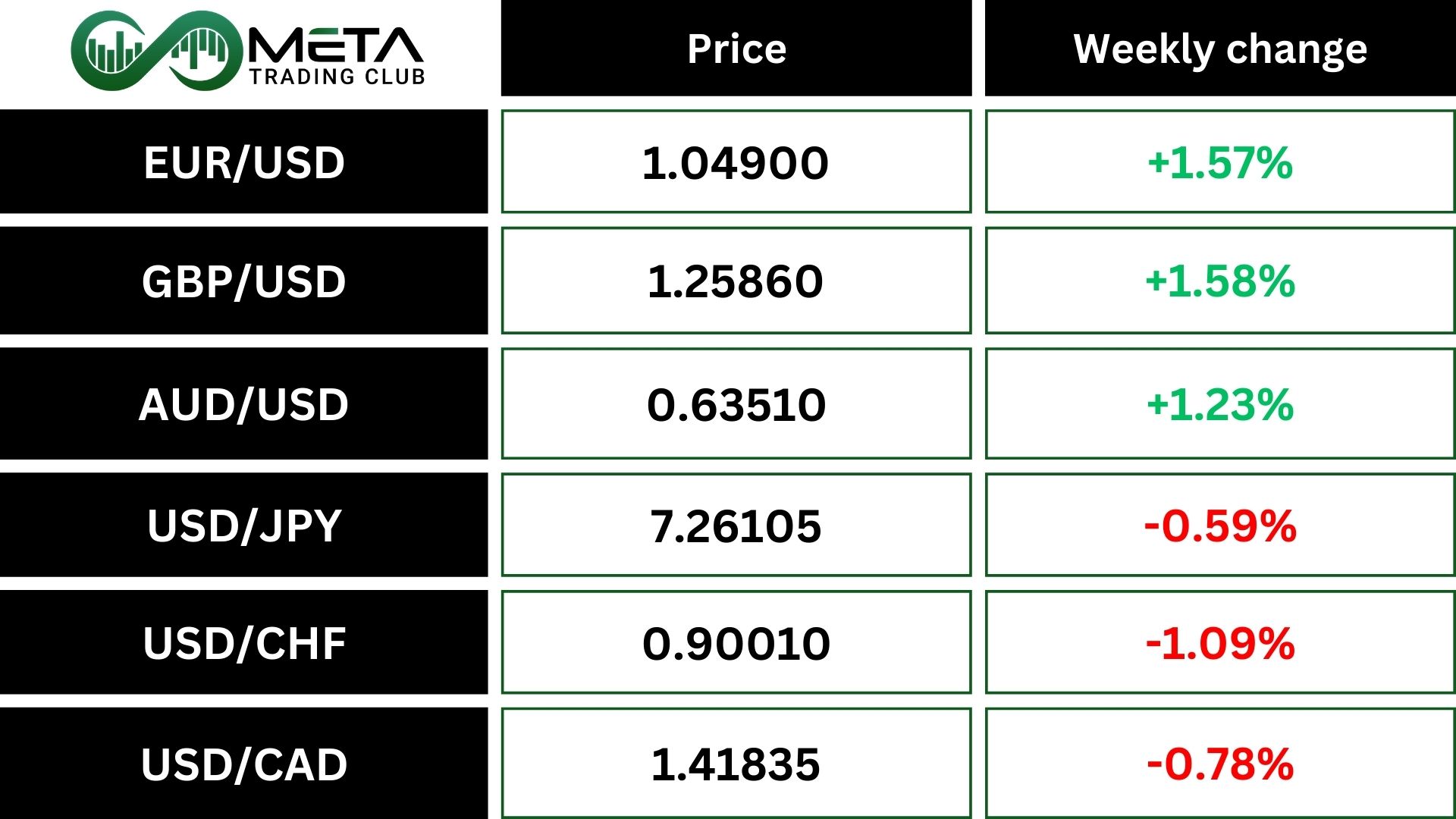

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The dollar index was set for a weekly loss against the euro. Delayed US trade tariffs raised hopes they won’t be as bad, and optimism about a Russia-Ukraine peace deal boosted the euro.

The dollar index fell to a nine-week low after worse-than-expected retail sales in January, making traders believe the Federal Reserve might cut rates twice this year.

EUR/USD gained driven by optimism over Ukraine peace talks. Meanwhile, the European Commission warned it would respond “firmly and immediately” to any tariff increases.

Against the Japanese yen, the dollar weakened by 0.59%.

Sterling extended its gains against the dollar, hitting an 8-week high above 1.26 due to weaker U.S. data, a stronger UK economy.

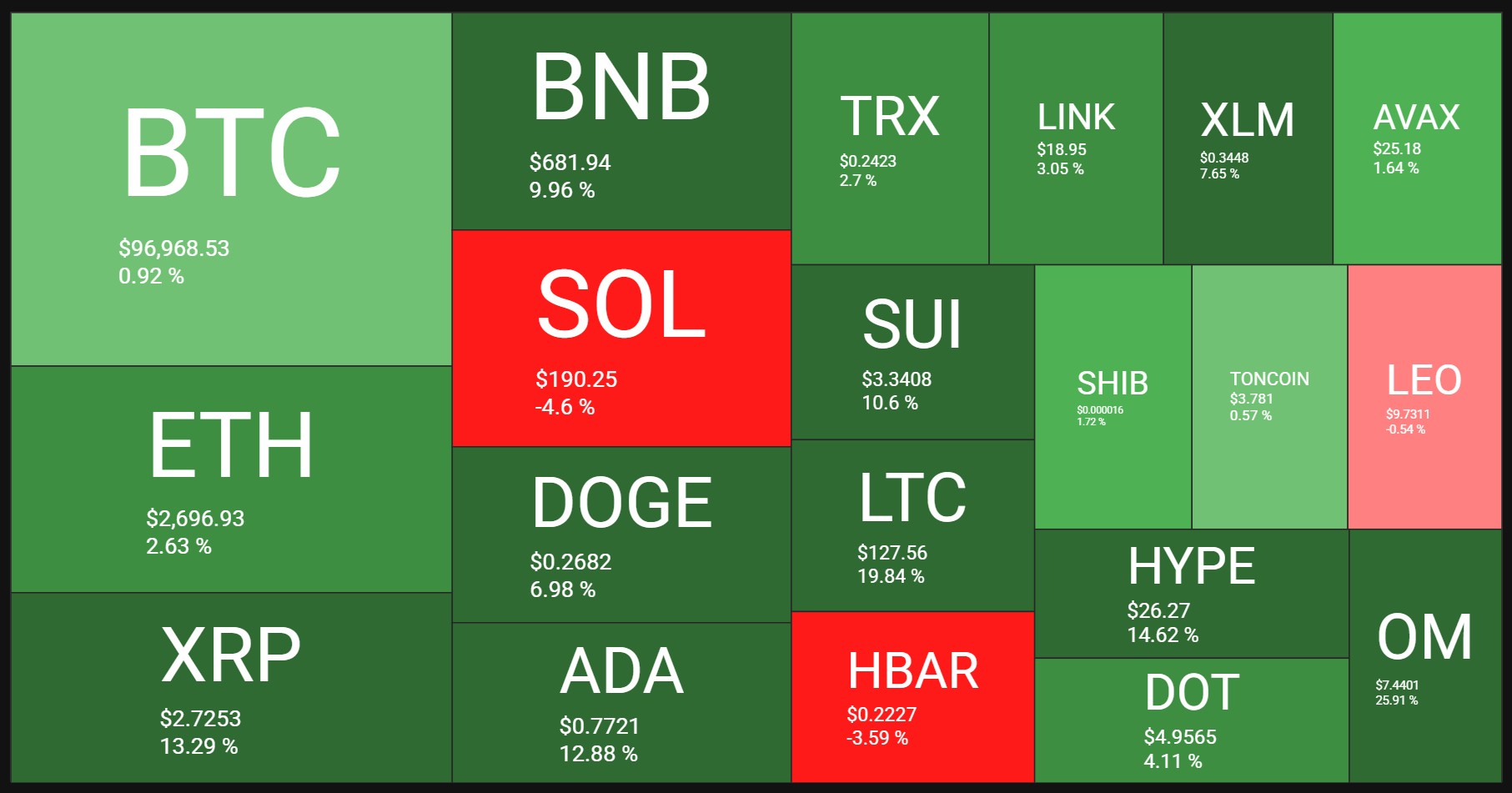

Crypto

Crypto Market Weekly Performance:

Source: quantifycrypto

Bitcoin‘s price is stuck around $96K, with buyers and sellers both trying to take control. If the price falls below this level, it could drop further to around $90K. However, if buyers step in and push the price up, it could reach $100K.

In a shorter time frame, Bitcoin’s price is in a pattern that looks like a flag. It’s just above an important support level. If it stays above this level, it could break out and continue to rise. But if it falls below, the price might drop quickly to $90K or lower. Traders should be ready for sudden price changes until a clear trend emerges.

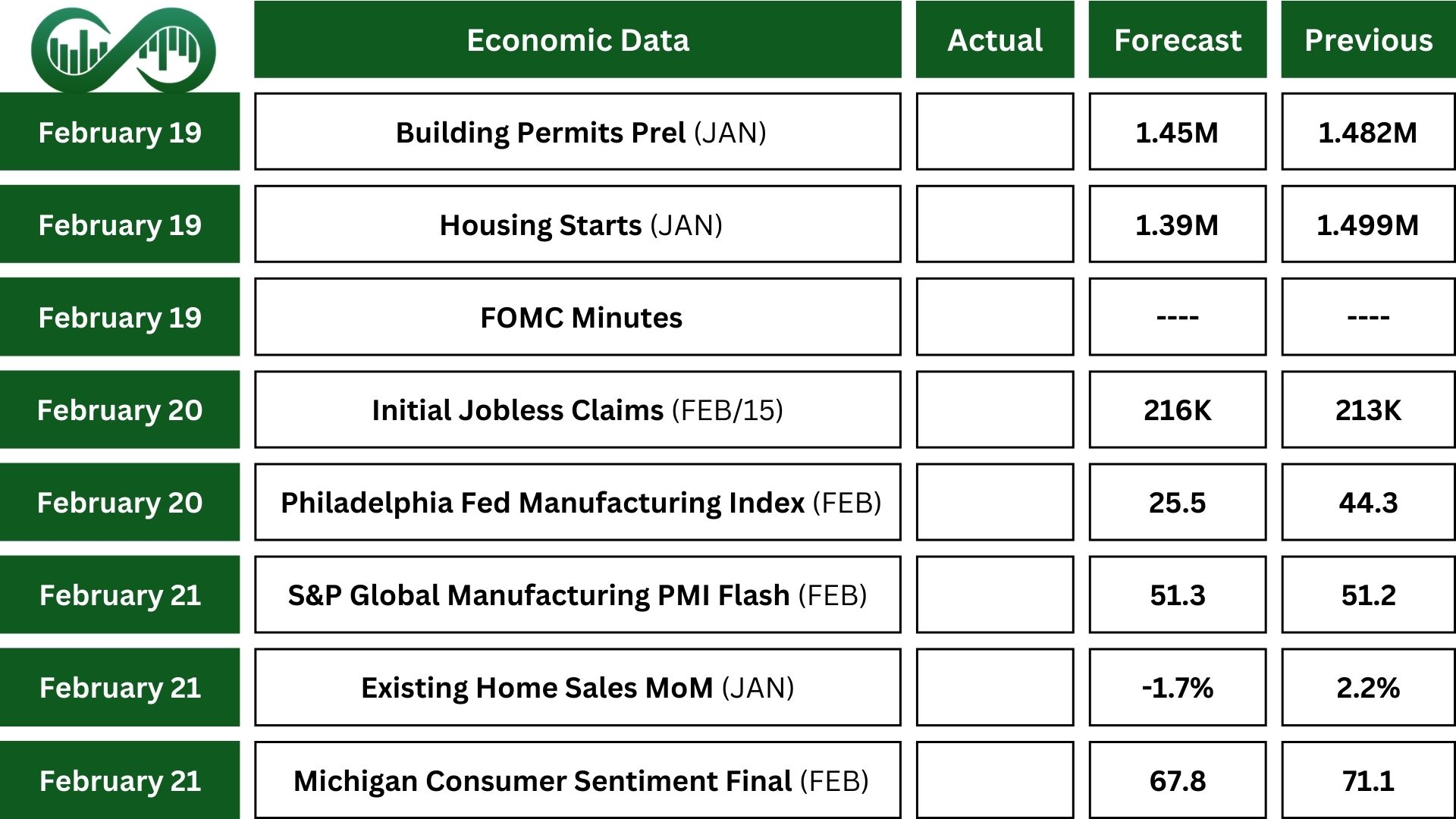

Next Week’s Outlook

Economic Events

In the US, traders will keep an eye on the FOMC minutes and comments from Fed officials to understand the central bank’s plans.

S&P Global PMIs will give an early look at February’s economic activity. Also, the NY Empire State Manufacturing Index is expected to show a smaller decline in New York’s manufacturing, while the Philadelphia Fed Manufacturing Index likely dropped from its 2021 peak.

Housing reports like the NAHB Housing Market Index, building permits, housing starts, and existing home sales will be important, with most signs showing a slowdown in the housing market.

Lastly, final figures for the Michigan Consumer Sentiment Index will be released.

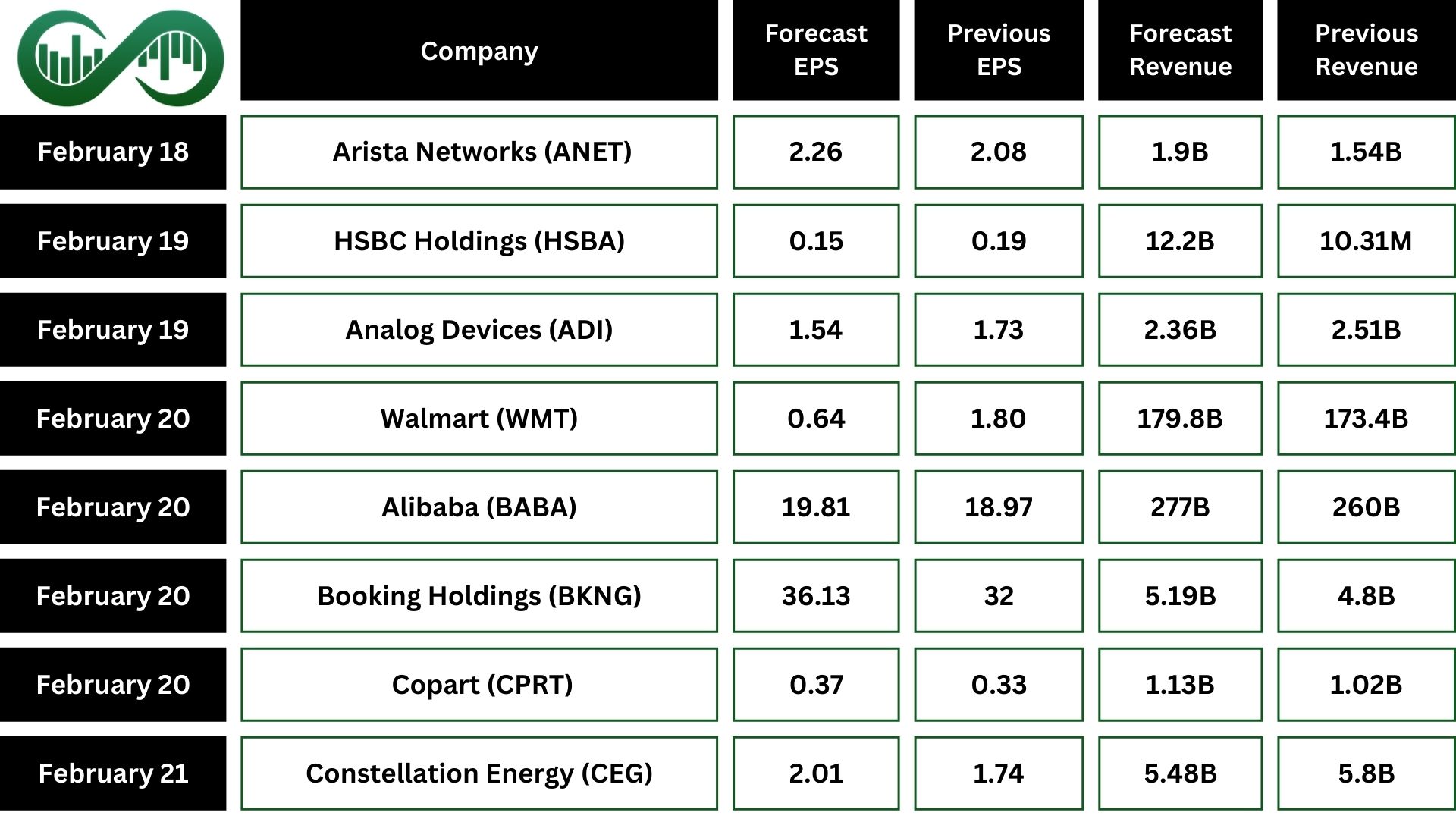

Earnings Events

In corporate earnings, major companies like Walmart (WMT), Booking Holdings (BKNG), Analog Devices (ADI), and Arista Networks (ANET) will report.

Meanwhile, US stock and bond markets will be closed on Monday for Presidents Day.