PepsiCo, Inc. is a global food and beverage leader headquartered in New York. Founded in 1965 through the merger of Pepsi-Cola and Frito-Lay, the company operates in over 200 countries and territories. PepsiCo’s diverse portfolio includes iconic brands like Pepsi, Mountain Dew, Gatorade, Tropicana, Lay’s, and Quaker. It is known for its broad product range, spanning soft drinks, snacks, and nutrition products.

PepsiCo focuses on performance with purpose, aiming for sustainable growth while reducing its environmental footprint. The company has committed to water conservation, sustainable sourcing, and reducing carbon emissions across its supply chain. In addition to its sustainability initiatives, PepsiCo continually innovates in health and wellness, offering more nutritious products to meet evolving consumer preferences.

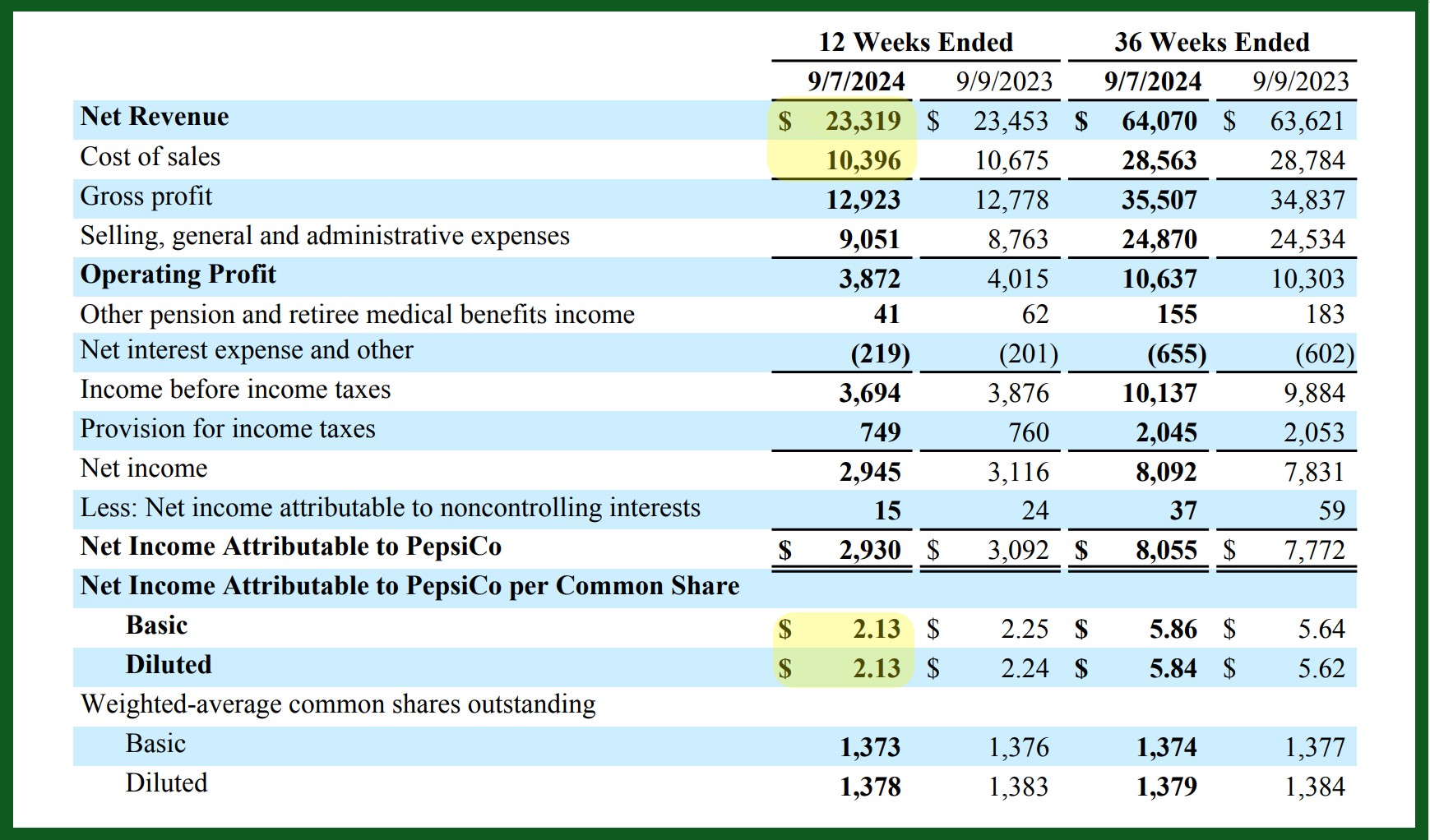

Pepsi Fiscal Q3 2024

PepsiCo (PEP) Q3 2024 earnings report shows stable performance with some mixed results across its divisions.

Here are the key points:

- Revenue: Net revenue declined 0.6% YoY to $23.32 billion, missing expectations.

- EPS: Adjusted EPS was $2.31, slightly above the $2.29 estimate.

- Regional Performance: North America saw weak demand, with Quaker Foods down 13%, while Europe grew 7%.

- Margins: Gross margin improved by 94 basis points, but operating margin shrank by 51 basis points.

The company reported net revenue declining 0.6% year-over-year to $23.3 billion, missing market expectations. However, organic revenue still grew by 1.3%. The company reported net income of $2.9 billion, translating to $2.13 per share, compared to $3 billion in the same period last year.

Despite these revenue challenges, PepsiCo exceeded earnings expectations with a core EPS of $2.31, slightly above the forecasted $2.29.

Notably, North American sales faced headwinds due to product recalls and weak demand, especially in Frito-Lay and Quaker Foods. Sales in international markets were also uneven: Latin America saw a 5% decline, while Europe experienced a 7% increase. The company lowered its 2024 revenue guidance, now expecting low single-digit growth, down from the previous estimate of 4%.

Key business segments difficulties:

- Frito-Lay North America saw a 1% decline in revenue.

- Quaker Foods North America was impacted by product recalls, leading to a 13% drop in revenue.

- PepsiCo Beverages North America remained flat but showed modest 1% organic revenue growth, driven by the strength of brands like Gatorade and Propel.

Guidance and Outlook

For the full year, PepsiCo adjusted its organic revenue growth forecast to a low-single-digit percentage, down from an earlier projection of 4%. However, they reaffirmed expectations for core constant currency EPS growth of at least 8%. The company plans to continue investing in brand support while managing costs in response to ongoing economic headwinds.

Board Statements

CEO Ramon Laguarta highlighted the resilience of PepsiCo’s operations despite “subdued category trends in North America” and disruptions caused by geopolitical tensions. The company’s profitability benefited from strong cost controls and targeted investments in productivity and market competitiveness. Laguarta emphasized PepsiCo’s focus on stimulating consumer demand through brand support and productivity enhancements for the remainder of the year.

Impact on the Market

PepsiCo’s stock responded positively, gaining over 1% despite the revenue miss, reflecting investor confidence in the company’s ability to manage costs and maintain profitability. However, the lowered guidance for organic revenue growth raised concerns about the overall macroeconomic environment and its potential effect on consumer demand and future performance.