After a day of active trading in the financial markets on Wednesday, it appears that the market took a more subdued stance today, likely in anticipation of the upcoming employment data and NFP release on Friday.

Now, considering the developments from the recent FOMC meeting, this report will delve into an analysis of various market conditions and explore potential scenarios for different asset classes.

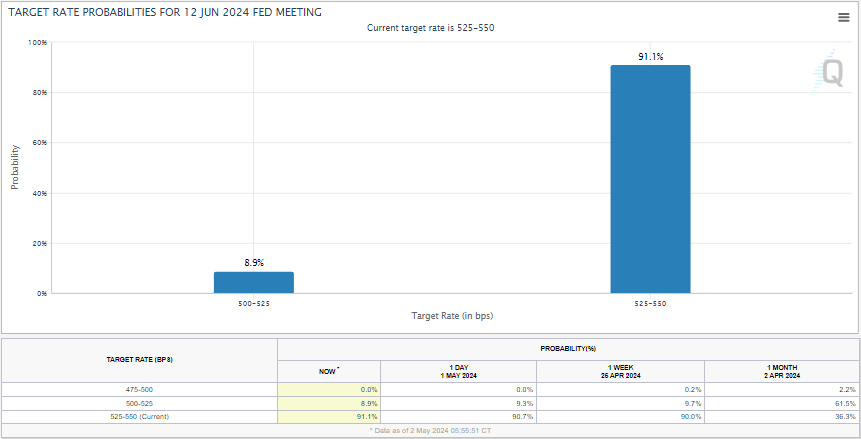

Economic Events:

During the most recent Federal Open Market Committee (FOMC) meeting held on April 30 – May 1, 2024, interest rates were maintained at the range of 5.25%-5.50%. This decision was widely anticipated, allowing the Federal Reserve additional time to assess whether the current rates effectively manage inflation while supporting economic growth. However, the minutes from the meeting revealed a somewhat hawkish tone, indicating, “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” This marks a shift from the language used in late 2023, when the FOMC hinted at the possibility of at least three rate cuts in 2024. The Federal Reserve has expressed ongoing concerns about inflation, which government reports confirm remains stubbornly high.

Market expectations leading up to the May meeting were therefore tempered regarding the likelihood of a rate cut.

During the 2022-2023 period, the Federal Reserve raised rates 11 times in efforts to curb inflation but has maintained rates steady at 5.25%-5.50% since July 2023. Following the September 2023 meeting, Federal Reserve Chairman Jerome Powell had suggested the possibility of one more rate hike before the end of 2023. However, this did not materialize, as the Federal Reserve’s aggressive rate hikes in 2022-2023 appeared to have achieved their intended effect. The sustainability of this stance remains uncertain. Nevertheless, Powell reiterated that no definitive decisions about the future have been made, emphasizing the Federal Reserve’s commitment to evaluating each meeting individually and expressing readiness to maintain rates unchanged for as long as necessary.

Source : CME

Earnings:

The first-quarter earnings season continues, with Apple , the iPhone maker, scheduled to report its earnings after the market close. While a sustained weakness in iPhone sales is anticipated, much attention will be directed towards the tech giant’s strategies and advancements in artificial intelligence.

Market expectations for Apple’s EPS stand at $1.5, with revenue of $90.33 billion. It remains to be seen whether Apple can deliver a positive earnings report akin to its competitors, given the challenging landscape.

Qualcomm saw a 5% increase in its stock price after the chipmaker announced stronger-than-expected guidance.

Source : EarningsWhispers

Gold (XAUUSD):

Gold strengthened in the aftermath of the FOMC announcement yesterday and experienced a resurgence following the press conference. It appears that gold has been primarily moving towards its fair price, driven by expectations related to interest rates.

It should be noted that gold tends to exhibit significant volatility during the release of NFP data. If negative momentum builds, $2296 per ounce emerges once again as a crucial support level for gold.

S&P500:

After the S&P 500 hit the floor of the flag pattern and the FOMC meeting, it appears that the S&P 500 is awaiting Apple’s earnings report, given its significant weighting in this index. Therefore, until the index breaks out of this pattern, we cannot expect any significant or sustained movements from it. In tomorrow’s report, we will focus on the impact of Apple’s earnings report on this index. There is a strong possibility that either the earnings report from Apple or the NFP data could serve as a strong driver, providing enough momentum for the index to break the pattern.

Foreign Exchange Market (FOREX):

Regarding the FOMC and its impact on the market, the discussion has centered around the forex market. It appears that USD/JPY could potentially initiate a downward trend towards 146. The Dollar Index indicates a downward bias, and the recent strengthening of the dollar could enter a corrective phase in the near future.

Bitcoin (BTC):

Bitcoin finally broke through a significant support level yesterday, and currently, there is no major support level for this digital asset. There is a possibility of increasing downward momentum, which could potentially push Bitcoin down to the $52,000 range.

US Crude Oil WTI :

Oil has precisely reached its support level of $79 per barrel as per yesterday’s scenario. Currently, demand is being observed from this level, and it remains to be seen whether this demand indicates a corrective move in the downward trend of oil prices or if there is a possibility of price reversal and a shift in the upward trend.

The MTC team wishes you a great day ahead!

Disclaimer: The views and opinions expressed in the blog posts on this website are those of the respective authors and do not necessarily reflect the official policy or position of Meta Trading Club Inc. The content provided in these blog posts is for informational purposes only and should not be considered as financial advice. Readers are encouraged to conduct their own research and consult with a qualified financial advisor before making any investment decisions. Meta Trading Club Inc shall not be held liable for any losses or damages arising from the use of information presented in the blog posts.