The Iron Condor is a complex, market-neutral options trading strategy designed for experienced investors. It involves four different options with the same expiration date but different strike prices. This strategy aims to profit from low volatility in the underlying asset and the passage of time, assuming the asset’s price remains within a specific range.

How it Works

An Iron Condor consists of two parts: a bear call spread and a bull put spread. Here’s how these components work:

- Bear Call Spread: Sell an out-of-the-money call option (higher strike price) and buy a further out-of-the-money call option (even higher strike price). This part profits from a drop in the asset’s price or time decay if the asset’s price stays below the lower call strike price.

- Bull Put Spread: Sell an out-of-the-money put option (lower strike price) and buy a further out-of-the-money put option (even lower strike price). This part profits from a rise in the asset’s price or time decay if the asset’s price stays above the higher put strike price.

The sold options (short positions) generate premium income, while the bought options (long positions) cap the maximum loss but also require a premium outlay.

Objective

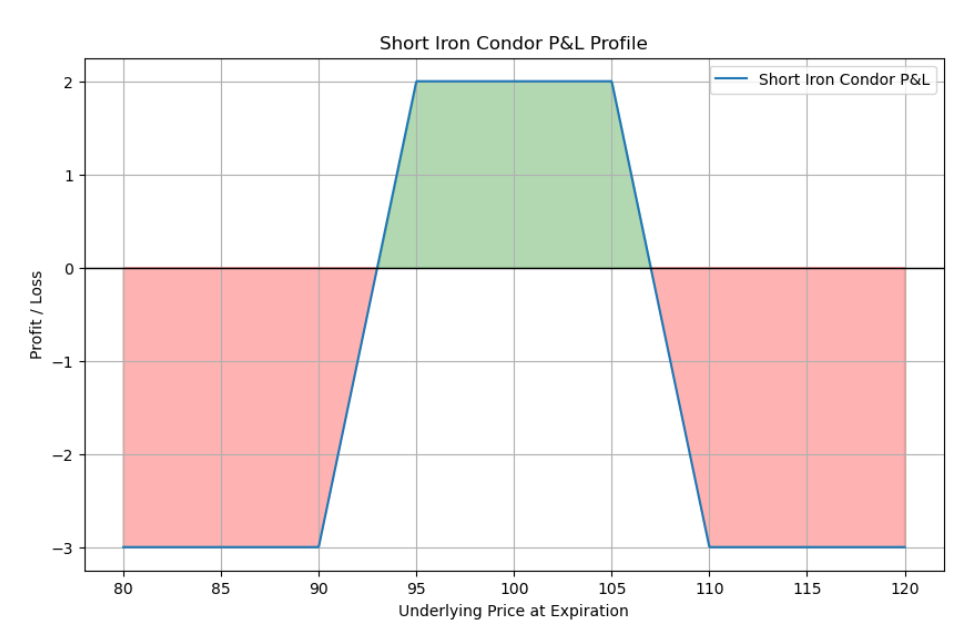

The primary goal of an Iron Condor is to collect the net premium from the difference between the sold and bought options. This strategy is most profitable when the underlying asset’s price stays within the range of the strike prices of the short options until expiration, allowing all options to expire worthless and the trader to keep the entire premium.

Risk and Rewards

- Maximum Profit: Limited to the net premium received when entering the trade. This occurs if the underlying asset’s price is between the strike prices of the short call and put options at expiration.

- Maximum Loss: Occurs if the price of the underlying asset moves significantly beyond either range, limited to the difference between the strike prices of the long and short options in one spread, minus the net premium received. The presence of long options prevents unlimited losses.

Break-Even Points: Calculated by adding and subtracting the net premium received to/from the strike prices of the short options. These points define the range within which the strategy can still be profitable.

The payout diagram, which resembles the body and wings of a big bird, gives rise to the moniker “iron condor.” An iron condor helps to clearly delineate the profit and loss sectors. The entire credit is realized as a profit at expiration if the price closes between the two short strike prices.

The maximum loss will be incurred at expiration if the underlying price is above or below one of the long strike prices. The total credit received, above or below the short options, determines the break-even points.

The break-even price, for instance, will be $2.00 above the short call strike and $2.00 below the short put strike if an iron condor is opened for a $2.00 credit.

There may be opportunities to end the position for a profit at any point prior to expiration, either by buying back only the short options or by selling the entire position or just one spread. The method will be beneficial if the options are bought for less money than they were sold for.