The equity markets this week, and in the coming week, are influenced by earnings reports. Geopolitical tensions still persist, and inflation reports have also been released this week. However, it’s worth noting that all of these factors will be covered in our weekly report on Monday. For now, let’s take a look at yesterday’s events and the potential direction for today’s markets

Economic Events:

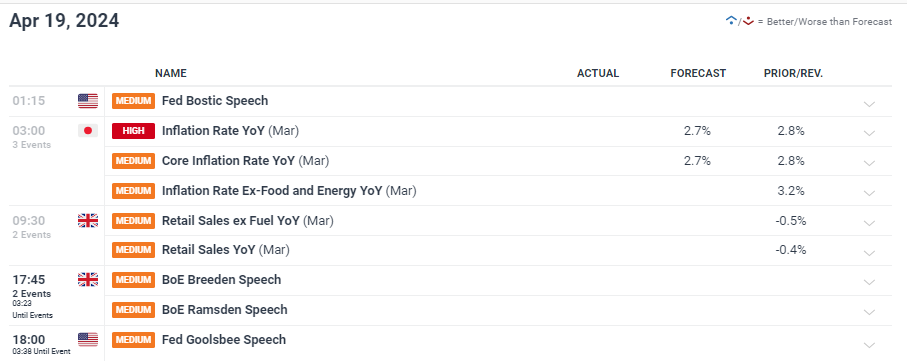

Yesterday’s most important economic data came from Australia’s employment figures, which showed an increase in the unemployment rate, albeit lower than market pricing and expectations. On the other hand, the US initial jobless claims data remained unchanged from the previous reading. Looking at today’s relatively quiet economic calendar, the most significant release was Japan’s inflation data, which came in at 2.6%. While Japan is not far from its inflation target of 1.5% to 2%, wage growth in the country may continue to support its economic momentum. Currently, the USD/JPY exchange rate has reached the 155 range, putting significant pressure on the country’s industry and economy. Additionally, noteworthy events include speeches by officials from the Federal Reserve and the Bank of England (BOE).

Source : Dailyfx

Earnings:

Yesterday, after the market closed, Netflix reported earnings that were significantly higher than market expectations. With an EPS of 5.28 compared to the market’s forecast of 4.51 and a revenue of $9.37 billion, Netflix posted very strong earnings. Netflix’s streaming platform has extensive applications in the media industry, and it continues to innovate with new series and attract more subscribers. You can see Netflix’s price chart. However, it should be noted that geopolitical tensions and capital outflows from risky markets on one hand, and dollar pricing on the other, have initiated a correction in the stock market, to which Netflix has not been immune.

The most important earnings reports scheduled for today belong to American Express and Procter & Gamble, which were released before the market opened. Both companies saw an increase in their EPS figures, but Procter & Gamble reported revenue slightly lower than market expectations.

Source : EarningWhispers

Gold (XAUUSD):

Gold behaved exactly as outlined in the previous report ( read here ) yesterday and up until before the US market opening today. The positive movement of gold towards the $2415 range was influenced by Israel’s attack on an Iranian airbase in Isfahan, which was followed by Iran’s statement indicating a willingness to de-escalate the conflict. However, it can be said that tensions are expected to decrease from now on, and gold may experience some corrective movement due to the reduction in inflation resulting from central bank monetary policies. Nevertheless, the ongoing conflict between Russia and Ukraine remains a factor, and any new developments such as Russian President Putin’s use of nuclear bombs could once again lead to an increase in gold prices.

S&P500:

The S&P experienced a positive move after the market opened yesterday, but as soon as it reached the Point of Control (POC) range, where significant trading had occurred, it was completely rejected. Following Israel’s attack on Iran last night, Tehran time, it experienced a 2.70% decline. However, with the start of the Asian trading session, it covered most of that decline. For now, the stock market trend is negative, and any positive movement could present a good selling opportunity for entering short positions.

Foreign Exchange Market (FOREX):

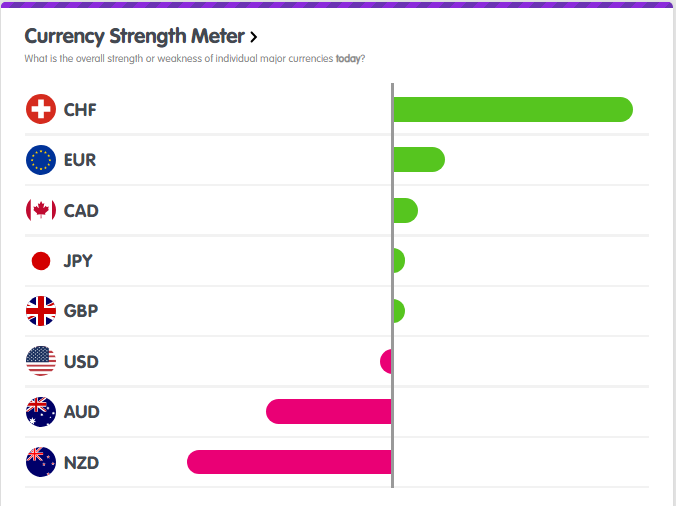

The forex market had a calm day yesterday. Among the major currencies, the Swiss franc was perceived as the strongest currency in the past 24 hours, while the New Zealand dollar was seen as the weakest fiat currency. This currency strength chart reflects some risk aversion in the market, but it seems that the opening of the US market could bring significant changes to this chart.

Source : Babypips

Bitcoin (BTC):

For Bitcoin, it can be said that all eyes are now on the halving event, especially with reduced geopolitical tensions. The decrease in miners’ income poses a significant risk to the network. With the rise in energy prices and the reduction in miner rewards, there is a possibility that many miners may exit the network, leading to a decrease in hash rate and, consequently, a drop in prices. However, the reduction in miner rewards also means a decrease in Bitcoin supply, which could lead to price growth. In the weekly report, we will delve into the possibilities and scenarios, but for today, the range of 66861 is designated as the resistance level, while the range of 63500 is considered as the support level.

US Crude Oil WTI :

Oil follows a similar chart pattern to gold, experiencing a positive movement after last night’s Israeli attack on Iran but quickly retracing its gains. While gold has been priced high due to Middle East tensions, the replenishment of US oil reserves means that further reductions in Saudi Arabia’s supply will not have a significant impact. For oil, the current scenario is bearish. However, in terms of risk to reward, it is not currently recommended as an asset.

Today’s Outlook :

For today’s US trading session, the last trading day of this week, Bitcoin seems poised to move higher. Oil is expected to have a neutral movement, while the stock market is considered to have a positive wave as a correction. Gold has negative momentum, and the reduction in tensions will not affect it much. In the forex market, the Swiss franc may continue to strengthen for now. However, the main focus is on the Aussie and Kiwi, as they have shown positive movements in the past two months, but with the release of employment data and purchasing managers’ index data, we can expect them to close the week on a negative note.

Disclaimer: The views and opinions expressed in the blog posts on this website are those of the respective authors and do not necessarily reflect the official policy or position of Meta Trading Club Inc. The content provided in these blog posts is for informational purposes only and should not be considered as financial advice. Readers are encouraged to conduct their own research and consult with a qualified financial advisor before making any investment decisions. Meta Trading Club Inc shall not be held liable for any losses or damages arising from the use of information presented in the blog posts.