The “Greeks” are crucial resources for options traders since they show how sensitive an option’s price is to different variables. Each Greek helps traders better manage risk by calculating the effect of a distinct market variable on the price of an option. Let’s examine each in turn:

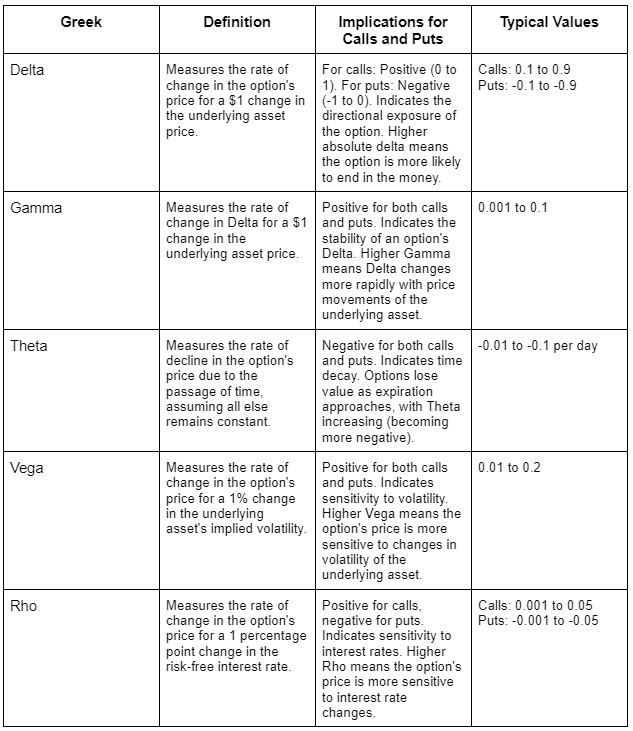

Delta (Δ)

Definition: Delta calculates how sensitive an option’s price is to a $1 shift in the underlying asset’s price. It is expressed as the difference between the option’s price and the underlying asset’s price change by one unit.

Use: Delta can be used to predict how much the price of an option will fluctuate in response to changes in the price of the underlying asset. Given that call options contain positive deltas (between 0 and 1), their values rise in tandem with the price of the underlying asset. Because put options have negative deltas, or values between -1 and 0, their value rises as the value of the underlying asset falls.

Gamma (Γ)

Definition: The rate of change in delta for a $1 change in the price of the underlying asset is measured by gamma. It shows how the delta will alter in response to changes in the underlying price.

Use: grasp the stability of an option’s delta requires a grasp of gamma. A high gamma signifies that the delta is extremely susceptible to variations in the price of the underlying asset, potentially resulting in notable fluctuations in the option’s price.

Theta (Θ)

Definition: Theta, often called time decay, is a measurement of the rate at which the value of an option decreases with the passage of time. It is shown as the price change of the option for a one-day reduction in the remaining time to expiration.

Use: Because theta shows how much an option loses in value every day as it gets closer to expiration, it is essential knowledge for options sellers (writers). As the expiration date draws closer, the pace at which options lose value increases.

Vega (𝜈)

Definition: Vega is a metric used to quantify how sensitive an option’s price is to variations in the underlying asset’s volatility. It is shown as the price change of the option for a 1% change in the implied volatility.

Use: Because it allows traders to predict how much an option’s price may fluctuate in response to changes in market volatility, Vega is important in volatile markets. In situations where volatility is high, options are typically more valuable.

Rho (Ρ)

Definition: Rho is a metric that quantifies how sensitive the price of an option is to changes in interest rates. It is expressed as the difference between the option’s price and the interest rate change of one percentage point.

Use: Since interest rates have a more noticeable impact over longer time horizons, Rho is more pertinent for longer-term choices. In situations when changes in interest rates are anticipated, it is crucial to take this into account.

Applying the Greeks

Risk management: Traders can more effectively control the risks connected to their options holdings by knowing the Greeks. To become market-neutral, an options portfolio can be hedged using delta (a process known as delta hedging).

Making Strategic Decisions: By exposing an option’s potential sensitivity to changes in the market, the Greeks can help with strategic decision-making, including choosing strike prices and expiration dates.

Meta Trading Club is a leading educational platform dedicated to teaching individuals how to trade and invest independently. Through comprehensive educational programs, personalized mentorship, and a supportive community, Meta Trading Club empowers traders to navigate financial markets with confidence and expertise.