What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

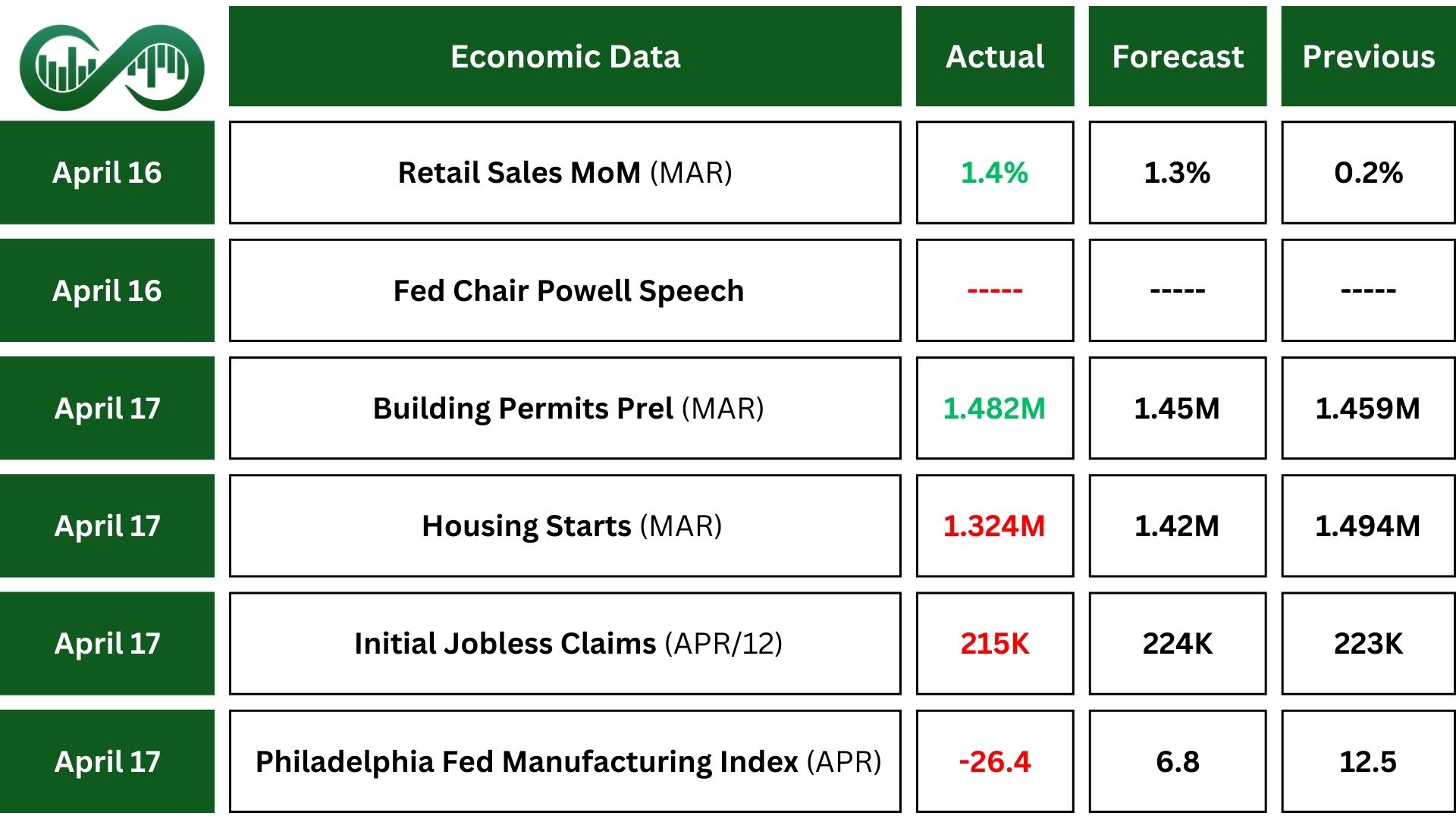

U.S. retail sales increased by 1.4% in March, the largest growth in over two years and surpassing expectations of 1.3%. The surge was primarily driven by a 5.3% rise in car and car part sales as buyers rushed purchases ahead of new tariffs. Excluding car sales, retail sales still grew by 0.5%, highlighting broader market strength.

Chair Powell highlighted slowing GDP growth in Q1, modest consumer spending, and strong vehicle sales, while imports rose as businesses prepared for tariffs, impacting growth.

He stated that consumer and business confidence are declining due to trade concerns. The labor market is stable unemployment, though wage growth is moderating but remains above inflation. Tariffs contributing to rising inflationary expectations.

Powell emphasized that no immediate policy changes are planned as the Fed awaits more clarity which led to a market drop.

Initial jobless claims in the U.S. dropped by 9,000 to 215,000 in mid-April, showing a strong labor market despite volatility in continuing claims, which rose to 1.885 million.

Building permits increased by 1.6% in March, exceeding expectations, while housing starts fell sharply by 11.4% due to weak demand, high prices, and elevated mortgage rates.

The Philadelphia Fed Manufacturing Index fell sharply to -26.4 in April from 12.5 in March, marking the largest drop since April 2023 and missing expectations.

Business activity decreased for 39% of firms, while 13% saw improvements, and 41% reported no change. The new orders index plunged to -34.2, its lowest since April 2020, and shipments declined to -9.1. Employment levels remained stable, while prices continued to rise. Growth prospects for the next six months remain weak.

Earnings Reports

Goldman Sachs

Goldman Sachs (GS) reported strong Q1 earnings, with net revenues of $15.06 billion, up 6% year-over-year. Its earnings per share (EPS) of $14.12 surpassed forecasts.

This results driven by record revenue in equities and fixed-income trading within its Global Banking & Markets division. While Asset & Wealth Management revenues slightly declined, the firm achieved record assets under supervision, reinforcing its position in the financial sector.

Bank of America

Bank of America (BAC) delivered impressive Q1 results, posting $7.4 billion in net income and an EPS of $0.90, exceeding expectations.

Revenue grew by 6% year-over-year to $27.4 billion, supported by higher net interest income and strong stock trading.

Consumer banking and wealth management also contributed positively, with deposits continuing their growth streak to nearly $2 trillion.

UnitedHealth

UnitedHealth (UNH) Q1 report highlighted a revenue increase of 9.8% year-over-year to $109.6 billion, but adjusted EPS of $7.20 fell slightly below forecasts.

The company faced challenges in Medicare Advantage plans, prompting a downward revision in its annual profit guidance. This led to a 24% drop in stock last week.

Netflix

Netflix (NFLX) delivered solid performance, with revenue growing 13% year-over-year to $10.54 billion and EPS of $6.61, exceeding expectations.

The company emphasized its focus on financial metrics rather than subscriber counts, highlighting growth in its ad-supported tiers.

Improved operating margins of 31.7% demonstrated strong financial health and investor confidence in the streaming giant.

Taiwan Semiconductor Manufacturing

U.S.-listed shares of Taiwan Semiconductor Manufacturing (TSM) reported a 60% increase in Q1 profits and said tariffs haven’t impacted them yet.

TSMC expects strong demand for its advanced 3nm and 5nm technologies to boost business in Q2 2025 but warned that tariff risks could still pose a challenge, even though customer behavior remains unchanged for now.

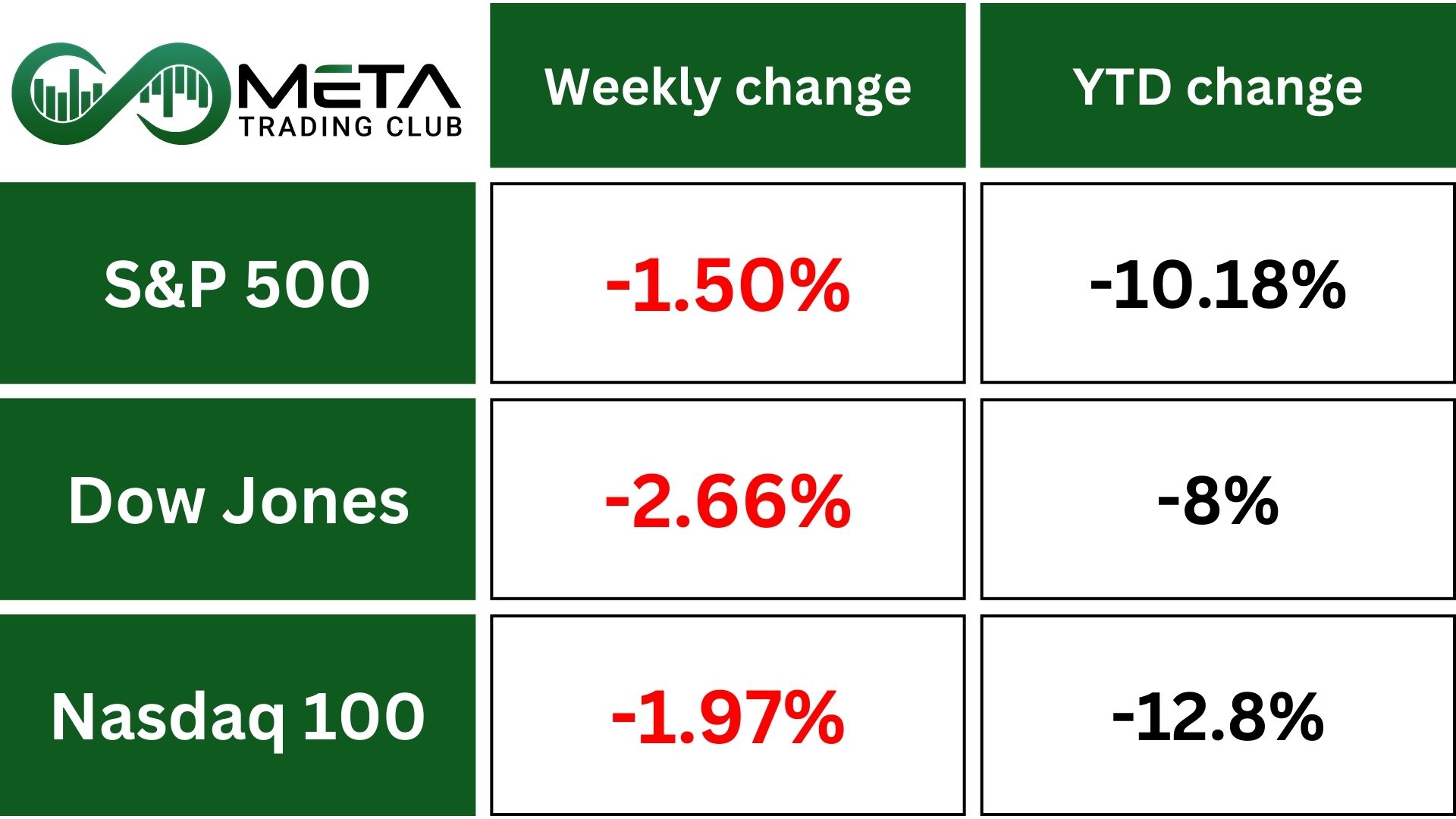

Indices

Indices’ Weekly Performance:

Wall Street had a chaotic, shortened week filled with tariffs, chip stock struggles, and political drama. The S&P 500 ended the week down 2.7%. Optimism faded as concerns over tariffs and geopolitical tensions pushed traders away from riskier assets. Tech stocks, especially Nvidia, dropped and dragging the market down further.

In the final hours of trading, reports emerged that President Trump was considering removing Fed Chair Jay Powell, criticizing him for being “too late and wrong” on interest rates. This added to market uncertainty.

Looking ahead, earnings season is heating up, with Tesla and Alphabet set to release key quarterly reports.

Stocks

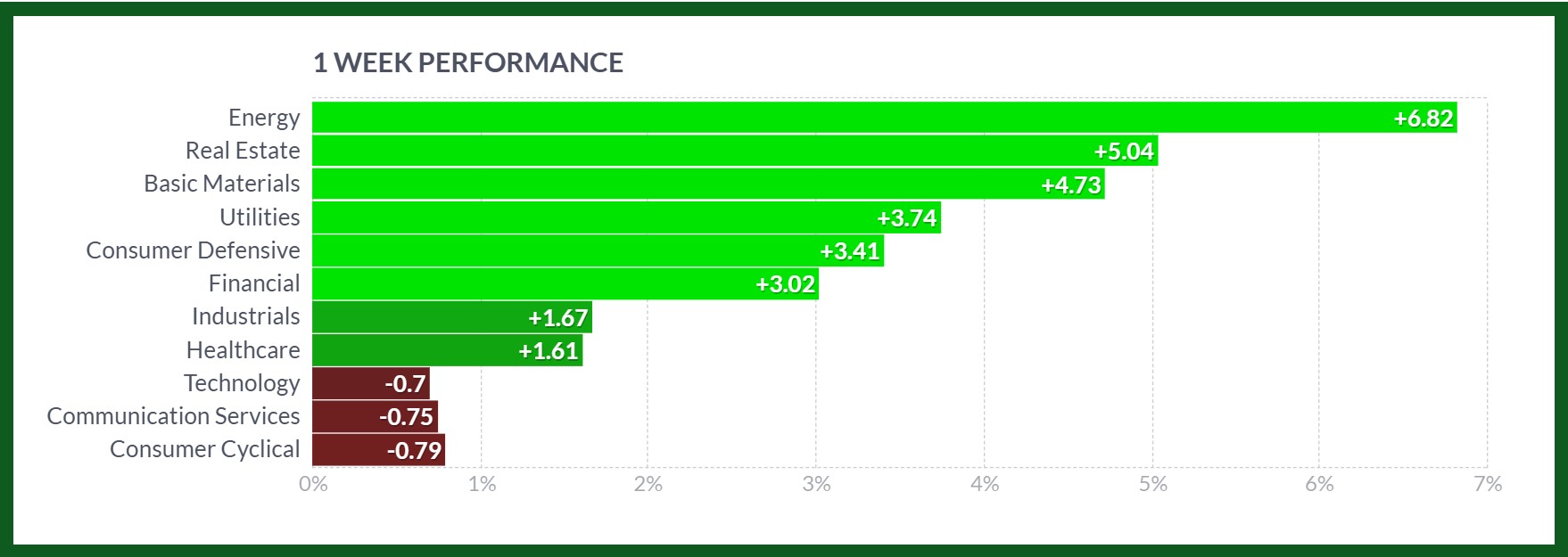

Sector’s Weekly Performance:

Source: Finviz

Last week, only a few sectors suffered losses. Technology, Consumer Discretionary, and Communication Services were hit the hardest, while Energy and defensive sectors remained strong.

- Energy: Surged 6.8% due to U.S. sanctions on Iranian oil exports, increasing supply concerns and boosting prices.

- Real Estate: Rose 5% as real estate kicked off the earnings season on a strong note, driven by standout performance from Prologis.

- Basic Materials: Gained 4.7%, driven by higher commodity prices and renewed industrial activity.

- Utilities: Increased 3.7%, benefiting from stable demand and investor preference for defensive assets.

- Financials: Climbed 3%, with strong earnings from major banks like Goldman Sachs and Bank of America highlighting increased net interest income and trading revenues. KBW Regional Banking Index rose 5%.

- Healthcare: Nudged up 1.1%, with Eli Lilly jumping 15% after its weight-loss drug showed success in trials, while UnitedHealth (UNH) plunged due to a cut in its profit forecast.

- Technology: Declined 0.7%, with Nvidia and AMD hit by regulatory and export issues. However, gains in Apple and Intel provided some relief.

- Communication Services: Dropped 0.75%, with Alphabet falling after a U.S. judge ruled against its ad tech practices. Alphabet faced setbacks from monopoly allegations

Stock Market Weekly Performance:

Source: Finviz

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Eli Lilly and Company (LLY): Surged 14.8% due to positive results from its experimental weight-loss pill in late-stage trials, rivaling Novo Nordisk’s Ozempic, which fueled investor optimism and boosted the stock significantly.

- Prologis (PLD): Rose 6% as delivered better-than-expected Q1 earnings and revenue, reaffirmed its 2025 earnings guidance, and maintained confidence despite lowering expectations for dispositions and development starts.

- Philip Morris (PM): Gained 6% following strong performance in global sales and potential shifts in regulatory policies supporting the tobacco industry.

- Netflix (NFLX): Increased 6% after gaining momentum due to posting strong earnings and positive growth expectations, signaling robust subscriber trends.

- Palantir (PLTR): Advanced 5.9% after experiencing optimism in the market for its artificial intelligence and data analytics capabilities.

- MicroStrategy (MSTR): Surged 5.7% due to market optimism on the crypto portfolio owned by the company.

- Realty Income (O): Jumped 5.6% as strong quarterly results supporting growth outlook.

Action Point

MicroStrategy (MSTR) has approached its downtrend line. A strong breakout with momentum could signal a further surge, but rejection from this level may lead to a decline toward lower support.

Palantir (PLTR) encountered resistance at the $98 level. A breakout above this resistance with increasing momentum could result in a price surge. However, if the stock is rejected at this level with weakening momentum, a decline toward the $75 support level is possible.

Tesla (TSLA) is set to release its earnings this week and is currently in a consolidation phase. If the stock manages to break its short-term downtrend line, further gains could be expected. However, if the earnings report falls short of expectations, it might break the strong support level at $212, potentially leading to a deeper decline. Keep an eye on the stock’s price movements around this critical support zone.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold (XAUUSD) has been the standout asset this year, significantly outperforming stocks, crypto, and the dollar. It surged to a record-breaking $3,290 per ounce, driven by escalating trade tensions between the US and China. These tensions have hurt global economic growth prospects, leading investors to move away from riskier assets and into the safety of gold.

As a result, gold has gained over 25% year-to-date, adding more than $4 trillion in market value, making the gold market worth approximately $21 trillion. In stark contrast, the S&P 500 has lost around 8%, Bitcoin is down 10%, and the US dollar index has fallen 8%.

Crude oil prices jumped last week, driven by reduced tariff concerns and optimism about potential U.S. trade deals with Japan and the EU. However, doubts about lifting U.S. export restrictions on Iranian crude, coupled with stalled nuclear talks, pushed prices higher as supply worries persisted.

China’s increased crude imports in March, reaching 12.1 million bpd, also supported prices. On the other hand, Goldman Sachs highlighted concerns about surplus crude due to the trade war and higher production, predicting a global surplus in 2025 and 2026.

Forex

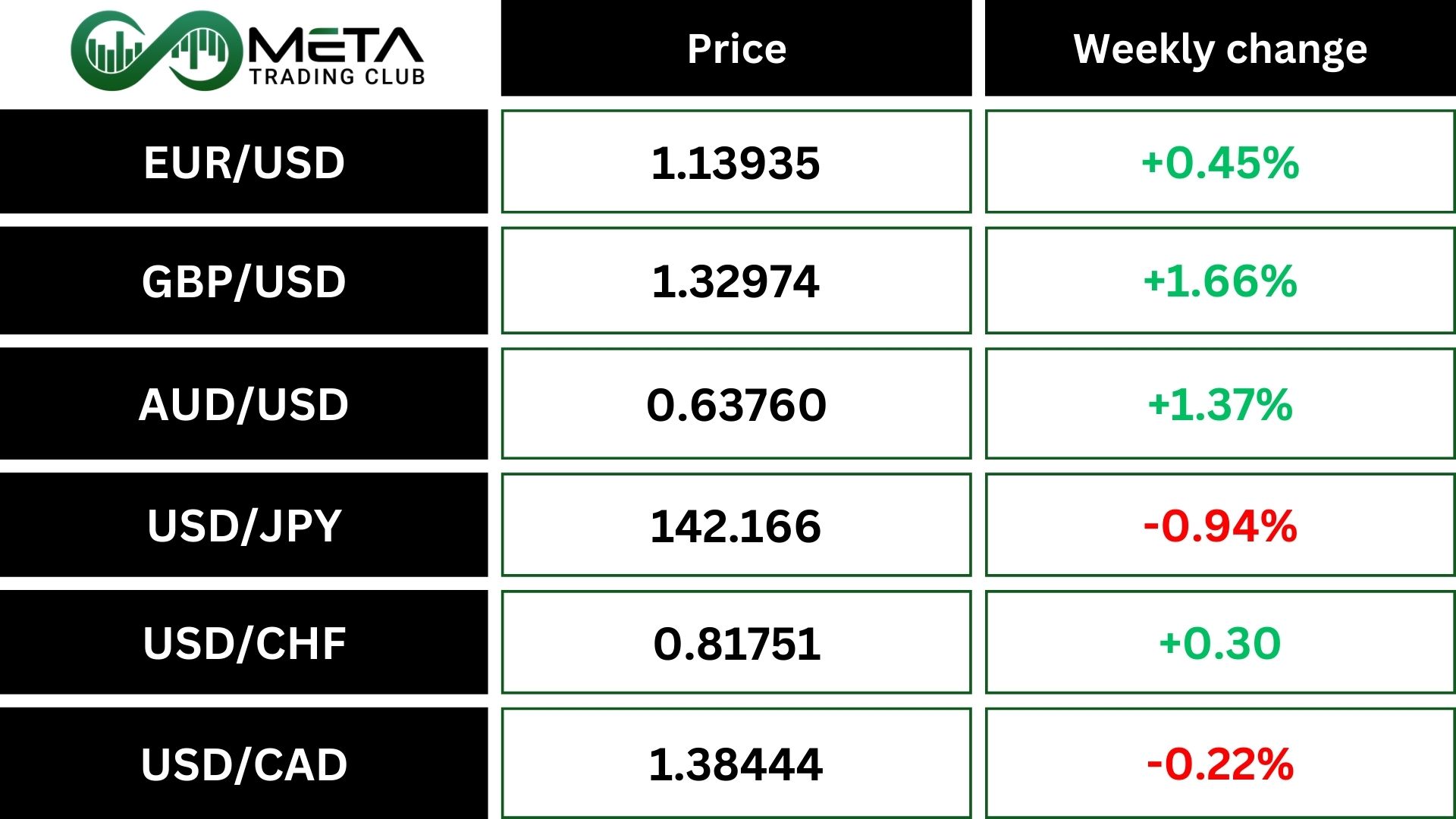

Weekly Performance of Major Foreign Exchange Pairs:

The U.S. dollar (DXY) regained strength last week after a period of weakness, while the euro dipped following the ECB’s seventh rate cut in a year. The dollar stabilized after previous sharp drops caused by tariff concerns and overseas investment shifts.

The GBPUSD pair is on a strong streak, rising last week. Sterling has gained over 4.5% during this period, while the dollar continues to lose ground against other currencies.

The Japanese yen has gained nearly 10% against the US dollar this year, with recent tariff concerns adding to its strength.

Crypto

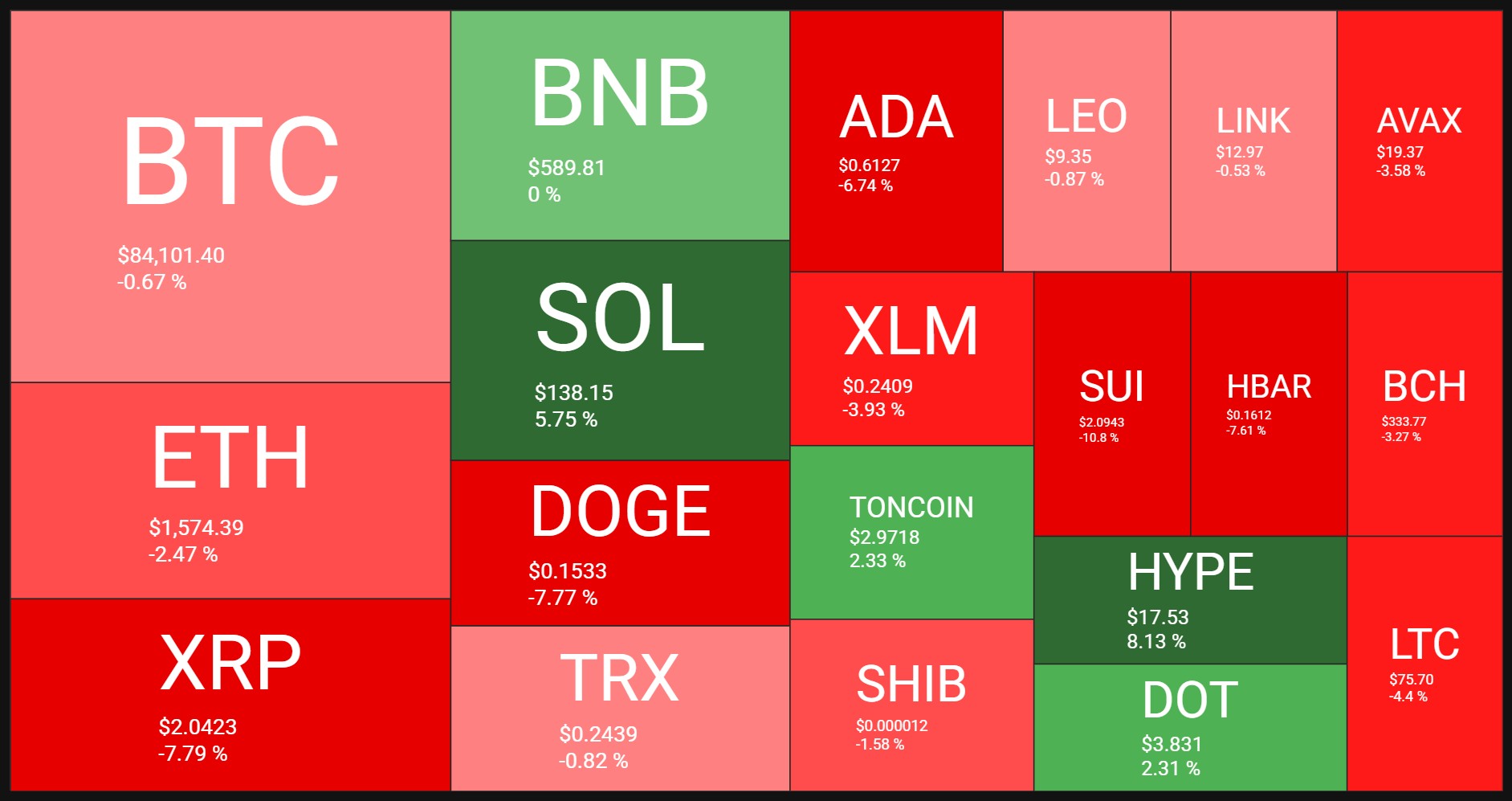

Crypto Market Weekly Performance:

Source: QuantifyCrypto

Bitcoin (BTCUSD) bounced back 14.6% after dropping below $75,000 in April, its lowest in five months. But struggles to break the $85,000 resistance level are raising worries about a possible bull trap.

Technically, if Bitcoin can reverse the downward momentum on the weekly RSI and break above the $85,000 resistance level with confirmation, a potential future decline might be avoided. However, if the lack of momentum continues, the coin could face rejection at the trendline and may fall to lower support levels.

Ethereum is undergoing significant changes to address challenges and adapt to competition. After facing leadership issues and developer departures earlier this year, it remains a top network for DeFi, stablecoins, tokenization, and decentralized apps.

Technically, ETH has reached a critical support zone at $1,500 and is currently in oversold territory on weekly time frames. If bullish momentum emerges, the crypto has the potential to bounce back from this level. However, if the $1,500 support is lost, further declines toward lower support zones may be expected.

Next Week’s Outlook

Economic Events

This week, investors will pay attention to speeches from Fed officials like Philip Jefferson, Adriana Kugler, Christopher Waller, Patrick Harker, and Austan Goolsbee.

Markets will keep an eye on potential changes in US tariff policy, including possible retaliation to Asian protectionism and signs of trade deals by President Trump.

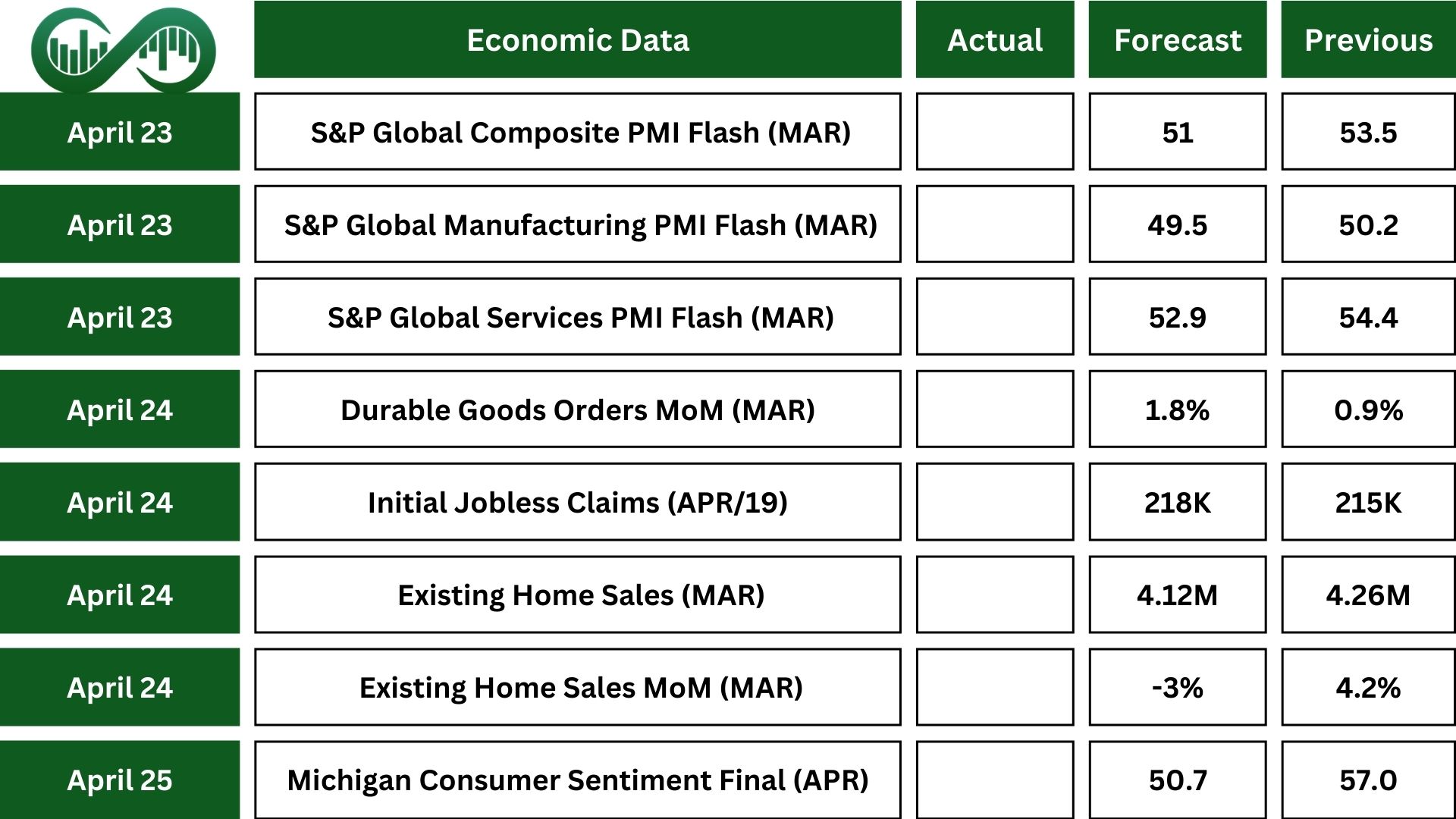

The US economic calendar will be fairly quiet. March’s durable goods orders are expected to rise for the third month in a row, while existing home sales may decline.

Additionally, the flash S&P Global PMI survey for April will provide insights into the impact of tariff threats on businesses.

Other reports include the Chicago Fed National Activity Index and the final reading of the University of Michigan Consumer Sentiment Index.

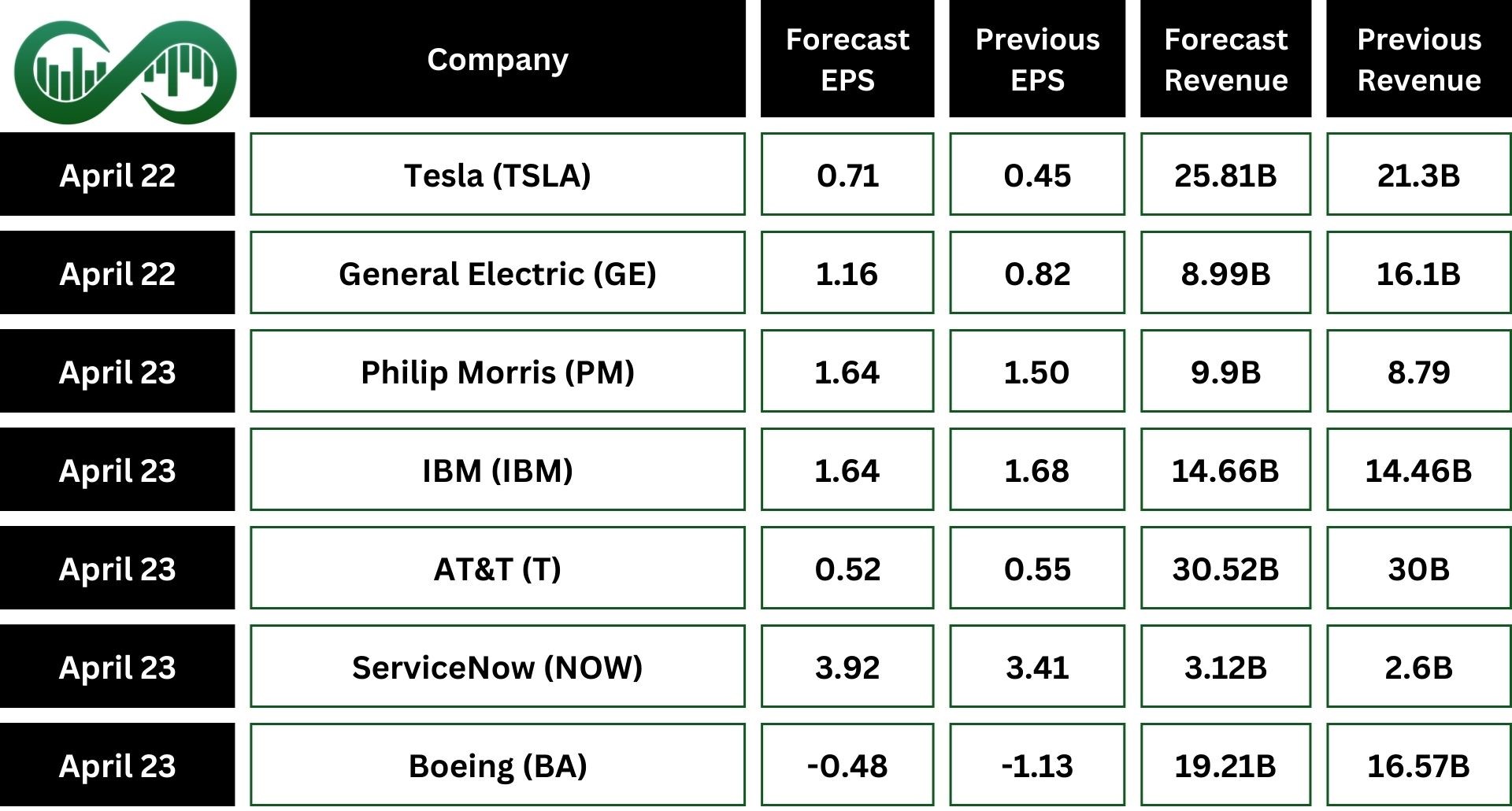

Earnings Events

This week, the earnings season picks up steam. It starts with Tesla (TSLA) much-awaited report on Tuesday, followed by updates from big companies like Alphabet (GOOGL), Procter & Gamble (PG), PepsiCo (PEP), Intel (INTC), Boeing (BA), Merck (MRK), Philip Morris (PM), IBM (IBM), AT&T (T), Verizon (VZ), T-Mobile (TMUS), ServiceNow (NOW), AbbVie (ABBV) and CME Group (CME).