What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

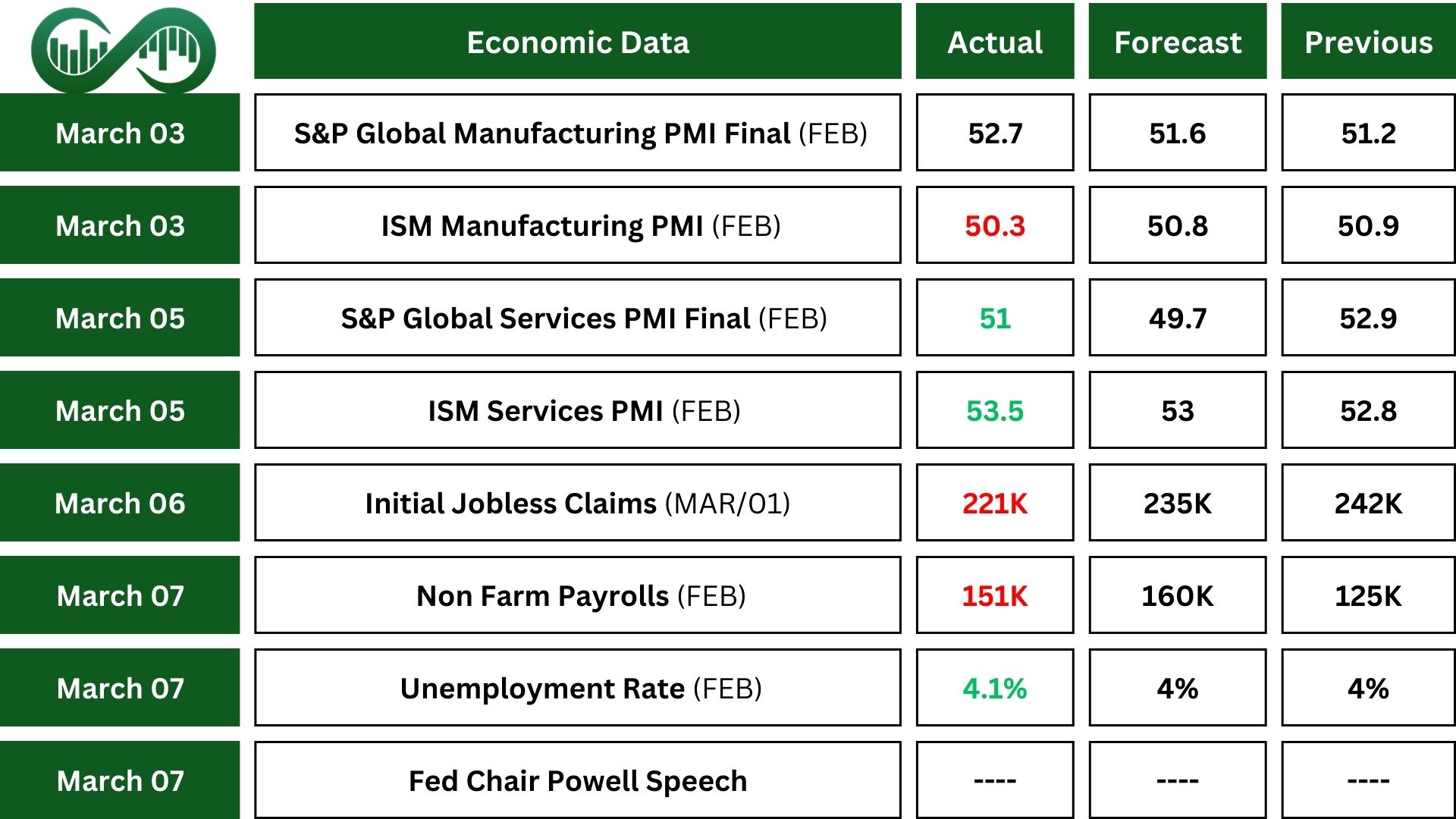

The ISM Manufacturing PMI fell to 50.3 in February. This signals slower manufacturing growth, with reduced demand, stable production, and ongoing job cuts. New tariffs caused higher prices, order delays, supply disruptions, and inventory challenges.

Meanwhile, the ISM Services PMI rose to 53.5, showing faster growth in services, with improvements in new orders, employment, and inventories, though price pressures increased. Despite this growth, concerns remain about the impact of tariffs and federal spending cuts on business forecasts.

Initial jobless claims dropped by 21K to 221K in late February, but continuing claims rose to 1,897K, reflecting labor market challenges. Federal employee claims increased due to layoffs by the Department of Government Efficiency (DOGE). Employers announced 172,017 job cuts in February, the highest since 2009, driven by DOGE actions, trade fears, and bankruptcies. Government, retail, and tech sectors led the cuts.

The US added 151K Non-Farm Payrolls in February, below the forecast. Growth was strong in health care, financial activities, and transportation, but federal jobs fell by 10K due to DOGE layoffs. Hourly earnings for private nonfarm and production workers both increased by 0.3%.

The unemployment rate rose to 4.1%, with 7.05 million unemployed and employment dropping by 588,000. The labor force participation rate fell to 62.4%, and the broader U-6 unemployment rate climbed to 8%.

Fed Chair Powell acknowledged potential slowdowns in spending and business uncertainty but emphasized strong economic indicators, inflation progress, and steady job gains. His positive outlook reassured investors, boosting the market, despite concerns about an economic slowdown and expectations of three Fed rate cuts by year-end.

Earnings Reports

CrowdStrike

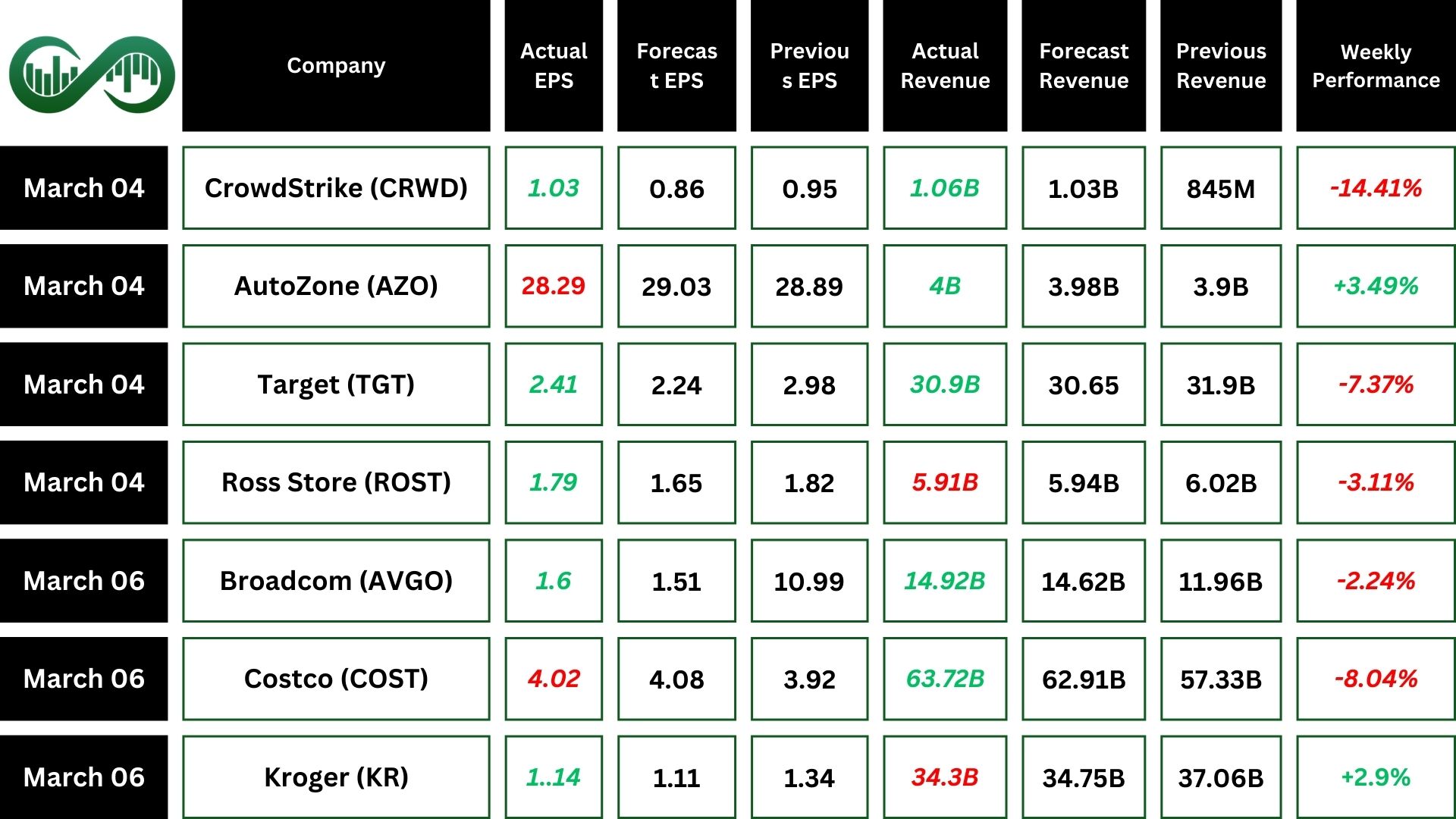

CrowdStrike (CRWD) reported a 23% rise in annual recurring revenue (ARR) to $4.24 billion and record free cash flow of $1.07 billion for fiscal 2025.

However, net new ARR fell 1% year-over-year, and Q4 saw a GAAP net loss of $92.3 million.

Growth from existing customers slowed, and $73 million in outage-related costs are expected in Q1 FY26. The stock dropped over 14% following the report, with margins under pressure due to investments and the Customer Commitment Program.

Technically, CRWD has broken the key support level at $334. If bearish signals are confirmed below this level, the price may decline further toward the next Fibonacci support zone at $300. On the other hand, if bullish signals are established above this support, the price could rebound and move higher.

Target

Target (TGT) reported a 0.8% decline in full-year 2024 net sales and a 0.9% drop in GAAP and adjusted EPS, compared to last year.

Also, in Q4 2024 comparable sales grew by 1.5%, driven by strong traffic and an 8.7% increase in digital sales. Same-day delivery rose over 25%, leading to GAAP and Adjusted EPS of $2.41, above estimates.

The company paid $513 million in dividends, repurchased $506 million in shares, and saw its after-tax return on invested capital fall to 15.4% from 16.1%.

Target’s stock fell following cautious Q1 2025 guidance, citing weak February sales, consumer uncertainty, tariffs, and inflation as key concerns.

Broadcom

Broadcom (AVGO) reported strong Q1 fiscal 2025 results, with revenue up 25% to $14.916 billion, exceeding expectations. GAAP net income was $5.503 billion, and non-GAAP net income was $7.823 billion.

The company posted GAAP EPS of $1.14 and non-GAAP EPS of $1.60, both above estimates. They generated $6.113 billion in cash from operations and $6.013 billion in free cash flow. The quarterly dividend is set at $0.59 per share.

For Q2 2025, Broadcom expects revenue of about $14.9 billion, a 19% increase from last year. This strong performance caused a 10% jump in stock price, driven by better-than-expected results and positive future guidance.

Costco

Costco (Cost) reported a 9.1% increase in Q2 fiscal 2025 net sales, reaching $62.53 billion, with net income at $1.788 billion ($4.02 per share).

February sales rose 8.8% to $19.81 billion, and the company operates 897 warehouses globally while expanding e-commerce operations.

Despite strong sales growth, lower-than-expected earnings led to a drop in stock, as investors remain concerned about rising costs and inflation’s impact on profits.

Technically, COST stock dropped following its earnings report, reaching the dynamic support level along its uptrend line. If the stock breaks below this trend line, a further decline toward the strong support level of $905 is expected.

Indices

Indices’ Weekly Performance:

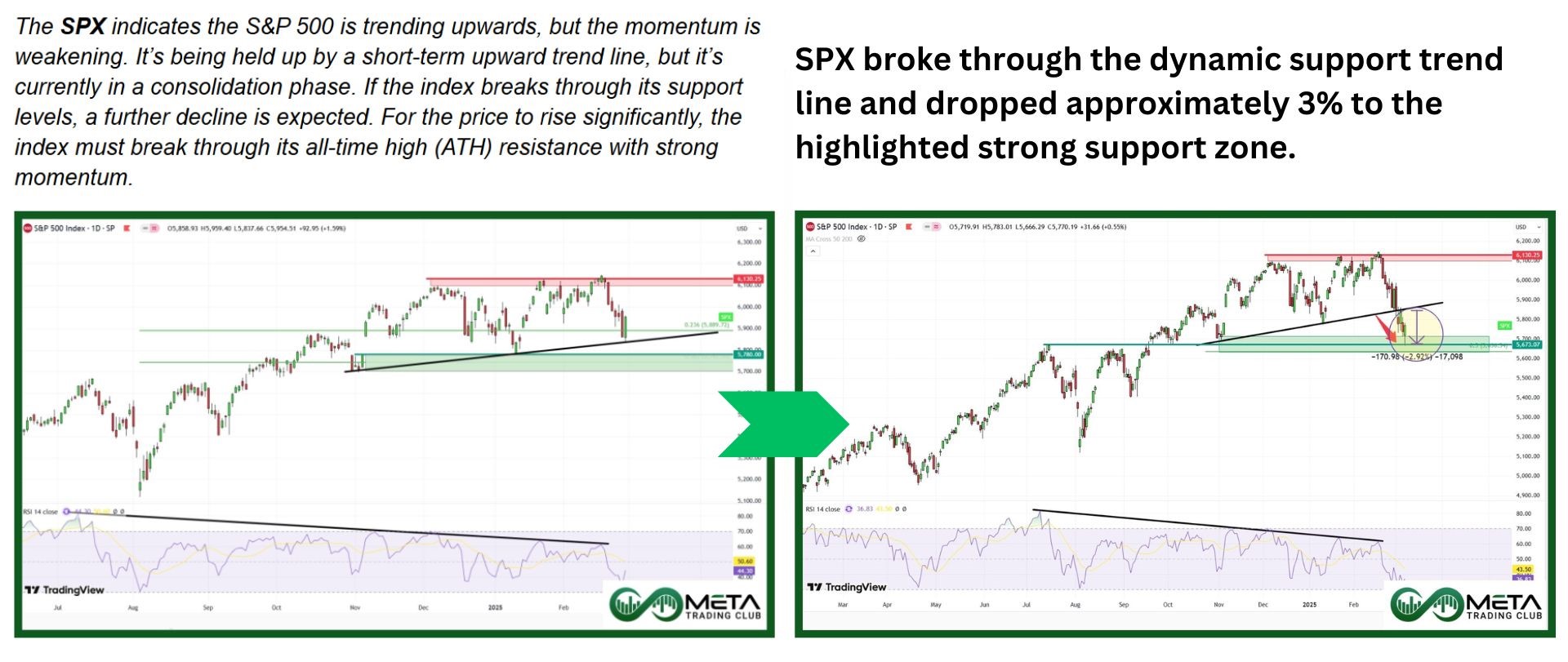

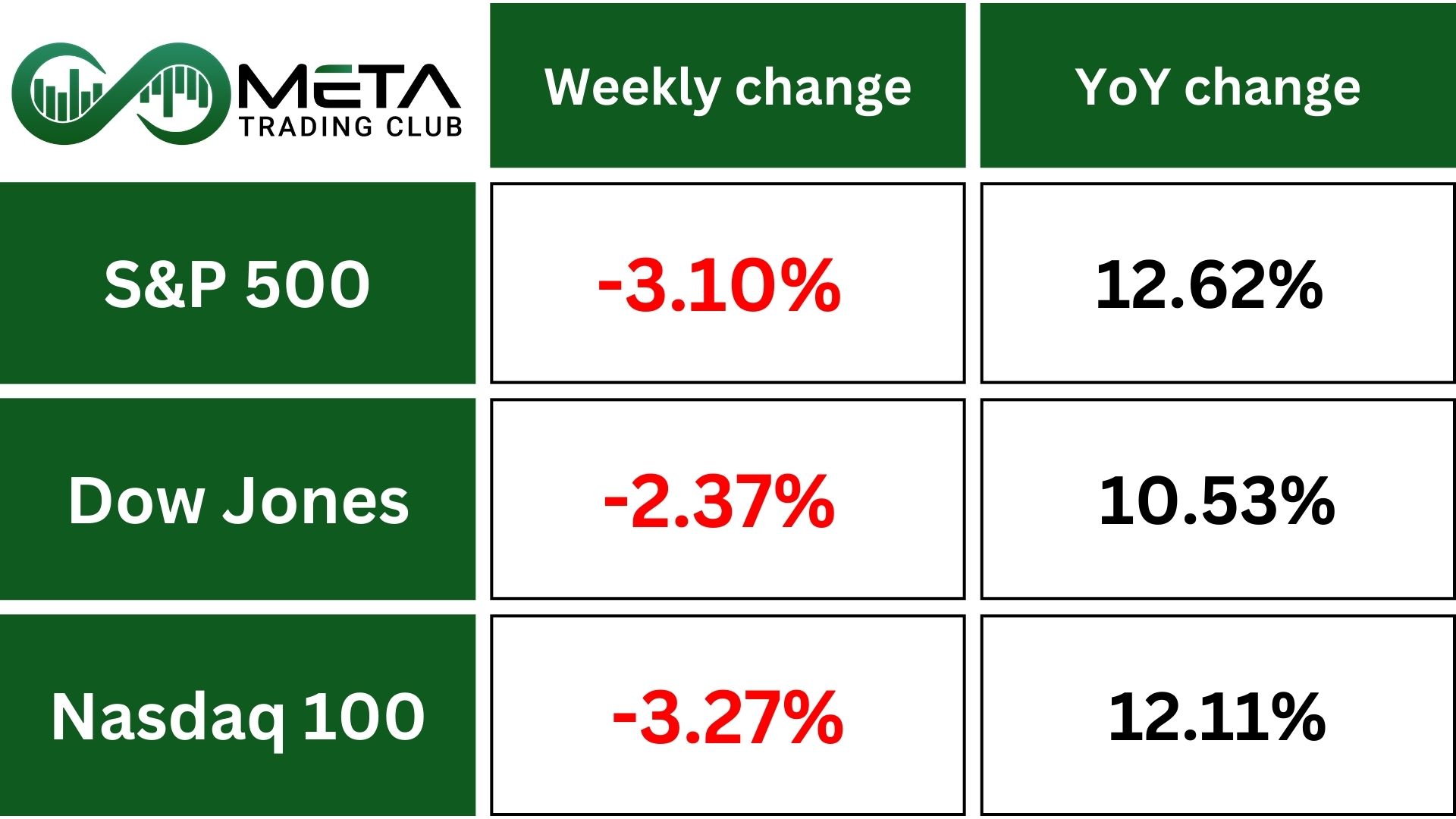

The S&P 500 (SPX) has fallen for three weeks in a row, dropping 3.1% due to trade war concerns. SPX is now 6.1% below its record high, the Dow (DJI) is 4.9% below its peak, and the Nasdaq (IXIC), which entered correction territory on Thursday, is 9.8% off its record high as of Friday.

The U.S. 10-Year Treasury yield (US10Y) is around 4.31%, possibly ending a five-week decline streak.

Despite brief dips during the week, the index bounced back by the end of Friday. The S&P 500 recovered, after Donald Trump announced a one-month delay on auto tariffs for imports from Mexico and Canada. This sparked hopes that other industries, like agriculture and food, might also get tariff relief.

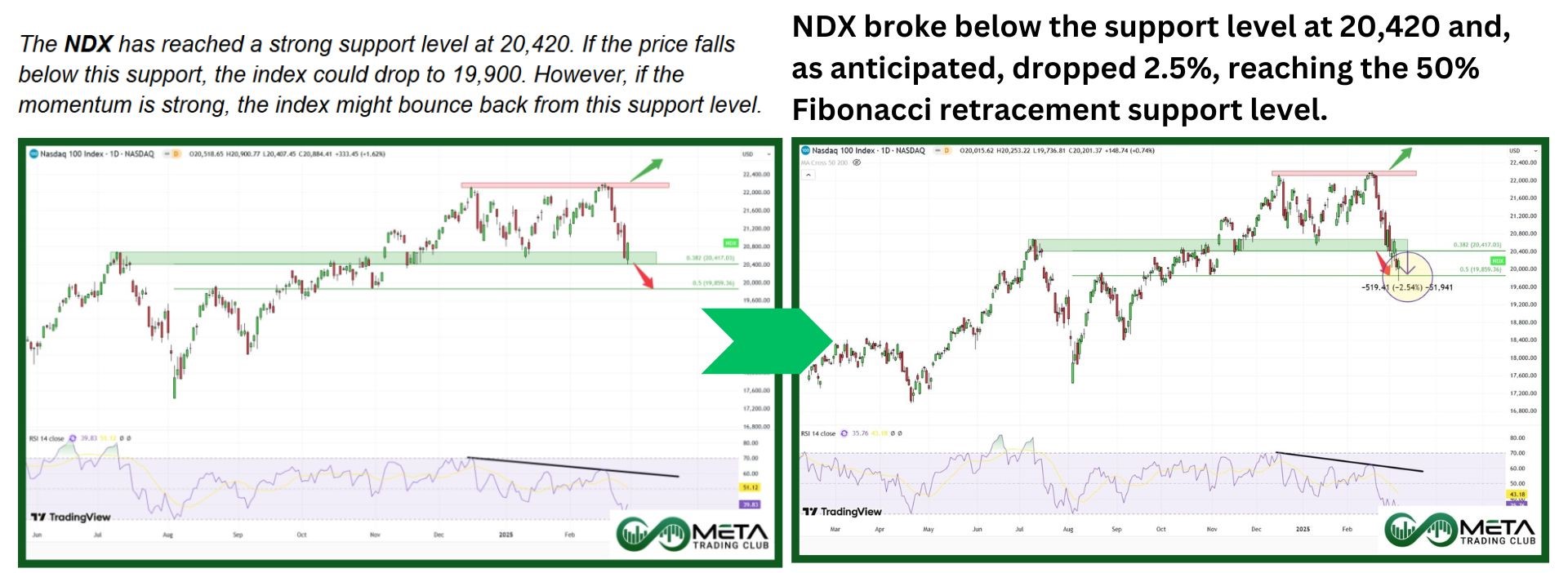

Technically, The SPX has reached a strong support zone at 5,670, which aligns with the dynamic support of the 200-day moving average. If bearish confirmations are established below this level, a further decline toward the next Fibonacci support at 5,514 is anticipated. However, if bullish confirmations emerge above this support, a pullback and potential price surge could occur.

Stocks

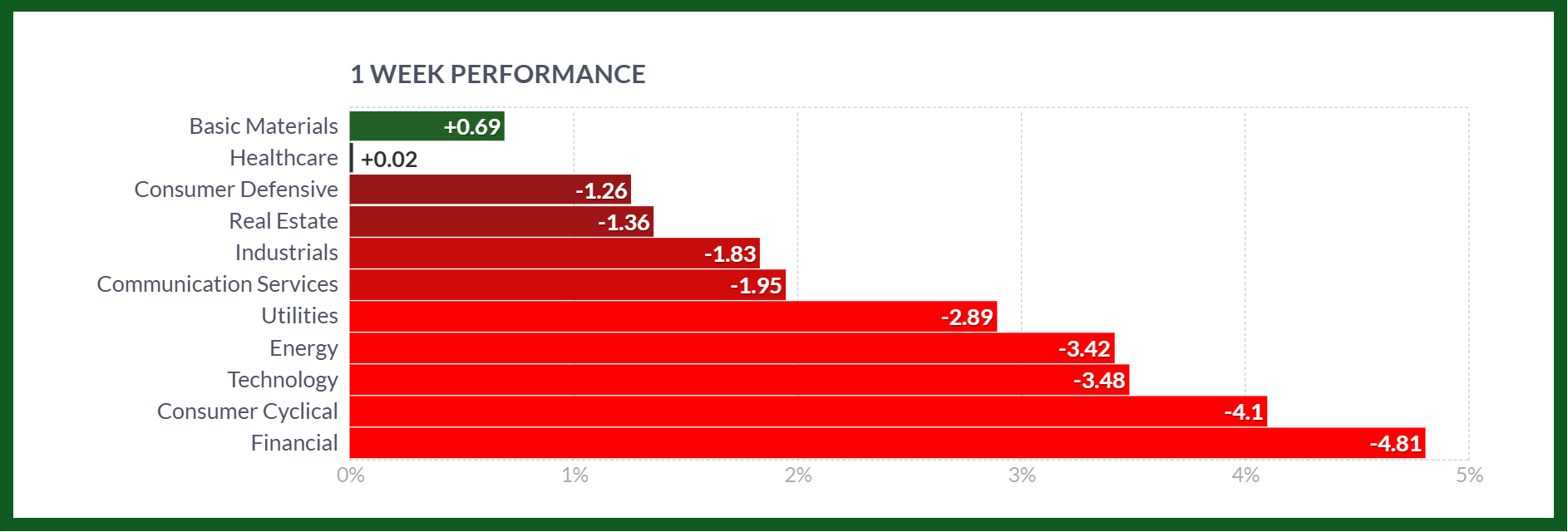

Sector’s Weekly Performance:

Source: Finviz

The first two months of 2025 were marked by uncertainty, with low volatility and momentum making early moves. Most sectors were affected: Financials and Consumer Discretionary were hit hardest, while Healthcare remained relatively stable.

- Financials dropped 4.8%, with major banks declining due to tariff concerns and economic slowdown fears. The S&P 500 banks index fell around 9%.

- Consumer Discretionary fell 4%. Best Buy (BBY) dropped after weak forecasts, and automakers like General Motors (GM) and Ford (F) faced tariff-related challenges but recovered slightly after exemptions were announced.

- Energy dipped 3.4%, impacted by U.S. crude build and OPEC+ output concerns, though it rebounded after hints of an output reversal.

- Technology declined 3.4%, with Hewlett Packard (HPE) losing 20% due to poor forecasts. Semiconductor index shed nearly 3%, despite Broadcom (AVGO) gaining briefly on positive AI chip demand news.

- Industrials fell 1.8%, though Huntington Ingalls (HII) rose on tax incentive promises.

- Consumer Staples slipped 1.2%, with Target (TGT) and Costco (COST) declining on disappointing forecasts.

- Healthcare edged up a bit, with Moderna (MRNA) gaining 15% after its CEO purchased shares.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their increase.

- MicroStrategy (MSTR): Surged 12%, driven by a rise in Bitcoin prices, as MicroStrategy holds significant Bitcoin assets.

- HCA Healthcare (HCA): Climbed 8% due to strong earnings reports and increased demand for healthcare services.

- General Dynamics (GD): Rose 8% after Trump’s address to Congress included plans for a missile defense dome, benefiting GD.

- Verizon Communications (VZ): Gained 7% after announcement that Starlink has no plans to take over any FAA telecom contract.

- Colgate-Palmolive (CL): Advanced 6% due to strong investor confidence in its fundamentals and strategic initiatives.

- PDD Holdings (PDD): Increased by 5%, driven by positive investor sentiments.

- Northrop Grumman (NOC): Gained 5% after Trump’s address to Congress included plans for a missile defense dome, benefiting NOC.

- Lockheed Martin (LMT): Rose 5% after Trump’s address to Congress included plans for a missile defense dome, benefiting LMT.

- McDonald’s (MCD): Gained 5% after McDonald’s gives its restaurants an AI makeover.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold prices rose about 2% last week, approaching record highs, as investors sought safety following weaker-than-expected U.S. jobs data. Job data showed in some sectors layoffs surged to a 2020 high, though jobless claims dropped more than anticipated.

Gold’s appeal was further supported by uncertainties in global trade policies. President Trump temporarily paused 25% tariffs on most goods from Canada and Mexico, but Canada’s retaliatory tariffs remain, and China is set to implement new trade measures next week.

Technically, gold prices may climb higher if they break through the all-time high resistance zone with strong momentum. However, if the precious metal faces rejection at the ATH, a decline toward $2,820 is expected. If this support level fails, the price could drop further, reaching the uptrend line.

WTI crude oil futures rebounded to $67.3 per barrel but are still set for a 3.3% weekly decline. Prices remain under pressure due to uncertainty over U.S. tariff policies, weakening demand, and expectations of increased oil output.

Also, OPEC+ plans to raise production in April, alongside the potential restart of the Kirkuk-Ceyhan pipeline and expanded output at Kazakhstan’s Tengiz field, adding to oversupply concerns.

Meanwhile, Canada’s retaliatory tariffs remain, and China’s countermeasures are expected next week, further impacting market sentiment.

Forex

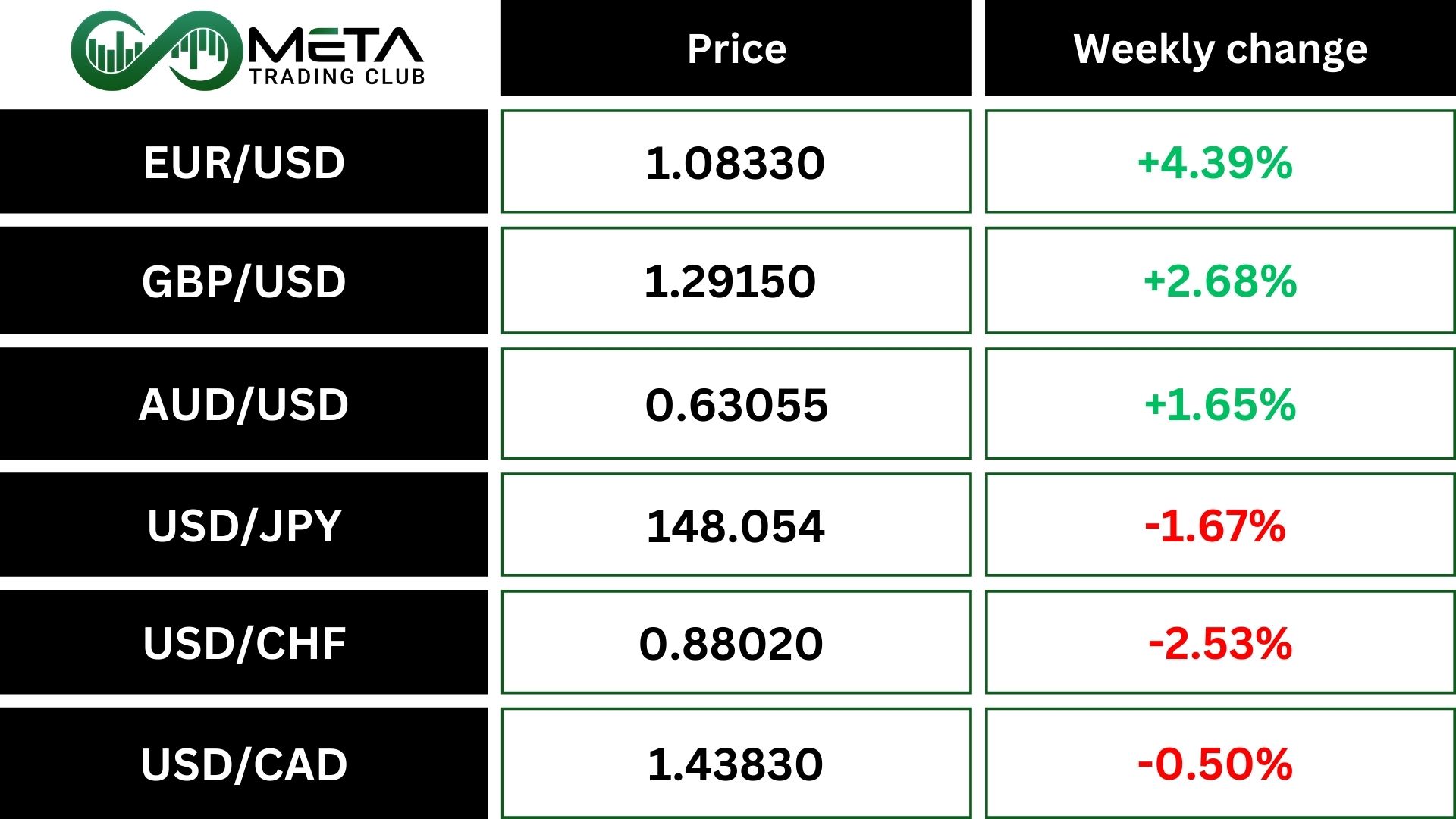

Weekly Performance of Major Foreign Exchange Pairs:

The dollar index (DXY) hit a four-month low after weaker-than-expected U.S. job growth in February but recovered slightly after comments from Federal Reserve officials, including Chair Jerome Powell.

Nonfarm payrolls rose by 151,000 (below the forecast), and the unemployment rate increased to 4.1%. Powell reassured that the U.S. economy remains stable and suggested no rush to adjust interest rates. Also, President Trump hinted at sanctions on Russia and potential tariffs on Canadian and European goods, adding to market uncertainty.

Meanwhile, the EUR/USD gained strength due to optimism about Germany’s spending plans and improved eurozone GDP growth. European Central Bank officials expressed confidence in overcoming inflation challenges.

Currency movements included GBP/USD rising slightly, limited by euro strength, and USD/JPY recovering from a five-month low after Powell’s remarks.

Key developments next week include Ukraine peace talks, German inflation data, and Japan’s trade and wage reports.

Crypto

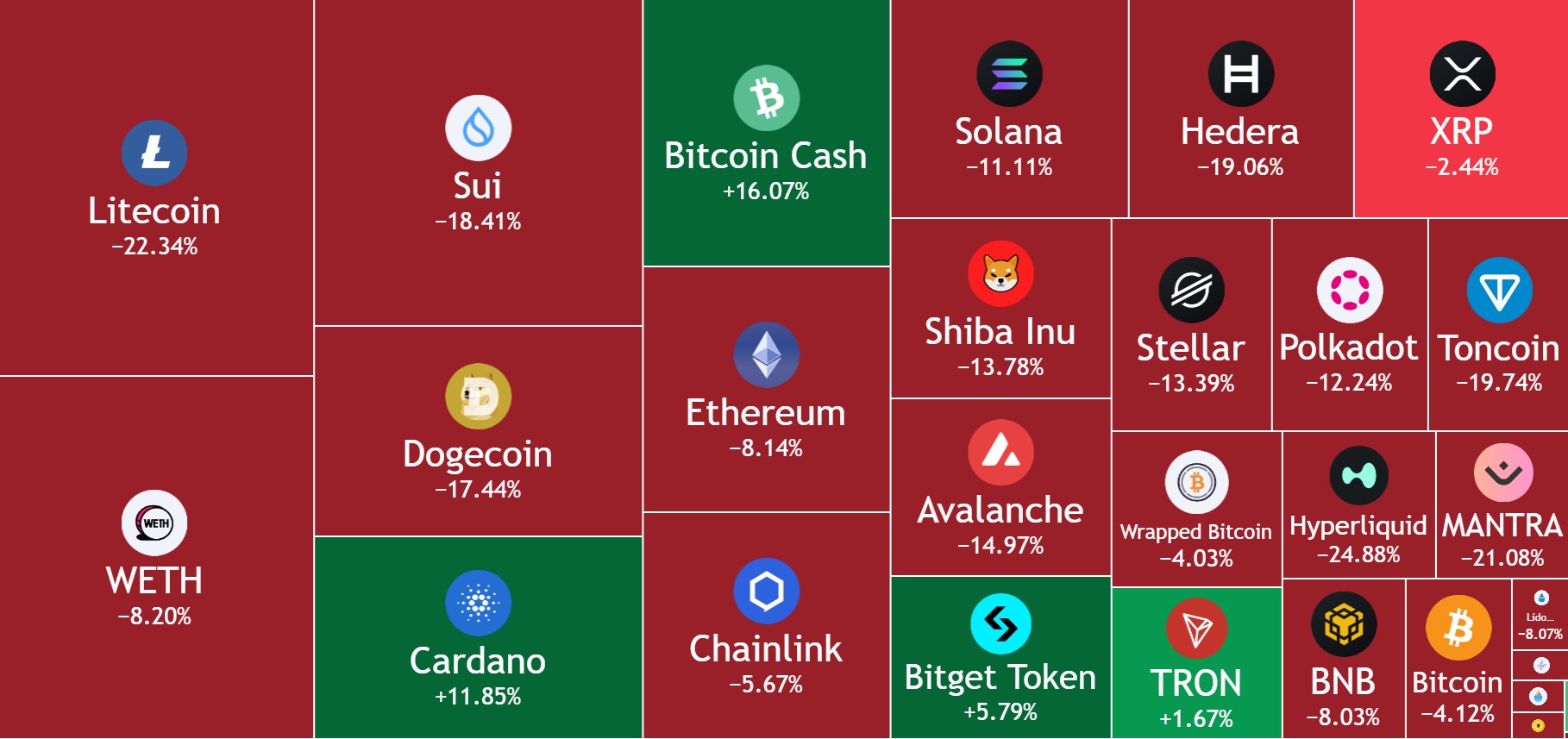

Crypto Market Weekly Performance:

Source: Tradingview

Bitcoin and other cryptos faced volatility last week, as investor sentiment remained weak following disappointment in the U.S. Strategic Bitcoin Reserve plan.

President Trump’s March 7 executive order proposed creating the reserve using seized cryptocurrency rather than purchasing Bitcoin directly, which dampened market expectations.

Analysts noted that the lack of federal Bitcoin investment has negatively impacted prices, highlighting the market’s sensitivity to government actions. To avoid further declines, Bitcoin must stay above the $82,000 support level.

Technically, BTC has reached the 200-day moving average, serving as dynamic support. If bullish confirmations occur, BTC could rise toward the uptrend line. For further upward momentum, it must break the downtrend line with strong force. However, if the Fibonacci support near $80K fails, a further decline to the next Fibonacci support level is expected.

Technically, ETH/USD has reached a strong, long-term support level around $2200. If Ethereum can break the downward RSI trendline, the price could surge, at least up to the crypto’s trendline. If ETH breaks the trendline, a further surge is anticipated.

Next Week’s Outlook

Economic Events

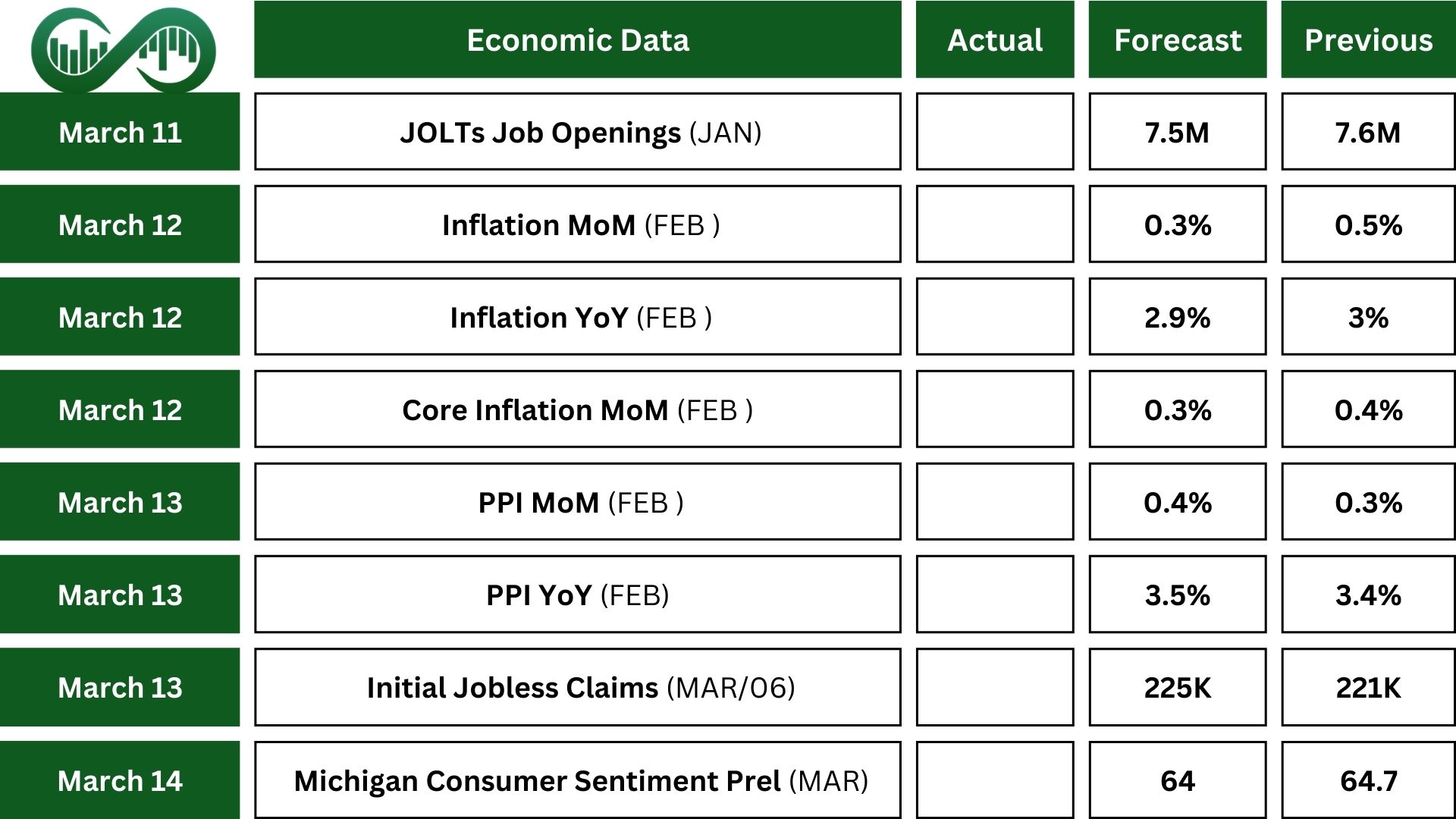

In the US, inflation data is the main focus, as markets watch for signs that tariffs might be raising costs. Both overall and core consumer prices (CPI) are expected to grow by 0.3% in February, a bit slower than January’s 0.5% and 0.4%. Producer prices (PPI) are also predicted to rise by 0.3%, easing from 0.4% in the previous month, while core PPI is expected to stay steady at 0.3%.

Traders will also pay attention to the job openings report (JOLTS), early results for the Michigan consumer sentiment index, and other key updates like inflation expectations, business optimism, and the budget statement.

In Canada, the central bank is likely to lower interest rates by 0.25% due to weak job data and the impact of US tariffs.

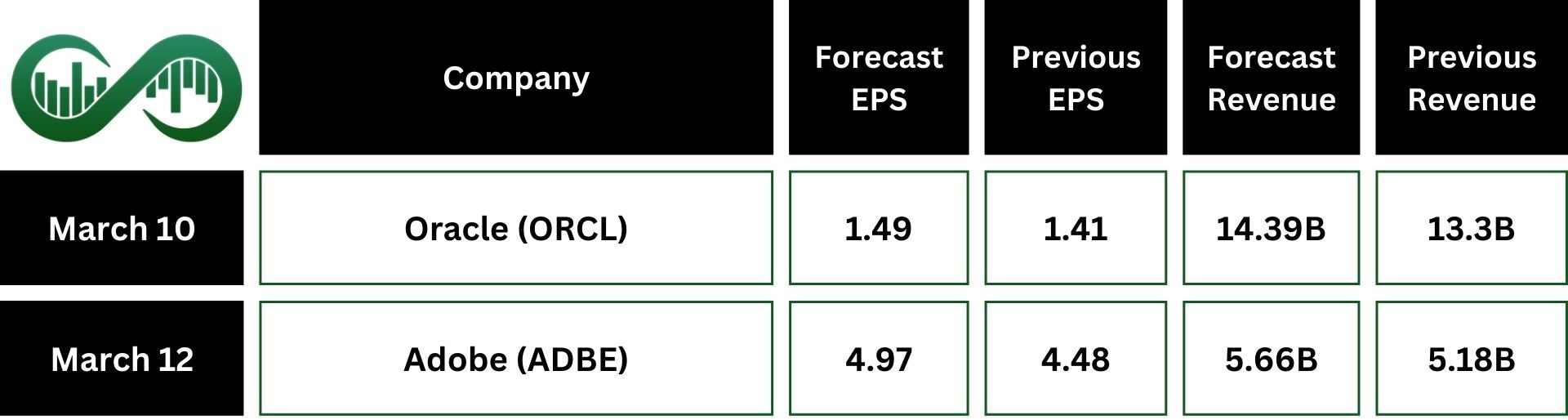

Earnings Events

Earnings season is almost complete, but the results from Oracle (ORCL) and Adobe (ADBE) remain significant.