Last Week’s Reports

Economic Reports

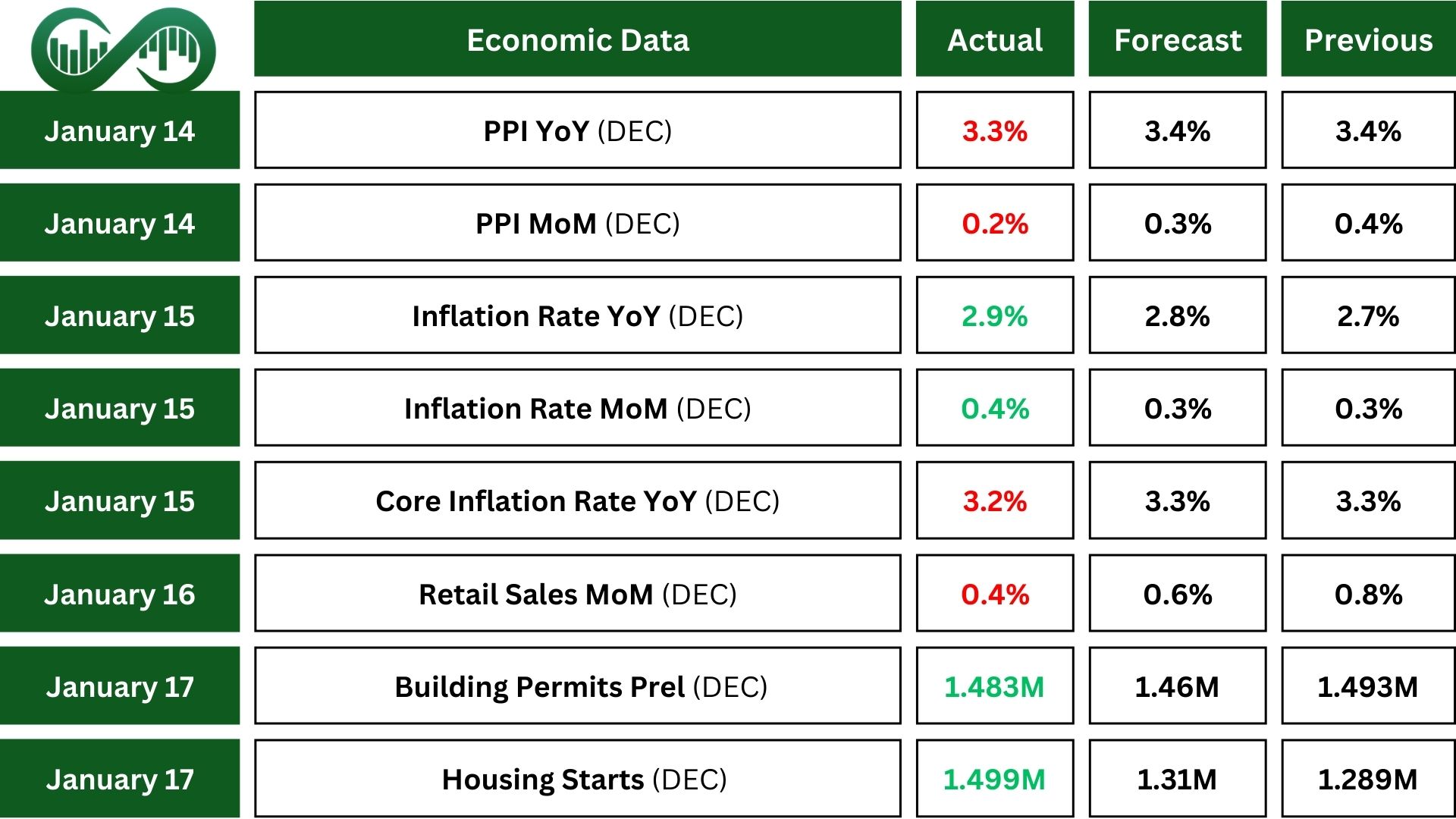

In December 2024, the Producer Price Index (PPI) rose by 0.2%, below the expected 0.3%. For the year, the PPI increased by 3.3%, up from 1.1% in 2023.

Core producer prices, which exclude food and energy costs, were unchanged in December from the previous month. The unchanged core PPI suggested some easing of inflationary pressures which relieved investors’ concerns.

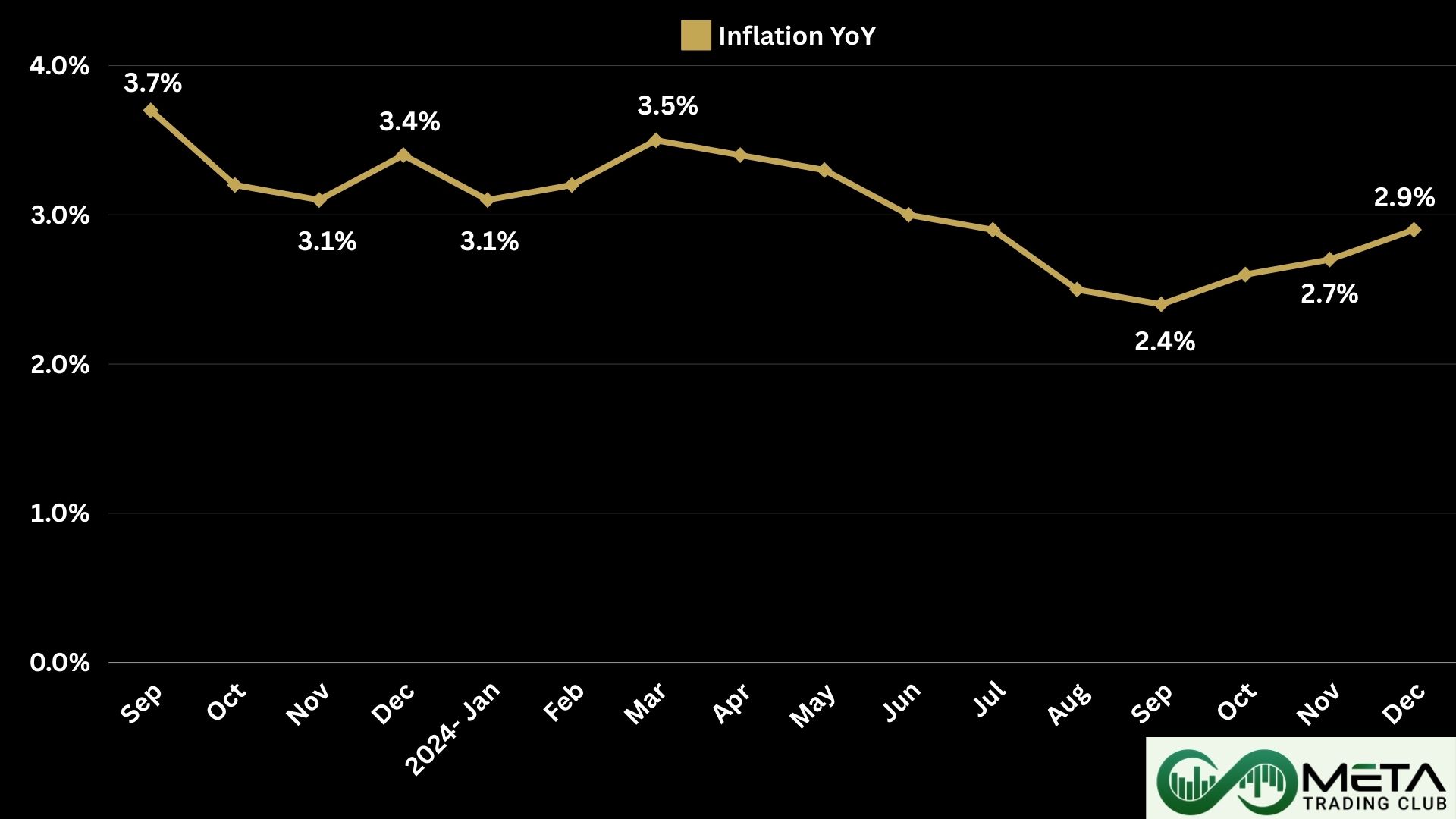

The U.S. Consumer Price Index (CPI) reports for December showed a rise in the inflation to 2.9% year-over-year, up from 2.7% in November. This increase was mainly due to higher energy prices, with gasoline prices rising by 4.4%.

Core inflation, which excludes food and energy, increased by 0.2% month-over-month, showing a slight slowdown. The report highlights ongoing inflation issues, which might affect the Federal Reserve’s interest rate decisions in 2025.

In December, retail sales rose by 0.4% from the previous month and by 3.9% from December 2023. Total sales for 2024 increased by 3%. These figures show steady growth in the retail and food services sectors, highlighting consumer spending trends and economic resilience during the holiday season.

Earnings Reports

JP Morgan Chase

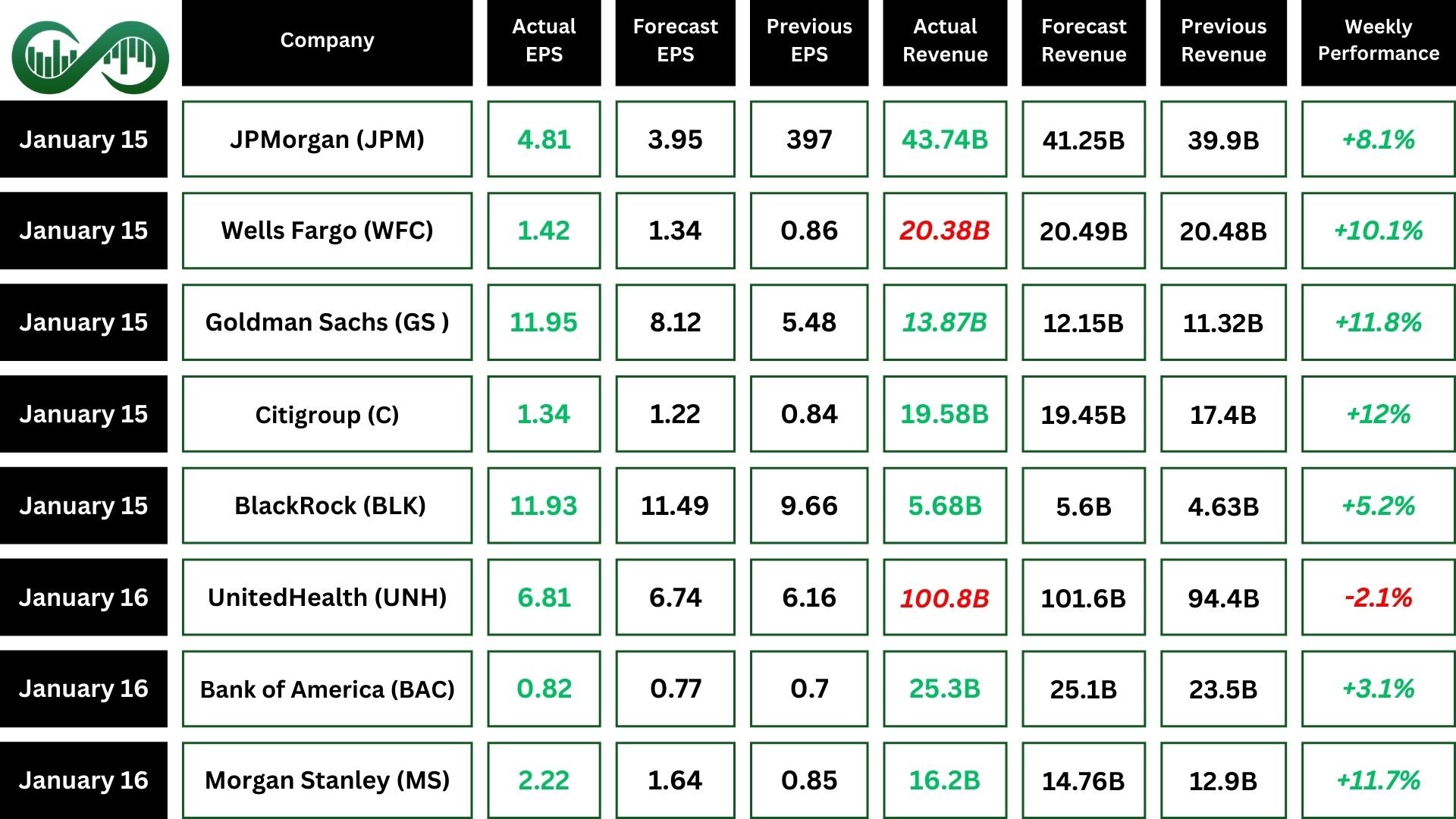

JPMorgan Chase (JPM) Q4 2024 earnings were better than expected. The bank’s record revenue was $43.74 billion, above the forecasts.

Net interest income was $23.47 billion, higher than the expected $22.93 billion. Earnings per share (EPS) were $4.81, beating the forecasts.

For 2025, JPMorgan Chase is optimistic about continued growth. The keynote of earnings was strong performance in fixed income trading and investment banking, with investment banking fees jumping 49% to $2.48 billion.

Technically, JPM stock has impressively surpassed its all-time high with strong momentum following the release of earnings. Maintaining this level could be an encouraging indicator for further growth.

Wells Fargo

Wells Fargo (WFC) Q4 2024 earnings report showed revenue of $20.38 billion, which was slightly below the expectations.

Net interest income was $11.84 billion, also below expectations due to changes in deposit mix and pricing. Diluted earnings per share increased 11%, with strong fee-based revenue growth.

However, their earnings per share (EPS) were $1.43, higher than the forecasts. For 2025, Wells Fargo expects net interest income to grow by 1-3%.

Technically, WFC stock has been approaching its all-time high following the release of earnings. Breaking and remaining above this level could be an encouraging indicator for further increases.

Goldman Sachs

Goldman Sachs (GS) Q4 2024 earnings were better than expected. The bank reported revenue of $13.87 billion, higher than the forecasts. Also, net interest income was $2.35 billion, above the expectations.

Earnings per share (EPS) were $11.95, beating the forecasted $8.07. Also, assets under supervision grew by 12%, reaching $3.14 trillion.

Technically, GS stock has reached a new all-time high with strong momentum after releasing its earnings. Staying above this level could signal further growth.

Citigroup

Citigroup (C) Q4 2024 earnings report showed revenue of $19.6 billion and net interest income was $11.2 billion, below expectations due to changes in deposit mix and pricing.

Earnings per share (EPS) came in at $1.34, above the forecasts. There is a 12% increase in revenues from the prior-year period and a net income of $2.9 billion, reflecting higher revenues and lower expenses.

Morgan Stanley

Morgan Stanley (MS) Q4 2024 earnings report revenue of $16.2 billion, surpassing the forecasts. Also, net interest income was $2.35 billion, higher than the expected. Earnings per share (EPS) came in at $2.22, compared to the forecasted $1.69.

Technically, MS stock has surpassed its previous all-time high with significant momentum following the earnings release. Maintaining this elevated level could indicate the potential for further appreciation.

UnitedHealth

UnitedHealth (UNH) Q4 2024 earnings report showed revenue of $100.8 billion, slightly below the expectations.

However ,net interest income was $8.3 billion, and earnings per share (EPS) were $6.81, both above expectations. Highlights include a 6.8% increase in revenue compared to last year and a positive outlook for 2025, with projected revenues of $450 billion to $455 billion and adjusted EPS of $29.5 to $30.

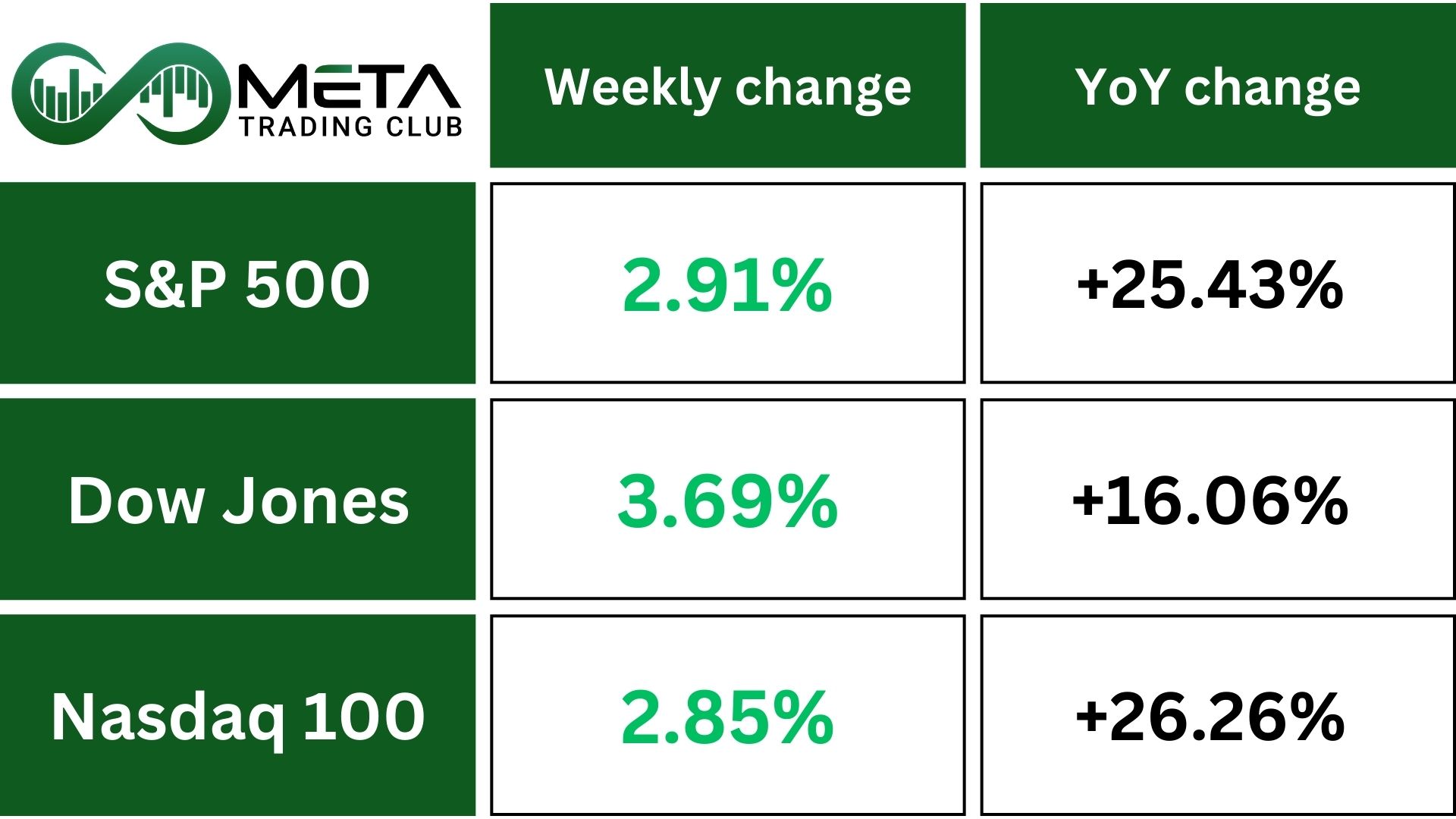

Indices

Indices’ Weekly Performance:

The U.S. stock market rallied this week, with almost all sectors gaining. Traders felt relieved as bond market interest rates fell back.

The S&P 500, Dow Jones, and Nasdaq all had weekly gains, putting them in positive territory for January. Also, they had their biggest weekly rally since Trump’s election in early November.

This is a positive sign for the U.S. stock market’s climb. Helping the recovery is the major drop in interest rates. After a rough start to 2025 with rising Treasury yields, the bull market is expanding as Trump’s inauguration approaches.

Technically, SPX has shown bullish signals by breaking both its downtrend line and RSI downward momentum trendline. This indicates a potential shift from bearish to bullish trend, with buyers gaining control. To maintain this upward movement, SPX needs to stay above these broken trendlines and have supportive market conditions. Keep an eye on key resistance levels and watch for potential pullbacks to test the trend’s strength.

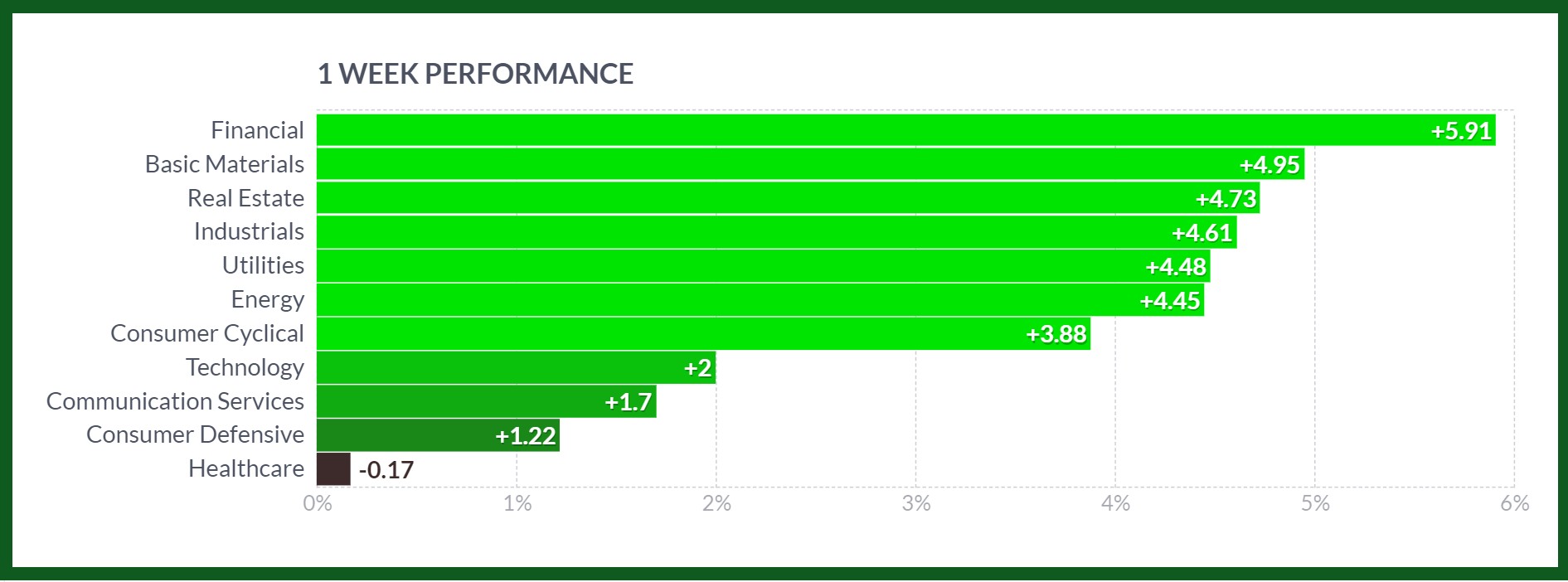

Stocks

Sector’s Weekly Performance:

Source: Finviz

Last week, Financials led the way with substantial gains, driven by strong earnings from big banks. Although most sectors experienced growth, the Healthcare sector saw a slight decline, influenced by regulatory concerns and market uncertainties.

- Financials: This sector saw a significant gain of around 6%, driven by positive earnings reports by big banks.

- Basic Materials: This sector performed well and increased around 5%, weaker than anticipated monthly producer inflation report.

- Real Estate: The sector gained 4.7% as bond market interest rates fell back.

- Industrials: The sector saw a rise of 4.6%, supported by good performance in manufacturing retails sales.

- Utilities: This sector experienced growth of 4.5%, driven by stable demand.

- Energy: The sector performed well and gained 4.4%, with rising oil prices and increased production contributing to its gains.

- Consumer Cyclical: This sector saw growth of 3.8%, reflecting strong consumer spending and positive economic indicators.

- Technology: The sector had a modest gain of 2%, supported by positive sentiment of the market.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their success:

- MicroStrategy (MSTR): Surged 21% due to increase in its Bitcoin price which the company holds.

- Intel (INTC): Climbed 12% following a report that a big company is now interested in taking over the US-based semiconductor manufacturer.

- Citigroup (C): Increased 12% following strong quarterly results.

- Applied Materials (AMAT): Rose 11.8% after brokerage upgrades stocks.

- Goldman Sachs (GS): Gained 11.7% after exceeding earnings expectations, with strong performance in investment banking and asset management divisions.

- Morgan Stanley (MS): Advanced 11.6% on impressive quarterly results, driven by higher trading revenues and strong performance in wealth management business.

- PDD Holdings (PDD): Grew 11.5% following growth in its e-commerce platform, attracting investors looking for exposure to the Chinese market.

- Deere & Company (DE): Increased 11.4% after expecting a positive earnings outlook and strong demand for its agricultural equipment.

- Wells Fargo (WFC): Rose 10.2% on strong quarterly earnings and optimistic projections for future growth in the financial sector.

- PayPal (PYPL): Increased 10% after Wells Fargo increased its price target.

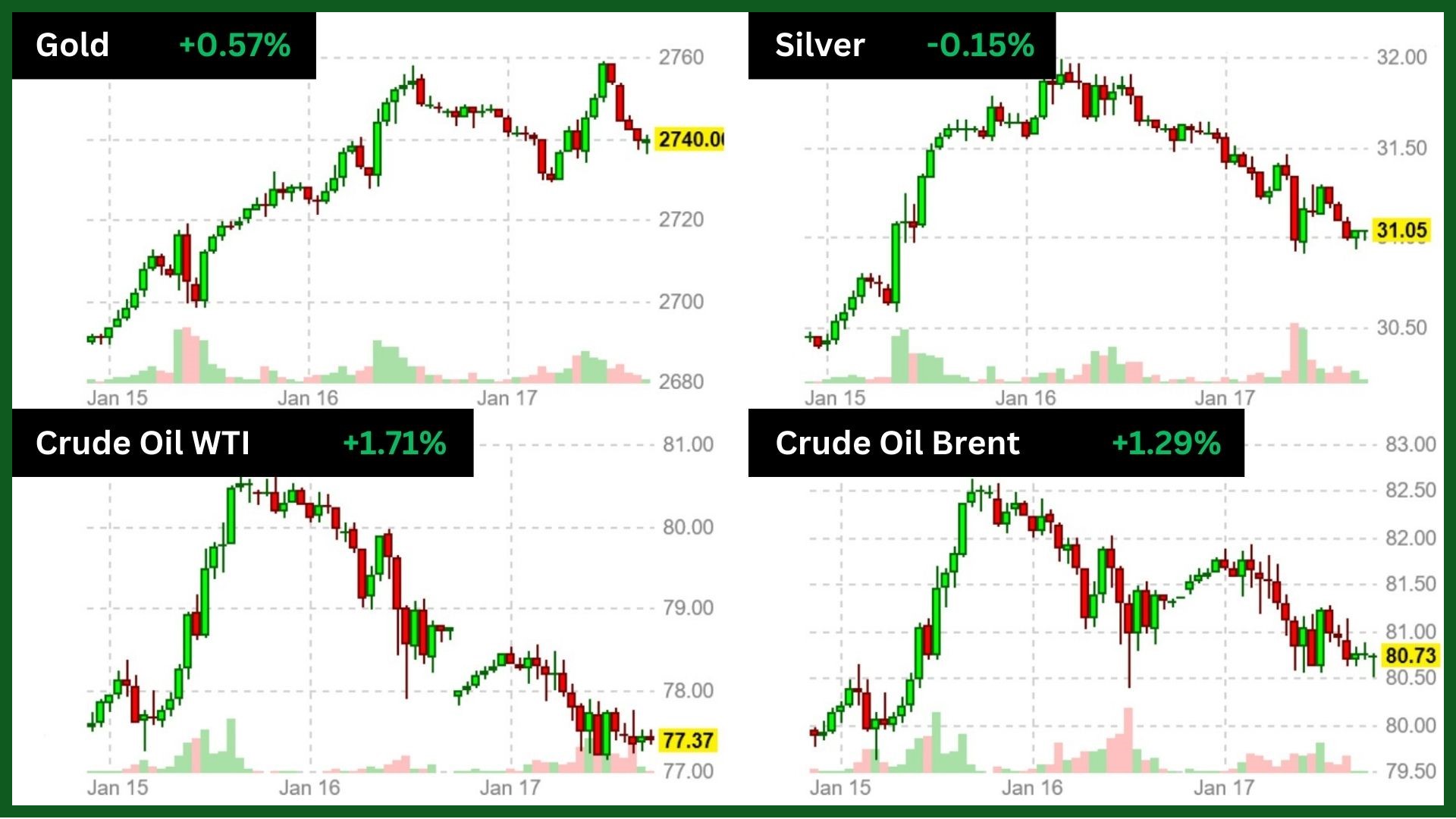

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold prices rose above $2,720 per ounce, then settled around $2,700. This happened despite Israel and Hamas agreeing to stop all war actions and release hostages. Negotiations are ongoing, so gold traders are ready to act quickly.

In the U.S., the recent CPI data showed that core inflation for December rose by 3.2%, less than the expected 3.3%. Lower inflation supports the case for more interest rate cuts from the Federal Reserve, which is good for gold because it makes holding gold more attractive.

Technically, gold broke out of a symmetrical triangle and reached to a strong resistance line. Bulls need more momentum to keep pushing prices higher. Gold has been fluctuating since reaching a record high of $2,790 per ounce. Future price movements will depend on new economic data and any renewed conflicts. Remaining above this resistance could be an encouraging indicator for further increases.

WTI crude oil futures fell on Friday due to expectations of a ceasefire in Gaza. Despite this drop, oil prices rose for the fourth straight week, up about 2%, driven by concerns over new U.S. sanctions on Russian oil, which could tighten global supplies.

Traders are also watching potential policy changes under a possible Trump presidency, which might include tougher sanctions on Russian oil. Additionally, China’s economic recovery and increased demand prospects have boosted market sentiment.

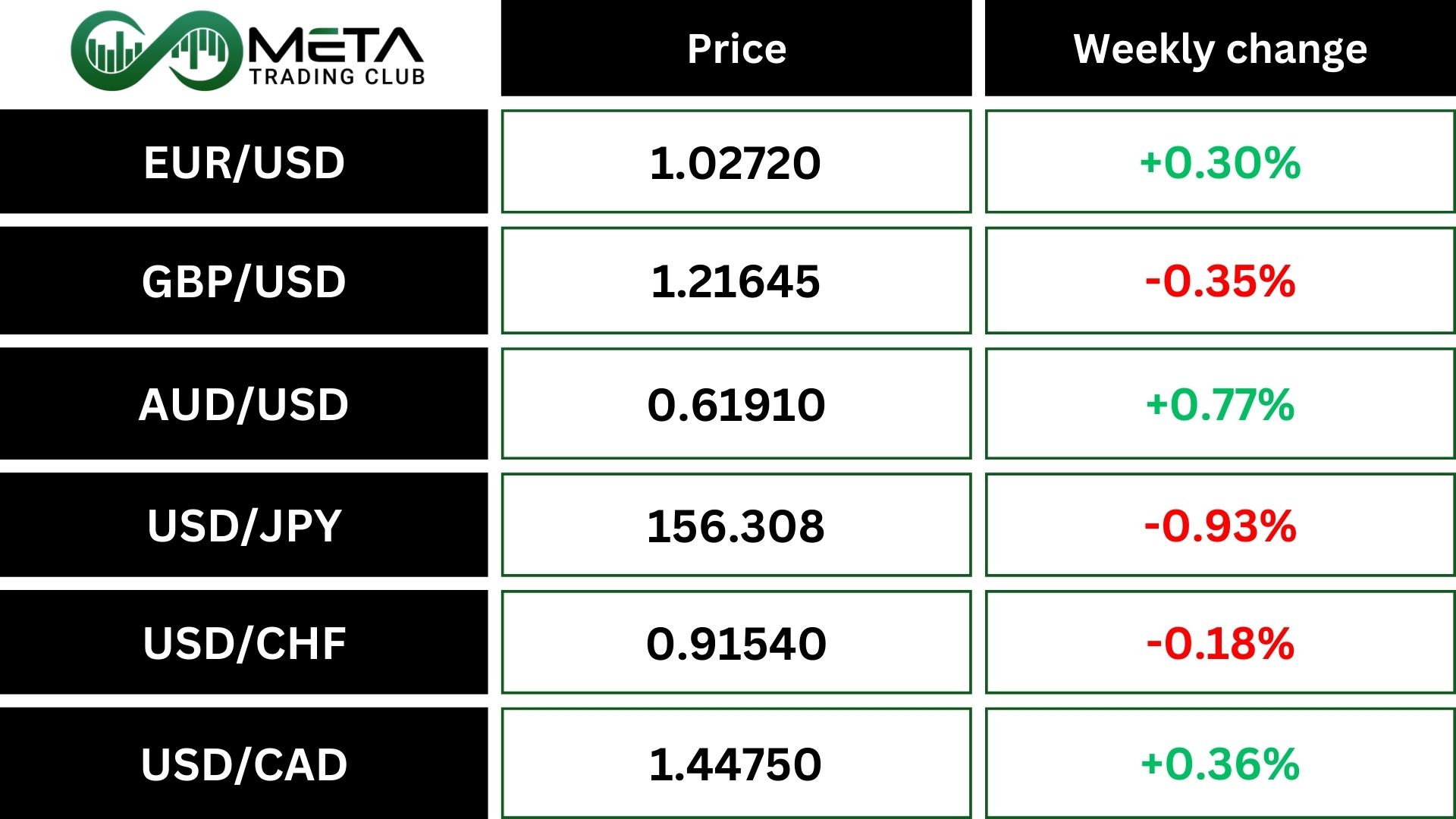

Forex

Weekly Performance of Major Foreign Exchange Pairs:

USD/JPY had its best weekly performance in over a month, as expectations for a Bank of Japan rate hike grew. It climbed against the dollar this week, reversing last week’s decline, and reached a one-month high of 154.98 per dollar on Friday.

GBP/USD fell 0.35%, close to the 14-month low it hit on Monday. British retail sales unexpectedly fell in December, raising the risk of an economic contraction in the fourth quarter.

DXY index was set to drop about 0.25% this week, ending a six-week run of gains.

USD/CNY was last trading at 7.3249 per dollar after data showed China’s economy grew 5.4% in the fourth quarter, beating analysts’ expectations. This positioned full-year 2024 growth at 5%, meeting Beijing’s target.

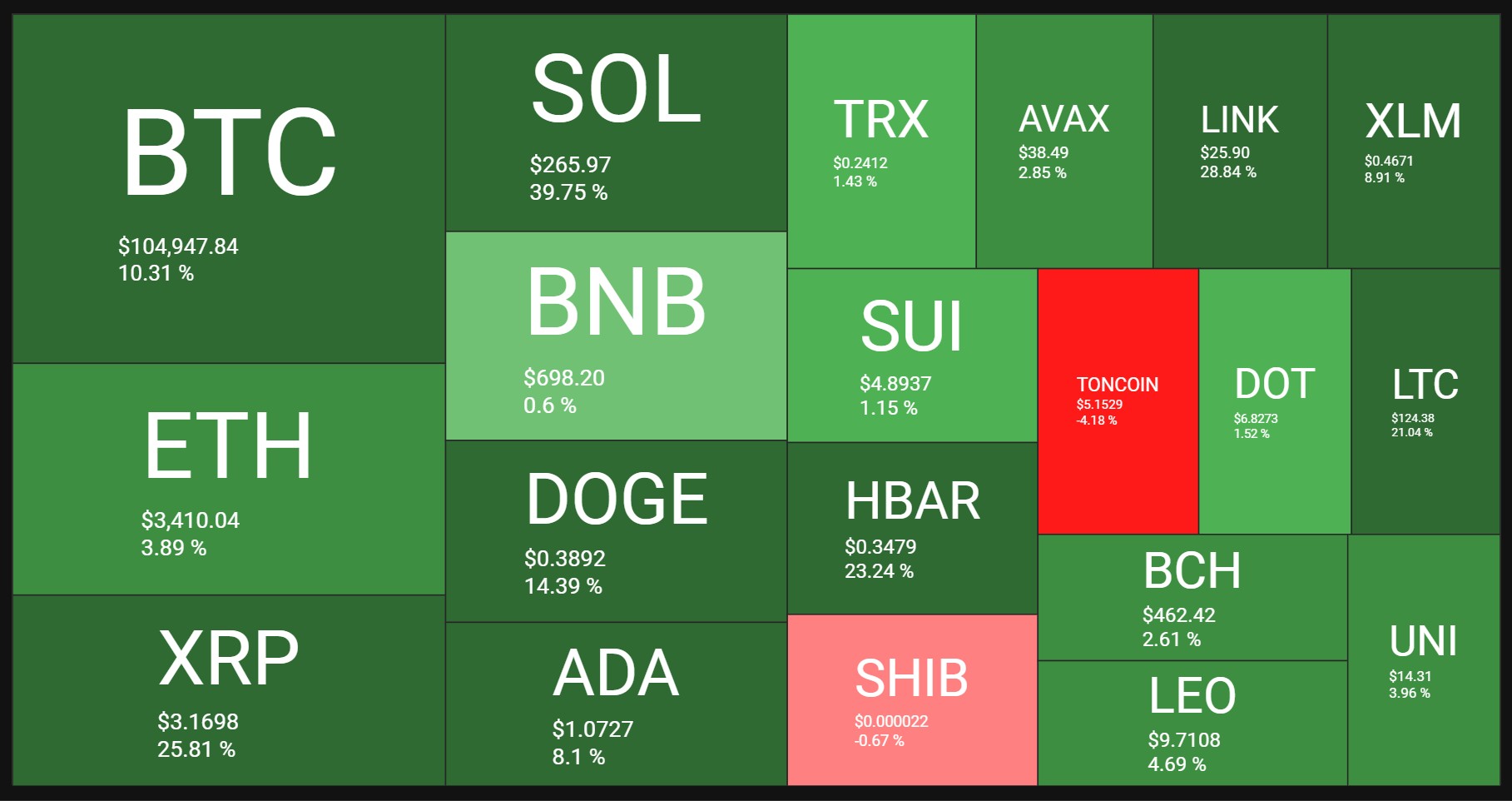

Crypto

Crypto Market Weekly Performance:

Source: quantifycrypto

Bitcoin prices rose to nearly $105,000. This followed positive news from Washington about a pro-crypto policy. Donald Trump wants to prioritize crypto in his administration. Experts in digital assets will execute these policies. An executive order aims to make crypto a national priority. This shift marks a significant change from the previous administration. Trump supports expanding the crypto industry in the US. He wants all Bitcoin to be made in the USA.

Technically, BTC has broken its downward momentum trendline on RSI and is approaching its all-time high of $108K. Successfully breaking through and maintaining this zone with strong momentum could indicate further price increases.

The altcoins, especially meme coins, have been hit hard since the emergence of TRUMP. TRUMP has now become the second-biggest meme coin, surpassing both PEPE and SHIB. Still, the largest meme coin currently is DOGE, with a market cap of around $54 billion.

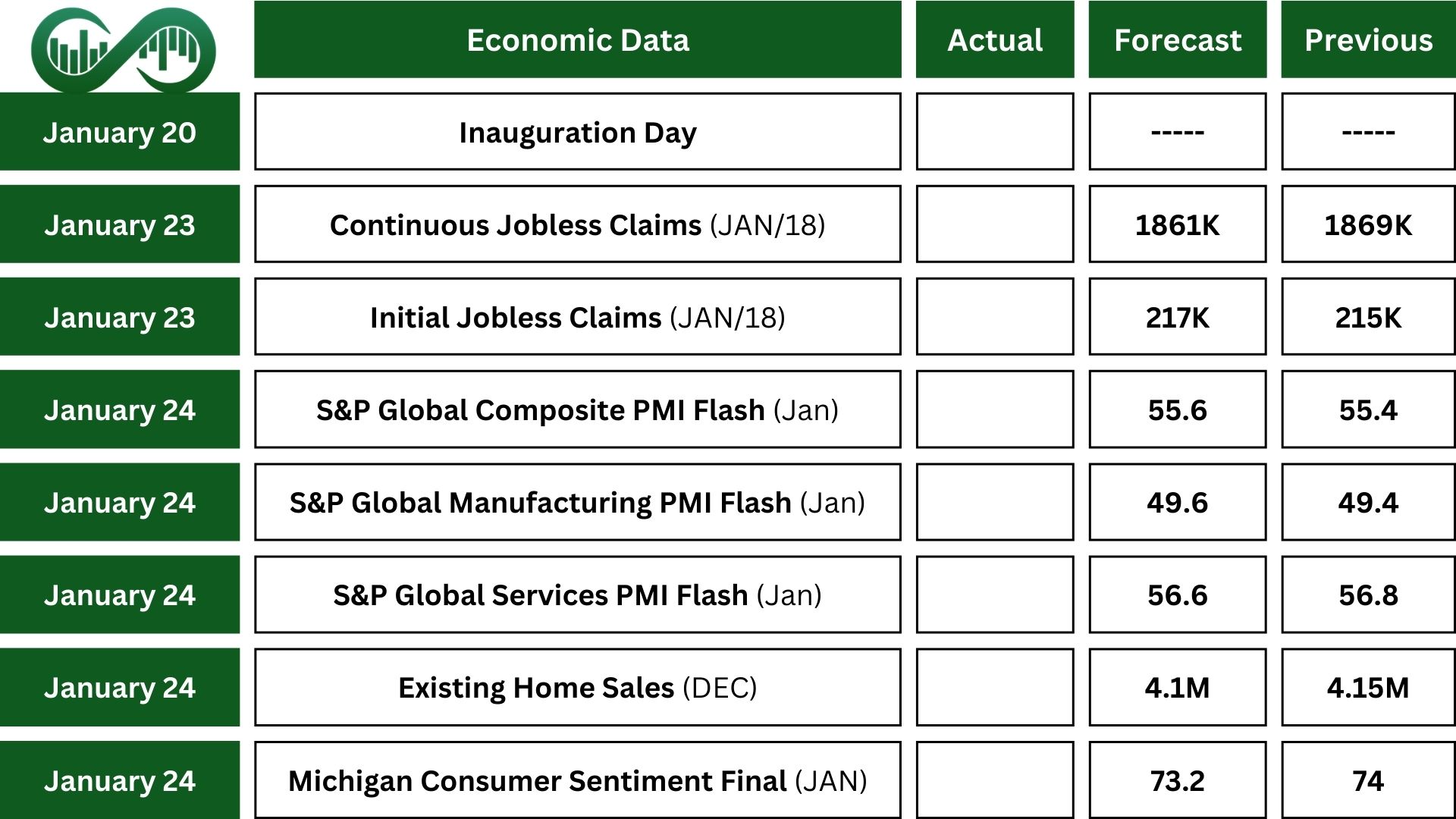

Next Week’s Outlook

Economic Events

On Monday, everyone in the US will be watching as Donald Trump becomes President. Traders will pay close attention to his speech to see if he mentions any new policies or executive orders.

The U.S. stock and bond markets will be closed Monday in honor of Martin Luther King Jr. Day.

On the economic front, there aren’t many major events. We’ll get an early look at private-sector activity in January with the flash S&P Global PMIs, as well as existing home sales and the final Michigan Consumer Sentiment reading.

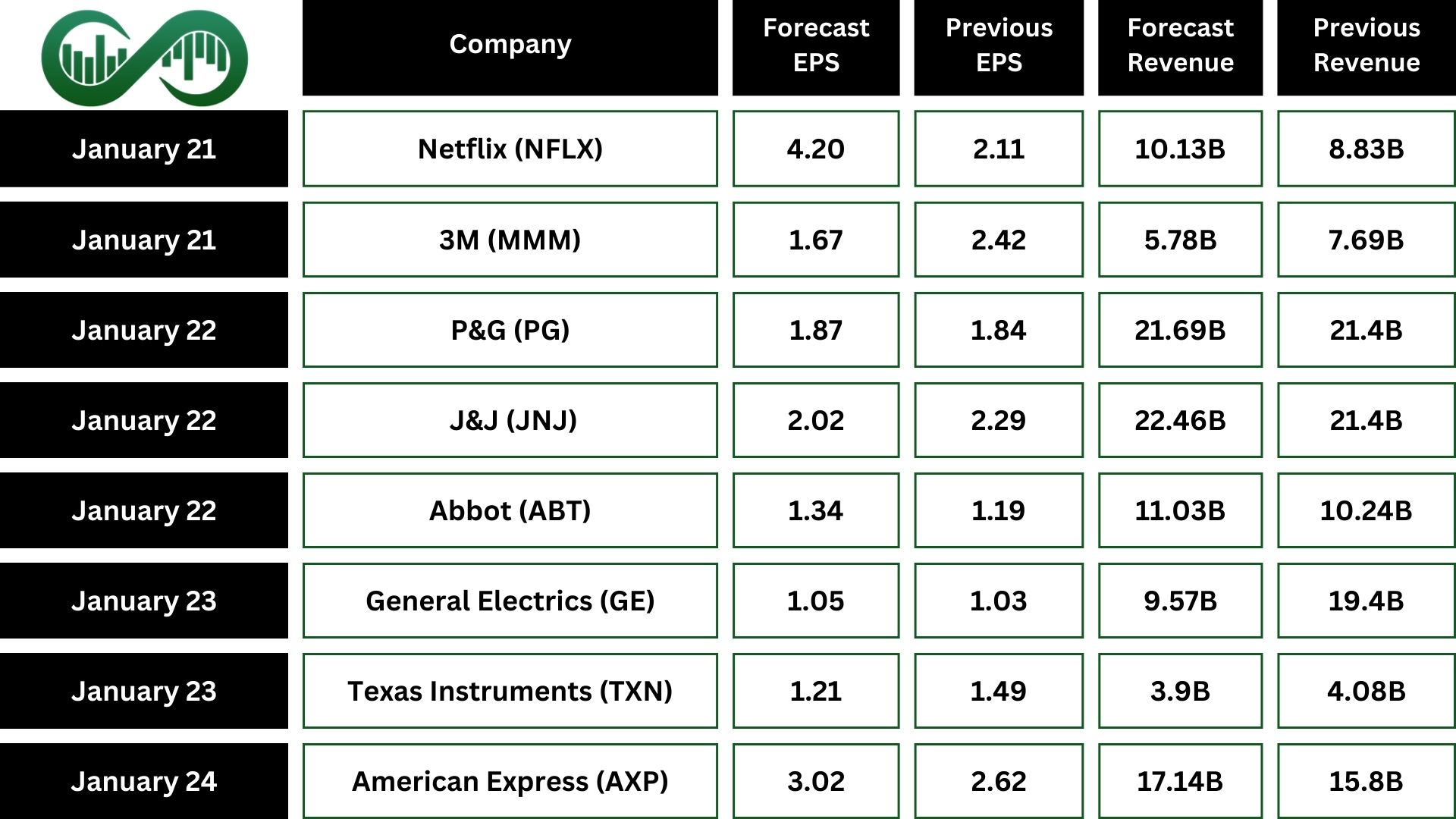

Earnings Events

Many big companies like Netflix (NFLX), Charles Schwab, Procter & Gamble (PG), Johnson & Johnson (JNJ), Abbott (ABT), Progressive, Intuitive Surgical, General Electric (GE), Texas Instruments (TXN), Union Pacific, American Express (AXP), Verizon, and NextEra Energy will be sharing their earnings reports soon.