Last Week’s Reports

Economic Reports

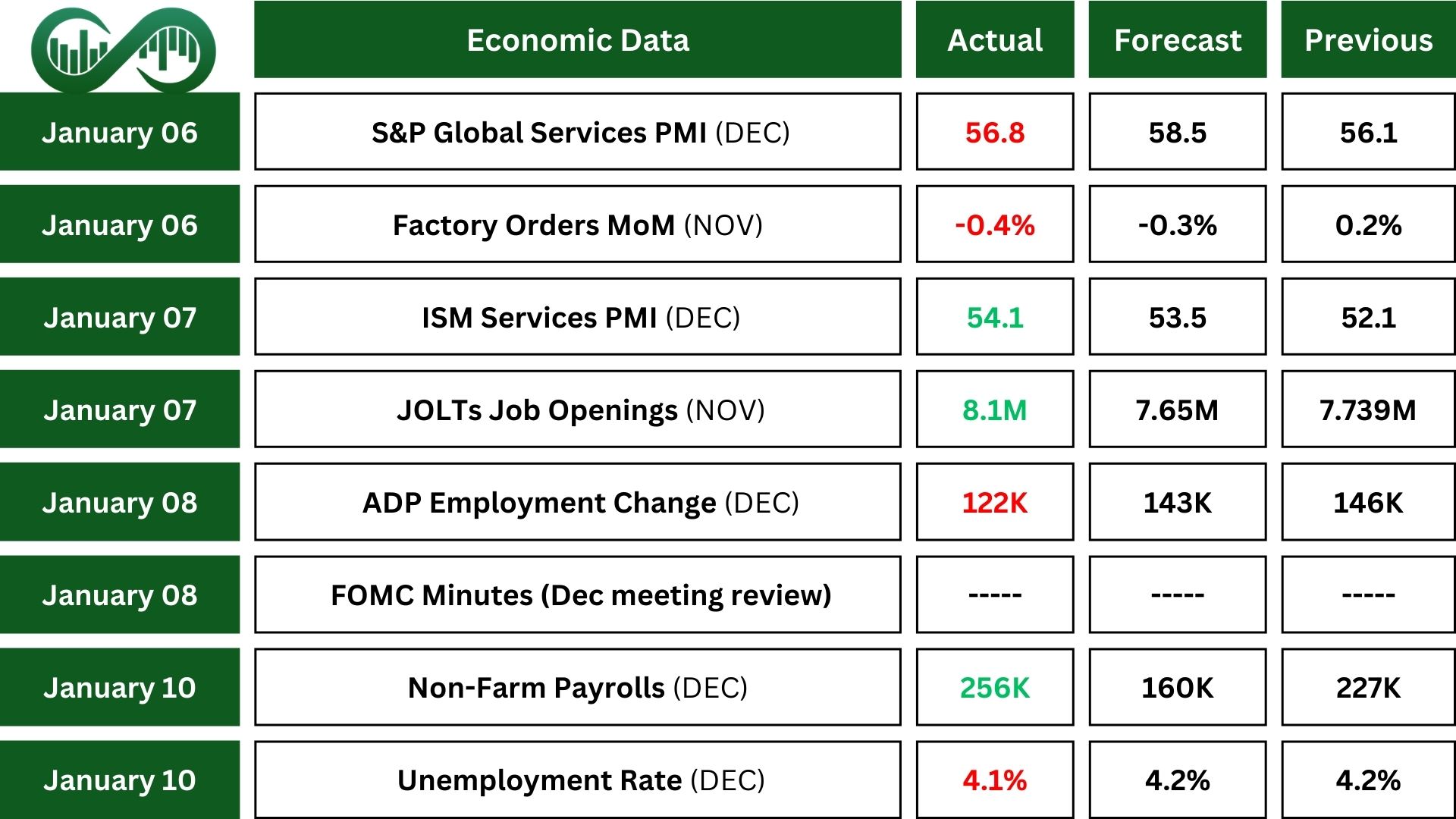

In December, the US Services PMI experienced strong growth. Index increased to 56.8, its highest in 33 months, showing that business activities expanded for the second month in a row. New orders grew quickly, reaching the fastest pace since March 2022, as customers were more willing to spend after the Presidential Election.

Michigan Consumer Sentiment was mostly stable in January. People are less worried about current living costs but more concerned about future inflation.

Year-ahead inflation expectations jumped to 3.3%, the highest since May 2024. Long-term inflation expectations also rose to 3.3%. This noticeable change was seen across different groups, especially lower-income consumers and Independents.

The minutes from the FOMC meeting held on December 17 and 18 were released last week. You can read the recap here.

Jobs Report

JOLTs: The report showed stability in job openings at 8.1 million, although this is fewer than last year. The number of quits decreased and layoffs and discharges were stable.

ADP: Private employers added 122K jobs in December, which was less than expected. Hiring slowed in several industries, and manufacturing jobs declined for the third month in a row. The labor market grew at a slower pace, with both hiring and pay increases slowing down.

Jobless Claims: The number of people applying for unemployment benefits in the US has decreased significantly, reaching the lowest level in eleven months at 201K. This was also lower than expected. The four-week average of jobless claims also saw a notable decline. Overall, the job market seems to be showing signs of stability with a positive trend in new unemployment claims.

Challenger: US employers announced 38,792 job cuts, the lowest in five months but a 5.5% increase from 2023. This was the highest since 2020. The technology sector had the most job cuts and the auto sector saw a 43.2% rise in job cuts.

Non Farm Payrolls: The report showed the US economy added 256K non-farm payrolls. This surpassed market expectations of 160K. Employment increased in health care, government, and social assistance sectors.

Unemployment: The unemployment rate in the U.S. decreased to 4.1%, down from 4.2% in the previous month, and below market expectations. Also, The labor force participation rate was 62.5%.

Wages: Average hourly earnings for all employees on private nonfarm payrolls increased to $35.69 in December. Over the past year, average hourly earnings have increased by 3.9%.

These strong job reports indicated a robust labor market, which could lead the Federal Reserve to maintain higher interest rates for a longer period to manage inflation.

Earnings Reports

Delta Air Lines (DAL) earnings report for fourth quarter and the full year 2024 shows a Strong performance. The company reported quarter operating revenue of $14.4 billion and earnings per share of $1.85, both earnings and revenue exceeding expectations.

Shares of Delta Air Lines rose by 9% immediately following the earnings report.

Over the past year, Delta’s stock has risen by roughly 50%, outperforming some competitors but trailing behind others. The strong financial results and positive outlook for 2025 have bolstered investor confidence, leading to a favorable reaction in the stock market.

Delta Air Lines has exhibited strong price performance, particularly with the significant gap up following the earnings report. The stock is reaching its all-time high (ATH), signaling robust bullish sentiment.

Breaking and staying above the ATH would likely attract more investors and traders, increasing buying pressure and driving the stock price higher.

Indices

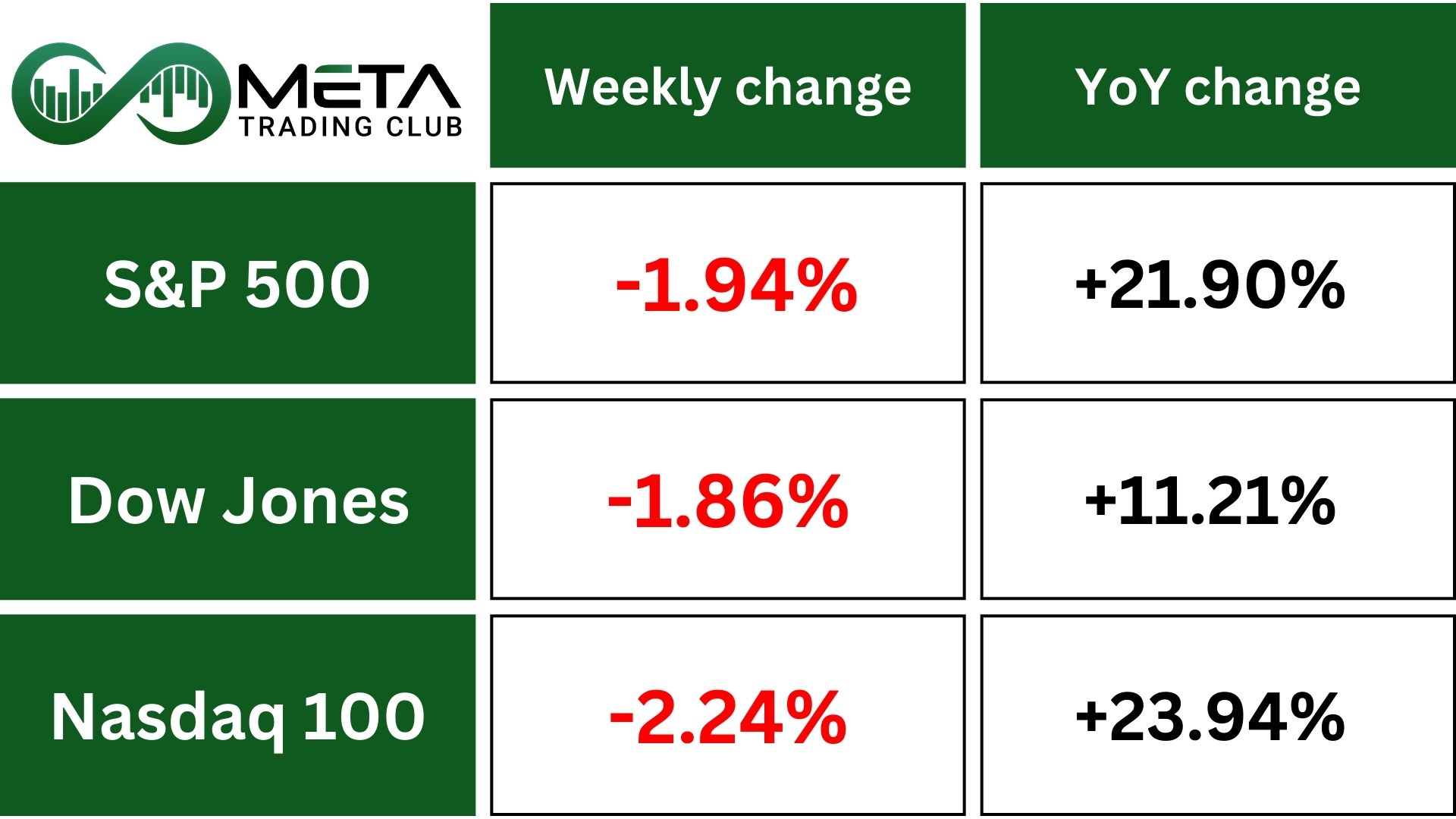

Indices’ Weekly Performance:

US stock indices dropped last week, especially on Friday after strong nonfarm payroll data boosted government bond yields and expectations that interest rates will stay high longer.

The Dow and S&P 500 both fell around 2%, while the Nasdaq dropped even more. Real estate and financial sectors, which are sensitive to interest rates, saw the biggest declines due to the strong jobs report and rising Treasury yields. The energy sector performed the best.

The S&P 500 Index is currently trading below a strong support zone, but it is nearing the 100-day moving average. The RSI indicates downward momentum, suggesting that the market may continue to face selling pressure. If the price remains below the 100-day moving average, a further decline to the next Fibonacci retracement level at 5,700 is anticipated.

Stocks

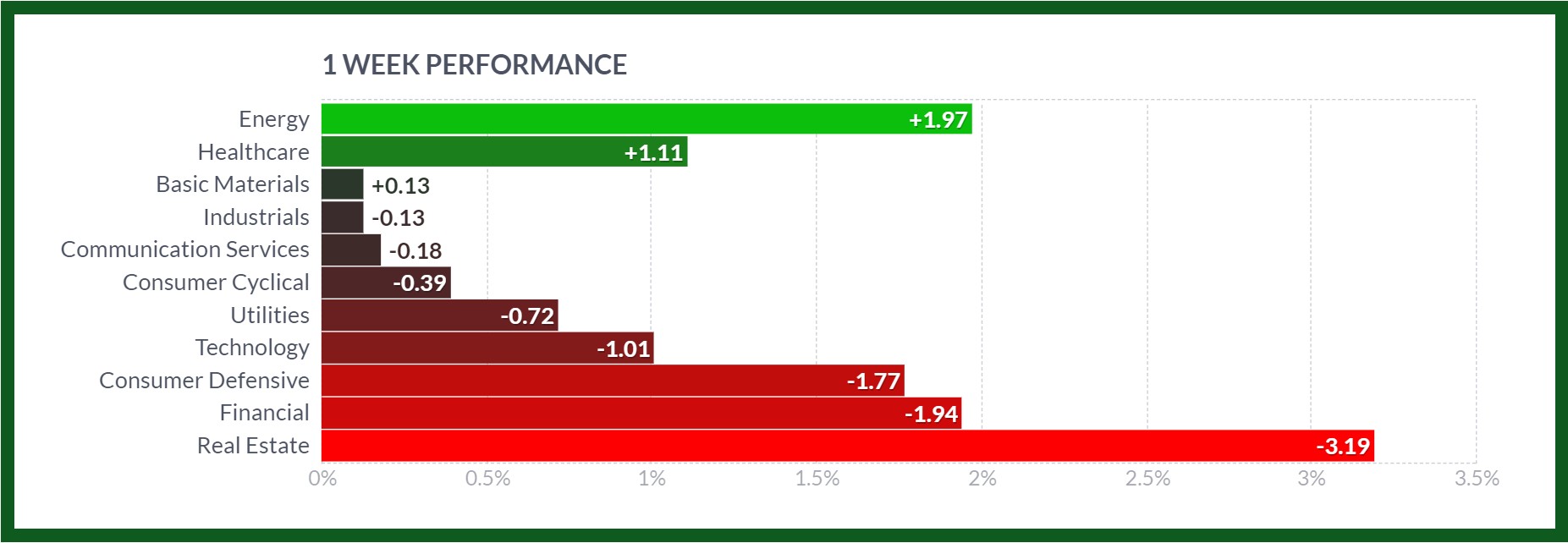

Stock Market Sector’s Weekly Performance:

Source: Finviz

The stock market saw varied performances across different sectors last week. Here’s a breakdown of how each sector fared:

Energy: Rose about 2%, due to increasing oil prices and heightened demand for energy resources.

Healthcare: Gained about 1.1%, driven by growing concerns around bird flu.

Technology: Decline of about 1%, influenced a report Biden planning new restrictions on AI chips exports

Consumer Defensive: Dropped by about 1.8%, likely due to concerns over consumer demand.

Financial: Experienced a significant decline of about 1.9%, due to the strong jobs report and rising Treasury yields. Also, insurers fall as LA fires set to be costliest in California history.

Real Estate: Saw the largest decline of about 3.2%, likely influenced by rising interest rates concerns.

Stock Market Weekly Performance:

Source: Finviz

Top Performing Stocks

The stock market saw some impressive performances last week, with several stocks making significant gains. Here are the top performers and the reasons behind their success:

- Constellation Energy (CEG): Surged 22% due to rise in energy prices.

- Delta Air Lines (DAL): Increased 13% due to positive earnings and industry outlook.

- Micron Technology (MU): Rose 13% as to provide memory for Nvidia’s gaming chips.

- United Airlines Holdings (UAL): Surged 12% as consumers spending rises

- GE Vernova (GEV): Up 10% by the increasing worldwide adoption of clean energy across industries.

- Texas Pacific Land (TPL): Rose 9.5% due to energy sector’s climb coincided with a rise in crude oil.

- Arm Holdings (ARM): Increased 8% as it considers acquiring Ampere Computing.

- MicroStrategy (MSTR): Surged 8% due to positive market sentiment.

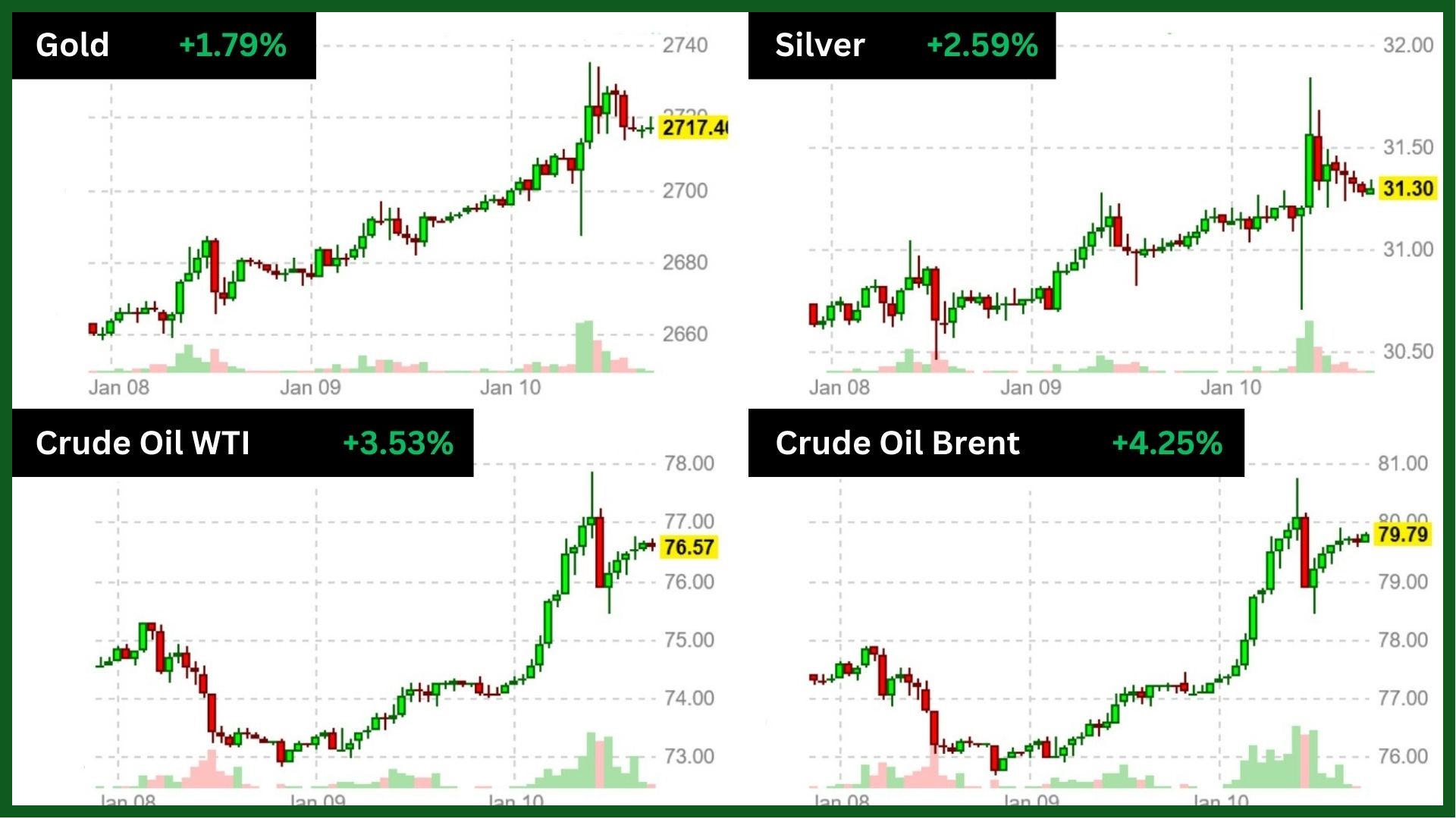

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold prices went up last week because people are unsure about the new Trump administration’s policies. At the same time, strong U.S. job data made people think the Federal Reserve might not cut interest rates as much this year. While a higher dollar is normally bearish for gold, the precious metal is rising as investors seek its safe haven.

Crude oil prices went up by over 3% last week, with Brent crude almost reaching $80 a barrel due to potential supply problems and higher demand for heating fuel because of colder weather.

Also, this weekly gains, supported by expected stricter U.S. sanctions against Russia and Iran, and declining Russian exports. Analysts say new U.S. sanctions will likely further reduce Russian crude exports, prompting Indian and Chinese buyers to find alternatives.

Forex

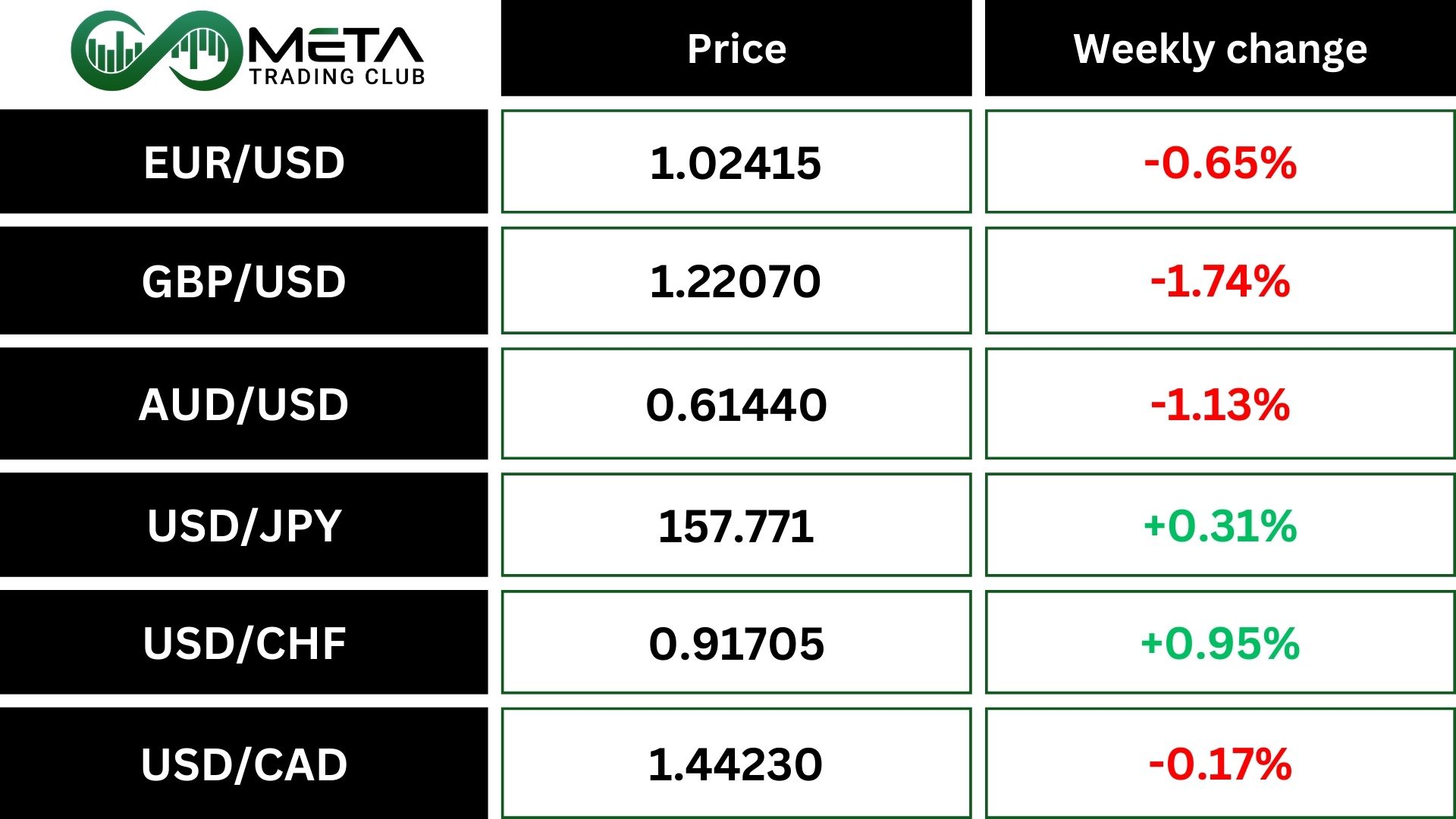

Weekly Performance of Major Foreign Exchange Pairs:

The British Pound fell to its lowest level since November 2023 after U.S. job data. It faced heavy selling pressure as yields rose. While it might bounce back slightly, significant recovery is unlikely before the U.K.’s December CPI and November GDP data releases this week.

The Euro fell to a 26-month low against the dollar due to concerns about European growth. Upcoming eurozone inflation data and comments from ECB might trigger more selling.

The USD/JPY reached a multi-month high of 158.89 but then fell as U.S. equities dropped and traders adjusted their positions. With Tokyo on holiday Monday, yen buyers are likely waiting for January 14 comments from BOJ may support higher price forecasts due to wage gains and yen weakness.

The Dollar index, which measures the dollar’s value against other currencies, reached its highest since November 2022. It’s on track for its sixth weekly gain in a row, last at 109.64.

Crypto

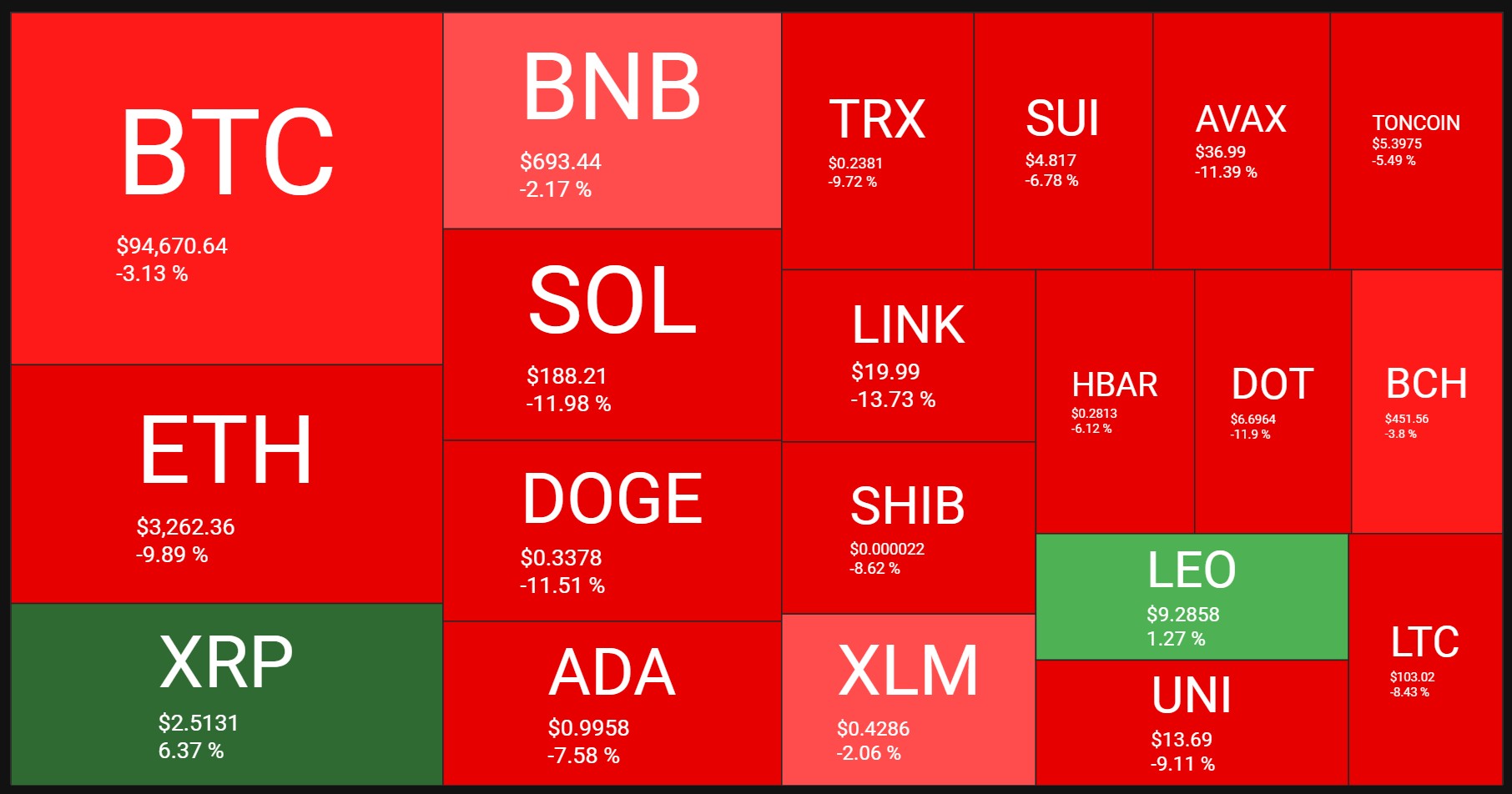

Crypto Market Weekly Performance:

Source: quantifycrypto

The recent drop in the cryptocurrency market can be explained by a few key reasons. First, there are growing worries about new government rules that might restrict crypto trading. Secondly, rising inflation and higher interest rates have made people cautious, leading them to avoid riskier investments like cryptocurrencies. Additionally, recent security breaches at some crypto exchanges have made investors nervous. Lastly, large-scale selloffs by major holders have led to a domino effect, pushing prices down further.

A significant number of investors have accumulated Bitcoin holdings between $98,000 and $100,000, creating a strong resistance level. The Bitcoin chart shows a period of consolidation with the potential for a major breakout. Keep an eye on the support and resistance levels for indications of a directional move.

Next Week’s Outlook

Economic Events

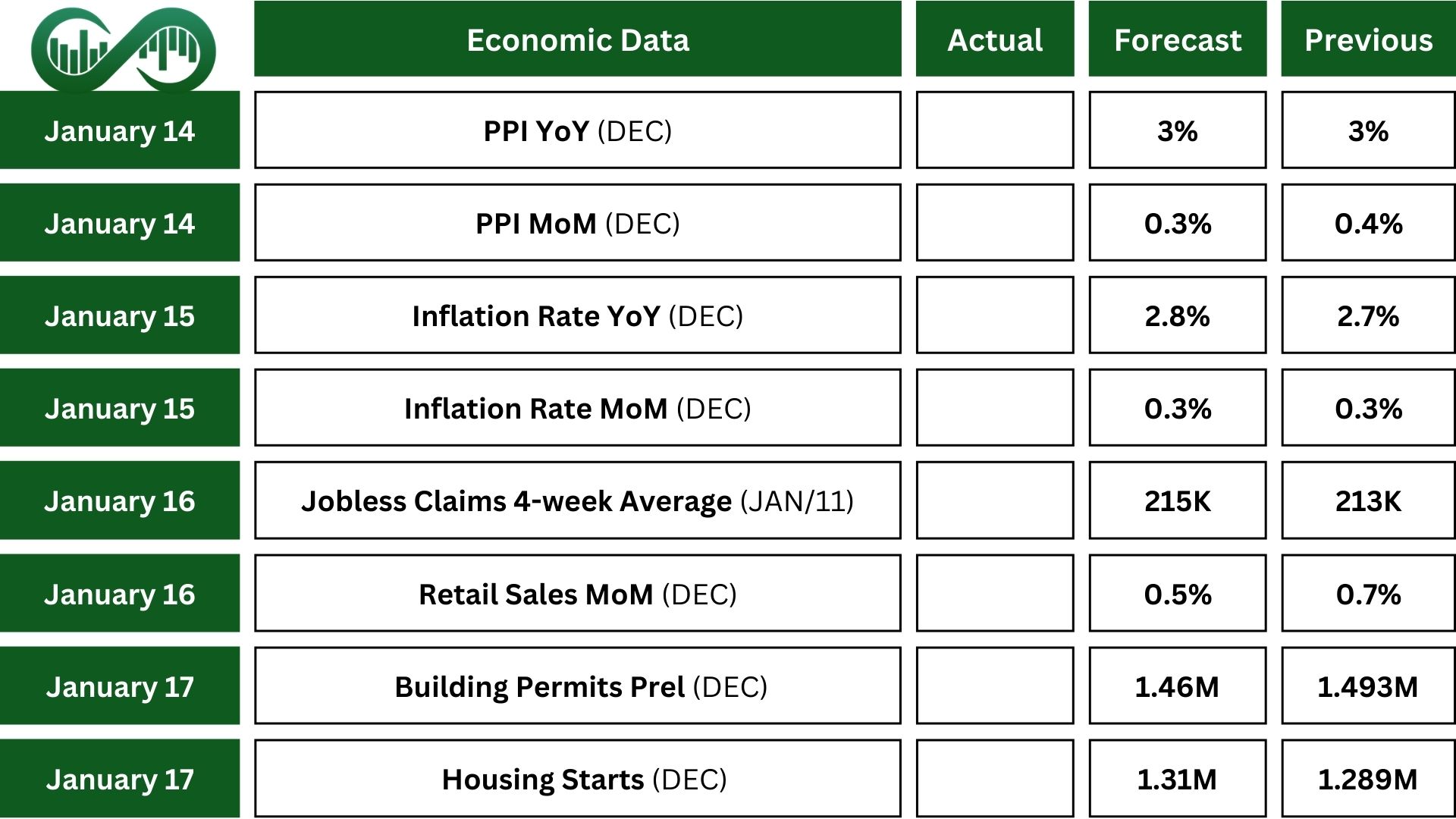

This week, the focus is on inflation, with the CPI report expected to show a 2.8% annual increase and a stable 0.3% monthly rate. Core inflation should stay at 3.3% annually and ease to 0.3% monthly.

PPI data is expected to show a 3% annual rise and a 0.3% monthly increase.

Retail sales are predicted to grow by 0.5%, down from 0.7%. Industrial production is forecast to increase by 0.2%.

Other important indicators include building permits, housing starts,, the Philadelphia Fed Manufacturing Index, export and import prices, the NY Empire State Manufacturing Index, the NFIB Business Optimism Index, and consumer inflation expectations. Traders will also watch comments from Fed officials for policy clues.

Earnings Events

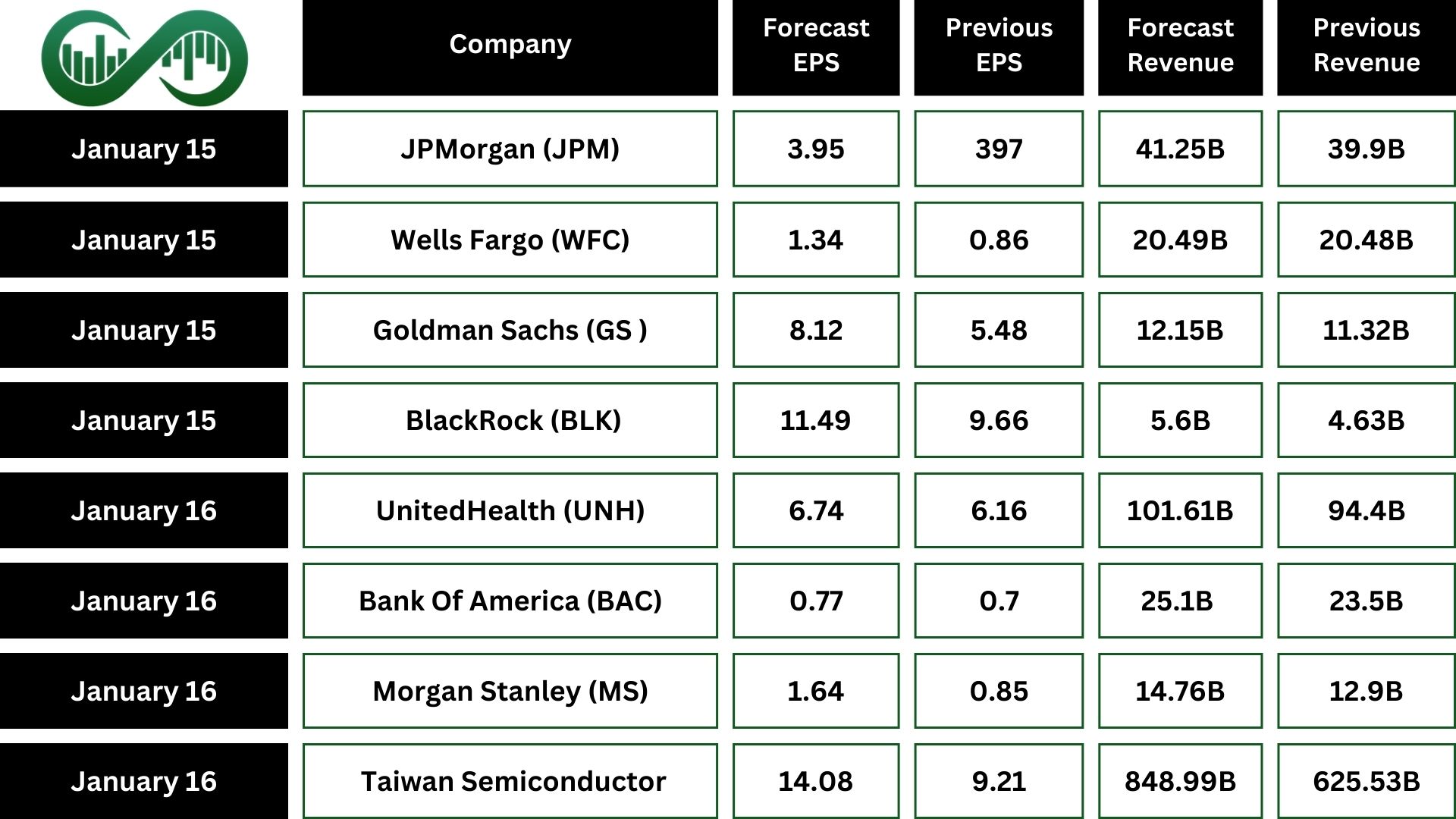

In the US, earnings season is in full swing. Major banks like JPMorgan Chase (JPM), Wells Fargo (WFC) , Goldman Sachs (GS), Citigroup (C), Bank of America (BAC), BlackRock (BLK) and Morgan Stanley (MS) are set to release their quarterly results.

Also, Taiwan Semiconductors will report.