Last Week’s Reports

Economic Reports

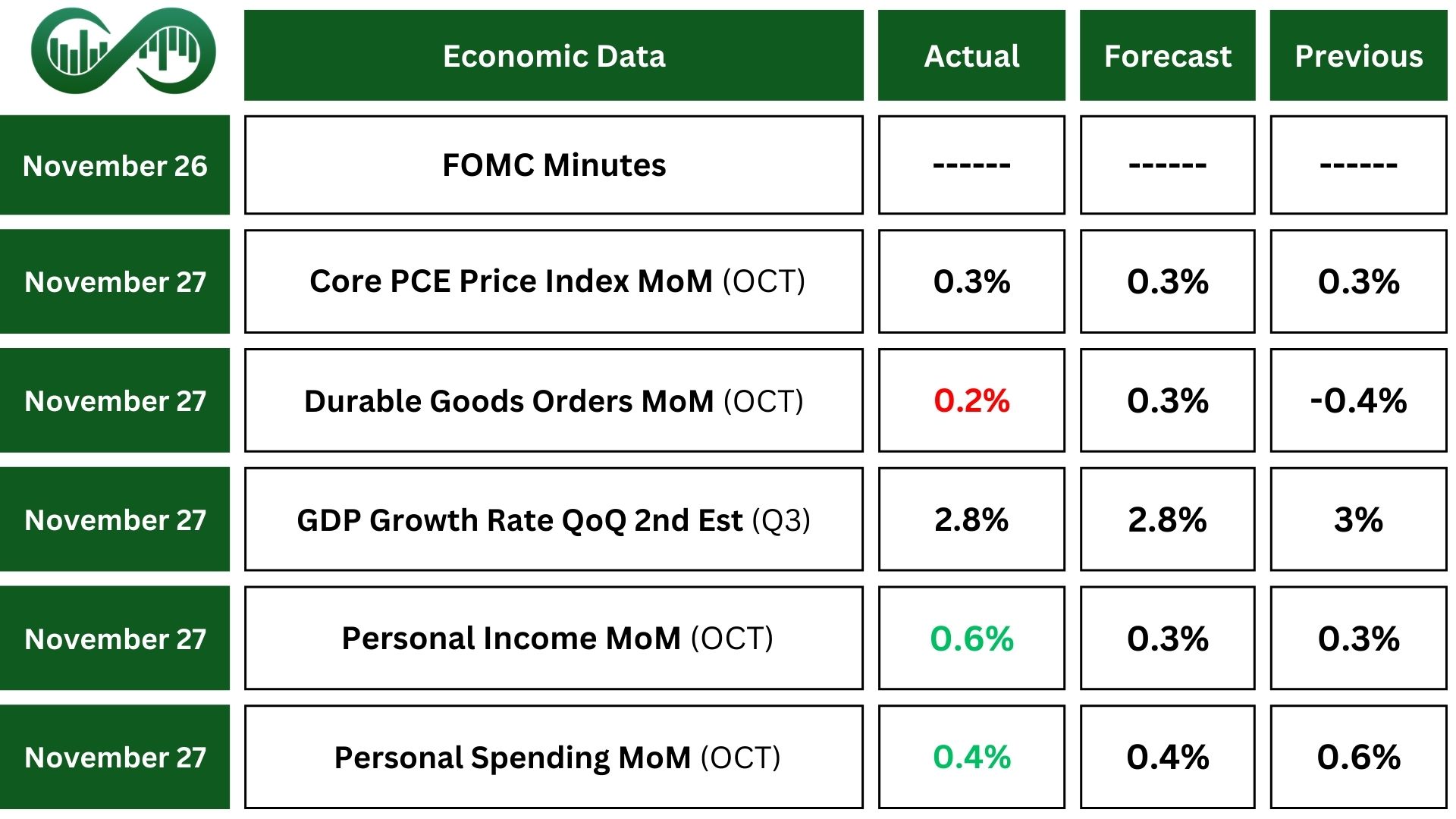

In the third quarter of 2024, the U.S. economy expanded with GDP growing at an annualized rate of 2.8%, following a 3.0% increase in the second quarter. This signals a healthy and expanding economy. Higher GDP growth can lead to increased consumer spending, benefiting companies.

In October, the overall PCE price index rose by 0.2%, and the core PCE price index, excluding food and energy, increased by 0.3%.

Year-over-year, the PCE price index rose by 2.3%, and the core PCE increased by 2.8%, indicating ongoing inflationary pressures.

Also, personal income in the U.S. increased 0.6% month over month with disposable personal income (DPI) rising by 0.7%. The rise in personal income suggests that consumers have more money to spend, which can boost economic growth. Higher disposable income can lead to increased consumer spending, driving demand for goods and services.

In October 2024, personal spending in the United States increased by 0.4% from the previous month. An increase in personal spending is a positive sign for the economy, as it indicates consumer confidence and contributes to GDP growth.

The good news is that personal spending is increasing at a slower rate than personal income. This is important because if spending grows faster than income, it can lead to more debt and potential financial instability.

Earning Reports

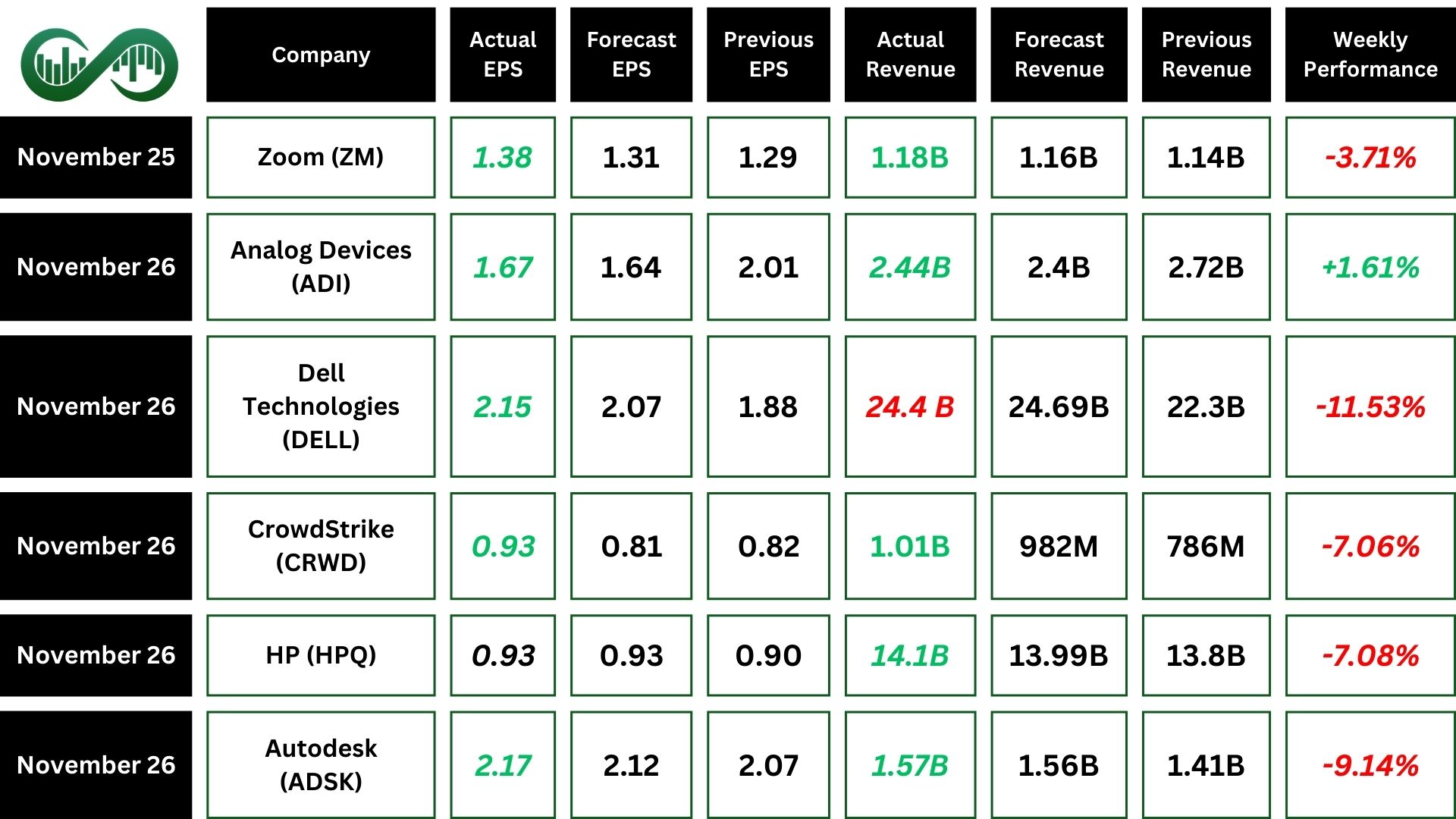

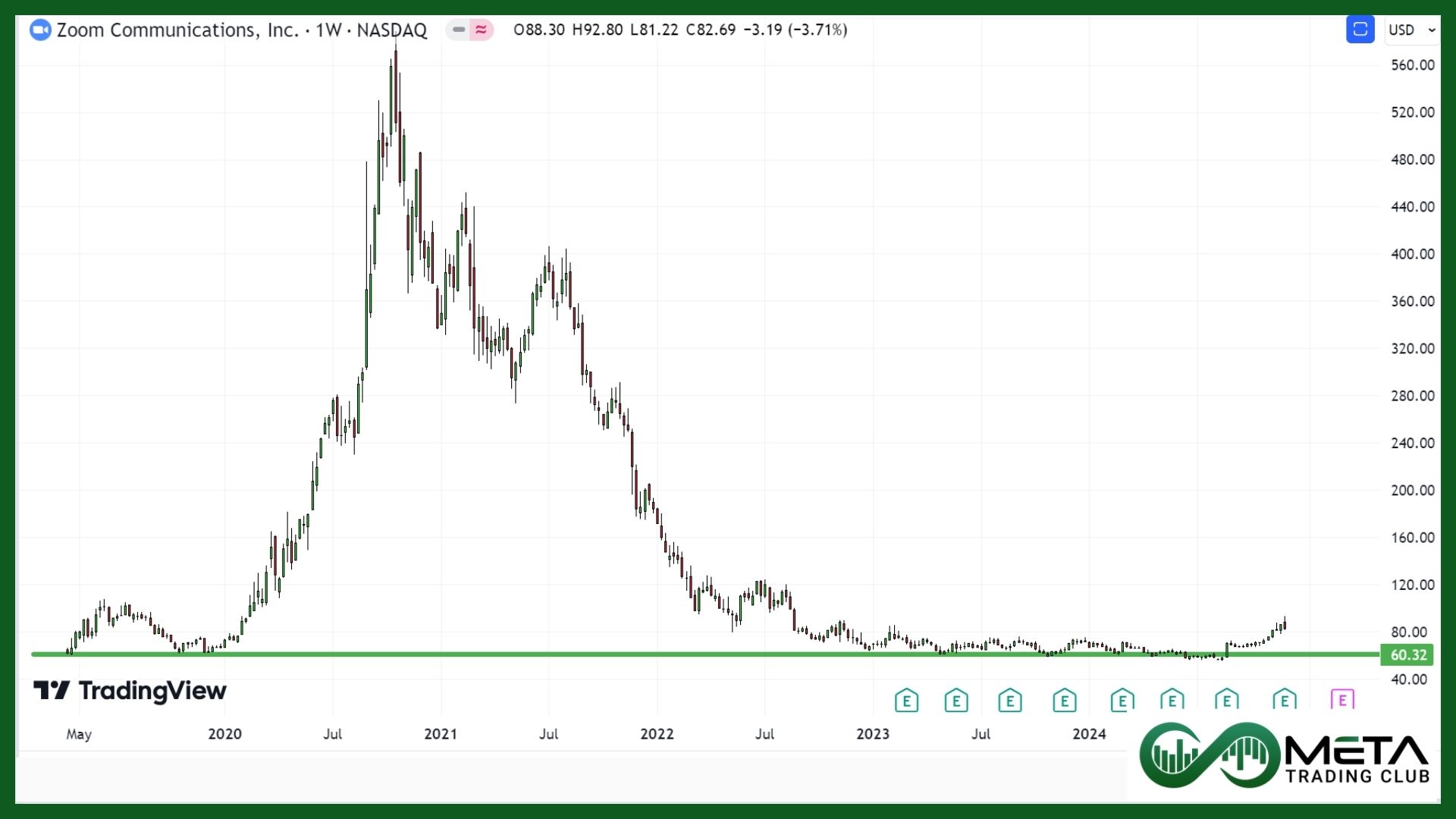

Zoom

Zoom (ZM) reported impressive Q3 2025 earnings, surpassing market expectations with a revenue surge to $1.18 billion, a 4% year-over-year growth. Also, the company reported a non-GAAP profit of $1.38 per share, exceeding estimates.

Additionally, Zoom introduced new features, including a premium Custom AI Companion and single-use webinar options for up to 1 million attendees. They also raised their full-year revenue forecast to between $4.656 billion and $4.661 billion, indicating strong confidence in continued growth.

While Zoom’s revenue grew by 4% year-over-year, this was a slower pace compared to previous quarters, raising concerns about future growth potential. Also, increased competition from other video conferencing platforms, like Cisco, put pressure on Zoom’s market share and growth prospects.

Dell

Dell Technologies (DELL) reported its Q3 2025 earnings with an EPS of $2.15, beating the estimates. The company’s revenue was $24.37 billion, which fell 10% from the same period last year, driven by a 33.8% increase in the Infrastructure Solutions Group. However, this revenue fell short of the estimate of $24.56 billion.

The Client Solutions Group saw a slight revenue decline, with the Consumer segment experiencing an 18.4% decrease year-over-year reflecting weak demand and profitability.

The unpredictability of AI shipments, especially with the transition to Nvidia’s new Blackwell chips, posed challenges for revenue forecasting.

CrowdStrike

CrowdStrike (CRWD) Q3 2025 earnings report showed strong financial performance with record revenue of $1.01 billion (a 29% increase year-over-year), an ARR exceeding $4 billion (up 27% year-over-year), and a robust gross margin of 78%, along with a 97% customer retention rate and $230.6 million in free cash flow (23% of revenue). Despite strong revenue growth, CrowdStrike reported a GAAP net loss of $0.07 per share.

Also, the company faced challenges, including a software update incident on July 19 that led to extended sales cycles and increased costs, resulting in an unexpected loss of $16.82 million. Additionally, a weaker-than-expected forecast caused a 6% drop in stock price, and the dollar-based net retention rate decreased to 115%.

Technically, CRWD is currently in a bullish trend, with a hidden divergence between the price and RSI that could cause the price to rise up to 377 or even further to the Fibonacci level around 387. This scenario remains valid as long as the price stays above 332.75.

However, if the price falls below 332.75 and breaks down the uptrend line, it could end the bullish trend and lead to a further decline in price, down to the next support zone around 295.

HP

HP (HPQ) reported positive results for Q4 of fiscal 2024, with a GAAP diluted net EPS of $0.93 and revenue of $14.1 billion, marking a 1.7% increase from the previous year and exceeding expectations.

They also announced a 5% dividend increase, showing confidence in future performance. However, the company’s full-year revenue of $53.6 billion showed a slight decline of 0.3%, reflecting a challenging market environment. Additionally, full-year net earnings decreased by 15% to $2.8 billion, and the non-GAAP operating margin slightly fell from 8.5% to 8.4%.

Autodesk

Autodesk (ADSK) reported its 3Q, 2025 with non-GAAP earnings of $2.17 per share, surpassing the estimate and improving 4.83% year-over-year. The company’s revenues were $1.57 billion, beating the expectations and growing 11% year-over-year. Growth was broad-based across products and regions in AEC and manufacturing, with strong renewal rates.

During the third quarter, Autodesk launched a new transaction model in Western Europe. Subscription revenues, making up 92.8% of total revenues, increased by 10.88% to $1.45 billion. Maintenance revenues, representing 0.57% of total revenues, declined by 25% to $9 million. Despite strong renewal rates, Autodesk faced challenges in growing new business.

Technically, ADSK price is currently in a bullish trend, with a support zone around $280. As long as the price stays above this support, it might rise up to 326 or even more up to its all-time high around $344. However, if the price falls below this support and breaks the uptrend line, it could signal the end of the bullish trend and potentially lead to further declines.

Indices

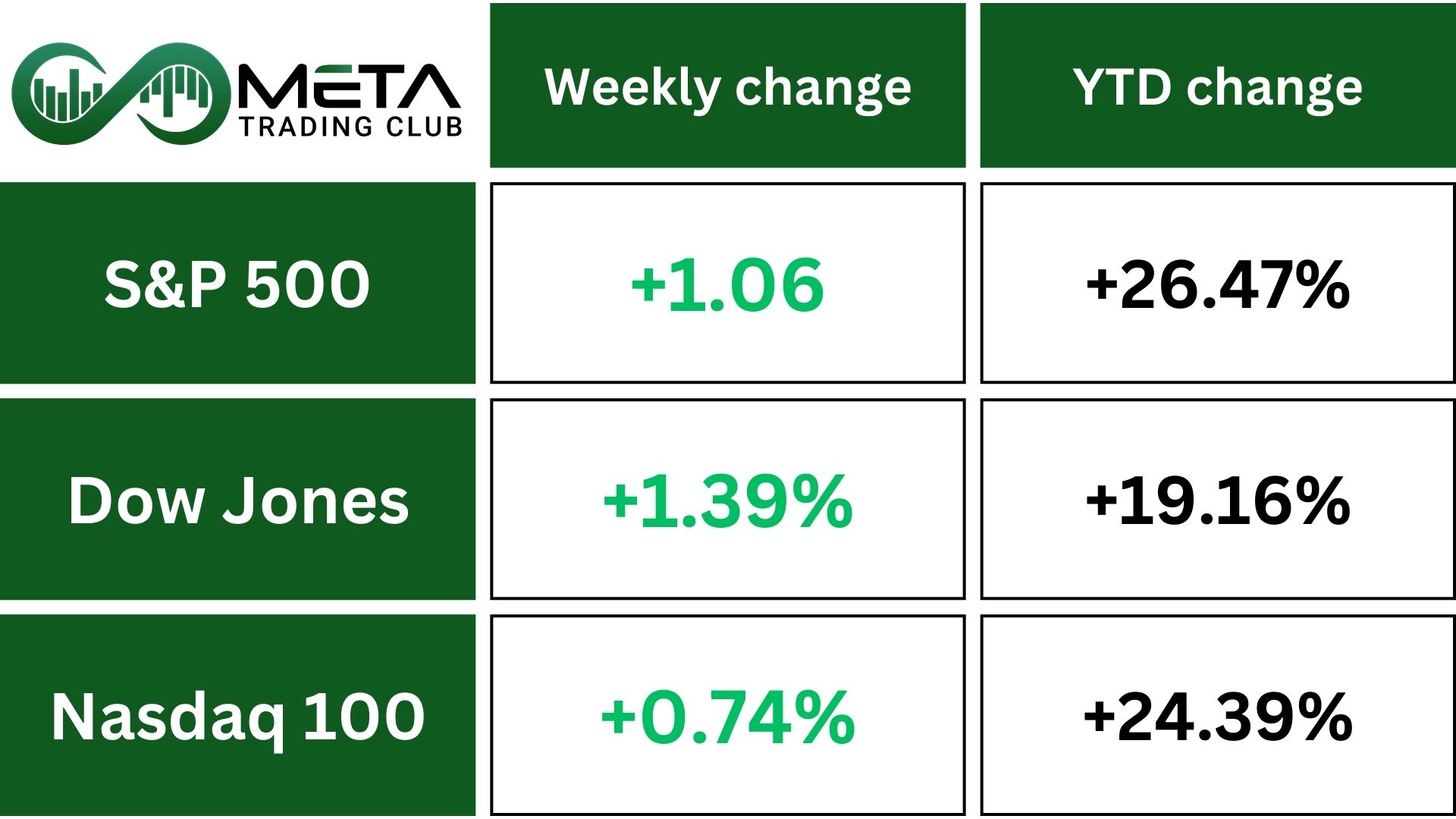

Indices’ Weekly Performance:

The Dow Jones Industrial Average and the S&P 500 hitting all-time highs is certainly a positive sign for investors. The gains in November across all three major indexes (Dow up 7.5%, Nasdaq up 6.2%, and S&P 500 up 5.7%) are impressive as well.

New tariffs and immigration policies could increase inflation. Strong economic data has led to speculation that the Federal Reserve will slow its pace of interest rate cuts. Traders are pricing in a 66% chance of a 25 basis point cut at the Fed’s December meeting.

Technically, SPX is currently below an important resistance level, which is a Fibonacci level of $6100. Also, the RSI, indicating weakness in momentum

If SPX rejects from this resistance it leads to a decline to around 5,870. The green rectangle marks a larger support zone, which is a critical area for the market to watch for future direction. However, if the index breaks upward through the resistance around 6,030 and remains above it, we might see further increases.

Stocks

Stock Market Sector’s Weekly Performance:

Source: Finviz

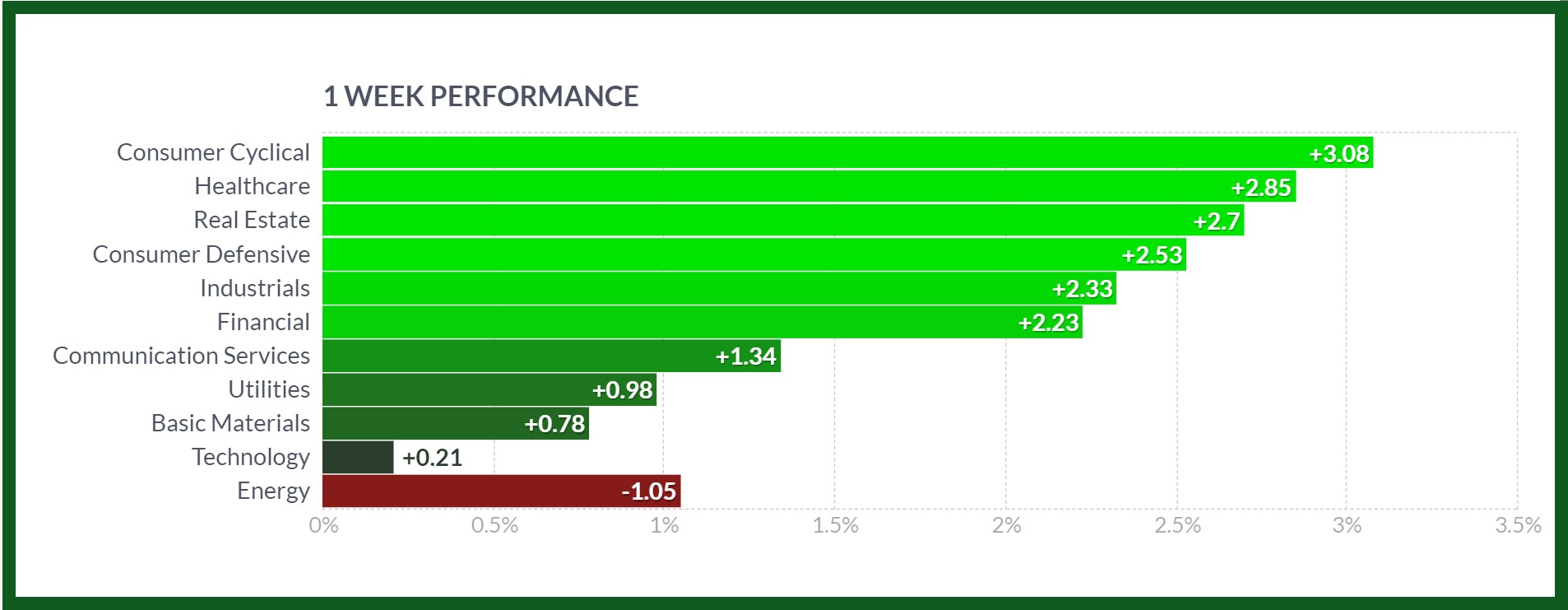

Last week’s sector performance:

- Consumer Cyclical: Boosted 3% by increased consumer spending and confidence.

- Healthcare: Rose 2.8%, driven by advancements in medical technology and successful drug trials.

- Real Estate: Up 2.7% influenced by high property demand and increase in building permits and home sales start.

- Consumer Defensive: Increased 2.5% as steady demand for essential goods for black Friday.

- Industrials: Rose 2.3% due to increased industrial production and infrastructure spending.

- Financial: Grow 2.23% due to favorable interest rates.

- Technology: Just increased 0.21%. Mixed performance due to drop in semiconductors and bounced back from Wednesday’s losses, boosting the Philadelphia SE Semiconductor Index.

- Energy: Fell 1.05% due to falling oil prices and decreased energy demand.

Stock Market Weekly Performance:

Source: Finviz

Global stocks soar, achieving their biggest monthly gains since May, fueled by Trump’s Wall Street surge.

Retailers import a lot of goods, and their profits and margins rely heavily on managing inventory levels. They are one of the industries most affected by tariffs.

However, the outlook for Black Friday and Cyber Monday sales is currently positive.

The news about Apple’s upcoming AI features for the iPhone 16 and the new tariffs on solar panel imports seem to have had a significant impact on their respective stocks.

Meanwhile, chip stocks bounced back from Wednesday’s losses, boosting the Philadelphia SE Semiconductor Index.

S&P 500 Top Gainers

Source: Tradingview

- Eli Lilly and Company (LLY): Surged 6.33% following its Florbetapir approved by UK regulator to test for Alzheimer’s disease.

- Ross Stores, Inc. (ROST): Rose 6% as the discount retailer lifted its full-year earnings outlook despite lower-than-expected fiscal Q3 sales amid softening consumer discretionary spending.

- Target (TGT): Increased 5.84% as shoppers spent $11.3M per minute online on Black Friday.

- Amazon (AMZN): Gained 5.46% due to increasing spending in black Friday and cyber Monday.

- Deere & Company (DE): Rose 4.3% as Farm Equipment industry, which Deere belongs, has gained 12% over last months.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold prices rose as the dollar and Treasury yields weakened following the U.S. holiday. After correcting from its October record high gold steadied and is now expected to benefit from a potential “Santa rally,” having risen in December for the past seven years.

Gold futures are currently stable, but the short-term outlook appears bearish.

As we can see on the XAUUSD chart, after breaking a major uptrend line, the price has begun ranging. Also there’s some weaknesses in momentum, as indicated by the RSI. We expect that the price will range between $2,600 and $2,700 for a while.

Crude oil fell to $72.13 a barrel, set for a weekly decline of over 3% as the Israel-Hezbollah ceasefire in Lebanon reduced supply concerns.

However, oil prices showed mixed movements early on Friday after OPEC+ decided to delay its planned meeting. The delay has created some uncertainty in the market as traders await decisions on production cuts.

We expect global inventories, reduced by OPEC+’s cuts, to rise in Q2 2025 due to increased supply from the U.S., Canada, and South America, coupled with weak demand growth.

Forex

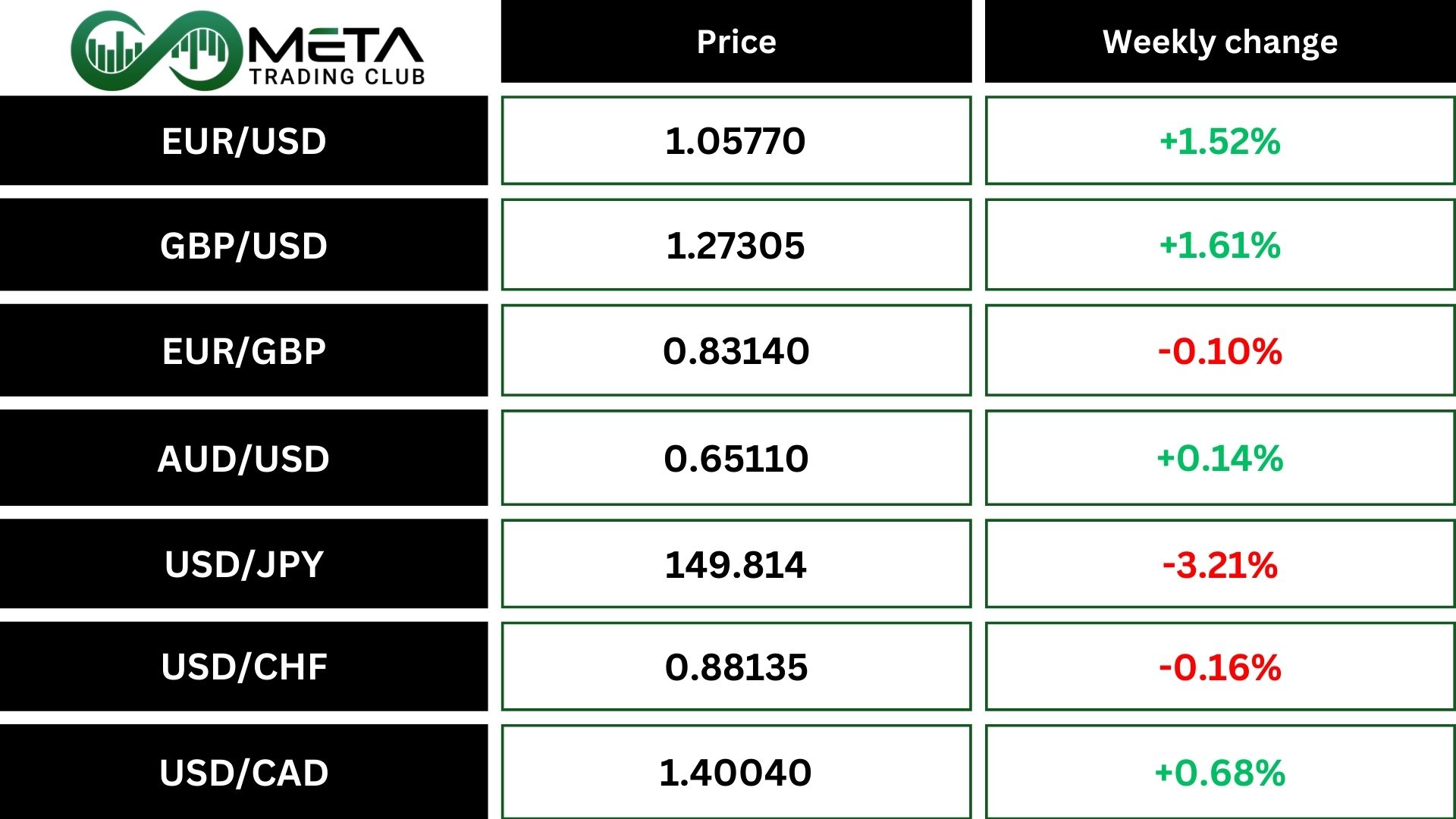

Weekly Performance of Major Foreign Exchange Pairs:

The yen surged to a six-week high against the dollar, driven by faster-than-expected inflation in Tokyo, which fueled expectations of a Bank of Japan interest rate hike next month. Tokyo’s core consumer price index rose 2.2% year-on-year in November, surpassing forecasts.

The dollar fell to 149.62 yen, marking a 3.21% weekly loss, the largest since July. The dollar index also declined, but it is still on track for a 1.59% rise in November due to expectations of pro-growth policies from the incoming U.S. administration.

The euro gained 1.5% for the week but is down 2.8% for November. French and German inflation data showed mixed results. ECB policymakers are divided on the need for further rate cuts.

Crypto

Crypto Market Weekly Performance:

Source: quantifycrypto

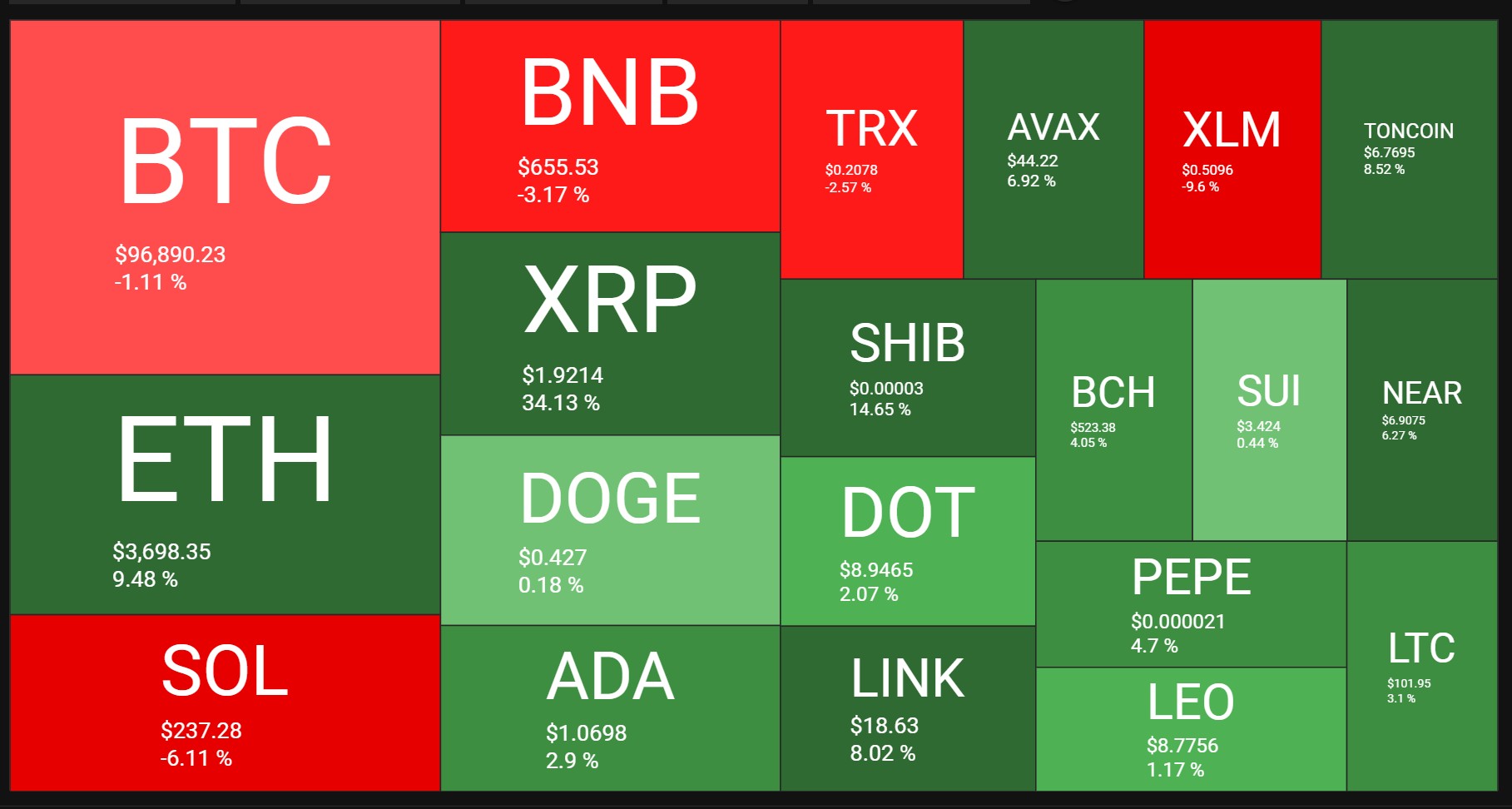

Bitcoin (BTCUSD) fell 1.1% last week but it attempts to recover its record high of $99,830 from a week ago. This month, the leading cryptocurrency is on track for a 39% increase. Also, this is its best performance since February which was driven by expectations of a more favorable regulatory environment under Trump.

The Bitcoin’s price is currently between its all-time high near $100,000 and a support area around $90,000. Weakness in momentum, indicated by the RSI, suggests the price may range between these two levels for a while. If the price breaks above $100,000, it could lead to further increases, but if it falls below $90,000, it might drop to around $85,000.

Shiba Inu (SHIB) could see a 75% increase if it maintains its current price level. The analysis suggests that SHIB is consolidating at a critical level, and a breakout above key resistance could drive significant gains.

The Ethereum price is currently below a dynamic resistance (down trend line) and a static resistance, both working from $3,800 to $4,000. If the price remains below these resistances, we expect it to range and consolidate. However, if the price can break these resistances upwardly and stays above $4,000, it might start a new bullish trend and rise up to its all-time high around $4,950 or even more.

Next Week’s Outlook

Economic Events

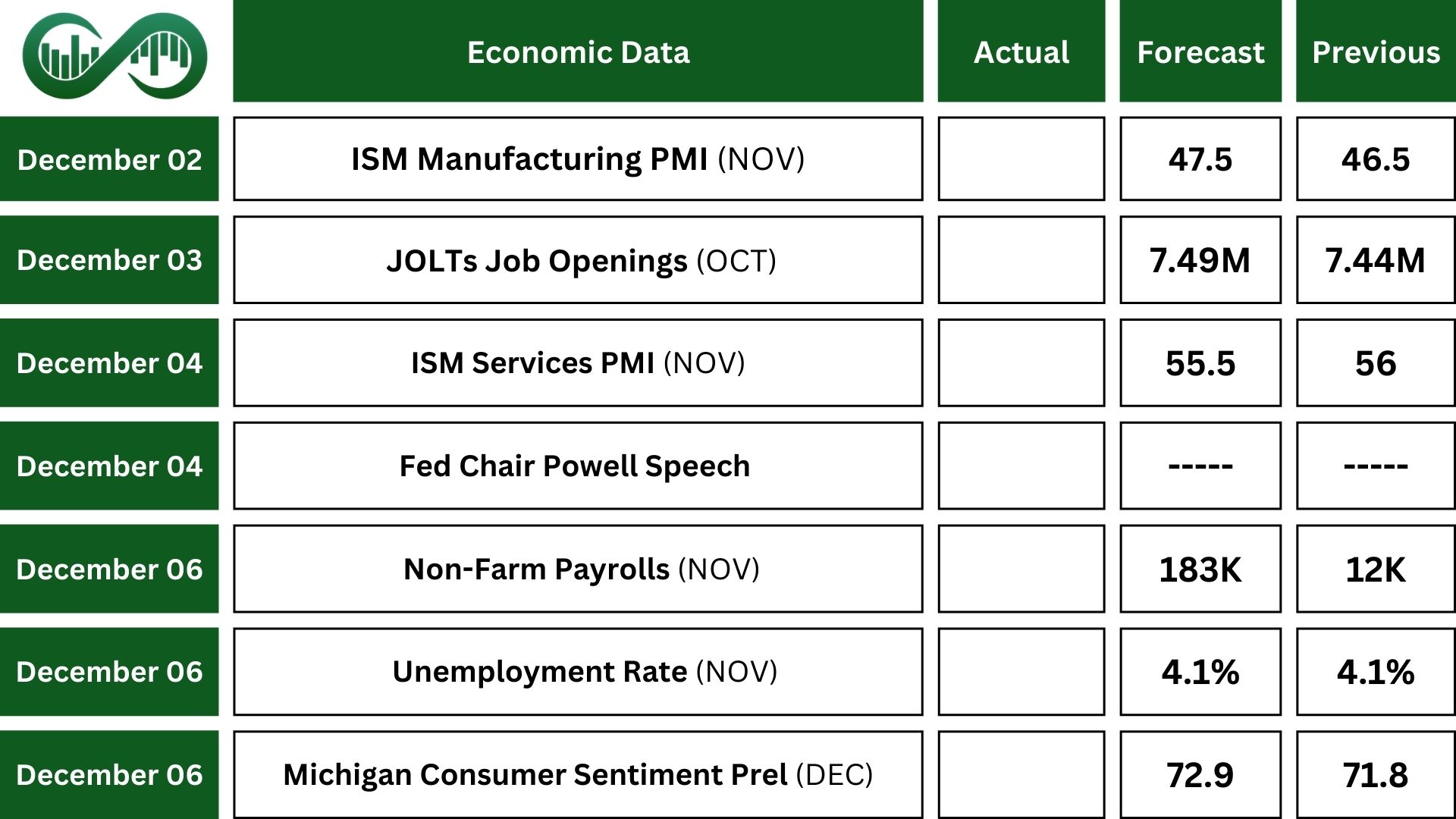

This week, the November jobs report will take center stage. The economy is projected to add 183K jobs, a significant improvement from the 12K added in October.

The unemployment rate is expected to hold steady at 4.1%, while wage growth is forecast to slow slightly to 0.3% from 0.4%.

Additionally, the ISM PMIs are due, with the services sector anticipated to see a slight slowdown and the manufacturing downturn likely showing signs of easing.

The JOLTS report is expected to reveal an increase in job openings to 7.49 million from 7.443 million.

Meanwhile, the Michigan consumer sentiment index is forecast to rise in December, and factory orders are likely to have rebounded in October with a 0.4% increase.

Other key indicators include final S&P Global PMIs, ADP employment figures, Challenger job cuts, consumer credit data, exports and imports, and construction spending.

Market participants will also closely watch appearances from several Fed officials, including Chair Powell at the New York Times DealBook Summit.

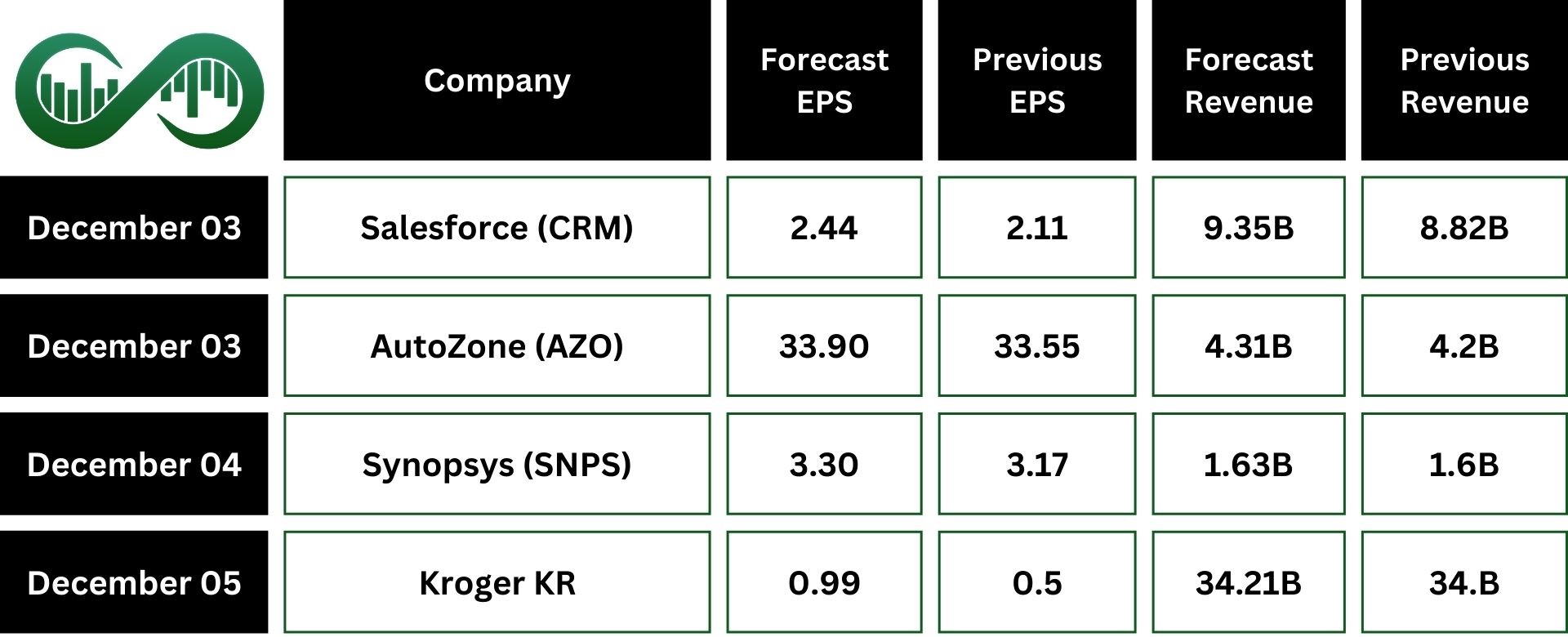

Earning Events

On the corporate side, major companies like SalesForce (CRM), AutoZone (AZO), Synopsys (SNPS) and Kroger (KR) will release their quarterly results.