Last Week’s Reports

Economic Reports

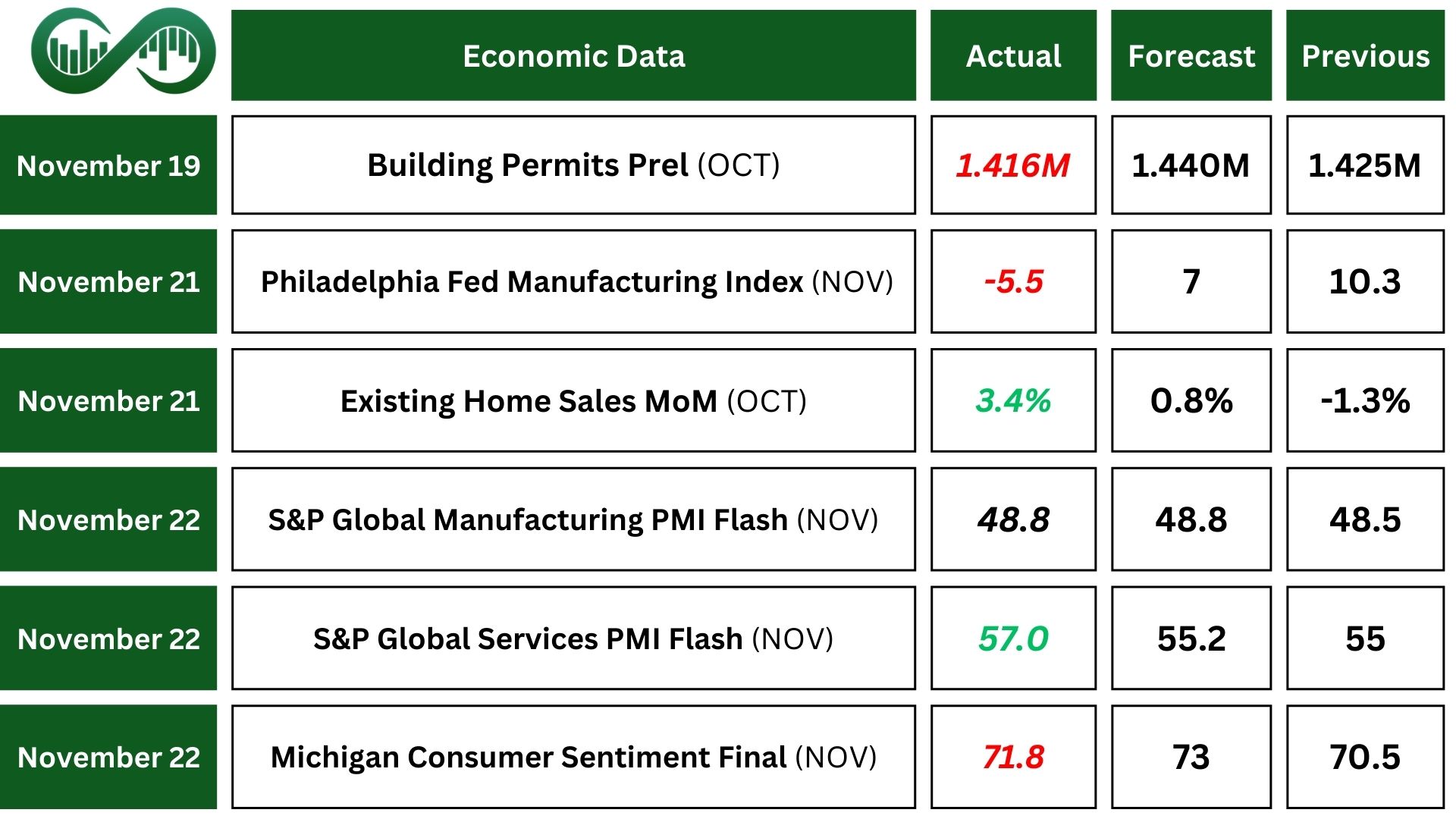

Building permits in the United States fell by 0.6% to an annual rate of 1.416 million in October. Fewer permits can result in a slower growth rate for new housing, potentially leading to higher housing prices due to limited supply.

The Philadelphia Fed Manufacturing Index dropped to -5.50 points in November, down from 10.30 points in October. This decline indicates a contraction in manufacturing activity in the Philadelphia region compared to the previous month.

The S&P Global US Composite PMI rose to 55.3 in November, up from 54.1 in October, preliminary data showed. This reading signaled robust expansion in the U.S. private sector, marking the strongest growth since April 2022.

The S&P Global Flash US Manufacturing PMI rose to 48.8 in November from 48.5 in October, matching market expectations.

The S&P Global US Services PMI rose to 57 in November from 55 in the previous month, well above market expectations and marking the sharpest expansion in the US services sector activity since March of 2022.

The University of Michigan Consumer Sentiment Index revised to 71.8 for November, slightly below the preliminary reading of 73. Also, year-ahead inflation expectations hold steady at 2.6%, long-run inflation expectations climbed to 3.2%, up from 3.0% the previous month, suggesting growing uncertainty about future inflation trends.

Earning Reports

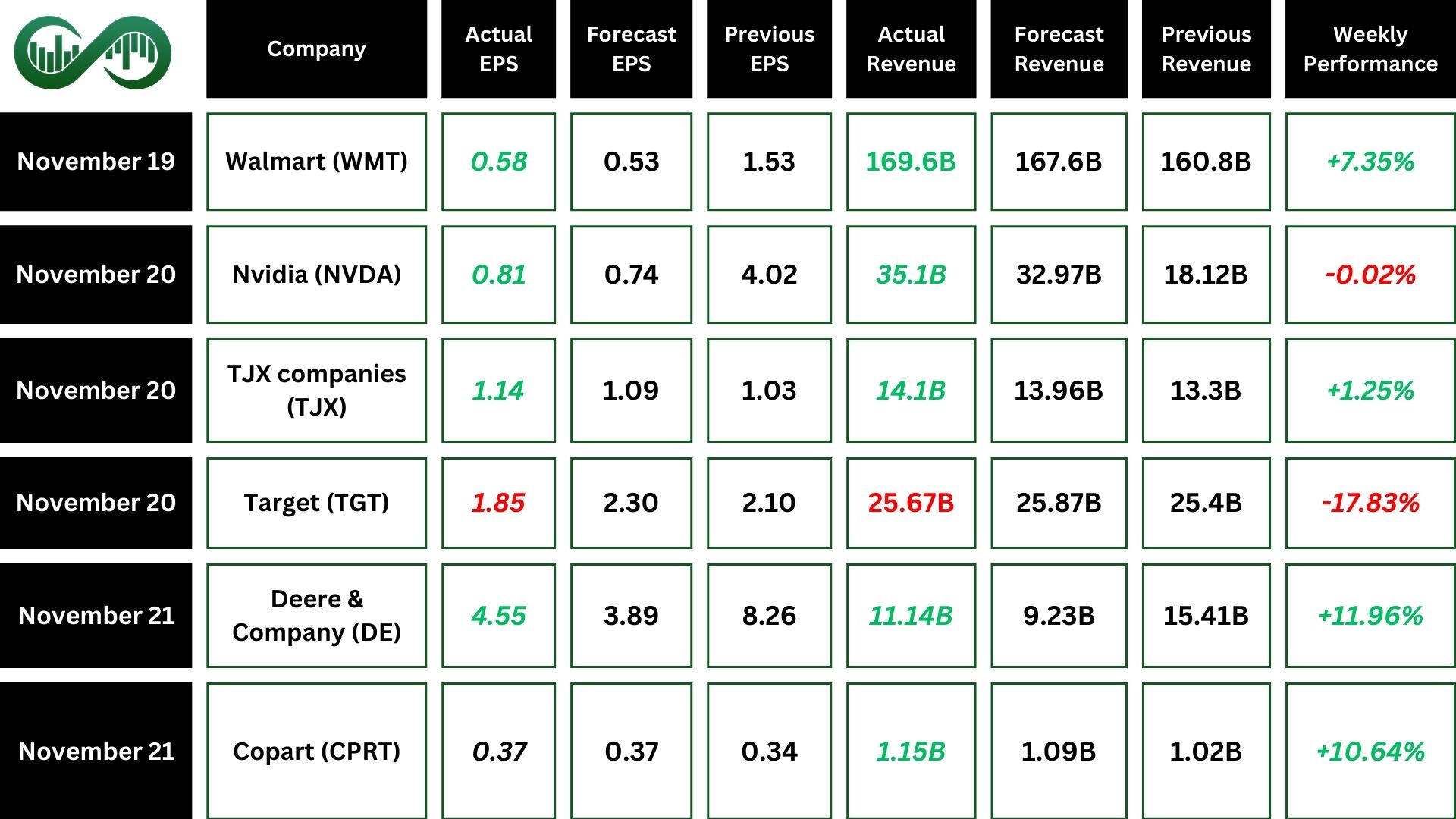

Walmart

In Q3 2024, Walmart (WMT) reported strong financial performance with consolidated revenue of $169.6 billion. This is a 5.5% increase in revenue which surpassed the forecasts.

The company also posted an adjusted EPS of $0.58, beating the expectations. Key drivers of earnings included a 5.3% increase in U.S. comparable sales, 27% growth in global eCommerce sales, and an 8.2% rise in operating income to $6.71 billion.

Walmart’s diversified strategy and strong market positioning contributed to robust revenue growth. Also, significant growth in eCommerce sales highlights the success of Walmart’s digital infrastructure investments. The company’s higher gross margins and growth in membership income supported profitability. Additionally, Walmart raised its full-year guidance, reflecting confidence in continued growth.

Target

In Q3 2024, Target (TGT) reported totalTarget reported total revenue of $25.7 billion, which was a 1.1% yearly increase. However, this fell short of the forecasts.

The company posted an EPS of $1.85, missing the forecasted EPS of $2.30. This represents a significant miss and resulted in a 20% decrease compared to the previous year. These are highlighting ongoing challenges in profitability and cost management

The beauty segment shows comparable sales growing by over 6%. This indicates successful strategic collaborations and high-demand cosmetics brands.

Despite the overall revenue miss, digital sales showed strong growth, emphasizing the importance of Target’s multi-channel retail strategy.

The price of Target Corporation (TGT) is currently in a bearish trend. There is a support zone between $90 and $100, which could create a significant ranging zone around this level and below the black downtrend line. However, if the price manages to break upward through the black downtrend line, it could lead to further price increases.

Nvidia

Nvidia (NVDA) showed an impressive performance in Q3 2025, with both revenue and EPS exceeding forecasts, driven by strong demand for their AI products.

Nvidia achieved a record quarterly revenue of $35.1 billion, up 17% from the previous quarter and 94% year-over-year.

Data center revenue reached $30.8 billion, up 112% year-over-year.

High demand for Nvidia’s Hopper and anticipation for the Blackwell AI chip contributed significantly to the growth.

Nvidia expects Q4 2025 revenue to be around $37.5 billion, with GAAP and non-GAAP gross margins expected to be 73.0% and 73.5%, respectively.

The price of NVIDIA (NVDA) remains in a bullish trend, although there are signs of weakening momentum that could lead to a decline toward the support zone around $130. As long as the price stays below its all-time high of around $153, this scenario is possible. However, if the price breaks upward through its all-time high and remains above it, it could lead to further increases.

Copart

Copart (CPRT) Q1 2025 results reflect strong revenue growth. The company exceeded revenue expectations achieving a 12.4% increase year-over-year. Also, the actual EPS was higher than forecasted by $0.02 per share.

Net income increased by 8.9%, gross profit rose by 10.4%, global service revenue increased by 15% and US insurance unit volume: grew by 12% year-over-year.

However, gross margin decreased to 44.7%, and facility-related costs increased by 22% due to hurricane responses.

The price of Copart Inc. (CPRT) is currently in a strong bullish trend, having recently broken above its all-time high and extended further. As long as the price remains above the key green support zones, the bullish trend will remain powerful. However, if the price falls back below these green support zones, it could signal potential further declines.

Deere & Company

Deere & Company (DE) reported a net income of $1.245 billion for Q4 2024, a significant decrease from the same quarter last year.

For the fiscal year 2024, net income was $7.1 billion, compared to $10.166 billion in fiscal year 2023.

Also, Deere & Company’s revenue fell short of the forecasted. The actual EPS was lower than the forecasted EPS.

The company faced significant market challenges, leading to a 28% decrease in quarterly revenue and a 16% decrease in annual revenue.

Despite the challenges, Deere & Company made strategic adjustments to align its operations with the current market environment.

The company projects net income for fiscal year 2025 to be in the range of $5 billion to $5.5 billion, reflecting cautious optimism.

Indices

Indices’ Weekly Performance:

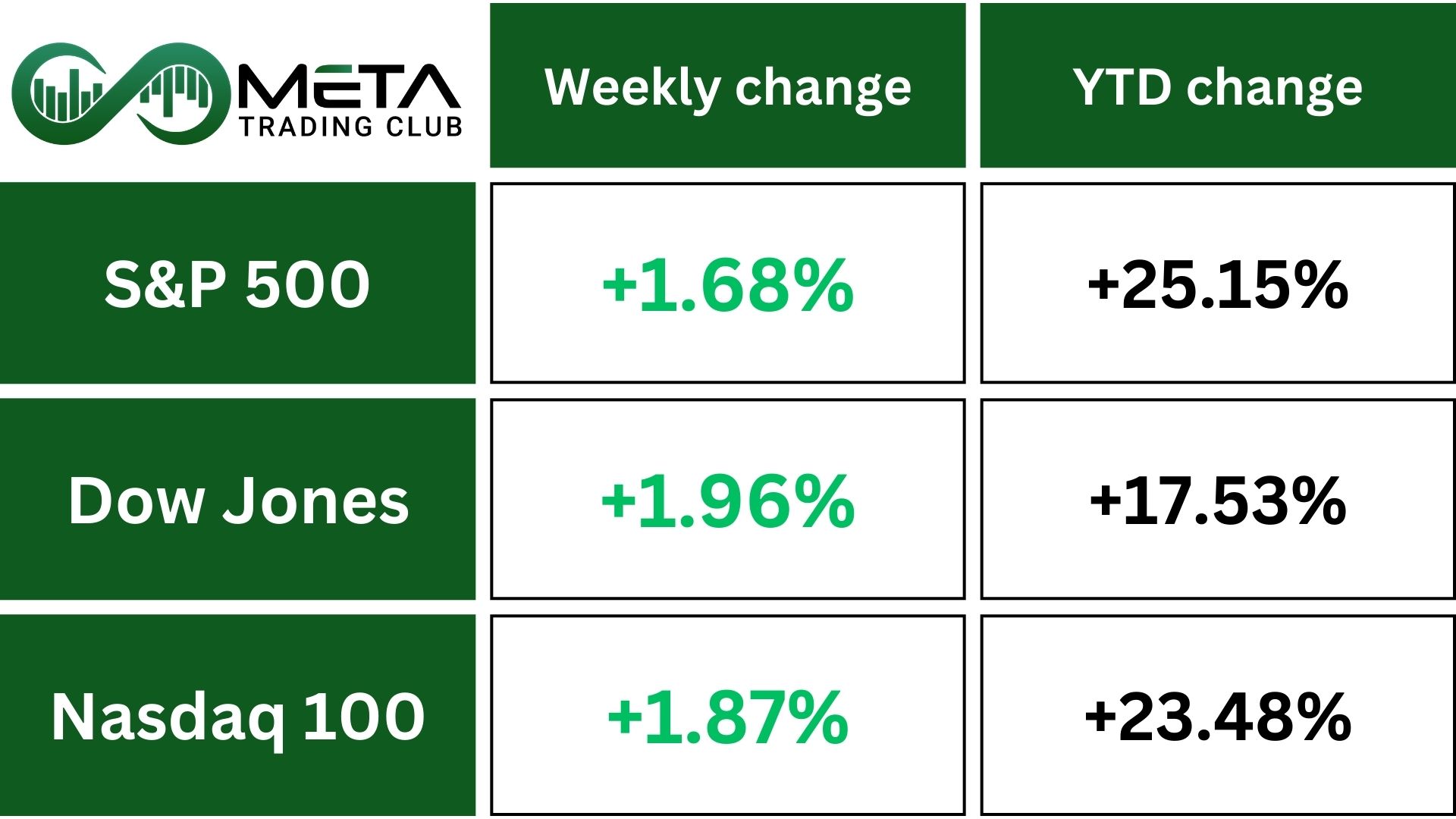

For the week, the S&P 500 and Nasdaq both rose by 1.7%, while the Dow increased by 2%. On Friday, the Dow Jones Industrial Average reached an all-time high.

The S&P 500 index has surged 31% over the past 12 months through Friday. The index SPX ended modestly higher at 5,969.34, just 0.5% below its record close on Nov. 11.

The potential policies from the Trump administration could shake things up. While deregulation should provide a “boost” for the market, “tariffs are a real concern,” she said.

The S&P 500 (SPX) has been in a bullish trend with two legs since March 2020, and we are currently at the end of the second leg, near an important Fibonacci level around 6100. The RSI shows some weakness in momentum. If the price stays below 6100 and the RSI continues to weaken, it could fall to Fibonacci retracement levels around 5450 (23.6%) or 5100 (38.2%).

Stocks

Stock Market Sector’s Weekly Performance:

Source: Finviz

Last week’s sector performance:

- Basic Materials, Consumer Defensive, and Energy sectors led the gains with a notable increase of 3.27% each.

- Industrials and Utilities also performed well, with gains of 3.11% and 2.77% respectively.

- The Real Estate and Technology sectors saw a rise of 2.43% each.

- The Healthcare sector increased by 2.04%.

- Financials and Consumer Cyclical sectors had modest gains of 1.75% and 1.62% respectively.

- The Communication Services sector had the smallest gain of 0.16%.

Overall, the market showed a positive trend with most sectors posting gains, reflecting investor confidence and a favorable economic outlook.

Stock Market Weekly Performance:

Source: Finviz

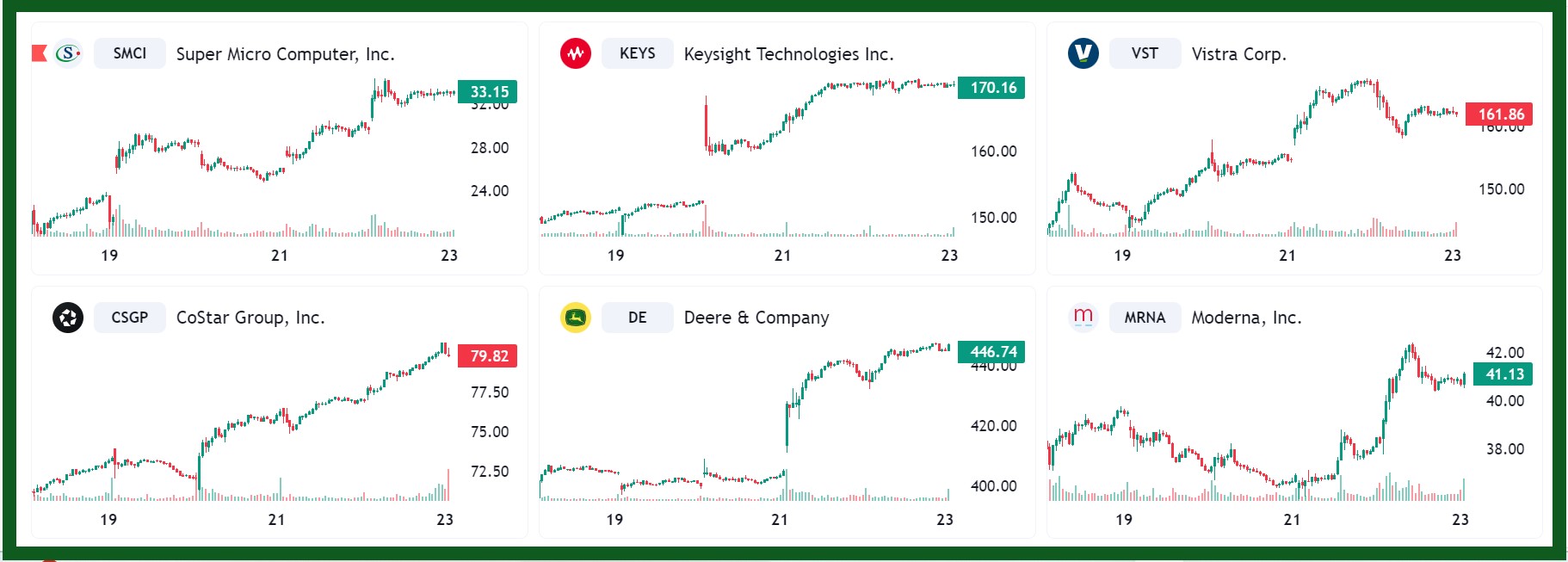

S&P 500 Top Gainers

Source:Tradingview

- Super Micro Computer (SMCI): Rose +78.42% said it submitted a compliance plan to the Nasdaq after receiving a notification letter that it was not in compliance with the Nasdaq’s timely filing rule.

- Keysight Technologies (KEYS): Increased +14.00% after the company issued an upbeat fiscal first-quarter outlook and reported better-than-expected results for the preceding three-month period.

- Vistra (VST): Up +13.91% owing to strong financial performance and advancements in technology.

- Deere & Company (DE): Increased +11.96% driven by strong quarterly earnings.

- Moderna (MRNA): Rose +11.56% due to positive news related to its COVID-19 vaccine and strong financial performance.

- Copart (CPRT): Gained +10.64% owing to strong fiscal performance.

- CrowdStrike Holdings (CRWD): Rose +10.54% with a growth strategy centered on becoming the one-stop solution for all enterprise cybersecurity needs through platform expansion.

- Tesla (TSLA): Up +9.93% driven by following reports about Trump’s plan for autonomous vehicle regulation.

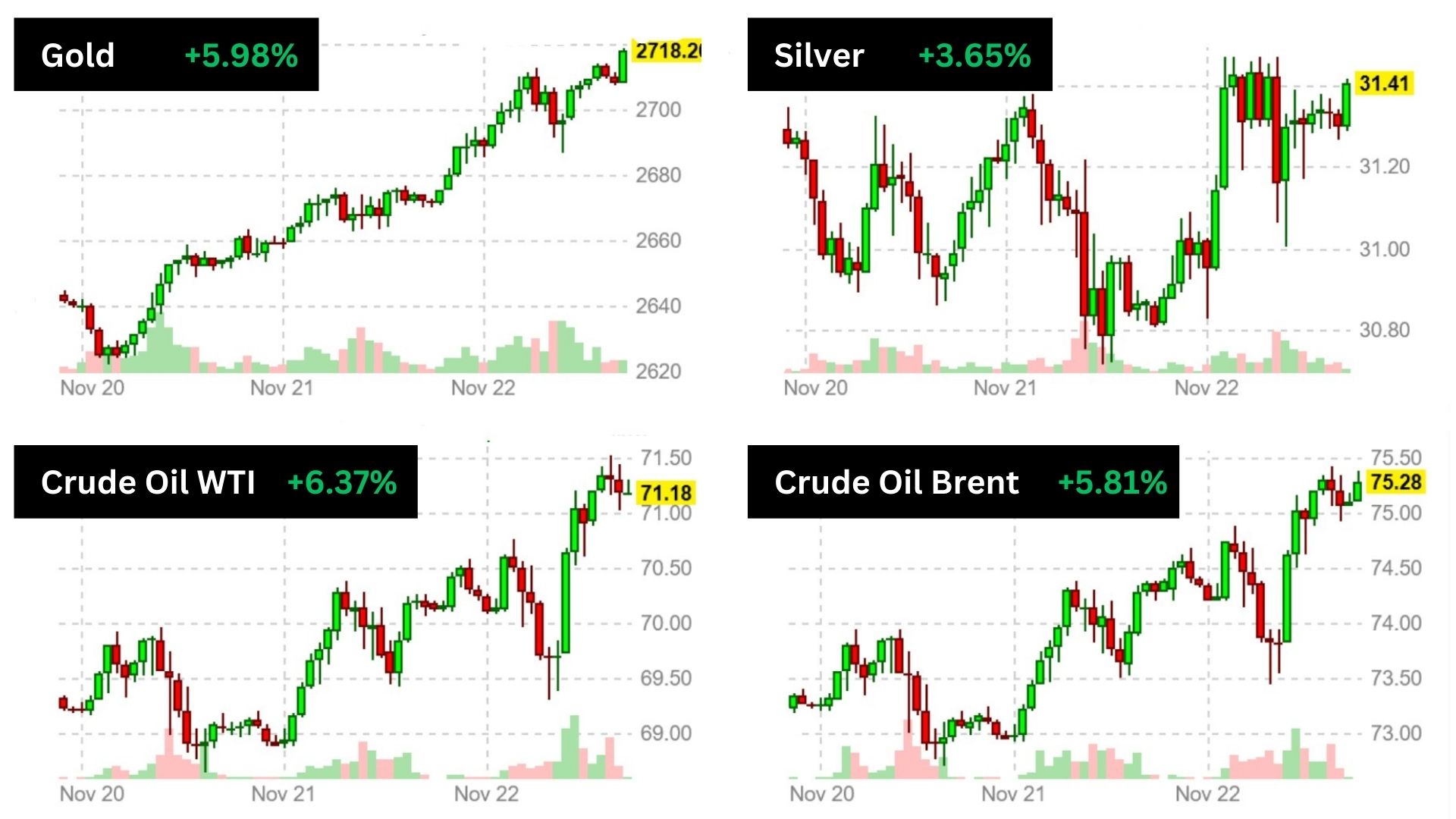

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Source: Finviz

Gold prices were set to achieve a more than 5% weekly gain as intensified missile attacks between Russia and Ukraine increased demand for safe-haven assets. These gains underscored gold’s role as a preferred hedge against geopolitical tensions.

Crude oil prices secured weekly gains of over 5% amid escalating geopolitical tensions, particularly between Russia and Ukraine. The conflict has raised concerns about potential disruptions in oil supply, driving prices higher. Additionally, Iran’s decision to increase its nuclear fuel-making capacity has added to market uncertainties, further boosting crude prices.

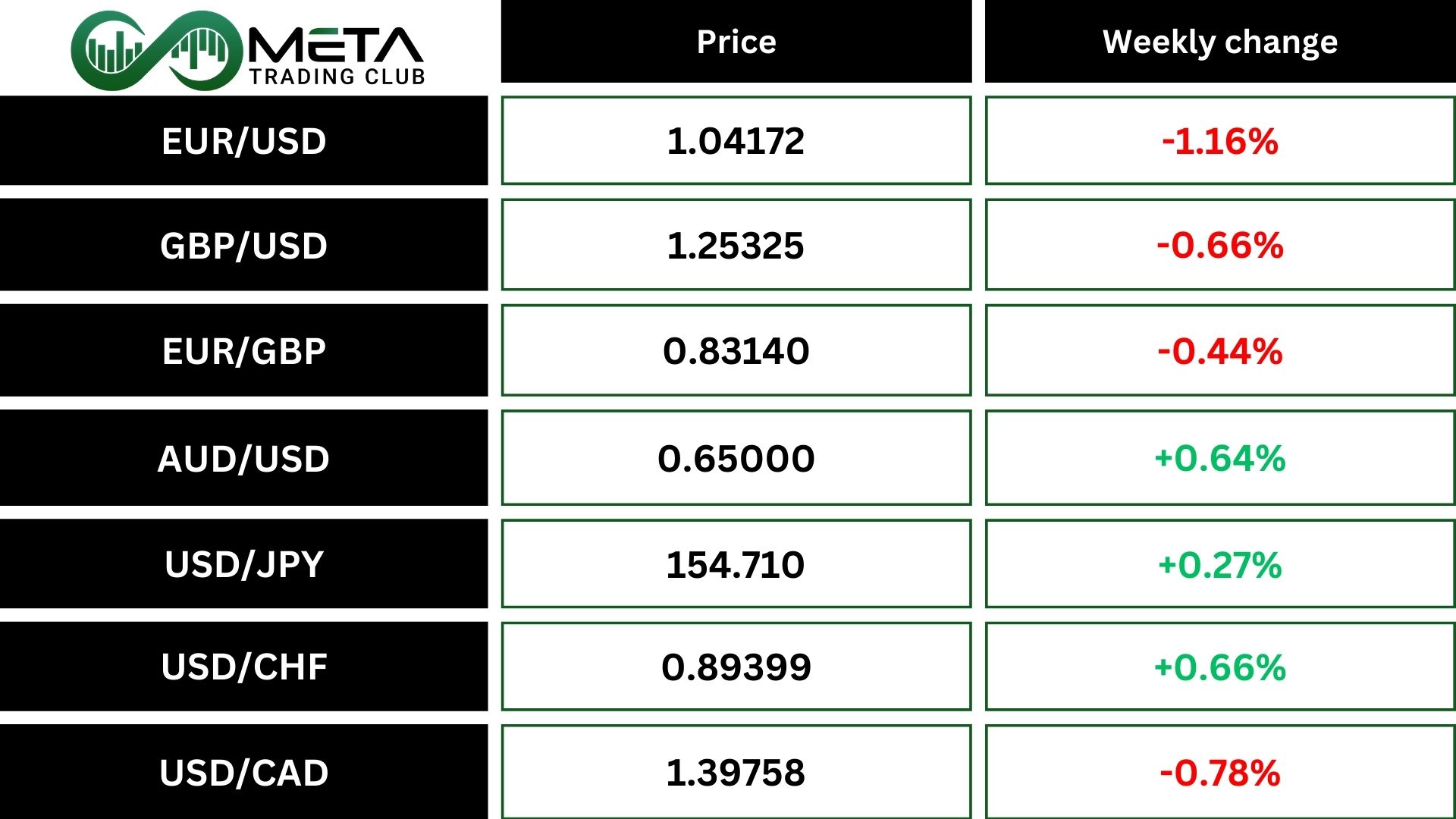

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The US Dollar saw significant strength, reaching a fresh yearly high, which weakened European currencies like the Euro and British Pound. Also, currencies like the Japanese Yen gained on geopolitical fears.

The dollar’s strength has also pushed the euro to its lowest level since 2022. Solid US economic data and a decline in euro-area business activity have bolstered the dollar further. This surge is accompanied by gains in US Treasuries, with yields moving away from recent highs.

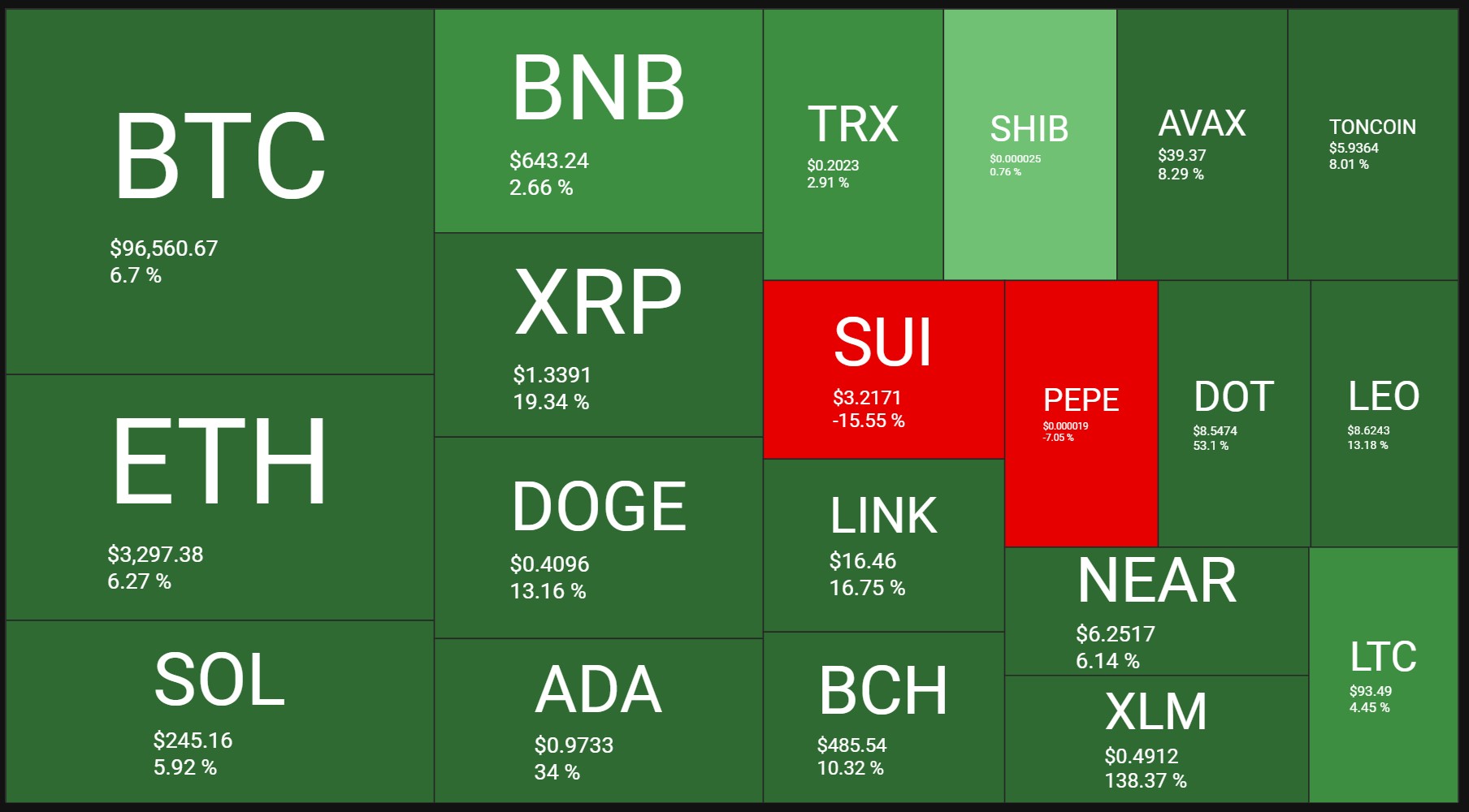

Crypto

Crypto Market Weekly Performance:

Source: quantifycrypto

Cardano (ADA) has surged over 200% in the past three weeks, reaching a 2.5-year high. Cardano (ADA) saw impressive weekly gains of over 38%, driven by increased market demand and positive sentiment. This surge highlights the growing interest and confidence in Cardano’s potential within the cryptocurrency market.

After an accumulation phase since November 2022, by breaking above 0.80, the price of ADA/USDT is now in a bullish trend. There are two important resistance zones around 1.25 and 1.60. As long as the price stays above 0.80, it can rise to these resistance zones as targets.

Bitcoin Spot ETFs have had an exciting week, with a significant surge in inflows. BlackRock’s IBIT ETF notably achieved a record-breaking $513 million single-day inflow. The total net asset value of Bitcoin Spot ETFs has now reached $107.488 billion, highlighting their growing dominance in the crypto ETF space. Additionally, major Bitcoin holders like MicroStrategy and Metaplanet are expanding their BTC reserves amid ongoing macroeconomic uncertainties.

Bitcoin is currently experiencing an uptrend, but there is some momentum weakness indicated by the RSI. It seems likely that Bitcoin will continue its upward movement through shallow price corrections and time corrections, while maintaining its support levels. The $100,000 mark is expected to be a psychological barrier for traders, and a correction may occur around this level. As long as the price stays above the support zones, targets based on Fibonacci levels around $107,000 are achievable.

Next Week’s Outlook

Economic Events

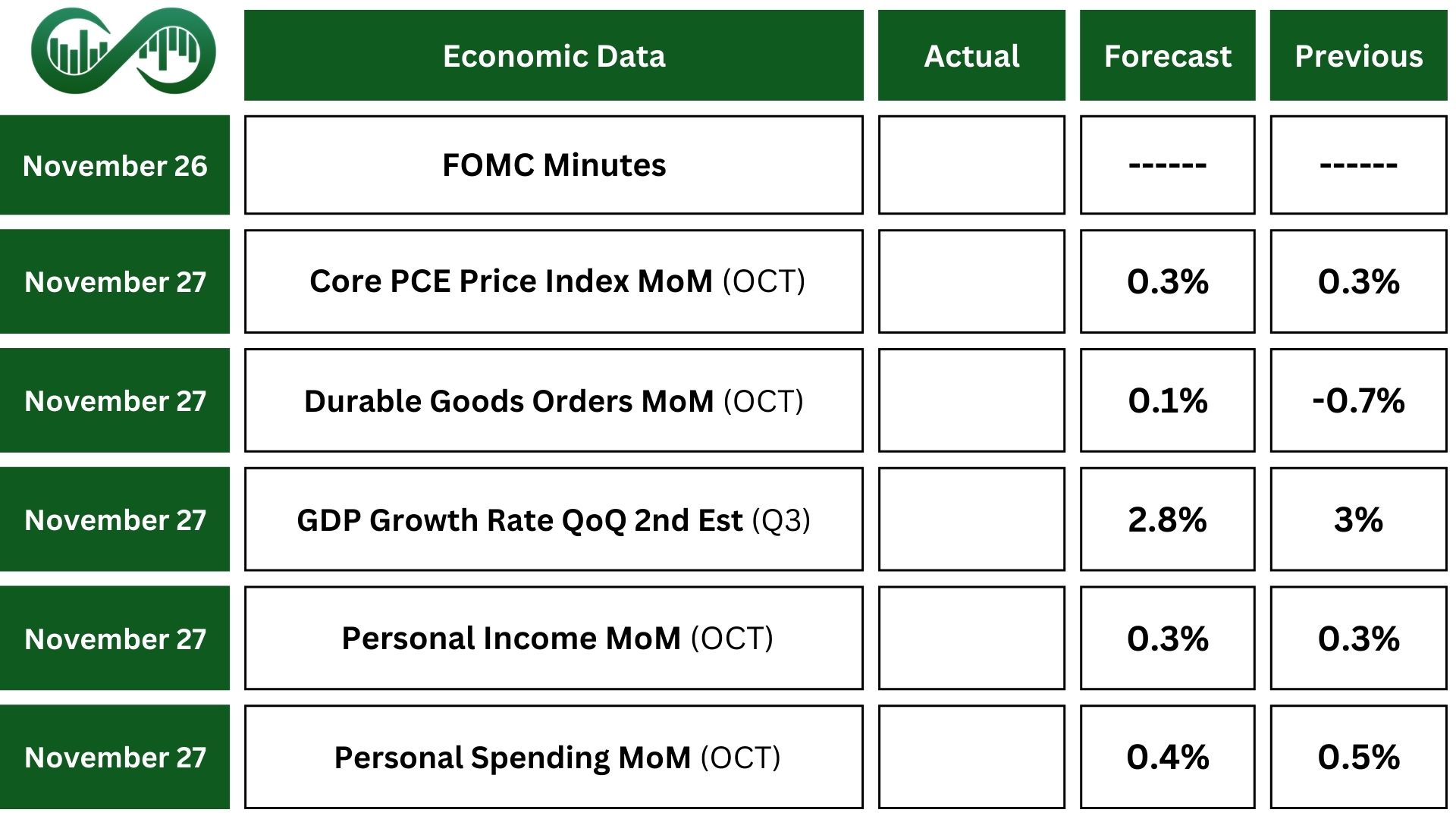

Next week in the US, FOMC minutes will be released on Tuesday.

The PCE report for October is expected to show a 0.2% increase, the same as in September, with core PCE steady at 0.3%.

Personal income is forecasted to rise by 0.3% and personal spending by 0.4%, a bit less than September’s 0.5% increase.

The second estimate of Q3 GDP is expected to confirm a 2.8% growth.

Durable goods orders might rise by 0.1%. Other important releases include corporate profits, wholesale inventories, various Fed indexes, house prices, consumer confidence, and home sales.

Earning Events

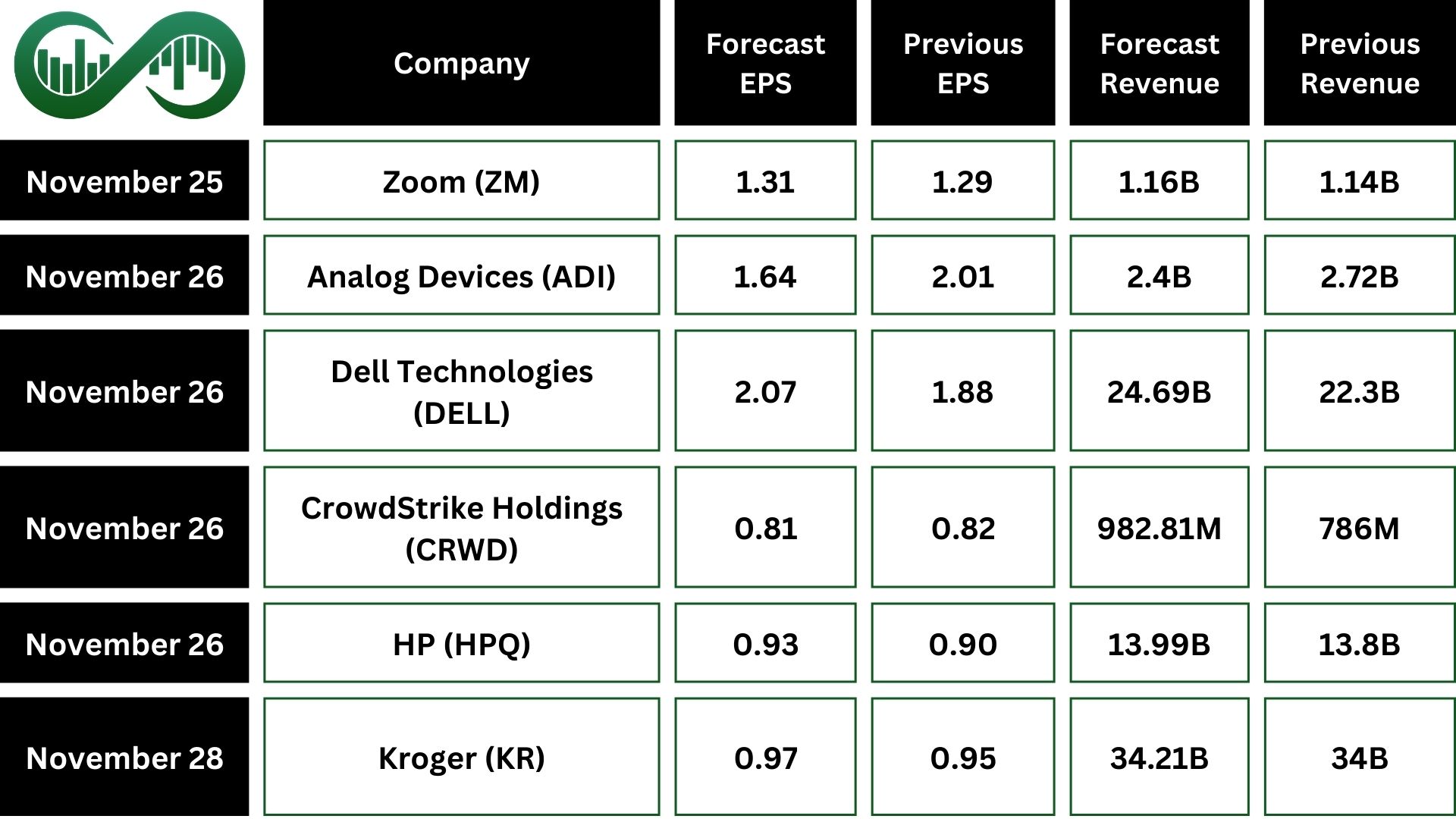

On the corporate side, major companies like Dell, HP, Zoom, Best buy, CrowdStrike, and Kroger will release their quarterly results.